![]()

On Oct. 25, NewCastle (TSX-V: NCA), Trek Mining (TSX-V: TREK), and Anfield Gold (TSX-V: ANF) announced a three-way business combination to form Equinox Gold (TSX-V: EQX). The new company will be led by mining entrepreneur Ross Beaty as Chairman (who is investing US$20 million), Christian Milau as CEO, and Greg Smith as President (both from Trek). This will immediately create a well funded mid-tier gold company on the path to production with plenty of potential for investors.

A note from TD Securities’ Analyst Daniel Earle, outlined the value this deal will create. TD Securities views this transaction positively as the merger will create a company that is more than the sum of its parts.

“In essence, we have what we view to be two unfunded and poorly understood development stories merging with a cash shell to create a higher profile company, both in terms of its leadership and market size, with a fully funded path to eventual mid-tier production.“

The combined company is expected to have $98 million in cash less costs at closing, excluding any asset sales, plus a US$85-million credit facility with Sprott and a US$200-million development facility. TD has a $2.00 12-month target price which is based on 0.9x its pro forma Equinox corporate NAV5% of $2.25/share.

If investors were looking to benefit early from the merger of the three companies, TD notes that NewCastle is currently trading at 0.32x their corporate NAV of 5% as of Nov. 1 which represents a significant discount to its peer group of gold development-stage companies in TD’s precious metals coverage, which are trading at an average of 0.49x NAV5%.

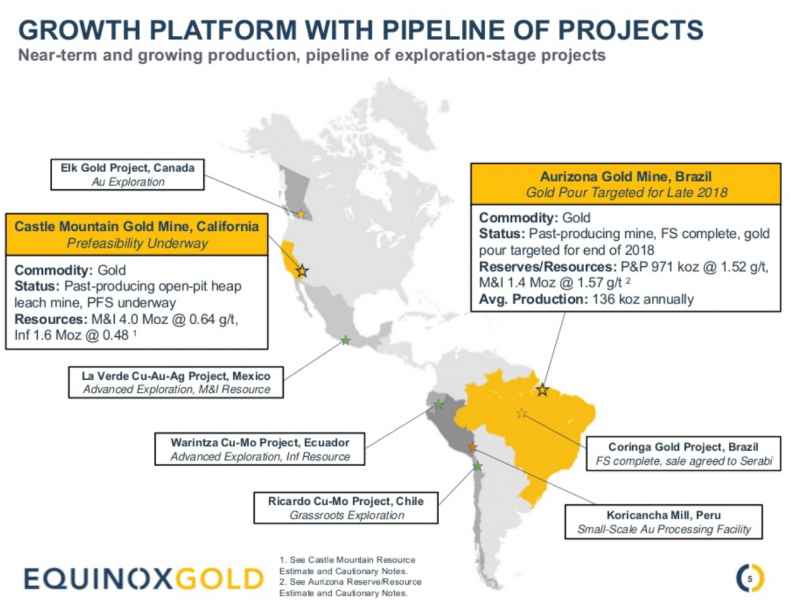

The new company’s main two assets will be the 100-per-cent owned Aurizona Mine in the Brazilian State of Maranhao and the Castle Mountain Project in California. However, there are plenty of projects that could generate other sources of value.

The Aurizona Mine is a past producer from 2010 to 2015 under Luna Gold, which failed under the heavy burden of a 17-per-cent gold stream and debt facility owed to Sandstorm Gold. The stream was restructured in March 2015 to a sliding-scale royalty of three to five per cent (3% at <US$1,500/oz Au). The mine has 971 koz @ 1.52 gpt in reserves and 1.4 Moz @ 1.57 gpt (Measured & Indicated Resources, inclusive). Annual production of 136 koz at US$691/oz (AISC: US$754/oz) over a 6.5-year mine life. First gold coming out of the mine is expected in the first quarter of 2018.

The Castle Mountain project is a past producer from open pit/heap leach and a small mill from 1991–2002. An updated resource estimate is due in September following a 44 km infill drill program, with a Pre-Feasibility study expected in Q1/18. The property has a resource of 4.0 Moz @ 0.64 gpt (Measured & Indicated Resources). There is plenty of potential for further exploration and resource expansion at Castle Mountain, if permitting proceeds smoothly.

The company also has prospective claims and spin out possibilities in Ecuador, British Columbia, Mexico, Chile and Peru. The company has generated more cash from the sale of assets from Anfield raising $22 million from the sale of the Coringa Gold project and the spin-out of copper assets in Mexico (La Verde — 746 Mt @ 0.4% CuEq M&I+I), Ecuador (Warintza — 195 Mt @ 0.6% Inf.) and Chile (Ricardo — concept/exploration) in 2018.

The transaction, if approved by the shareholders of Newcastle and Anfield, is expected to close on or about Dec. 22, 2017, just in time for Christmas, a possible gift for weary gold investors.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.