ETP inflows again commandeered the gold investment market in Q3. Demand for bars and coins was, almost without exception, weaker across all markets.

Investment demand in Q3 totaled 335.7t, 44% up year-on-year and 8% above the five-year quarterly average demand for the sector of 311.4t. Year-to-date investment reached a record of 1,389.2t, 10% above the previous Q1–Q3 high of 1,268.5t from 2010.

The motives behind, and geographical distribution of, inflows into ETPs are discussed in detail in Key themes. Momentum behind these inflows has tapered off slightly, but Q4 has still seen marginal inflows. In the context of a 10% fall in the price, this highlights that price momentum is secondary to the strategic motives underpinning investment. Overall, we maintain a positive outlook on the sector, particularly given the fragile macroeconomic backdrop, such as negative interest rates and geopolitical risks.

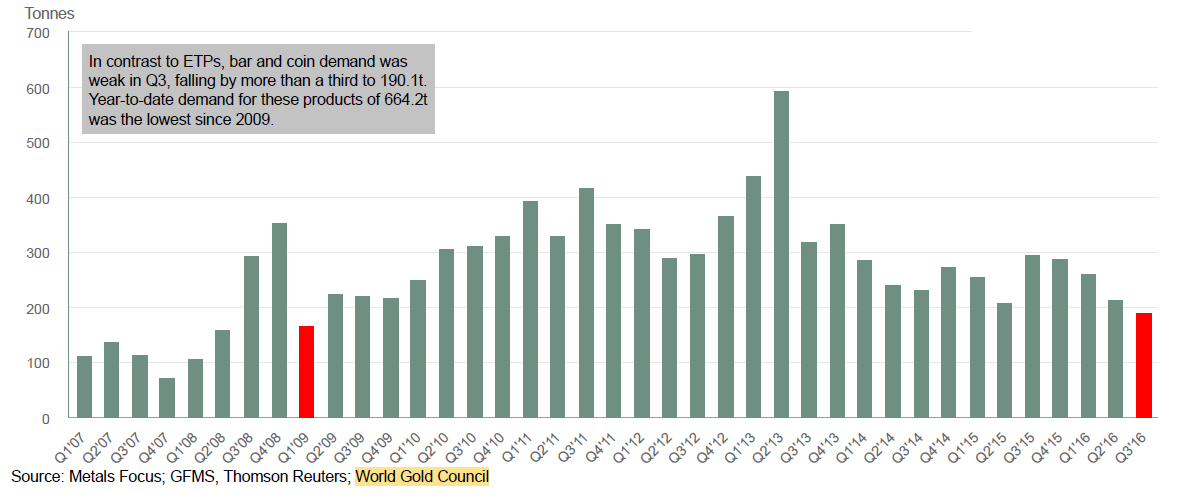

Bar and coin demand was contrastingly weak in Q3, falling by more than a third to 190.1t. Year-to-date demand for these products of 664.2t was the lowest since 2009. The high gold prices that were a major cause of weakness in the jewellery sector were similarly off-putting for investors, and the lack of momentum in the price during the quarter was a further deterrent. Market research shows that investors look for a low, or rising, gold price as a signal to buy – both of which were notably absent in the third quarter. But the price drop in the opening weeks of Q4 has provoked a response in some markets. Our Focus Box ‘Q4 Update: impact of prices on consumer demand’ provides further detail on investors’ perceptions of – and reactions to – recent price moves.

Chart 8: Retail investment demand has been weak

- Year-to-date retail investment demand for bars and coins is at its lowest level since 2009.

- High gold prices were a major cause of weakness across most markets. Weak demand in India was compounded by the government’s focus on curbing cash transactions.

- Demand may improve in Q4; the price drop in the first week of October resulted in an uptick in retail investor interest in the US, India and China.

Indian bar and coin demand very weak in 2016 to date; Q4 holds better prospects

Investment demand fell for the third consecutive quarter in India, down 30% to 40.1t. At just 100.7t, year-to-date

demand for bars and coins is the lowest for 12 years, below that even of 2009 when the first quarter saw negative investment for the only time in our time series. Investors already reluctant to buy at such persistently high gold prices, were also put off by the government’s focus on curbing cash transactions. Demand for gold bars was more greatly affected by the measures than that for gold coins, as cash remains one of the primary means of purchasing gold bars. Surging stock markets bumped gold further out of the spotlight.

Despite the depressed market, there is a growing market for branded gold coins in India, which – going forward – should support investment demand in India. The Indian Gold Coin, from MMTC has sold 185kg since its launch in November 2015 and is currently available through around 300 outlets. Similarly, the Tola Coin will appeal to customers who look for purity and brand. In another move, IBJA launched a personalised coin this festival season. IBJA has launched a store in Mumbai and wants to set up 100 stores in the next three years. Our report ‘India’s gold investment evolution’, produced in conjunction with MMTC, takes a detailed look at the market for branded gold coins in India.

European investment sank to an 8-year low, but net demand masks underlying activity

Europe’s bar and coin market failed to replicate the flows pouring into ETPs in the region. Investment in bars and coins fell to an 8year low of 37.6t in Q3, down 37% from the same period last year. The year-on-year decline is all the more marked for the fact that Q3 2015 was the strongest third quarter for four years, as investors responded to the falling gold price. Nevertheless, bar and coin demand during the most recent quarter was unarguably anaemic – 38% below the five-year quarterly average of 61.1t.

The weakness is largely reflective of a sharp bout of selling in July. This was triggered by the jump in the gold price – the short-lived response to the UK’s Brexit vote – which saw the euro-denominated gold price reach three year highs. The price based in sterling was even more marked, due to the selloff in the pound in the immediate wake of the referendum.

On the face of it, the 11% decline in UK bar and coin demand seems to indicate that investors in that market were inactive. This was far from the case. Gross levels of both buying and selling were elevated during the quarter, indicating a heightened level of activity in trading gold bars and coins. The two sides largely cancelled each other out, creating net demand of just 2.4t for the quarter. This pattern was repeated across the region: selling back of existing holdings swelled the stock of bars and coins available for purchase in the secondary market. This helps to explain depressed sales of newly minted coins.

The focus among French investors on selling into the price rally, resulted in a second consecutive quarter of net negative investment. Year-to-date investment is marginally negative at 0.2t. A negative fourth quarter would result in annual disinvestment in France for the first time since 2008, prior to the global financial crisis.

For Q1–Q3, demand is 14% down on 2015 and consequently Europe has slipped to second place in market size: on a year-to-date basis, China’s bar and coin market is the world’s largest.

Bar and coin investment still weak in China; funds diverted to ETPs

Retail investment in China stabilized after the washout of the preceding quarter, but the decline from 2015 levels was acute. Q3 demand of 41t – down 23% – equated to a year-to-date total of 162.5t, almost bang in line with last year.

Bar and coin purchases from commercial banks and large retailer chains dropped sharply in the third quarter: data from a couple of commercial banks show sales of gold falling by, on average, 50% year-on-year. GAPs saw net redemptions as the 2year high in the price in early July prompted a spike in liquidations.

The decline in demand was partially offset by direct individual withdrawals from the SGE, which remained elevated – many multiples of the withdrawals in Q3 2015. But more permanent attrition resulted from investors diverting funds to ETPs. Lower transaction costs and the introduction of online platforms and mobile applications offering access to ETPs with minimal entry requirements attracted many erstwhile bar and coin investors.

As well as a reticence to buy gold at high price levels, lower disposable incomes were a key factor underlying the weak demand picture.The sluggish economy, lower take home incomes and rising housing outlays have fostered a desire among Chinese households to build a cash buffer. The pressure of rising real estate prices on disposable incomes is a function of the degree to which property is used as an avenue for investment in China. Research by Knight Frank, in constructing their Prime International Residential Index, put Shanghai as the third fastest growing property market globally.

The fourth quarter has started on a more positive note in China, thanks to the price drop in early October. Consumers were swift to respond to lower prices and remain alert to any further buying opportunities.

Heightened price sensitivity still a feature of the US market

US demand for gold bars and coins almost halved from Q3 2016, down 43% to 17.4t. The year-on-year comparison in US investment was never going to be easy; Q3 2015 was an exceptional quarter which saw demand jump as the gold price dipped. Putting the recent quarter into context, it is 5% stronger than the five year quarterly average of 16.6t. And year-to-date demand is 14% ahead of last year at 62.8t.

Indicative of the fact that US retail investors remain keenly aware of price fluctuations in gold, September saw a surge in sales as bargain hunting emerged on the dip down in prices towards US$1,300/oz. And October has continued in similar fashion, with sales of Eagle coins surging thanks to the weaker gold price.

Middle Eastern investment sinks to record low

Paltry levels of Middle Eastern demand were largely a function of weakness in Iran. This is partly due to a downwards revision in our data series to reflect a shift from investment to jewellery purchases amid a dearth of newly minted gold coins: indeed, the market faced net disinvestment in the face of high gold prices. But demand in other regional markets was also far from healthy. Bar and coin investors faced similar challenges to jewellery consumers: high gold prices, lower oil revenues squeezing incomes and political instability all contributed to the lowest level of regional investment in our time series of just 1.9t – a fraction of the 19.7t five year quarterly average.

The 47% year-on-year drop in Turkey’s bar and coin demand was partly the result of last year’s strong Q3 base. Demand has bumped along in the range of 4–5t since the beginning of last year, with the exception of the third quarter when political turmoil coincided with lower prices to spark a rush for safe haven holdings of gold. Demand is expected to continue in a similar vein for the rest of the year, given very high local prices (due to lira weakness) and the persistent negative geopolitical climate.

Investment in the smaller Asian markets shelved in the face of high prices

Retail investment demand across the smaller markets in Asia stalled in the face of higher gold prices. Investors viewed the price hike as temporary and held off from making any purchases of bars and coins in anticipation of a correction back towards US$1,300/oz. A 4 relatively benign inflation environment across markets including Thailand and Indonesia also undermined the motive for buying gold as an inflation hedge. Fourth quarter demand is expected to pick up as October’s price drop offered a good buying opportunity for those waiting for lower prices.

Footnotes:

1. Read more: https://www.gold.org/mygoldguide/newsandtrends/indiangoldcoin

2. Read more: http://www.businessstandard.com/article/ptistories/ibjagoldtosetup100storesin3years116101200503_1.html

3. Read more: http://www.gold.org/research/indiagoldcoin

4. Knight Frank, The Wealth Report 2016.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.