The world’s two biggest gold miners both announced mega-mergers over the past 5 months or so. These huge deals briefly garnered some interest in the usually-forgotten gold-stock sector, and fleeting praise from Wall Street analysts. But gold-stock mega-mergers are bad news for gold-miner shareholders on all sides. They reveal the serious struggles of major gold miners, and really retard future upside in their stocks.

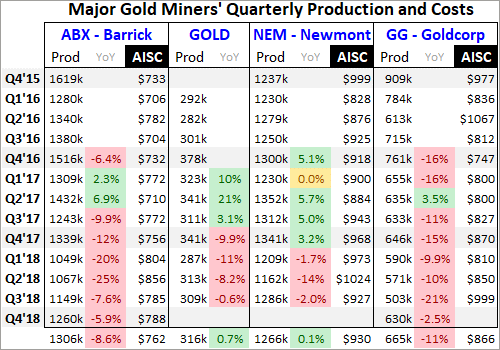

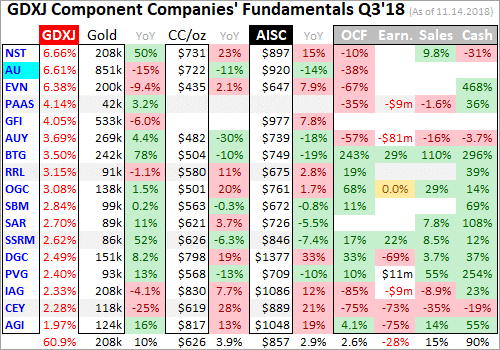

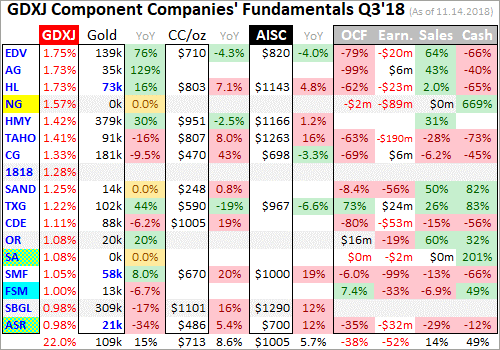

For decades the largest gold miners in the world have been Newmont Mining (NEM) and Barrick Gold (ABX). These behemoths have long dwarfed all their peers in operational scope. While the gold miners are in the process of reporting Q4’18 results now, their latest complete set remains Q3’18’s. As after every quarterly earnings season, I analyzed them in depth for the major gold miners of GDX back in mid-November.

The GDX VanEck Vectors Gold Miners ETF is the world’s leading and dominant gold-stock investment vehicle. In Q3 alone NEM and ABX mined a staggering 1286k and 1149k ounces of gold! To put this in perspective, the average of the next 8 largest gold miners rounding out the top 10 was just 508k ounces. Newmont and Barrick have long been in a league of their own, with commensurate market capitalizations.

In mid-November NEM and ABX were worth $17.1b and $14.9b, granting them massive 11.0% and 9.5% weightings within GDX. These two gold giants alone accounted for over 1/5th of GDX! That gives them outsized influence in not only that ETF, but in the entire gold-stock sector. GDX is the sector benchmark of choice for gold stocks these days, so the fortunes of NEM and ABX stocks really affect overall performance.

Gold-mining stocks are generally divided into three tiers based on their production. Anything over 1000k ounces annually is considered a major, which works out to 250k per quarter. NEM and ABX produced so much gold in Q3 they exceeded this threshold by a colossal 5.1x and 4.6x! They are really super-majors. Mid-tier gold miners produce between 300k to 1000k ounces every year, while juniors are under 300k.

Back on September 24th, 2018, Barrick Gold shocked the gold-stock world. It announced it was merging with Randgold (GOLD), which was really an all-stock acquisition of GOLD by ABX worth $6.5b. Barrick shareholders would own 2/3rds of the new combined company, while Randgold’s would own the rest. To avoid confusion, this essay uses the classic ABX and GOLD stock symbols to represent Barrick and Randgold.

ABX had been Barrick’s ticker for decades, but was just recently abandoned on January 2nd. With this mega-merger finished, the new company took over the excellent GOLD symbol going forward. That is a wise decision, as anyone who types “gold” into any brokerage account will see Barrick Gold. Years ago before Randgold got that coveted symbol, another major miner had it and really seemed to benefit from it.

In Q3 Randgold was the 10th-largest gold miner in the world producing 309k ounces. Added on top of Barrick’s 1149k, the new combined 1458k would take back the top-gold-miner crown from Newmont which produced 1286k that quarter. Apparently size matters a lot when you’re a gold-mining executive. But with both ABX and GOLD suffering chronic declining production, that mega-merger reeked of desperation.

Newmont’s leadership wasn’t happy with losing the pole position among global gold miners. So it soon got to work on looking for a mega-merger of its own. On January 14th, NEM announced it was acquiring major miner Goldcorp (GG) in an all-stock deal worth $10.0b! That looked like one-upmanship taking it to Barrick. NEM and GG shareholders would own about 2/3rds and 1/3rd of the new combined colossus.

Goldcorp was the world’s 7th-largest gold miner in Q3’18, producing 503k ounces of gold. Added on to Newmont’s 1286k, that creates a new monster running at an unprecedented 1789k-ounce quarterly rate! If bigger is better, these new combined super-major gold miners ought to be the best seen in history. But unfortunately in gold mining that isn’t true, and these new giants will likely fare worse than if they hadn’t merged.

In their merger announcements, the CEOs of all 4 of these major gold miners tried hard to sell their deals as wonderful news for shareholders. They argued that synergies and cost savings would make these new combined titans more effective at producing superior returns for their shareholders going forward. And as always with any large merger, Wall Street analysts universally applauded these mega-mergers as good.

Sadly the opposite is likely true, these deals are bad news for all the owners of Newmont and Barrick as well as former owners of Goldcorp and Randgold. These new giant super-majors are even bad news for the gold-mining sector as a whole. The odds are really high that their stocks will really underperform the smaller major, mid-tier, and junior gold miners in coming years. That will hurt this entire sector on multiple fronts.

Contrary to their CEOs’ marketing propaganda, none of these four major gold miners approached these deals from positions of strength. They’ve all been struggling with weakening production and rising costs. Gold mines are wasting assets that are constantly depleting, and it is increasingly challenging to find new gold to mine economically at the scale and pace the majors need. These mergers didn’t solve that core problem!

This table looks at the quarterly production, its year-over-year change, and all-in sustaining costs per ounce mined of Barrick, Randgold, Newmont, and Goldcorp during today’s secular gold bull. It started in late Q4’15 out of deep 6.1-year secular lows in gold. Barrick deleted Randgold’s old website, so there is no Q4’15 GOLD data. And as of Wednesday afternoon NEM and GG hadn’t yet reported full Q4’18 results.

Barrick and Newmont didn’t just effectively dilute their shareholders by 50% for some relatively-meager cost-saving synergies, but because they can’t grow their production internally. ABX’s gold mined each quarter has been falling sharply on balance for years! It has seen brutal YoY drops as high as 25.5%, which ought to be impossible for a world-class gold major. 7 of the last 9 quarters have seen big declines.

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses.

And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost for its first four quarters as a merged company, and then waning production will again be unmasked.

While the new giant Barrick will have more capital to develop new gold mines and expand existing ones, it seems unlikely that will be enough to turn this super-major around. Barrick and Randgold operated about 12 and 4 gold mines respectively pre-merger. So bringing another few online in coming years might not move the needle enough to outpace depletion. And it takes over a decade to permit and build new mines.

The entire gold-mining industry has been greatly starved of capital largely since 2013, with 2016 being a modest exception. Thus the big investments necessary to find new large-scale gold deposits and slowly advance them to mine builds have been severely lacking. So this whole industry’s pipeline of new gold to mine has been crippled, all but pinched shut. Declining miners merging does little to solve this problem.

Newmont has fared way better than Barrick in recent years, actually enjoying strong production growth on balance from Q4’16 to Q4’17. But this past year even mighty NEM has started to suffer from waning gold production. It averaged 5.9% YoY declines in the first three quarters of 2018. I suspect NEM is just a little behind ABX in rolling over into depletion outpacing mining growth. ABX’s merger forced NEM to act.

While Goldcorp was long celebrated as the world’s best major gold miner, it has been struggling for years with slowing production. Over the last 9 quarters GG only saw one modest production gain, with its gold mined dropping a colossal 11.0% YoY each quarter on average! So although GG produces about twice as much gold as Randgold, it might be a worse acquisition target due to its faster pace of shrinking production.

Like ABX and GOLD, it’s hard to imagine combining two more weakening majors NEM and GG will yield a way to stop and reverse their falling production. Again for their first four quarters together this new giant Newmont will appear to see big annual production growth. But once that post-merger comparison rolls past, the declining gold across all its mines will again be revealed. Mega-mergers can’t negate mine depletion.

Randgold didn’t even bother reporting industry-standard all-in sustaining costs, which is why they’re not included above. But its cash costs were often on the high side, so it’s likely the new combined company will drag overall mining costs higher. Barrick’s major-leading low AISCs aren’t likely to last with GOLD’s mines thrown in the mix, which means higher costs and lower overall profitability for Barrick going forward.

Newmont should benefit more from Goldcorp’s lower cost structure. NEM averaged $975 AISCs in the first three quarters of 2018, way higher than the $877 average in Q3’18 among the GDX gold miners. GG’s AISCs averaged $886 over that 9-month span, so the new combined Newmont should benefit from lower costs. But that may not last long, as weakening production eventually pushes per-ounce costs higher.

Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. So slowing production yields fewer ounces to spread mining’s big fixed costs across. If these new super-major gold behemoths can’t arrest their depleting production, their costs will inevitably rise in the future hurting profitability. Again these mega-mergers didn’t solve that problem.

So it looks like the managements of Barrick and Newmont just issued $6.5b and $10.0b of new stock so they could report big merger-driven production surges for a single year! Once those pre- and post-merger year-over-year comparisons pass, the vexing waning-production problems at all four of these predecessor gold miners will again become apparent. But that’s not even the biggest reason these mergers are bad news!

Even before these mergers as apparent in mid-November when I analyzed Q3’18 results, both Newmont and Barrick already had very-large market capitalizations of $17.1b and $14.9b. That again granted them massive 11.0% and 9.5% weightings in GDX. Like most stock indexes and ETFs, GDX’s components are weighted by market cap. Goldcorp and Randgold ranked 6th and 7th then in market cap and weightings.

Adding NEM and GG together as of mid-November would catapult their market cap and GDX weighting to $25.1b and 16.0%. Adding ABX and GOLD together yields a similar $22.3b market cap and 14.5% total GDX weighting. So these two super-majors alone could account for a crazy 30.5% of GDX’s weighting! That is almost scarily concentrated, although we don’t yet know how GDX’s managers will deal with this.

As of this week the new combined Barrick only has an 11.1% GDX weighting, while Newmont is at 8.2% since its mega-merger is not yet consummated. It will be interesting to see whether the new companies’ weightings going forward are kept in market-cap proportion or somehow limited. I hope it’s the latter, as many of the other gold miners in GDX have far-better growth prospects than these new super-majors.

ETF weightings aside, higher market caps create plenty of problems of their own. I’ve written essays in the past on picking great gold stocks, and surprisingly market capitalization is the single most important factor for future gains. The gold stocks with the largest market caps usually significantly underperform their smaller peers. These new super-majors are so darned big that they really compound this problem.

In mid-November when I analyzed the GDX miners’ Q3’18 results, the average market cap of its top 34 component stocks was $4.3b. Excluding NEM and ABX, that fell to $3.5b. It takes proportionally more capital inflows, investors buying shares, to push a larger stock higher than a smaller one. If the super-majors are worth $24b, it takes 6x as much buying of their stocks to drive the same gains as on a $4b company!

Imagine the different forces involved turning a supertanker versus a tugboat. The bigger any stock in the stock markets, the more inertia it has and thus the more capital is needed to overcome that and move the stock. And market-cap issues are not just a size thing in gold stocks. Smaller major, mid-tier, and junior gold miners have way fewer gold mines and much-lower production, which makes it far easier to grow output.

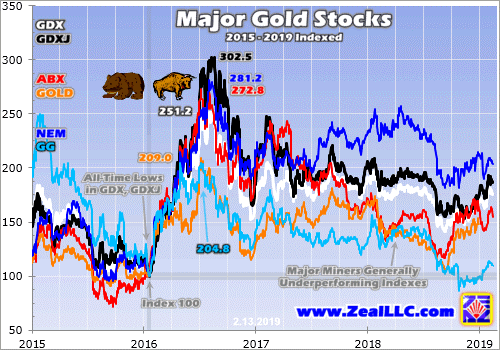

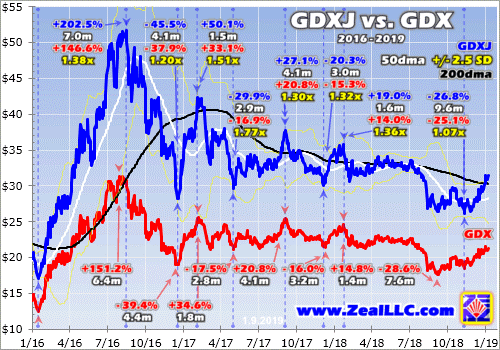

While Newmont is a temporary exception since it was bucking the major trend and growing production in 2017, Barrick, Randgold, and Goldcorp all really underperformed their sector in recent years. This chart looks at the indexed performance in ABX, GOLD, NEM, and GG stocks compared to the leading sector ETFs of GDX and the smaller GDXJ which largely tracks mid-tier gold miners under 1m ounces annually.

Both GDX and GDXJ fell to all-time lows back in mid-January 2016 when this gold-stock bull was born. So all 6 stocks are indexed to 100 as of that day, revealing their relative performance since. Despite their heavy weighting in GDX, the major gold miners generally lag their key sector benchmarks. ABX, GOLD, and GG have really struggled in recent years as their managers failed to stem big production declines.

This chart is pretty damning, showing why the managers of Barrick and Newmont are desperate to show rising production even if only for a year after their wildly-expensive mega-mergers. ABX and GOLD have both been really underperforming their peers, scaring investors away while putting serious pressure on managements to turn things around. NEM resisted that, but its production started to decline too in 2018.

And GG has been a basket case, actually managing to fall below its deep secular lows of early 2016 in recent months! That’s a sad fate for what was the world’s best major gold miner for many years. NEM buying this dog is likely to drag down NEM’s stock performance to some midpoint between what it has done and how GG has fared. For the most part the largest gold miners haven’t been good investments.

The much-larger market caps coming from combining struggling majors into super-majors is highly likely to exacerbate this underperformance trend. The new Newmont and Barrick are way bigger and far more ponderous, and will require a lot more share buying to move their stock prices materially higher. But why will most investors even bother to buy these titans when many smaller mid-tier gold miners are thriving?

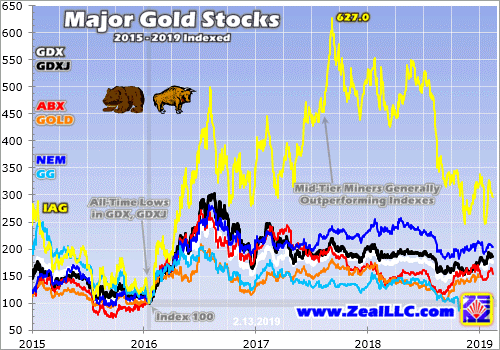

This next chart adds a single additional mid-tier gold miner to illustrate their outperformance. I chose IAMGOLD (IAG) for this example for a couple reasons. It produced 882k ounces in all of 2018, which makes it a larger mid-tier gold miner nearing that 1000k+ major threshold. And IAG is unremarkable fundamentally. It mined the same 882k ounces in 2017, so there was no production growth at all last year.

And its 2018 all-in sustaining costs are expected to come in on the high side near $1070 per ounce, which is worse than most of the majors. So there’s really nothing special about IAG operationally suggesting it should far outperform. If I wanted to cherry pick, there are other mid-tier miners that have trounced what IAG has done in recent years. Yet even IAG wildly outperformed the majors and sector ETFs during this gold bull.

If Newmont and Barrick were the only gold-mining stocks, they’d certainly be worth owning during a secular gold bull. But why own these massive supertanker-like gold miners when smaller major, mid-tier, and junior gold miners’ stocks are performing way better? The smaller miners not only have lower market caps easier to bid higher with much-smaller capital inflows, but plenty also have superior fundamentals.

They tend to have just a few or less gold mines, making it much easier to grow production by expanding existing mines or building new ones. Those expansion events act as major psychological catalysts to get investors interested in those stocks, fueling disproportionally-large buying to catapult them higher. There is really no reason to deploy capital in large majors when mid-tiers are easily running circles around them.

Even if like me you don’t own Newmont or Barrick and have no intention of investing in them, they could cause problems for the entire gold-stock sector. Their hefty GDX weightings mean their stocks have way-outsized influence in how that leading ETF fares. If these super-majors’ giant stocks lag, they are going to retard GDX’s upside which in turn will leave traders less optimistic and more skeptical on gold miners’ outlook.

So mega-market-cap gold miners could significantly slow the overall sentiment shift from bearish back to bullish which is necessary to attract in buying. If capital inflows diminish because of the perception this sector isn’t rallying enough, the bull-market uplegs will unfold slower and maybe end smaller. Even more problematic, the super-majors’ high weightings in GDX suck ETF capital away from more-deserving miners.

Most investors prefer sector ETFs over individual stocks, so lots of capital will flow into GDX as investors get interested in gold stocks again. GDX’s managers have to allocate any differential buying pressure into its underlying component companies in proportion to their weightings. The newly-merged Barrick and Newmont will likely command much-bigger weightings, starving smaller component miners of capital inflows.

But despite these mega-mergers being bad for everyone except the managers of those companies paying themselves huge compensation, all is not gloom and doom. If the new Newmont and Barrick continue to suffer waning production after their initial merger-boost year, investors will shift capital out of them into the other gold miners. That will gradually throttle their market caps and thus weightings in GDX, mitigating damage.

And if these super-majors taint the performance or expected upside in GDX enough, GDXJ may very well usurp it as the gold-stock sector benchmark of choice! While falsely billed as a Junior Gold Miners ETF, GDXJ has really become a mid-tier gold miners’ ETF. It has been increasingly outperforming GDX, and that trend could accelerate since GDXJ will hopefully never include the larger majors led by NEM and ABX.

With so many fundamentally-superior smaller gold miners to pick from, investors have no need to own the larger majors. Plenty of mid-tier miners are still growing their production organically, by expanding their existing mines or building new ones. Their upside as gold continues marching higher in its bull market is enormous, dwarfing what is possible in the giant majors struggling with waning production. Avoid the latter!

One of my important missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with the greatest upside potential. The trading books in both our weekly and monthly newsletters are currently full of these better gold and silver miners. Most of these trades are relatively new, added in recent months as gold stocks recovered from deep lows. So it’s not too late to get deployed ahead of big gains!

To multiply your wealth in stocks you have to do some homework and stay abreast, which our popular newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. Walking the contrarian walk is very profitable. As of Q4, we’ve recommended and realized 1076 newsletter stock trades since 2001. Their average annualized realized gain including all losers is +16.1%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is gold-stock mega-mergers are bad news for everyone in this sector. Combining major gold miners already struggling with slowing production doesn’t solve the problem, but only masks it for a single year. The resulting super-majors’ massive market capitalizations saddle their share prices with big inertia. They are going to require much-larger capital inflows to rally materially, really retarding their upside.

Their higher weightings within sector ETFs will lead to worse perceived sector performance, delaying the necessary sentiment shift from bearish back to bullish. And the super-majors will suck up more of the capital allocated to gold-stock ETFs, starving smaller and more-worthy gold miners of buying. Thankfully some of these problems can be avoided by shunning Newmont and Barrick, and sticking with great mid-tier miners.

Adam Hamilton, CPA

February 19, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Gold stocks’ young upleg is gathering steam, marching steadily to higher lows and higher highs. These bullish technicals are gradually improving sentiment, fueling mounting interest in this contrarian sector. That’s helping the gold stocks regain lost ground relative to gold, the driver of their profits. Fundamentals are growing more favorable as gold itself powers higher. All this portends much-bigger gold-stock gains coming.

Despite a strong rebound upleg in recent months, the gold miners’ stocks are still flying under the radars of most speculators and investors. They aren’t aware the gold stocks are running again, and likely don’t realize how massive gold-stock uplegs can grow. That’s unfortunate, because the biggest gains are won early in young uplegs before they are universally recognized. Buying low early on is the key to multiplying wealth.

The most-popular gold-stock benchmark these days is the GDX VanEck Vectors Gold Miners ETF. It was launched way back in May 2006, giving it a first-mover advantage that has grown into an insurmountable lead. This week GDX’s net assets of $10.5b were a colossal 52.4x larger than the next-biggest 1x-long major-gold-miners-ETF competitor! GDX is the lens through which most traders now view gold-stock fortunes.

And they’ve been excellent in recent months, with GDX boasting performance well outpacing gold as well as the general stock markets. This first chart looks at this sector ETF’s price action over the last several years or so. That’s technically been a gold-stock bull, because gold itself remained in a bull market over that span. Since gold overwhelmingly drives gold-stock performance, it defines gold-stock bull-bear cycles.

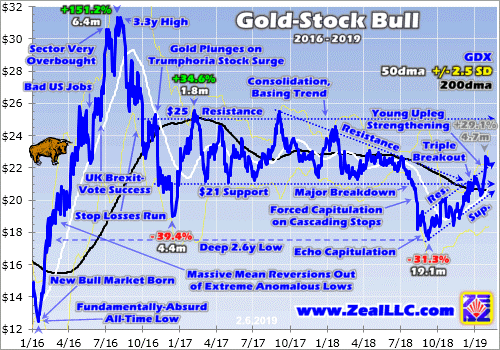

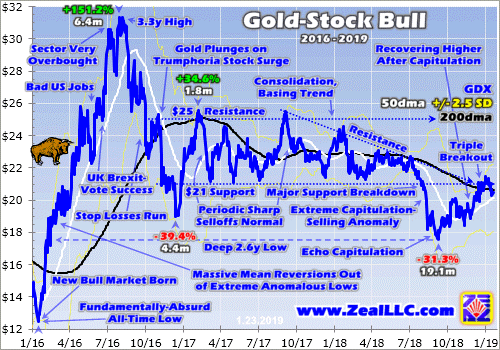

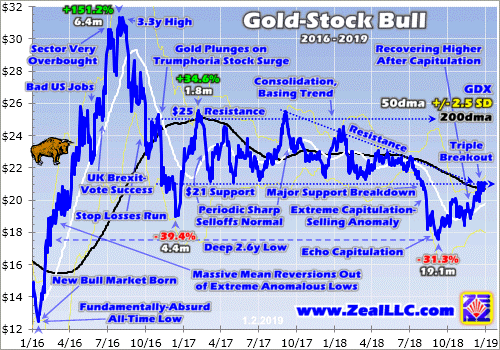

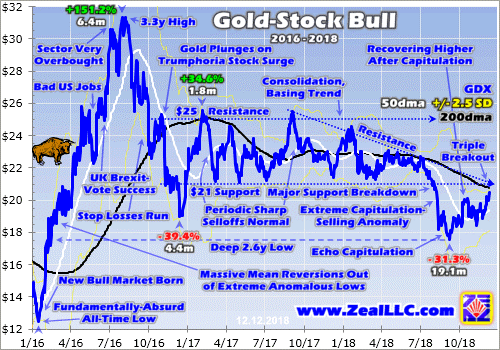

In mid-September GDX shares plunged to a deep 2.6-year secular low. That was fueled by an extreme forced capitulation in gold-stock shares, the result of stop losses being sequentially triggered in cascading fashion. The GDX price action of recent years setting the stage for this latest low and subsequent upleg is important to understand, and I’ve written recent essays explaining it. Today’s focus is the young upleg since.

It’s actually been quite impressive, and more traders will soon take notice. After bottoming at $17.57 on September 11th, GDX started powering higher in the tight well-defined uptrend bracketed above. Despite the incredibly-bearish sentiment you’d expect after a capitulation plunge leading to major lows, the gold stocks started marching higher on balance. Their young upleg has gathered steam and achieved much since.

GDX has carved a textbook-perfect series of higher lows and higher highs. That inexorably pushed it to a major triple breakout in late December and early January. GDX clawed back above three major overhead resistance lines. The first was the longstanding $21 support of GDX’s prior consolidation basing trend, which had persisted for 21.5 months before early August. Following a major breakdown, it became resistance.

The second was the downward-sloping resistance of a bearish descending-triangle technical pattern that had formed since GDX crested in early September 2017. And the third and most important was GDX’s 200-day moving average, shown in black in this chart. Seeing GDX overcome all three of these major overhead resistance zones in short order was a very bullish sign implying gold stocks were off to the races.

At best so far their young upleg per GDX has powered 29.1% higher in 4.7 months! That’s impressive by any standard. For comparison the S&P 500 broad-market stock index actually fell 6.4% during that span. And gold only rallied 10.3% in its own parallel upleg, so the major gold stocks have enjoyed good 2.8x upside leverage to the metal which drives their profits. That’s on the high side of the typical 2x to 3x range.

GDX has pulled back modestly since hitting its latest upleg high on January 31st, which was a breakout above its uptrend channel. Mid-upleg retreats within trend are perfectly normal and expected. They keep uplegs healthy and extend their longevity by periodically bleeding off excess greed. Without pullbacks, it would flare bright enough to suck in enough near-future buying for the upleg to prematurely exhaust itself.

And just this week this young gold-stock upleg reached another major technical milestone. On Tuesday GDX flashed a Golden Cross buy signal as its 50dma climbed back above its 200dma. Golden Crosses following deep oversold lows are incredibly bullish, signaling major new uplegs or entire bull markets! So they are one of the most-widely-followed and heeded buying signals among technically-oriented traders.

The initial major upleg of this gold-stock bull soared in essentially the first half of 2016, when GDX skyrocketed 151.2% higher in just 6.4 months! Nearly 2/3rds of those entire gains happened after the last Golden Cross following super-oversold lows flashed in early March 2016. These powerful buy signals aren’t just hard technical confirmation that a major upleg is underway, but they occur fairly early in upleg lifespans.

Today’s young gold-stock upleg is the most-consistent, longest-lived, and technically-sound one seen since that H1’16 monster! In general the more gradually uplegs rally, the stronger their technical and sentimental foundations and the longer they are likely to last. Slow-and-steady gains help prevent trader psychology from getting too unbalanced and extreme, granting more time for capital inflows to push prices higher.

GDX did enjoy a larger 34.6% surge over just 1.8 months leading into early February 2017. But that was so sharp it soon burned itself out and failed. Today’s young upleg is far more solid with a lot more staying power. And it remains on the small side by gold-stock standards, implying the lion’s share of its gains are still coming. While GDX’s massive 151.2% blast higher in H1’16 was unusual, gold-stock uplegs tend to get big.

The last secular gold-stock bull ran from November 2000 to September 2011. Just over half of that was in the pre-gold-stock-ETF era before GDX’s launch, so a different benchmark was used to measure it. During that long 10.8-year span, the classic HUI NYSE Arca Gold Bugs Index skyrocketed an astounding 1664.4% higher! Today’s hated gold stocks were the best-performing stock-market sector of that decade.

That life-changing secular gold-stock bull consisted of 12 separate uplegs. Excluding a giant anomalous one soaring after 2008’s first stock panic in a century, the 11 normal ones averaged gains of 80.7% over 7.9 months! Large uplegs are par for the course in the small and volatile gold-stock sector. So the 29.1% GDX gains we’ve seen so far in today’s young upleg are nothing. It’s likely to grow much larger in coming months.

Technically GDX should easily rally to $25 fairly soon, which was the old upper-resistance line of its long consolidation basing trend. That would extend this upleg’s gains over 42%. At that point GDX’s upside momentum would likely drive an upside breakout. And seeing GDX climbing to new multi-year highs over $25 would certainly catch traders’ attention, leading to a surge in capital inflows to chase gold stocks’ upside.

GDX’s bull-to-date peak was $31.32 in early August 2016, which wasn’t lofty as a mere 3.3-year high. It wouldn’t surprise me at all to see GDX challenge those levels before this young upleg matures then gives up its ghost. Rather interestingly that would grow this upleg to 78% gains, which is right in line with the previous secular bull’s average. The gold stocks still have lots of room to power much higher from here.

Their coming gains are inexorably intertwined with gold like usual. Gold-stock uplegs are directly driven by parallel gold uplegs. Rising gold prices boost gold stocks both sentimentally and fundamentally. They motivate speculators and investors to redeploy capital in the gold miners, and buying begets buying. The longer and higher gold stocks rally, the more traders want to buy them. Gold gains fuel this virtuous circle.

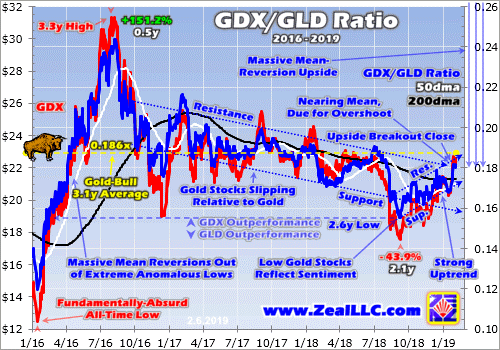

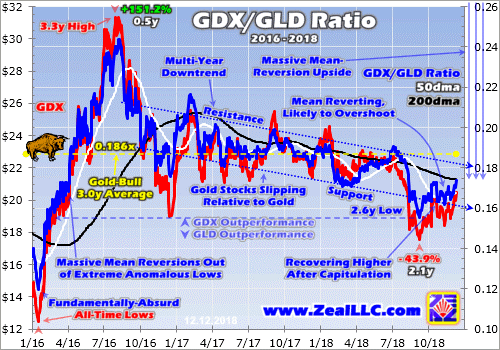

But more importantly higher gold prices directly drive higher earnings at the gold miners, fundamentally justifying higher gold-stock prices. This critical relationship is approximated by the ratio between gold-stock and gold price levels. It also portends big gold-stock gains coming. This next chart looks at the GDX/GLD Ratio during recent years’ gold-stock bull. GLD SPDR Gold Shares is the world’s leading gold ETF.

When this GGR is rising it means gold stocks are outperforming gold. That’s normally what happens in gold-stock uplegs. Like GDX itself, its ratio to gold is also climbing in a strong uptrend since those deep mid-September gold-stock lows. But the GGR remains on the low side of today’s gold bull, and has vast room to mean revert higher to pre-bull averages. I explained all this in depth back in a mid-October essay.

In mid-September as gold stocks’ forced capitulation decimated sentiment, the GGR collapsed to merely 0.155x. A single share of GDX was worth less than 1/6th of a single share of GLD. That also happened to be a 2.6-year secular low in the ratio of gold-stock price levels to gold prices. That simply reflected the seriously-bearish psychology that invariably accompanies major lows. But the GGR has recovered since.

By that latest interim GDX high on January 31st, the GGR had mean reverted back up to 0.182x. That is actually still below this bull market’s average of 0.186x over the past several years or so. But the climbing GGR proves gold stocks are making a major recovery relative to gold. Note above today’s young upleg is seeing the longest, strongest, and solidest GGR rally since H1’16! This upleg is the real deal, no flash in the pan.

After the GGR is forced to major lows or highs well off its averages, it tends to not only mean revert but overshoot proportionally. Since this key fundamental metric of gold stocks fell 0.030x below its bull mean at worst in mid-September, it ought to power a similar amount back above it before this upleg matures. That implies a 0.216x GGR is likely as gold stocks get more popular the longer their upleg rallies higher.

This week GLD traded near $124, so GDX regaining 0.216x means its price would rally to $26.78. That would make for a 52% upleg at today’s gold prices, and would drive that major breakout over GDX’s old $25 resistance line. And of course higher gold prices would lead to proportionally-higher GDX targets at any given GDX/GLD Ratio. Looking at today’s gold-stock levels compared to past means shows huge upside.

Back in mid-October when GDX was still only trading in the $18s and few believed a new gold-stock upleg had been born, I explored the GGR. This small contrarian sector was the last cheap one in wildly-expensive stock markets. I looked at some past GGR levels from the last secular gold-stock bull to point out how far gold stocks could soar. Consider the couple-year spans surrounding 2008’s wild stock panic.

In the 2 years after that extreme anomaly, 2009 and 2010, the GGR averaged 0.422x. And in the 2 years before that fear superstorm, it averaged 0.591x. Those are not high levels at major gold-stock toppings when euphoria reigned, but mere means. GDX ought to be able to regain those well-established levels later on in this bull market. At today’s gold prices, the post-panic average would catapult GDX to $52.33.

That would make for 198% gains from the recent secular low, a tripling in major gold miners’ stock prices! And that still wouldn’t be close to GDX’s $66.63 record hit at the end of gold stocks’ last secular bull back in September 2011. At the pre-panic 2-year-average GGR, this week’s gold levels would support an all-time GDX high of $73.28. That’s 317% higher than recent lows, more than a quadrupling in gold-stock price levels!

And all this assumes flat gold in the low $1300s, which is very unlikely. Gold is enjoying its own young upleg powering higher, which was sparked by the serious stock-market selloff in Q4. At $1350, $1400, or $1450 gold, the gold-stock price levels implied by GGR mean reversions are much higher. And that doesn’t account for the typical proportional overshoot towards the opposite extreme after deep GGR lows are hit.

The key takeaway here is gold stocks’ upside potential remains very large despite the progress so far in this young upleg. The big majority of this particular gold-stock upleg almost certainly remains ahead, so it’s not too late to get deployed before everyone else figures it out. Once gold stocks start surging faster than gold, the resulting bullish psychology becomes self-feeding enticing in more capital fueling bigger gains.

Big gold-stock uplegs are fully justified fundamentally by higher gold prices. Consider an example. The gold miners are now reporting their Q4 results, but the last complete set was Q3’s. Then the major gold miners of GDX reported average all-in-sustaining costs of $877 per ounce. These generally don’t change much regardless of prevailing gold prices. Mining costs are largely fixed when mines are being planned.

That’s when engineers and geologists decide which ore to mine, how to dig to it, and how to process it to recover the gold. So higher gold prices directly amplify gold miners’ bottom lines. While I’ll wade through the gold miners’ Q4 results once they are all released and write a new essay on them, AISCs are highly likely to remain near Q3 levels. Let’s call it $875 per ounce. In Q4 gold’s price averaged $1228 despite the rally.

That means the major gold miners were collectively earning about $353 per ounce mined. Meanwhile so far in Q1 gold is averaging $1296, which is a hefty 5.5% higher quarter-on-quarter. Assuming AISCs are flat across this industry, that implies gold miners are now earning $421 per ounce. That’s a massive 19.3% QoQ jump in profits on a 5.5% higher gold price, making for strong 3.5x upside leverage to gold.

The higher prevailing gold prices thanks to its own upleg are fueling fatter earnings for the gold miners. That provides the critical fundamental underpinning supporting major gold-stock uplegs. They are not just psychological phenomena driven by shifting sentiment, but actually reflect better operating conditions. I doubt historical gold-stock uplegs could’ve averaged such big gains without real fundamental foundations.

The unfortunate thing about major gold-stock uplegs is most speculators and investors ignore them until way too late. Traders love buying high and chasing momentum, but hate buying low before those big gains happen. So sadly the great majority of traders miss the great majority of major gold-stock uplegs. They don’t start deploying capital until after most of the gains are already won, which usually leads to later losses.

While today’s young upleg is gathering steam, we’ve likely only seen the first third or so. Thus there is still time to buy gold stocks relatively low before others start chasing their momentum in coming months after they are much higher. Why buy high later when you can still buy low now? And the best gains won’t be won in big ETFs like GDX, but in the stocks of fundamentally-superior smaller mid-tier and junior gold miners.

The major gold miners dominating GDX are really struggling to grow their gold production. Depletion is outpacing mine growth leading to higher costs and lower profits. That really retards their and thus GDX’s upside potential. But plenty of smaller gold miners are growing their output through new mine builds and expansions, which also lowers their costs. Their stocks’ upside potential utterly trounces the GDX majors.

The earlier you get deployed, the greater your gains will be. That’s why the trading books in our popular weekly and monthly newsletters are currently full of better gold and silver miners mostly added in recent months. The gains we won in 2016 were amazing the last time American stock investors returned to gold. Our newsletter stock trades that year averaged +111.0% and +89.7% annualized realized gains respectively!

The gold-stock gains should be similarly huge as today’s young gold and gold-stock uplegs grow. The gold miners are the last undervalued sector in these still-expensive stock markets, and rally with gold during stock-market bears unlike anything else. To multiply your wealth in the stock markets you have to do your homework and stay abreast, which our newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. You can subscribe today for just $12 per issue!

The bottom line is this young gold-stock upleg is really gathering steam. Technically it has rallied higher on balance for months now in a strong uptrend, carving higher lows and higher highs. GDX has broken out above three major resistance lines, and just flashed a key Golden Cross buy signal! All this has really started to shift sentiment back to bullish, which will attract in lots more capital to chase the momentum.

And these mounting gold-stock gains are fundamentally justified by gold’s own growing upleg. Gold-stock earnings amplify underlying gains in gold, making big stock-price surges righteous. Now is the time to get deployed relatively low, before most traders figure this out and start piling in. The evidence suggests a major gold-stock upleg is underway and mounting, and they tend to average gains far bigger than today’s.

Adam Hamilton, CPA

February 11, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Silver recently started outperforming gold again, a watershed event. For long years this white metal has mostly lagged the yellow one, relentlessly battering silver sentiment. But gold surging into year-end 2018 finally sparked some life into moribund silver. This is a bullish sign, as silver has soared in the past once rising prices reach critical mass in attracting new investment capital. Silver looks to be nearing that point again.

Despite a good finish, 2018 was a rough year for silver. Its price slumped 8.6%, way worse than gold’s -1.6% performance. And that still masks miserable intra-year action. At worst in mid-November, silver had plunged 17.3% year-to-date. That was 2.2x gold’s comparable loss, and at $13.99 silver languished at a major 2.8-year low. A soul-crushing 96% of its early-2016 bull market had been reversed and lost!

Back in December 2015 silver had bottomed a few days before gold at a deep 6.4-year secular low. Over the next 7.6 months silver soared 50.2% higher, outpacing gold’s parallel new-bull upleg by 1.7x. That promising start didn’t pan out though, silver crumbed once gold’s advance stalled and failed. Ever since its August 2016 peak of $20.56, silver mostly ground sideways sandwiched between two major downlegs.

It was the latter one that finally bottomed in mid-November 2018, with hope lost and silver bearishness universal and suffocating. Silver’s fortunes are heavily dependent on gold, and silver effectively acts like a gold sentiment gauge. The weak silver prices reflected the lack of enthusiasm for gold, which wasn’t far above its own 19.3-month low of mid-August. Gold had slumped to $1200, and threatened to break below.

For better or worse, gold drives silver. Traders usually ignore the tiny silver market until gold has rallied long enough and high enough to convince them its upside momentum is sustainable. So when gold itself is down in the dumps, silver doesn’t have a prayer. But gold bottomed that day and started clawing back higher, so silver joined along in the bounce. That gradually grew into a new silver upleg over the next 8 weeks.

By early January, silver had rallied 12.4% on a 7.7% gold rally. That made for 1.6x upside leverage to gold, which is still on the low side historically. But it was a welcome change after silver spent much of last year sliding considerably. A sub-span of that advance really caught my attention. Between the hawkish FOMC meeting on December 19th to the young new year on January 3rd, silver surged 7.9% in 9 trading days.

That was 1.9x gold’s 4.2% advance, and silver’s best outperformance relative to gold since that major upleg in H1’16! Something was changing in the left-for-dead silver market, with capital starting to return after more than a couple years of self-imposed exile. Over this past week silver enjoyed another solid stretch of outperformance, offering further confirmation. It started last Friday when gold itself soared 1.7%.

Gold ignited after a Wall Street Journal article claiming the Fed was considering ending its quantitative tightening early! That dovishness hit the U.S. dollar and catapulted gold higher. Over the next 4 trading day’s silver surged 4.8% on gold’s 3.0%, for 1.6x leverage. If that buying can push silver high enough to reach a psychological critical mass and become self-feeding, it portends major silver upside in coming months.

The more silver rallies, the more speculators and investors will want to buy it. The more capital they push into silver, the faster it will ascend. Buying begets buying in silver just like almost everywhere else in the markets. While upside momentum in itself is bullish anytime, silver’s upside potential is far greater than usual because it has been so darned undervalued. That’s made room for massive mean-reversion gains.

Silver’s “valuation” can be inferred relative to gold, its dominant driver. While the global silver and gold supply-and-demand profiles are independent with little direct linkage, these precious metals are joined at the hip psychologically. Silver rarely rallies materially unless gold leads the way. Silver traders look to gold for cues, which makes silver amplify gold’s moves. Silver’s technical relationship to gold is ironclad.

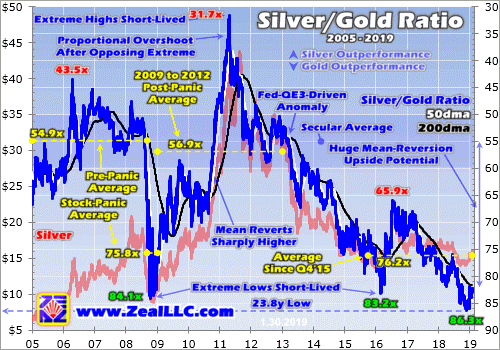

All this makes the Silver/Gold Ratio the most-important fundamental measure of silver-price levels. It is technically calculated by dividing daily silver closes by daily gold closes. But that yields tiny decimals that are hard to parse mentally, like the mid-week SGR of 0.012x. It is far more brain-friendly to consider this ratio from the opposite direction, via the Gold/Silver Ratio. This week it ran at an easier-to-comprehend 82.2x.

Mathematically the SGR is identical to an inverted GSR. So charting the GSR with an upside-down scale yields the same line as the SGR, but with way-more-intelligible numbers. Here this inverted-GSR SGR proxy in blue is superimposed over the silver price in red. Silver has rarely been lower relative to gold than it was in recent months. That portends monster upside as silver mean reverts higher leveraging gold.

At that latest secular silver low in mid-November, the SGR fell to 85.9x. In other words, it took nearly 86 ounces of silver to equal the value of one ounce of gold. While silver started recovering, it initially lagged gold enough to force the SGR lower still. At the end of November it slumped as low as 86.3x on close, an astounding level. That was actually an extreme 23.8-year secular low in the SGR, nearly a quarter-century!

Silver hadn’t been lower relative to gold since early March 1995, practically a lifetime ago considering all that’s happened in the financial markets since. Even during the greatest market fear event in our lifetimes the SGR wasn’t lower. During late 2008’s first-in-a-century stock panic, the SGR just briefly hit 84.1x in mid-October. Being highly-speculative and super-sensitive to sentiment, silver had plummeted leading into it.

That stock-panic episode of extreme SGR lows shows what’s probable after silver inevitably reverses and mean reverts higher. Over the 3.7 years since 2005 leading into that panic, the SGR averaged 54.9x. That was right in line with the mid-50s that had been normal for decades. Silver had generally oscillated around 1/55th the price of gold, so miners had long used 55x as the proxy for calculating silver-equivalent ounces.

With silver so radically out of whack relative to gold, those extreme SGR panic lows weren’t sustainable. Like a beachball pushed too far under water, silver was ready to explode higher to reestablish its normal relationship with gold. That indeed happened during the post-panic years. After plummeting as low as $8.92 in late-November 2008, silver more than doubled by early December 2009 with a 115.4% gain.

While silver was really outperforming gold after its anomalous lows, at best in that initial post-panic rally the SGR only regained 58.6x. That was still below the 55x secular average. So silver continued slowly grinding higher on balance into late 2010. Then gold started surging again, creating the right sentiment conditions to unleash self-feeding silver buying. Silver skyrocketed from there, surging far faster than gold!

The faster silver soared into early 2011, the more traders wanted to own it and the more capital they poured into it. This psychological phenomenon of higher prices being more attractive runs through nearly all markets. The crazy bitcoin mania in late 2017 was a recent example. Silver’s virtuous circle of surging and new capital inflows finally climaxed in late April 2011 at $48.43 per ounce. That was one heck of a bull.

Starting from those extreme stock-panic lows radically undervalued relative to gold, silver had rocketed 442.9% higher in 2.4 years! And that massive run didn’t simply stop at a 55x SGR, but instead the huge buying momentum drove a proportional upside overshoot. The SGR peaked at 31.7x, which was 4/5ths as far above that long-term 55x mean as the SGR was below it at stock-panic lows. This principle is crucial.

After longstanding price relationships driven by some kind of inexorable fundamental or psychological links are forced to extremes, they don’t just mean revert. That reversion momentum blasts them right through their average to overshoot proportionally towards the opposing extreme! This behavior is very pendulum-like. The farther the SGR is pulled one way, the stronger its swing towards the other side of the arc.

Interestingly that massive mean-reversion-overshoot bull following 2008’s stock panic ultimately dragged the SGR high enough to average 56.9x in those post-panic years between 2009 to 2012. Despite great volatility in this ratio, it continued to gravitate towards that 55x secular mean. That persisted until early 2013 when the Fed’s unprecedented open-ended third quantitative-easing campaign greatly distorted markets.

That year alone the Fed conjured $1020b of QE capital out of thin air to inject into the markets! That forced the flagship US S&P 500 broad-market stock index 29.6% higher that year. Such blistering gains made investors forget about gold and silver, so they fell precipitously. That shattered fragile sentiment leading to multi-year bear markets in the precious metals. Silver leveraged gold’s downside like usual.

Thus the SGR slowly collapsed between early 2013 to early 2016 as gold and silver languished in Fed-driven bear markets. That was a very-challenging time psychologically, scaring away the great majority of contrarian speculators and investors. Ultimately silver plunged so far that the SGR fell to 83.2x at worst in late February 2016. That was an extreme low rivaling the 2008 stock panic’s, which truly defies all reason.

Again such SGR extremes weren’t sustainable, so silver blasted higher with gold and amplified its gains in roughly the first half of 2016. Unfortunately that new-bull upleg was cut short, capping silver at mere 50.2% gains and the SGR at 65.9x. Silver’s typical mean reversion out of extreme SGR lows was indeed underway, but unfortunately it was short-circuited by Trump’s stunning surprise election victory that November.

The stock markets started surging on hopes for big tax cuts soon with Republicans controlling the House, Senate, and presidency. So stock traders dumped gold-ETF shares which hammered the gold price and sucked silver down with it. Silver continued underperforming gold on balance until late November 2018 and that latest extreme 86.3x SGR low. Silver both fell faster than gold and rallied slower than it over this span.

Again that crazy nearly-quarter-century low in silver prices relative to gold prices was more extreme than both during late 2008’s stock panic and after late 2015’s secular low. Shockingly the SGR average since Q4’15 is now running 76.2x, which is actually worse than the 75.8x in the four months in late 2008 hosting that stock panic! Silver has languished far too low relative to gold in recent years, an unsustainable anomaly.

That guarantees a massive mean reversion higher for silver as gold’s young upleg continues to unfold. Seeing gold power higher on balance will motivate speculators and investors to redeploy into silver, which will fuel outsized gains in the white metal. That process is already underway, as proven by silver’s sharp gains relative to gold straddling the dawn of this new year. Silver is starting to outperform gold and mean revert!

Let’s assume the worst-case scenario, a silver upleg that fizzles prematurely due to an exogenous shock like Trump’s election win was back in late 2016. If the SGR merely revisits 65x, at $1250 gold that would mean silver near $19.25. While that’s only a 38% upleg from the mid-November lows, it is still well worth riding. At $1300 and $1350 gold, that very-low 65x SGR would yield silver prices near $20.00 and $20.75.

But with the stock markets almost certainly rolling over into a major new bear, it’s unlikely gold’s upleg will be truncated small again. As long as stocks generally weaken, gold investment demand will remain high driving up gold prices. That will keep traders excited about silver, chasing its gains and bidding it ever higher. It’s hard to imagine the SGR not at least mean reverting to its 55x secular average in this scenario.

At 55x and $1250, $1300, and $1350 gold, silver would power up near $22.75, $23.75, and $24.50. Such levels would make for a total silver upleg of 63%, 70%, and 75% from those deep mid-November lows. So even without a proportional overshoot, silver’s upside potential is big after being hammered to such deep lows relative to gold. Some magnitude of mean reversion higher is certain after such extreme SGR lows.

It would take a major gold upleg running for a couple years to fuel an SGR overshoot. In essentially the first half of 2016, this gold bull’s first upleg powered about 30% higher. That is actually on the small side by historical gold-upleg standards. Apply it to gold’s deep mid-August lows driven by record short selling in gold futures, and that yields an upleg target near $1525. That would work wonders for silver sentiment.

Once gold breaks decisively above its bull-to-date peak of $1365 from July 2016, excitement will explode driving outsized self-feeding investment demand. That should fuel a proportional mean-reversion overshoot in silver. Silver far outperforming gold as capital flooded in could even push the SGR up near 35x briefly. While such an upside extreme wouldn’t last any longer than downside ones, silver would soar.

At $1400, $1450, and $1500 gold, a mean-reversion-overshoot SGR of 35x would catapult silver way up near $40.00, $41.50, and $42.75 per ounce! That implies silver upleg gains ranging from 186% to 206% from mid-November’s low. The key takeaway here is after extreme SGR lows, silver’s resulting mean-reversion gains can grow massive. Silver far outperforms gold for a long time after underperforming for years.

That inevitable outperformance already started through late December and early January, when the SGR recovered sharply from 86.3x to 82.0x. That rapid rebound in silver prices is a strong indication that a major mean reversion is now underway. And history proves that once silver starts moving, it tends to rally fast as momentum builds. Buying begets buying, with higher silver prices fueling larger capital inflows.

As always the biggest gains will be won by the fearless contrarians who buy in early before everyone else figures this out. Investors and speculators alike can play silver’s big coming upside in physical bullion, its leading SLV iShares Silver Trust silver ETF, and the silver miners’ stocks. But only the latter will leverage silver’s gains, making them exceptionally attractive. Consider their example from that last major silver upleg.

Again in 7.6 months in mostly the first half of 2016, silver powered 50.2% higher before Trump’s surprise election win short-circuited that rally. The leading SIL Global X Silver Miners ETF rocketed an immense 247.8% higher in essentially that same span! That made for huge 4.9x upside leverage to silver’s gains, which is pretty awesome. The major silver miners’ stocks will amplify silver’s upside in its next big upleg too.

At Zeal we recognized the extreme anomalous lows in the SGR in late 2015 and early 2016 and deployed aggressively in both gold and silver stocks. The resulting gains were outstanding, with the stock trades in our popular weekly and monthly newsletters averaging +111.0% and +89.7% annualized realized gains in 2016! We’ve filled our trading books again in recent months in anticipation of the next big gold and silver uplegs.

To multiply your wealth in the stock markets, you have to do your homework and stay informed. That’s where our newsletters really help. They draw on my decades of experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. I study the markets all day everyday so you don’t have to. Subscribe today and enjoy the fruits of our hard work for just $12 per issue!

The bottom line is silver has started outperforming gold again. After getting pummeled near a quarter-century low relative to gold, silver started surging late last year. Following past extreme SGR lows, silver powered higher in major-to-massive mean-reversion uplegs and bull markets. Their advents have been signaled by silver beginning to rally faster than gold after suffering long periods of underperformance.

That’s now happening again, which is a super-bullish omen for silver. Capital inflows are accelerating as gold’s gains restore more-favorable sentiment. As long as gold continues meandering higher on balance, silver buying will beget more silver buying. That portends big gains coming in silver and especially the stocks of its miners. Silver mean reversions higher out of extreme lows relative to gold can run for years.

Adam Hamilton, CPA

February 4, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

The gold miners’ stocks have slumped in January, tilting sentiment back to bearish. This sector’s strong December upward momentum was checked by gold’s own upleg stalling out. Gold investment demand growth slowed on the blistering stock-market rally. But uplegs always flow and ebb, and this young gold-stock upleg merely paused. The gold miners’ gains will likely resume soon, rekindling bullish psychology.

Most investors and analysts track the gold-mining sector with its leading ETF, the GDX VanEck Vectors Gold Miners ETF. GDX was this sector’s pioneering ETF birthed in May 2006, creating a huge first-mover advantage that is insurmountable. This week GDX’s net assets of $9.9b were an incredible 56.7x larger than the next-biggest 1x-long major-gold-miners ETF! GDX dominates this space with little competition.

Back in early September, the gold stocks plunged to a major 2.6-year secular low per GDX. This sector suffered a brutal forced capitulation on cascading stop-loss selling, devastating sentiment. The triggering catalyst was gold getting pounded to its own major lows in mid-August on record futures short selling. At worst GDX fell to $17.57 on close, which was down an ugly 24.4% year-to-date. Most traders fled in disgust.

But major new uplegs are born in peak despair, and that was it. The gold stocks started recovering out of those fundamentally-absurd levels, gradually carving a solid upleg. By early January GDX had rallied 22.3% higher in 3.7 months, fueling more-optimistic sector sentiment. Plenty of speculators and investors including me were comparing 2019’s setup for gold stocks to the first half of 2016, a wildly-lucrative stretch.

That was just after today’s gold bull ignited, and its maiden upleg surged 29.9% higher in just 6.7 months. Such gold strength ignited a flood of capital into the gold miners, catapulting GDX an enormous 151.2% higher in essentially that same span! This year when GDX’s latest closing upleg high of $21.48 was achieved on January 3rd, traders were salivating at the prospects of another mighty H1’16-like gold-stock upleg.

But instead of powering higher, the gold stocks stalled and started drifting lower. By last Friday the 18th, GDX had slumped 5.4% over a couple of weeks or so to $20.31. That really discouraged the gold-stock traders, torpedoing the nascent bullishness driven by GDX’s powerful 10.5% December rally. I’ve been getting lots of e-mails from discouraged traders moping, and often convinced this gold-stock upleg fizzled.

Sentiment has really deteriorated in recent weeks as gold-stock prices retreated. One manifestation of this resurgent bearishness is apparent in how individual gold miners’ stocks are reacting to company-specific news. Early in new quarters, many gold miners report their prior quarter’s production. And early in new years, plenty also give guidance for new full-year production. Traders are selling hard on this news.

Even though these production reports and outlooks have generally been flat to good, they are being used as excuses to sell. When traders wax bearish, all news is considered bad. So when pessimism reigns early in new quarters, it’s not unusual to see traders flee. Conversely when gold stocks are rallying nicely early in new quarters, this news is typically bought. Gold stocks’ reaction to news is a sentiment indicator.

Interestingly selling on full-year production guidance is usually a poor decision. Gold-miner managers try to maximize their compensation which is heavily driven by their stock’s price. So they tend to lowball their production estimates early in new years, leaving room to beat them later in those years. Then when they exceed their own expectations, their stocks catch strong bids into year-ends maximizing their personal earnings.

Plenty of traders have written me worrying that January 2019 is nothing like January 2016, arguing that a major new gold-stock upleg isn’t underway. They are dead wrong, everyone forgets the gold stocks also fell in much of that pivotal month. In the first couple weeks of January 2016, GDX actually dropped 9.1% despite a parallel 2.5% gold surge! Then like now, emotional gold-stock traders were irrationally scared.

That monster H1’16 gold-stock upleg didn’t start until January 20th that year, which was that month’s 12th trading day. That was after most of the post-quarter and new-year news releases. This year’s slump is actually better, not worse. GDX was only down 3.7% month-to-date on this month’s 13th trading day, on gold’s slight 0.1% drift lower over that span. Early-year weakness doesn’t preclude major uplegs brewing!

While most traders want to assume otherwise, gold stocks’ young upleg remains very much alive and well. This chart is updated from my essay several weeks ago heralding GDX’s major upside triple breakout, a super-bullish technical event. While GDX did slump in recent weeks after achieving that, its upleg is still rock-solid. All uplegs meander higher in fits and starts, taking two steps forward before one step back.

I’m not going to rehash this chart after analyzing it in depth just a few weeks ago. But scared gold-stock traders can take solace in some brief observations. First note the early-January-2019 pullback in GDX is far less severe than the early-January-2016 one. While that month birthed a monster upleg, it wasn’t all rainbows and unicorns until the very end. Weak-handed excitable traders had to be shaken out before the surge.

Second look at GDX’s solid upleg since early September 2018, which again rallied 22.3% at best over 3.7 months as of January 3rd. Uplegs are simply series of higher lows and higher highs often unfolding in a defined uptrend channel. All that still perfectly applies to GDX, its technicals remain very bullish. Both its upleg lows and highs are gradually marching higher, revealing zero technical strain on this young upleg.

Once again this upleg was born at GDX’s deep 2.6-year low of $17.57 on September 11th. Over the next few weeks into early October, GDX surged 8.4% to $19.05. Then it quickly pulled back to $18.39, which was still 4.7% above upleg-start levels. From there GDX powered up another 9.3% over the next couple weeks to $20.10 in late October. Then it suffered a bigger retreat to $18.42 by mid-November, still a higher low.

GDX rebounded strongly from there, surging another 16.6% to $21.48 by early January. And after such a strong run it slumped again to $20.31 last Friday. While it remains to be seen if that proves the latest upleg low, the higher lows so far have run $18.39, $18.42, and $20.31. And the higher highs clocked in at $19.05, $20.10, and $21.48. This is a textbook-perfect gold-stock upleg so far, offering nothing to worry about.

These higher lows and higher highs have formed an excellent uptrend channel for this upleg. Connecting these lows and highs creates parallel lower-support and upper-resistance lines. I didn’t draw them in this chart because they’d be difficult to see at this scale, but they are really well-defined. As of this week the support line extends near $19.50. So even if GDX slumped that low, its uptrend channel would remain intact.

Resistance now projects near $21.75, which would be another new upleg high. Odds are GDX will head back up there to challenge it in the coming few weeks or so. GDX may have started bouncing from last Friday’s level a bit under its 200-day moving average, which is now running $20.65. It could head a little lower first to its 50dma which is down near $20.14. And maybe it will even drop to $19.50 lower support.

It’s important to realize that as long as GDX remains above that uptrend-channel support line, its upleg is just fine. Any action over that is merely upleg noise that isn’t worth worrying about technically. It is normal for pullbacks within uplegs to bleed away bullishness and rekindle bearishness. That’s actually essential for uplegs’ health and longevity, keeping sentiment balanced so uplegs don’t prematurely burn out.

All the upside triple-breakout analysis and bullishness I discussed in early January remains valid and in force today. This gold-stock upleg has just paused, which is par for the course. All uplegs flow and ebb, gradually meandering higher on balance. None shoot up in straight lines, not even that monster one in H1’16. That was riddled with multiple strong selloffs, with one even hitting support below GDX’s 50dma.

The reason this young gold-stock upleg paused in recent weeks was gold’s own upleg stalled out. Gold miners’ stocks are ultimately just leveraged plays on gold. Their profits really amplify changes in gold’s price, which lets major gold miners’ stocks leverage gold’s underlying moves by 2x to 3x. Gold’s own young upleg that is driving gold stocks’ one hit its latest high near $1294 in early January the same day as GDX.

At that point gold had rallied 10.2% upleg-to-date, which GDX’s 22.3% upleg leveraged by a normal 2.2x in a similar span. Gold had bottomed a few weeks before the gold stocks, in mid-August instead of early September. Gold stocks’ performance relative to gold in this upleg has been normal. That leverage is often on the low side of its range early in young uplegs, then climbs to the high side later as momentum mounts.

At worst since its own January 3rd high, gold had slumped 1.0% to $1280 on last Friday. It is certainly no coincidence that is the exact span of gold stocks’ latest pullback. GDX’s young upleg will resume as soon as gold catches a bid again. That is dependent on gold investment demand resuming. It was strong in Q4, but faded significantly in January. This next chart looks at the leading proxy for gold investment demand.

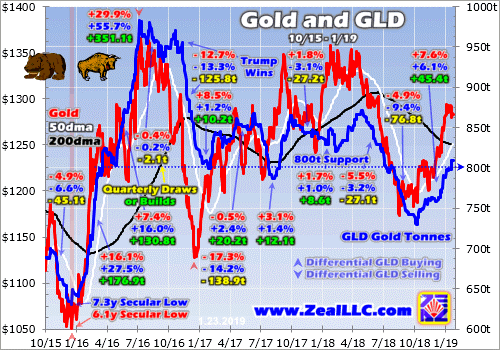

That is the physical bullion holdings the dominant GLD SPDR Gold Shares gold ETF holds in trust for its shareholders. They are reported daily, a far-higher-resolution read than the quarterly supply-and-demand data from the World Gold Council. In last week’s essay I explained this chart in depth, analyzing why the capital flows into and out of GLD alone by American stock investors overwhelmingly drive the global gold price.

It superimposes GLD’s bullion holdings in blue over the gold price in red. Rising GLD holdings show that American stock-market capital is moving into gold via the conduit of this leading gold ETF. In Q4 and especially December gold surged higher on heavy differential buying of GLD shares. But in January that GLD buying has moderated. That’s why gold’s advance stalled out, which in turn drove gold stocks’ pause.

Again I discussed this chart just last week, so there’s no need for more comprehensive analysis. For our purposes today, note how GLD’s holdings climbed modestly in October and November after they had fallen to a deep 2.6-year secular low of their own in early October. GLD had suffered 5 consecutive monthly draws of 24.2 metric tons, 28.0t, 18.8t, 45.0t, and 12.9t between May and September, an ugly streak.

But that trend of American stock-market investors selling gold via GLD shares ended in early October. GLD enjoyed its first big build the very day the US stock markets suffered their first sharp plunge! That snowballed into an 11.8t build in October and 7.7t in November. That investment buying fueled modest gold rallies of 2.1% and 0.5% those months. Then in December that GLD-share buying really accelerated.

Last month enjoyed a sizable 25.9t build in GLD’s holdings, the biggest since September 2017. Those capital inflows fueled a much-larger 4.9% gold rally in December. When investment capital is flowing into gold, its price naturally climbs. And that in turn drives the gold miners’ stocks higher. Gold’s 2.1%, 0.5%, and 4.9% gains in the last several months drove parallel 2.2%, 0.8%, and 10.5% monthly rallies in GDX.

On the surface January has looked good too, with GLD’s holdings surging another 22.1t month-to-date as of the middle of this week. But nearly 9/10ths of that build came on only 2 trading days, January 2nd and 18th. Out of 15 trading days so far, January has seen 4 GLD-holdings build days, 3 draw days, and fully 8 unchanged. American stock investors’ differential GLD-share buying hasn’t been consistent this month.

That’s enabled gold-futures speculators to push gold modestly lower. Unfortunately we can’t know how much selling they’ve done, or whether it was exiting longs or adding new shorts, because of the federal-government partial shutdown. The weekly Commitments of Traders reports usually published by the CFTC haven’t been released since mid-December, so there is no data on gold-futures speculators’ trading.

But gold drifting lower this month despite a solid GLD build on balance proves they have to be selling. A sharp bounce in the US Dollar Index is a major factor driving those gold-futures sales. But the main one is the surging US stock markets. They are really retarding gold investment demand, making investors forget the wisdom of prudently diversifying their stock-heavy portfolios with gold. That has paused gold stocks.

The flagship U.S. S&P 500 broad-market stock index (SPX) plunged 19.8% over 3.1 months between late September and late December, a severe correction nearly entering bear-market territory. It was that SPX drop that reignited gold investment demand and fueled gold’s latest young upleg. Last week’s essay dug into this critical relationship between the SPX and gold. The SPX’s sharp rebound since weighed on gold demand.

Between the SPX’s Christmas Eve near-bear low and last Friday, this leading index rocketed up 13.6% in just several weeks! That violent bounce that looked and felt exactly like a bear-market rally nearly erased 4/7ths of the preceding correction. That has reignited widespread greed and complacency in the stock markets, the exact mission of bear rallies which are the biggest and fastest seen in all of stock-market history.

Gold stalled out in January because the SPX is surging so fiercely, retarding the impetus to diversify with gold. And the gold-stock upleg paused because gold stopped advancing. So this probable bear rally in the stock markets is to blame for gold stocks’ early-year weakness. But once these overbought U.S. stock markets roll over decisively again, gold psychology will flip back to favorable and big investment buying will resume.

When gold starts powering higher again, gold stocks will be off to the races. That portends big gains still coming in GDX, and even larger ones in its little brother GDXJ. It is effectively a mid-tier gold miners ETF these days, and its upleg gains during recent years’ bull market have outpaced GDX’s by about 1.4x on average. GDXJ simply has a better mix of gold miners than GDX, with fewer problems expanding production.

Yet the best gains by far won’t be won in the ETFs, but in the smaller mid-tier and junior gold miners with superior fundamentals. GDXJ still has deadweight in its top holdings, miners struggling with declining production and rising costs. The better gold miners are growing their output through new mine builds and expansions, generating greater gains. Finding and owning these better gold-mining stocks is essential.

The earlier you get deployed, the greater your gains will be. That’s why the trading books in our popular weekly and monthly newsletters are currently full of better gold and silver miners mostly added in recent months. The gains we won in 2016 were amazing the last time American stock investors returned to gold. Our newsletter stock trades that year averaged +111.0% and +89.7% annualized realized gains respectively!

The gold-stock gains should be similarly huge in this next major gold upleg. The gold miners are the last undervalued sector in these still-very-expensive stock markets, and rally with gold during stock-market bears unlike anything else. To multiply your wealth in the stock markets you have to do your homework and stay abreast, which our newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. You can subscribe today for just $12 per issue!

The bottom line is this young gold-stock upleg is just paused. The current technicals certainly don’t justify increasingly-bearish sentiment. This sector’s leading benchmark GDX is carving higher lows and higher highs, climbing on balance in a well-defined uptrend channel. Uplegs don’t shoot higher in straight lines, pullbacks within them are normal and expected. They serve to rebalance sentiment keeping uplegs healthy.

Gold stocks’ pullback this month was driven by gold’s own young upleg stalling. Strong gold investment demand fueled by recent months’ serious stock-market selloff moderated after stocks screamed higher in a violent bear-market-rally-like bounce. The resulting rekindled bullish psychology overshadowed gold again. But once stock-market selling resumes, so will the young uplegs in gold and its miners’ stocks.

Adam Hamilton, CPA

January 29, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Gold investment demand reversed sharply higher in recent months, fueling a strong gold rally. The big stock-market selloff rekindled interest in prudently diversifying stock-heavy portfolios with counter-moving gold. These mounting investment-capital inflows into gold are likely to persist and intensify. Both weaker stock markets and higher gold prices will continue to drive more investment demand, growing gold’s upleg.

Early in Q4’18, gold reached a major inflection point. It languished during the first three quarters of 2018, down 8.5% year-to-date by the end of Q3. Investors wanted nothing to do with alternative investments with the stock markets powering to new record highs. The flagship S&P 500 broad-market stock index (SPX) had rallied 9.0% in the first 3/4ths of last year. That left gold deeply out of favor heading into Q4.

But a critical psychological switch was flipped as the SPX started sliding last quarter. After long years with little material downside, stock traders had been lulled into overpowering complacency. They were shocked awake as the SPX plunged 14.0% in Q4, its worst quarter since Q3’11. They poured back into gold as stocks burned, driving it a strong 7.6% higher in Q4! Rekindled investment demand was the driver.

Unfortunately gold investment demand is rather murky. Gold is bought and sold every day all over the world, in countless venues ranging from major exchanges to tiny third-world merchants. Tracking even the majority of this in real-time is impossible. The best-available data on global gold investment comes from the World Gold Council. But it is only published once per quarter, about a month after quarter-ends.

I can’t wait to see the WGC’s new Q4’18 Gold Demand Trends report due out in early February. These quarterly GDTs are very well done and essential reading for all investors. But while detailed and informative, their resolution is really low only being released 4 times per year. Investors need alternative data sources to understand and game what’s going on with gold investment demand between the GDTs, like now.

Thankfully there’s an excellent proxy of investors’ capital flows into and out of gold published daily, a high-resolution read. It is the physical gold bullion held in trust for the shareholders of the world’s dominant gold exchange-traded fund. That of course is the American GLD SPDR Gold Shares. GLD was created and launched by the World Gold Council way back in November 2004, and has grown into a gold juggernaut.

As part of the WGC’s GDT work each quarter, it tracks the world’s top 10 physically-backed gold ETFs. At the end of Q3’18 when you could hardly give away gold to American investors, GLD’s holdings still accounted for nearly 32% of the world’s top-10 gold-ETF total. Add in the 2nd-largest ETF which is also American, the IAU iShares Gold Trust, and these two leading ETFs control over 3/7ths of the global top-10 total.

The primary constituency for American gold ETFs is American stock investors. So what they are doing in terms of capital flows through GLD especially is exceedingly important for gold. In recent years most of the major quarterly moves in gold prices are nearly fully explainable by GLD’s holdings alone! They must be watched daily, as changes in them have proven the key to gold’s fortunes. It’s important to understand why.

The American stock markets are the biggest in the world, and American investors’ capital is vast beyond compare. At the end of Q3’18, the collective market capitalization of the 500 elite SPX stocks alone was a staggering $26,141.4b. By comparison, GLD’s total physical-gold-bullion holdings of 742.2 metric tons were only worth $28.4b. That’s less than 1/9th of a single percent, which for all intents and purposes is zero.

Thus if even the tiniest fraction of U.S. stock-market capital migrates into or out of GLD shares, gold itself moves big. This dominant gold ETF effectively acts as a conduit between stock-market capital and gold. But as these colossal pools of capital slosh into and out of GLD, it is always at risk of failing its mission of tracking the gold price. The supply and demand of GLD shares and gold are independent of each other.

So differential buying or selling of GLD shares by American stock investors must be directly equalized into the underlying global gold market. This mechanism is simple in concept. When GLD shares are being bought faster than gold itself, this ETF’s price threatens to decouple from gold’s price to the upside. To prevent this, GLD’s managers need to shunt that excess GLD-share demand directly into gold in real-time.

They issue enough new GLD shares to offset that excess demand, and then use the proceeds to buy physical gold bullion held in trust for GLD’s shareholders. So when GLD’s daily holdings are rising, that reveals American stock-market capital is flowing into gold. This GLD capital pipeline into gold also works similarly on the downside, when American stock investors dump GLD shares faster than gold is being sold.

GLD’s share price will soon disconnect from gold’s price to the downside. This ETF’s managers avoid that by buying back GLD shares to sop up the excess supply. They raise the capital to do this by selling some of GLD’s physical-gold-bullion holdings. So when GLD’s daily holdings are falling, American stock-market capital is being pulled back out of gold. These holdings closely mirror world gold-investment trends.

My chart this week compares GLD’s daily gold holdings in metric tons with the gold price over the past several years or so. After falling to a major 6.1-year secular low in December 2015, gold started powering higher in a new bull market. Since gold hasn’t retreated 20%+ from its bull-to-date peak in July 2016, this bull remains alive and well. It has been overwhelmingly driven by American stock-market capital flows via GLD.