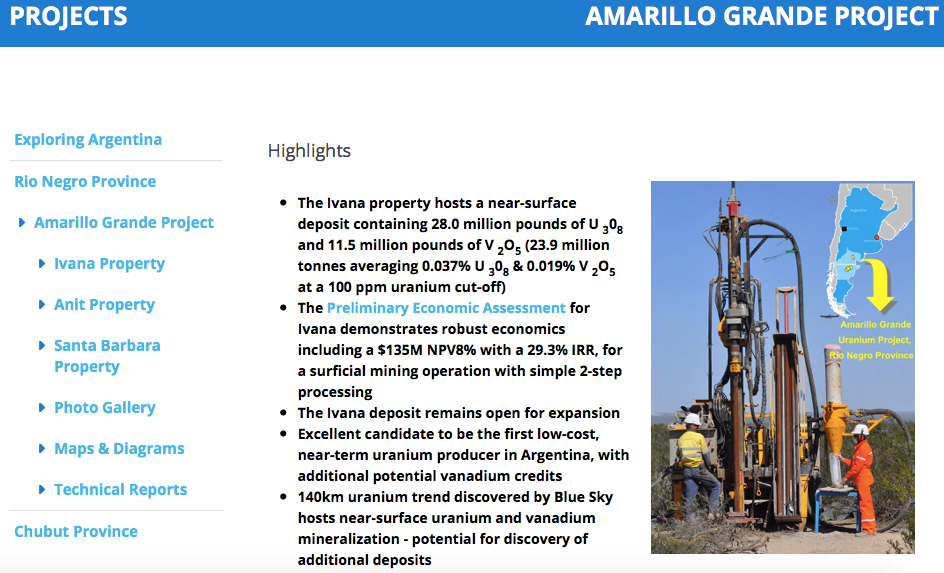

In February, Blue Sky Uranium (TSX-V: BSK; OTC: BKUCF) delivered a very positive Preliminary Economic Assessment (“PEA“) on the Ivana uranium-vanadium deposit at the Company’s 100%-owned Amarillo Grande project in Argentina. The after-tax IRR & NPV is 29.3% & $135M. The upfront cap-ex is estimated at $128M. Importantly, the all-in sustaining cost is estimated to be in the lowest quartile of the global cost curve, at $18.27/lb. The resource contains nearly 23M pounds uranium, plus 12M pounds vanadium. These indicative economics are based on just a 13-yr. mine life. The metrics are strong, but they could get even better. CEO Niko Cacos has stated in recent interviews that the next C$2-$3M capital raise (probably in May) will fund them into the 4th quarter, and pay for well over 100 shallow drill holes that could potentially double the resource size.

The Company is well on its way to a larger resource. On April 29, Blue Sky Uranium reported,

“additional high-grade uranium & vanadium results from pit sampling carried out in the area immediately west of the Ivana Uranium-Vanadium deposit, at the Company’s wholly-owned Amarillo Grande Project in Rio Negro, Argentina. This newly-identified near-surface mineralization is open to expansion, as indicated on Figure 1, (https://bit. ly/2IZknLO) but drilling is required for further testing as the target zone is interpreted to be at greater depth in adjacent areas.”

Doubling the resource would provide a strong foundation for a blockbuster Pre-Feasibility Study (“PFS“) next year. Ultimately, management believes there’s potential for > 100 M pounds uranium, which might include > 50 M pounds vanadium. That would take longer to drill out, so I’m assuming a doubling in the next 9 months and a PFS completed in about a year from now. In my opinion, all else equal, a PFS could show an after-tax IRR > 35% and all-in sustaining costs of $16-$17/lb. The mine life could be extended to 20+ years, or annual production of uranium + vanadium in the initial 10 years could be significantly increased.

Therefore, if management is correct in their belief that a doubling of the resource is possible by 1H 2020, then the current market cap of C$20M = US$15M could be an attractive entry point. If over a longer time frame the Company could triple, quadruple or quintuple the current resource, then instead of bottom quartile costs, they could be looking at a project in the bottom decile. However, they don’t need to spend the time & money this year or next to get anywhere near 100 M pounds of uranium on the books. They have to deliver a strong PFS and then assess the uranium market at that time. If the market has improved, I think that Blue Sky could start production by 2022.

Uranium & vanadium prices over the past 6 months have had a negative impact on company share prices. Uranium bottomed at about $17.5/lb. in 2016, but rebounded to a bit over $29/lb. in Q4 of last year. Sentiment started to shift, momentum seemed to be gaining, but the spot price stalled. It now sits at close to $26/lb. Likewise, vanadium had a tremendous run, from about $3/lb. 3 years ago to just shy of $34/lb. in early November, 2018. Since then vanadium pentoxide (China price) has fallen to ~$12/lb., down 65%. As an aside, cobalt is off about 62% from its 52-week high.

Most analysts & industry pundits believe that both vanadium & uranium prices are headed higher by year-end and higher again in 2020. For vanadium, a price between $10-$20/lb. could be the new normal. Blue Sky doesn’t need a high vanadium price, it’s just icing on the cake. At $10/lb., it doesn’t help project economics all that much. At $20/lb. it has a moderately favourable impact. The PEA uses a $15/lb. price assumption.

Everyone talks about the spot price when they discuss uranium. The spot price is ~$26/lb., but the long-term contract price is quoted at $32/lb. {See Cameco’s pricing page}. Notice that the spread between contract & spot prices over the past 4.25 years ranged from 7% to 89% and averaged 37%. Currently the spread is about 23%. All Blue Sky needs to start production early next decade is $10/lb. more in the spot price, which would likely translate to a contract price in the mid $40’s/lb. The Company doesn’t need that price this year, or even next year. Early 2021 would be perfect timing.

According to the PEA, Blue Sky’s Project has a 20% IRR at $40/lb., and that will likely improve in the upcoming PFS.

It’s not rocket science to understand why prices should rise…. Utilities have been on the sidelines for years, buying in the spot market, letting uranium inventories shrink, because they are not worried about re-supplying. All of that will change beginning next year, and more in 2021-2022. In fact, in 2021-25 global utilities are most exposed to a potential spike in prices (they’re increasingly un-contracted). Blue Sky could time the market perfectly by commencing production in 2022. Of the 60-80 uranium juniors, how many could possibly be in production as soon as 2022? I’m thinking less than 6. Why so few? Most are at exploration stage in jurisdictions where it routinely takes 5 to 15 years to reach production, (if ever). Many can’t raise capital, so their projects are dead in the water.

And, for those who are more advanced, if they require a minimum of $50+/lb. to get off the ground, they could be stalled as well. Once the market realizes that a) uranium prices are headed higher, (but not necessarily to $50+/lb. anytime soon), b) an ideal time to enter production would be in the first half of next decade, and c) sustainable low cost & security of supply will be critically important — there could be a tsunami of capital pouring into just a handful of uranium juniors. Blue Sky Uranium would likely be one of the first to benefit. And, with a market cap of just US$15M, it could become an attractive takeover target.

I mention security of supply, the Section 232 Petition in the U.S. makes it clear that uranium imports into North America & Europe, are increasingly from State-owned or controlled enterprises in adversarial countries like Russia and its allies, or countries heavily influenced by China. Energy Fuels states in a recent press release that, “greater than 60% of newly mined uranium now comes from State-owned enterprises that unfriendly nations own or control.”

If or when the U.S., the largest consumer of uranium in the world, faces a challenge in obtaining uranium, even if it starts to look like there might be a problem…. utilities will be anxious to source uranium from safe havens. Argentina certainly qualifies as a safe haven. Management has been operating natural resource companies in Argentina for well over 20 years, they have extensive contacts and vast experience in the country. They believe that first production could be in 2021, I’m saying 2022 to be conservative. Whether it’s 2021, 2022 or 2023, that’s still near-term production compared to the vast majority of uranium peers, most of whom need $50+/lb. uranium or are in jurisdictions known to take a long time to advance projects into production.

Fewer than 6. That’s right, I said fewer than 6 uranium juniors could reach production by 2022, if the long-term contract price remains below $50/lb. Think about that for a moment. By contrast, there are over 300 cannabis-hemp related companies listed in Canada and/or the U.S. A lot of those companies will be viable or will be acquired. It’s really hard to pick the best cannabis plays, but if one wants to place a bet on uranium, Blue Sky Uranium deserves to be high on the list of names to consider.

Peter Epstein

May 3, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Blue Sky Uranium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Blue Sky Uranium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of Blue Sky Uranium and Blue Sky was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) is a great name. The Company is defending against Chinese dominance of Rare Earth Elements (“REEs“), and Defense Departments require select REEs to defend their countries! Several REEs are very difficult or impossible to replace in critical applications, yet enable products essential to modern civilization. Any company outside of China that can reliably produce a few key REEs will have a license to print money. This week, SGS Canada provided select head assay results from a 30-tonne bulk sample. Four REE assays were reported in this press release {see chart below}. Using the price/kg of each metal, the in-situ value is ~US$ 535/t. That’s equivalent to ~ 0.41 troy ounces Gold or ~12.8 g/t Gold.

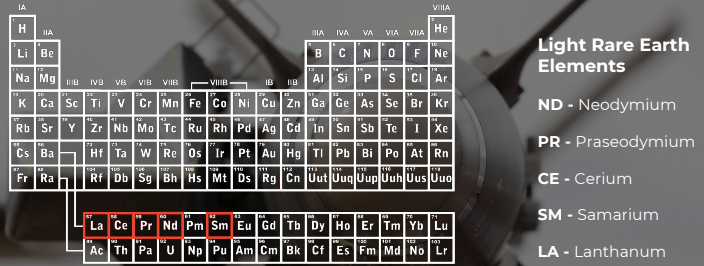

In the following interview of CEO Max Sali, readers will learn more about REEs and about Light Rare Earth Elements (“LREEs“), which REEs are in highest demand, and for which applications. Spoiler alert, Neodymium & Praseodymium are in the top 4 or 5. I asked Max why his team believes that its deposit of LREEs might be economically viable given the odds stacked against any deposit becoming a mine. To finish off, we discussed some early-stage uranium assets the Company picked up in the famous Athabasca basin. {Corporate Presentation}

Please give readers the latest snapshot of Defense Metals.

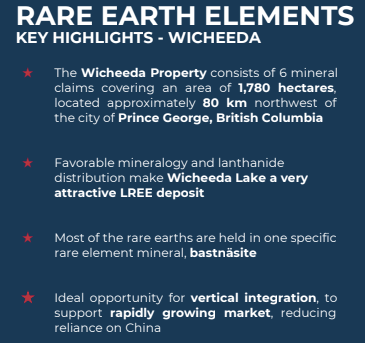

Sure. Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) is focused on sourcing, exploring and developing rare earth & uranium properties in Canada. Our flagship project is the Wicheeda rare earth deposit. NOTE: {here’s a good, brand new article by Rick Mills on Defense Metals}

The Wicheeda deposit (6 mineral claims, 1,780 hectares) is 80 km northwest of Prince George, in British Columbia, (“BC“) Canada, and contains potentially exploitable concentrations of Rare Earth Elements. The deposit was explored in the 1970’s & 1980’s, but received little further attention until 2008 when it was drilled by Spectrum Mining Corp. They reported an Inferred resource of 11.3 million tonnes. More recently, SGS Canada provided us with an important update on the deposit. Four REE assays from a 30 tonne bulk sample we sent them earlier this year showed significant concentrations of both Neodymium & Praseodymium.

The Wicheeda deposit is a very exciting project because we can potentially get it into production fairly quickly, especially given nearby infrastructure (roads, rail, water, power, labor, mining equipment & services). A favorable mineralogy & Light Rare Earth Element (“LREE“) distribution make the Wicheeda deposit highly attractive. Some impurities can be removed through electromagnetic separation done on site. The press release we put out this week was important because it gave us a new understanding of the deposit, {see graph below}. Total Rare Earth Oxide (“TREO“) was 4.81%, which we feel is attractive.

Wicheeda is ideally suited for open pit mining and conventional flotation to produce a REE-enriched oxide concentrate. In addition to Lanthanum, Cerium & Neodymium, we also have Praseodymium. Importantly, the deposit is open in most directions and outcrops at surface, meaning a low strip ratio and the potential for expansion. Encouraging bench-scale tests have been done, giving our team the goal of a 60%+ concentrate.

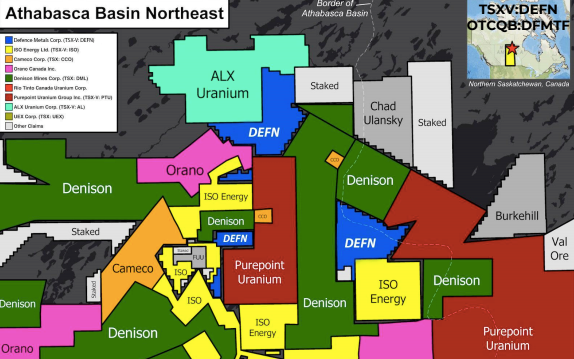

Although the main focus is our rare earth deposit, we also have 2 prospective uranium properties (5 claims blocks), in the heart of the eastern Athabasca basin near Denison Mines and IsoEnergy. Both of those companies are spending millions on drilling this year. IsoEnergy has made a new high-grade discovery 5-10 km from one of our properties.

Which rare earths are in the deposit? Which rare earths in your deposit are most valuable?

The following REEs can be found, Lanthanium, Cerium, Praseodymium, Neodymium, Samarium, Europium, Gadolinium, Yttrium & Dysprosium. There are also trace amounts of a few others. Neodymium & Praseodymium are the most valuable in the suite.

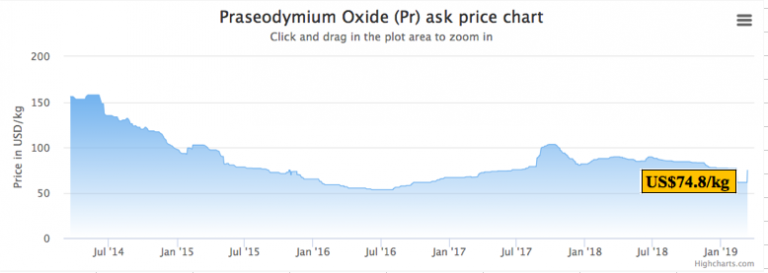

How have the prices of your most important rare earth metals trended over the past few years?

Neodymium and Praseodymium are the most important rare earth metals we have identified at the Wicheeda deposit. Neodymium (Nd) & Praseodymium (Pr) are the two rare earth elements which form the majority of rare earth permanent magnets. Below are 5-yr price charts from Kitco. The most recent prices of US$62.0 per kg for Neodymium Oxide and US$78.4 per kg for Praseodymium Oxide are down from recent highs, but up 35%-40% from mid-2016 lows.

Does management have any indicative information on metallurgy, the potential recoveries of individual metals?

Bench-scale flotation and hydrometallurgical test work was done on Wicheeda deposit drill cores at a SGS Lakefield lab during 2010/2011. SGS successfully developed a flotation flow sheet that recovered 83% of the rare earth oxide (REO) and produced a concentrate grading 42% REO. Subsequent hydrometallurgical testing in 2012 on a 2-kg sample of the concentrate grading 39.7% TREO (total REO) produced an upgraded and purified precipitate containing 71% TREO through a process of pre-leaching and roasting.

SGS Canada is well into the planned work program which includes chemical & mineralogical characterization, grindability & laboratory flotation testing on a 200-kg subsample (of the 30 tonne surface bulk sample). The objectives are to validate the process and confirm that conditions of the previously established 2010/2011 bench-scale drill core flotation test work can be upscaled to the current bulk sample; in addition to further optimization of the process flowsheet.

What will management learn from SGS Canada’s work?

As mentioned, Defense Metals delivered a 30 tonne surface bulk sample from the Wicheeda deposit to SGS Canada. SGS is conducting a multi-phase program of bench-scale metallurgical test work preparatory to commissioning larger scale flotation pilot plant testing. Larger scale pilot plant production is expected to validate bench-scale metallurgy and produce LREE product samples for potential off-take partners. The ultimate goal of the test work is to finalize the process flowsheet prior to the commissioning of larger-scale pilot plant testing. SGS has agreed to give us regular updates on its progress. In addition, Defense Metals plans to re-assay the ‘pulps’ used to produce a new 43-101 Inferred resource estimate. A Preliminary Economic Assessment (“PEA“) will follow.

Defense Metals also has uranium assets in the eastern Athabasca basin, please describe those properties.

Yes, these properties are early stage, and total nearly 10,000 hectares. We have people reviewing the historical work done on the properties, which actually comprise 5 claim blocks. We will likely do some airborne electromagnetic survey work, but to be honest, the eastern Athabasca basin is a hotbed of activity, so we may just allow our neighbors to drill around us and see what they find. Our holding costs on the properties are extremely low.

We are very pleased to have Dale Wallster join our technical advisory board. Dale is a geologist & prospector with 35 years’ experience in North American mineral deposit exploration, with a focus on the targeting & discovery of unconformity-related uranium deposits. He was President & Founder of Roughrider Uranium Corp., a company acquired by Hathor Exploration in 2006 for its strategically located uranium properties in the Athabasca Basin. Dale and his team are widely credited for the discovery of Hathor’s Roughrider deposit. In January 2012, Hathor became a wholly-owned subsidiary of Rio Tinto as part of a C$650 million acquisition.

Why should readers consider buying shares of Defense Metals?

Defense Metals (TSV-V: DEFN) / (OTCQB: DFMTF) offers an attractive, early-stage way to play the REE market. Our LREE deposit appears to be sizable and is open in multiple directions. It contains potentially economic amounts of select rare earth metals. At least 2 of the REEs, Neodymium (Nd) & Praseodymium (Pr) are quite valuable and in high demand for use in permanent magnets. There are indications that the metallurgy of the Wicheeda deposit is favorable and considerable testing is being done on metallurgy.

If the Company receives additional positive reports from SGS Canada, that could be a catalyst for our share price, as it would provide support for the thesis that we can put the project into initial production fairly quickly. While still early-stage, the Wicheeda deposit has had ample historical work done on it dating back decades, and is undergoing significant, wide-ranging testing right now. If we can advance this project in 2019 the way that we think we can, our current market cap of C$5.1 M = US$3.8 M (23.75 M shares outstanding) could prove to be an attractive entry point.

Thank you Max, that was very interesting, congratulations on the new assay results.

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Defense Metals, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Defense Metals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares in Defense Metals and it was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic. [ER] may buy or sell shares in Defense Metals and other advertising companies at any time.

By Tina Leto

The odds seem to be against uranium. Fukushima’s nuclear power plant is still disabled; the U.S. Supreme Court seems to be leaning towards staying Virginia’s moratorium on uranium mining, and projects such as Berkeley Energía’s Salamanca mine in Spain are facing major opposition.

So, why mine uranium and why now?

The answer is quite simple, actually. There is increased demand, and, after a period of volatility, prices are going up.

A series of current events are increasing demand and pushing up the value of U308. Bank of America Merrill Lynch commodities team raised its uranium concentrate price estimates for 2018, 2019 and 2020 by 3%, 22% and 32%, respectively.

Cameco CEO Tom Gitzel has a bullish look on uranium but remarked prices still have a long way to go to create some sort of optimism in the market, things are moving forward, even if it is in a slow and steady pace. The current spot price is up 40% from last year and has reached its highest level in over two-and-a-half years at around $28.75/lbs.

So, what is happening?

First, we need to take into account that, nearly eight years after the Great East Japan Earthquake, the resource-poor country has already reactivated five nuclear plants and nine reactors and has approved a 20-year operations extension for the Tokai Daini reactor located some 115 kilometres northeast of central Tokyo.

Although it is unlikely that it achieves it by 2030 as promised by the government, the Land of the Rising Sun is working towards its goal of generating a fifth of its electricity from nuclear plants in the next decade. To achieve this, of course, they will need the raw material, uranium.

Then we have China, whose uranium demand is expected to grow to around 10,800 tonnes by 2020 and rise to between 16,300 tonnes and 18,500 tonnes by 2025. The Xi administration has said it will spend $2.4 trillion to expand its nuclear power generation by 6,600% and in the near term, it plans to connect five reactors to the electricity grid and start building six to eight additional units.

In Southeast Asia, India is carrying out an aggressive growth policy reliant on nuclear power that uses both local and imported uranium. At present, the subcontinent has 22 nuclear reactors, 14 of which use foreign inputs, and it is in the process of finishing up six new units. In the next few years, 19 reactors are expected to be built.

In the Middle East, Saudi Arabia commenced reactor procurement discussions with supplier countries, as it plans to build two large nuclear power reactors and projects 17 GWe of nuclear capacity by 2040 to provide 15% of the kingdom’s power.

Canada, on the other hand, just launched its Small Modular Reactor Roadmap to promote the construction of such infrastructures, which are capable of generating up to 300 MW for small and remote communities and mines that are not connected to the electric grid.

As all of this is happening, supply is starting to see cuts given the decision by Canada’s Cameco to suspend its McArthur River/Key Lake operations in Saskatchewan, the world’s largest uranium mine, and the resolution of Kazakhstan’s state-owned Kazatomprom to lower output by 20% over the next three years as well as perform another 6% production cut over previous expectations.

*image courtesy of Bloomberg

In addition to the reduced supply, Kazatomprom recently sold 8.1 million lbs of its annual production to Yellow Cake, a new uranium holding company that raised $200 million in a London-based IPO and whose management is buying and storing large amounts of the metal in anticipation of higher prices.

Back in March, the World Nuclear Association reported that there are 448 reactors operative and 57 new reactors under construction, 158 reactors planned or on order, and another 351 proposed. The need for uranium is there and it is not going anywhere. Financial advisors believe that global consumption will grow from about 172 million lbs in 2017 to some 190 million lbs in 2019 while a supply gap should be in place by 2022-2023.

The balance seems to be slowly shifting into a deficit for the first time in more than a decade and, on top of all the cuts previously mentioned, the decision of producers like Cameco to buy larger quantities of material from the spot market going forward to fulfill long-term sales contracts will add upward pressure to the prices.

A drill hole away from a game changer

In other words, now is the time to invest in uranium stocks. With three projects underway, Azincourt Energy Corp (TSX.V: AAZ) is betting on a bright nuclear future. The primary focus of the Vancouver-based explorer and developer is its advanced exploration joint-venture with Skyharbour Resources, the 25,000+ ha East Preston Project, located in the Athabasca Basin, Saskatchewan where their team generated new drill targets to follow up after a successful geophysical exploration program.

Azincourt President and CEO Alex Klenman “These targets are similar to NexGen’s Arrow deposit and Cameco’s Eagle Point mine. East Preston is near the southern edge of the western Athabasca Basin, where targets are in a near surface environment without Athabasca sandstone cover.”

This region is gathering a lot of attention lately, especially after Skyharbour’s option partner Orano Canada (formerly Areva) announced recently that it plans to spend $2.22 million over the next year on exploration and drilling programs at the Preston project, which is right next door to the Azincourt/Skyharbour JV on East Preston.

In the next six years, big player Orano may end up investing about $6.04 million on exploration at Preston in exchange for up to 70% of the project. This is a hot zone of exploration with the Preston property and Azincourt/Skyharbour’s East Preston to be drilled at the same time. Who will make the first major discovery is anyone’s guess but, as always, it only takes one drill hole to transition from dwarf to giant.

Skyharbour President and CEO Jordan Trimble “Over the past decade, we have seen a number of notable discoveries in the Athabasca Basin. The most notable of which was made by Nexgen Energy, at their Arrow deposit (25 km away from Skyharbour and Azincourt’s East Preston Project) where they have hundreds of millions of lbs of uranium at a high grade and boast a $1B market cap.”

And Azincourt seems to be betting at growing big time in the uranium space. Besides East Preston, the company led by Alex Klenman carries 10% of the Fission 3.0 Patterson Lake North project in Athabasca, and it recently acquired three highly prospective Peruvian-based properties known as the Escalera Group.

The South American project consists of three concessions occupying over 7,400 hectares on the Picotani Plateau, which have yielded historical samples of 6500 ppm uranium and recent samples of 3500 ppm uranium. Escalera is currently undergoing a mapping and sampling program.

According to Azincourt’s management, this latter grassroots play in an emerging uranium district combined the firm’s presence in the world-famous Athabasca basin are the well-founded pillars that boost its confidence in the silvery-white metal.

About the author: Tina Leto is a seasoned Canada-based writer focusing on the resource world.

![]()

‘In order to produce half a million cars a year…we would basically need to absorb the entire world’s lithium-ion production.’ – Elon Musk

“The skillsets that young people should learn about mining should apply to everything. We just need to do a better job of explaining to people in urban environments that the human activity of mining is absolutely fundamental to the way this planet is going to evolve. Completely and totally fundamental.” – Robert Friedland, Ivanhoe Capital

The future envisioned by industry leaders hinges heavily on the production of new materials to power and build the future. Leaders such as Elon Musk have been developing the blueprint for the future with electric cars, battery grids and renewable energy solutions. While, other leaders such as Robert Friedland are looking to supply the materials to build this future. Mr. Friedland makes the case and understands the story that is unrolling in real time. Mining is the critical component to meet the world’s demands for a sustainable future. The prerequisite for this future is mining and with every mineral discovery and development project, this future is coming closer.

Mr. Friedland is not the only miner that realizes the economy of tomorrow will require the development of new mining assets. Azincourt Energy Corp. (TSX-V: AAZ) is a Canadian junior exploration company that has been actively building their mining asset portfolio in anticipation of the future demand for minerals that will provide clean energy; from lithium to uranium to cobalt.

Azincourt Energy Chairman, Ian Stalker is an experienced mining executive that sees the writing on the wall when it comes to the materials and fuel that future technology will require. Mr. Stalker is a senior international mining executive with over 45 years of hands-on experience in resource development. Over his career Mr. Stalker has directed over twelve major mining projects, from exploration drilling to start-up, including gold, base metal, uranium and industrial minerals. He is currently CEO of LSC Lithium (TSX.V: LSC), and Chairman of Plateau Uranium (TSX.V: PLU), and is the former CEO of UraMin Inc., the London and Toronto listed public uranium company that was acquired by Areva for US$2.5 billion in August 2007. In a recent press release, Mr. Stalker outlined the current strategy for Azincourt.

“The lithium market is obviously very strong right now, and the near-term future for lithium demand remains extremely positive. Our decision to expand Azincourt’s focus to include lithium and other materials is something we feel strongly about. To get a foothold and exposure in this environment, at this time, is an important and strategic step for us.”

Azincourt recently acquired five lithiums projects in located in the Winnipeg River Pegmatite Field, Manitoba, Canada. Two of the projects, the Lithium One and Two projects, are adjacent to Quantum Minerals Corp.’s Cat Lake lithium project which includes a historical estimate from drilling in 1947 that defined 545,000 tonnes of 1.4 percent lithium oxide (Li2O). Drilling could prove up this ground.

Two other of the acquired lithium projects, the Lithman West and East projects are adjacent to the Tanco Mine lease property. These projects are part of the Winnipeg River pegmatite field which hosts numerous lithium-rich pegmatites or “hard-rock” lithium such as the Tanco pegmatite that has been mined at the Tanco mine since 1969 for spodumene, a major component for hosting lithium (Li), and other rare earth ores.

Azincourt has scheduled exploration work to begin in the spring of 2018, with a field program that includes detailed mapping of the known pegmatite outcroppings on the Lithium One and Lithium Two projects. This will be followed immediately by a comprehensive chip sampling program designed to generate targets for the drill programs anticipated at both properties during the summer of 2018.

Previous work in 2016 produced twelve samples between a range of 0.02 per cent to 3.04 per cent Li2O from the Eagle pegmatite, and up to 2.08 per cent Li2O. Select sampling will concentrate on the Eagle and FD5 pegmatites at Lithium Two, and on the Silverleaf pegmatite at Lithium One, which returned values as high as 4.33 per cent Li2O in the 2016 exploration program (see press release dated Feb. 1, 2018).

On Feb. 8, 2017, the company signed a non-binding letter of intent to acquire the BullRun erythrite project, a prospective cobalt property located six kilometres northwest of the town of Cobalt, Ont. (see press release date Feb. 8, 2018). Alex. Klenman, President and CEO of Azincourt Energy commented on the company’s strategy with this acquisition.

“We’ve been looking into adding a potential cobalt property as we grow our project portfolio, so we’re pleased to move to LOI on this. We are going to immediately begin a comprehensive due diligence process to gain as much understanding as we can on the potential of the project, and we hope to progress to the definitive stage in due course. In addition, we are actively reviewing other potential projects that will continue to strengthen the company in the growing clean energy space. We haven’t filled our want list yet, so we remain very active on the acquisition front.”

True to the company strategy, Azincourt announced a new project that is adjacent to the western edge of Plateau Uranium’s (TSX-V: PLU) Macusani Project in Peru. This project contains the high-grade Falchani discovery that includes consistent 3,000-3,500 ppm Li over 100m intercepts at depth, and U3O8 grades up to 500 ppm over 50m intercepts at surface. The plateau features areas of uranium-rich surface mineralization as well as lithium mineralization at depth.

Initial leach test results conducted by Plateau Uranium in December showed that 77-80% of contained lithium can be extracted from Falchani. Plateau’s Macusani Project is fast becoming one of the world’s largest undeveloped uranium-lithium districts. Although Macusani started life as a pure uranium story, exploration and metallurgical work has unearthed the lithium resource at depth.

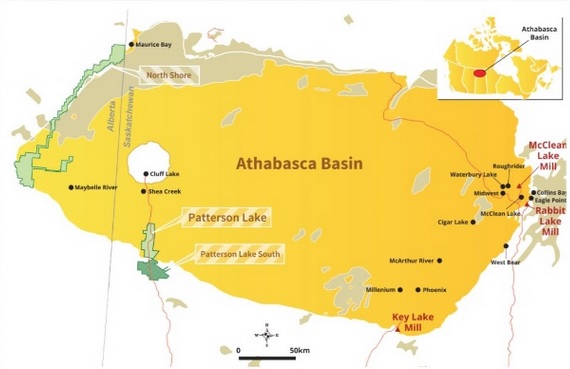

The company has been developing two projects in the Athabasca basin, in Northern Saskatchewan, home to the largest and highest grade deposits in the world, the Preston Project and the Patterson North Lake Property.

The Preston project comprises a large land position (approx. 121,249 hectares) strategically located to the south of NexGen Energy’s (TSX-V: NXE) Rook 1 project hosts the high grade Arrow deposit, as well as proximal to Fission Uranium’s (TSX: FCU) Patterson Lake South project host to the high grade Triple R deposit. The company has 15 drill target areas associated with eight prospective exploration corridors that have been successfully delineated through extensive geophysics.

The second project, The Patterson Lake North property “PLN” lies next to the northern edge of the Patterson Lake South property, owned by Fission Uranium Corp. (TSX-V: FCU) where uranium mineralization has discovered over 2.24 kilometres (east-west strike length) in four separate mineralized “zones.”

To date Azincourt has spent $3 million earning into PLN. Prior to Azincourt’s involvement, Fission spent approximately $4.7 million on exploration on PLN. There are three separate target areas that are drill-ready.

Azincourt Energy Corp. recently completed a private placement for gross proceeds of $1,655,000. In addition, the company has received an additional $1,215,009.48 in gross proceeds from the exercise of warrants over the past several weeks.

“We have more than enough funds to meet existing work requirements on our lithium and uranium projects for the next year or so, and further, the additional funding means we have upward flexibility in how we approach our work programs and portfolio expansion. Simply put, we can put more dollars into the ground, and into acquisitions,” said Mr. Klenman.

With ~69 million shares outstanding, cash in the bank, the company trading at 19 cents, the company has plenty of exploration news on the way, shares in Azincourt present a current opportunity.

While inventions and ideas grab the headlines, little attention is given to the fundamentals of building a clean energy future. Azincourt Energy Corp. (TSX-V: AAZ) has put together an impressive portfolio of mineral projects from lithium, uranium to cobalt; the minerals that will fuel the future. Azincourt Energy is in the early stages and with news on the way, investors should pay attention.

Clicker Here to Visit the Company’s Web Page: http://azincourtenergy.com/

*** The mineral reserve estimate cited above as part of the Lithium Two project is presented as a historical estimate which does not conform to current National Instrument 43-101 standards. A qualified person has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves. Although the historical estimates are believed to be based on reasonable assumptions, they were calculated prior to the implementation of National Instrument 43-101 standards. These historical estimates therefore do not meet current standards as defined under sections 1.2 and 1.3 of NI 43-101; consequently, the issuer is not treating the historical estimate as current mineral resources or mineral reserves.

***MiningFeeds.com was compensated for the creation and publication of this article. This does not constitute investment advice.

With tax-loss selling in full effect and the equity markets experiencing extreme volatility heading into the Christmas season, we take a look at uranium and the companies involved in the mining and exploration of yellow cake. What do you need to know about uranium?

In mid-2007 the price of Uranium reached over (US) $135.00 /lb, a high point for U3O8. The high price spurred expansion of existing mines, construction of new mines; and, the reopening of old mines as well as new prospecting.

Then the bubble burst and uranium beat a hasty retreat to the (US) $40.00 /lb mark. Earlier this year on March 11th, while the price of uranium was making a resurgence, Japan experienced the worst earthquake disaster in its modern history. The earthquake, a 9.0 on the richter scale, was followed by a deadly tsunami that resulted in near complete destruction of the infrastructure in northern parts of Japan and served a serious blow to the uranium market.

The Fukushima disaster certainly cast a shadow over the uranium mining industry and, these days, forecasting the spot price of uranium is akin to predicting the direction of the wind. But Dundee Capital Markets Vice President and Senior Mining Analyst, David Talbot, sees very strong fundamentals for uranium – particularly in the absence of substitutes for nuclear generation. His assessment suggests that uranium use will rise with growing populations and needs.

Talbot notes in a recent interview, “We forecast uranium prices of between $65 and $75 per pound over the next couple of years, especially once the HEU (highly enriched uranium) Agreement goes offline.”

In what was nothing short of a terrible year for the uranium industry, the end of 2011 will undoubtedly be marked by sighs of relief from uranium mining and exploration professionals around the world. With the sector beaten and bruised from the fall-out of the nuclear reactor crisis in Japan, is it finally time for a sector recovery?

As early as last summer, many analysts and investors were pondering that very question. David Talbot, an analysts at Dundee Capital Markets, remarked in a research note, “We are starting to hear a buzz in the sector – many investors are starting to realize that many of these stocks are trading well below their net asset values.” Some analysts, including Talbot, are of the opinion that, despite the Fukushima reactor meltdown, longer-term fundamentals haven’t changed for uranium and there will be more demand than supply in two to three years. However, two or three years is not the near-term as some point out. Mining investment advocate Peter Grandich noted on November 14th, 2011, that uranium stocks are “clearly a contrarian play“.

Heading into December, a month that may very well attract some significant tax-loss selling from off-side owners of uranium stocks, we take a look at the once high-flying mining subsector. Are uranium stocks radioactive gifts beneath the Christmas tree or are they just plain radioactive? From biggest to smallest we start with Denison Mines.

1. Denison Mines Corp. (TSX: DML – AMEX: DNN)

One of the few intermediate uranium producers, Denison mines combines production in the U.S. with a diversified development portfolio of projects in North America, Zambia and Mongolia. And for those who like strategic menerals, Denison also produces vanadium as a co-product from some of its mines in Colorado and Utah. The company’s most significant development project is the Phoenix deposit located in the Athabasca Basin in Saskatchewan.

The Athabasca Basin is a region of Northern Saskatchewan and Alberta Canada that is best known as the world’s leading source of high-grade uranium. The region currently supplies about 20% of the world’s uranium. The world’s largest high-grade uranium mine, Cameco’s McArthur River mine, is located in the Basin. The region has been in the headlines recently as Hathor Exploration (TSX: HAT), a junior exploration company with eleven uranium projects in the Basin, was the subject of a bidding war between Cameco (TSX: CCO) and Rio Tinto (LSE: RIO). Rio Tinto recently emerged as the winner paying $4.70 per share valuing the company at $654 million.

How does Denison Mines measure up? On September 30th, 2011 the company announced quarterly earnings of $0.04 per share. With a healthy balance sheet and a strong cash position which attributes 10% of the company’s market value, Denison is currently trading at (CDN) $1.46 for a market cap of $560 million which is right around the company’s net asset value and well below the price paid for Hathor Exploration.

2. Ur-Energy Inc. (TSX: URE – AMEX: URG)

Ur-Energy is a junior mining company focusing on exploration and development of uranium properties in the United States and Canada. On October 24th, 2011 Ur-Energy received the thumbs up from the Wyoming Department of Environmental Quality (WDEQ). WDEQ issued a permit to mine the company’s Lost Creek uranium project. The permit authorizes Ur-Energy to construct and operate the Lost Creek ISR uranium mine facilities, including the first mine unit. Construction on a two-million-pounds-per-year processing facility is scheduled to start in the summer of 2012. However, prior to mine development, Ur-Energy requires approval from the U.S. Bureau of Land Management (BLM) which it is has yet to receive.

Regardless, with the ink still wet on the WDEQ permit, Ur-Energy announced a strategic marketing arrangement with NuCore Energy. Under the agreement, NuCore will provide uranium marketing advisory and professional services with the intention of negotiate uranium off-take sales agreements for the future production derived from the company’s Lost Creek mine.

On September 30th, 2011 Ur-Energy reported $28.8 million in cash and short-term investments and liabilities of just over $2.7 million. The company’s shares are trading at around $1 per share valuing the company at just over $100 million. Dundee analyst David Talbot has a $3.25 price target on the company’s shares.

3. Uracan Resources Ltd. (TSX-V: URC)

Uracan Resources is one of many junior uranium stocks that appear to be down and out. Or is it? In 2007, with uranium prices hitting record highs, Uracan Resources hit highs of over $1.60. Today, in the aftermath of the Japan crisis, the company’s shares are trading at a mere $0.07 valuing the company at $10 million. With net liquid assets north of $5 million (over half the companies market cap) the market is deeply discounting Uracan’s mineral properties which, according to the company’s most recent financial statements, have seen almost $30 million of past exploration and development expenditures.

Uracan is lead by well-know Vancouver mining venture capital professional Gregg Sedun. Mr. Sedun is a former corporate finance lawyer with 28 years of mining industry-related experience and now heads Global Vision Capital. Global Vision Capital develops mining projects and raises expansion capital for those projects from its network of institutional and professional retail investors. Collectively, Gregg Sedun and Global Vision Capital have raised over $1 billion in support of mining venture development; which may provide investors with some comfort that Uracan, although down, may not be out.

MiningFeeds.com recently connected with Mr. Sedun for an exclusive interview – CLICK HERE – to read more.

Earlier this year on March 11th, while the price of uranium was making a resurgence, Japan experienced the worst earthquake disaster in its modern history. The earthquake, a 9.0 on the richter scale, was followed by a deadly tsunami that resulted in near complete destruction of the infrastructure in northern parts of Japan and served a serious blow to the uranium market.

With tax-loss selling in full effect and the equity markets experiencing extreme volatility as the end of 2011 draws near, we connected with Stewart Wallis of Crosshair Energy for an exclusive interview to find out what’s in store for the company in 2012.

Crosshair is a diversified mining and exploration company focused on uranium, vanadium and gold. After a difficult 2011 for the uranium sector, what is on the horizon in 2012 for your uranium projects?

In 2012 we will be focusing on our Wyoming uranium projects, Bootheel and Juniper Ridge. Both projects will have 43-101 resource updates released early in January, followed by scoping studies to be completed in the first quarter. Based on these reports, the 2012 programs will focus on permitting and additional drilling designed to aggressively advance these projects towards development.

Your Canadian uranium projects are located in the CMB Labrador and Crosshair spent $3.8 million on drilling in 2011 – what is the timeline for updating the company’s uranium resource estimates?

Crosshair maintains multiple and expandable uranium resources in Labrador. 2011 drill programs were conducted on both the CMB Uranium/Vanadium Project and the CMB Joint Venture Project, with a goal of increasing the uranium and vanadium resources as well as testing new targets outlined from earlier exploration programs. We anticipate updated resource estimates in 2012 on the CMB C-Zone/Armstrong corridor and the Joint Venture Two Time Zone.

How important is vanadium to the economics of the company’s CMB uranium/vanadium project?

We have not completed a scoping study on the CMB project so we cannot predict the actual cash benefit of the vanadium as a by-product. However, the vanadium mineralization occurs in the hanging wall of any open pit which might be developed on the uranium mineralization and we do know that the vanadium recoveries range from 13.4% to 93.6% based on our metallurgical test work in 2010. Typical recoveries range between 45-85%, and based on our metallurgical test reports a reasonable vanadium recovery of 85% was selected in our resource estimate.

Comparatively speaking there are quite a few uranium companies that are trading at or near 52 week lows – in your opinion, is the market effectively “throwing the baby out with the bath water” at these valuations?

Since Fukushima, all uranium companies are trading at approximately 60% of their pre Fukushima values. Once the world realizes that there are no other “green” options for base load power, the valuations of uranium explorers and developers should increase.

CXX has been trading at a discount to its peers since the Labrador Mining Moratorium was announced in April 2008. One could expect that our share price should improve when this Moratorium is removed. The INUIT government is reviewing the lifting of the Moratorium and a vote is expected to be held on or about the week of December 12th, 2011.

With Rio Tinto’s proposed acquisition of Hathor Exploration many people are wondering what’s next for the uranium sector. Is M&A something the management team is considering at this juncture?

Crosshair is constantly looking at both property and company acquisitions. Earlier this year we announced that we were looking at acquiring the US assets of AusAmerican Mining, an Australian Company. Upon completion of our due diligence and based on the current market situation we declined to proceed with the transaction. That being said we continue to evaluate other situations in the uranium sector.

Your Gold project is located in the Newfoundland and Crosshair completed a Bulk Sample in late 2010 – what is the status of this project?

The company has spent approximately $1.9 million since April 2008 on its 60% owned Golden Promise Property in central Newfoundland. This Joint Venture project with Paragon Minerals contains a NI 43-101 Inferred Resource of approximately 89,500 ounces contained in 921,000 tonnes at a grade of 3.02g/t that is open and expandable. Our 2,174 tonne Bulk Sample, done with a goal of better determining grade and recoverability rates, produced approximately $430,000 in gold and silver earlier this year.

Crosshair recently completed a name change from Crosshair Exploration to Crosshair Energy – is it safe to assume that, at some point, you intend to spin-out your gold project to focus on energy?

Crosshair is currently evaluating its strategic options for its gold assets and these options may include a sale, spin-out or option agreement.

Uracan Resources is one of many junior uranium stocks that appear to be down and out. Or is it? In 2007, with uranium prices hitting record highs, Uracan Resources hit highs of over $1.60. Today, in the aftermath of the Japan crisis, the company’s shares are trading at a mere $0.07 valuing the company at $10 million. With net liquid assets north of $5 million (over half the companies market cap) the market is deeply discounting Uracan’s mineral properties which, according to the company’s most recent financial statements, have seen almost $30 million of past exploration and development expenditures.

Uracan is lead by well-know Vancouver mining venture capital professional Gregg Sedun. Mr. Sedun is a former corporate finance lawyer with 28 years of mining industry-related experience and now heads Global Vision Capital. Global Vision Capital develops mining projects and raises expansion capital for those projects from its network of institutional and professional retail investors. Collectively, Gregg Sedun and Global Vision Capital have raised over $1 billion in support of mining venture development; which may provide investors with some comfort that Uracan, although down, may not be out.

Gregg thanks for joining us, you’ve been involved in the mining venture capital markets for some time, please tell our readers a little about yourself and why did you get involved in uranium?

By way of background, I have had a 28-year career in mining, corporate finance and venture capital, of which about half was as a mining/finance lawyer and half running a venture capital firm I founded specializing in starting or financing early stage resource opportunities. My venture capital career started as a founding director of Diamond Fields Resources, which had a huge world-class nickel discovery called “Voisey’s Bay”. Diamond Fields was sold for $4.3 Billion in 1996 which allowed me to retire from law and start my own venture capital business. I am proud to say that this business has gone very well, as I have been involved in numerous companies as a founding shareholder and/or director that have resulted in significant shareholder gains.

In 2006, I became interested in uranium, based on a strongly increasing curve of the commodity price that was moving up from $25/lb., and eventually hit $140/lb., driving up valuations of uranium companies. I became aware of a very significant package of uranium properties that were previously owned by about 50 companies in the last big uranium play in Canada in the 1970’s and 1980’s. I partnered with Frank Giustra (one of the world’s great mining promoters) and Clive Johnson of Bema Gold fame to launch Uracan to buy 100% of all of the aforementioned properties, giving us a massive land position of over 1000 sq. km. We began exploring and immediately made a discovery in the Double S Zone, which we have expanded over the last 5 years to a significant NI 43-101 compliant resource. Unfortunately two unexpected events, the 2008 financial crisis and the 2011 Japan tsunami, seriously affected the junior uranium exploration and development sector, resulting in slowed growth for all uranium companies. That said, Uracan is excited about the future for uranium and we believe our patience and long-term business strategies will be rewarded in the coming years.

Obviously the earthquake in Japan deeply effected the uranium market. From a business management perspective, how did Uracan respond to the disaster?

Since Uracan is a uranium exploration company not currently in production, the earthquake in Japan did not dramatically affect our day-to-day business operations, other than causing us to modify our exploration program to reduce the company’s burn rate. However, the earthquake had repercussions on uranium demand which in turn affected uranium prices. This has resulted in dramatically lower valuations for all uranium related companies. The ability of these junior uranium companies to raise capital has therefore been hindered, causing a reduction in their exploration programs. We were no different than all of the other uranium juniors in this regard.

We would expect that as demand continues to rise for uranium and nuclear power, that this trend will reverse itself and Uracan will be in a strong position for future growth.

Where are your projects based and how are things progressing?

Uracan is in the business of exploring and developing bulk tonnage, near-surface uranium deposits at its two 100%-owned projects in Quebec and Saskatchewan, Canada. Our company’s focus is to develop these uranium deposits, which can be economically explored and mined, in order to maximize shareholder value. The Company’s flagship 1000 km2 project on the North Shore of Quebec hosts two main claim groups: Costebelle and Turgeon. We have been exploring in Quebec since 2006 and have been making steady progress toward our end goal. During that time, we have drilled approximately 346 holes and 65,800 meters.

At the Turgeon Claim Group, our project hosts a NI 43-101 compliant total Indicated Resource estimate of 21.5 million tonnes at an average grade of 0.014% U3O8 containing 3.11 million kilograms (6.86 million pounds) of U3O8 using a 0.010% cutoff at the Double S Zone. Within the Double S, Middle and TJ zones, the project hosts a combined total Inferred Resource estimate of 140.65 million tonnes at a weighted average grade of 0.012% U3O8 containing 16.826 million kilograms (37.095 million pounds) of uranium using a 0.010% cut-off. This project has year-round access, excellent infrastructure, and good open pit economics, which can be put into production relatively easily with low operating costs.

In the last two years, however, Uracan has concentrated its exploration efforts on the higher grade A4 and CC-11 Zones within the Costebelle Claim Group, which lies east of our Turgeon resource area. The grade at the Costebelle zones is approximately double that of the Turgeon zones. Costebelle has been the focus of Uracan’s drilling in 2010 and 2011, with the intention of establishing a new higher grade NI 43-101 compliant resource for this location. Summer mapping and sampling programs have identified numerous prospective zones within the Costebelle and Pontbriand claims that also require further investigation.

The Company’s intention is to continue evaluating the resource potential of these new and existing zones at the North Shore project in Quebec until we have established a large enough resource that we can advance into the next stage of development.

Uracan’s second property is a 100 sq. km project in Saskatchewan’s Wollaston domain, south of the Athabasca Basin. Our Pipewrench Lake property has had approximately 2600 meters drilled in 16 holes with encouraging results of up to 12.7 m at 0.142% U3O8.

Some people think this December could be an excellent time to revisit uranium stocks as investors look to lock-in tax losses. Is the sector finally ready for a rebound?

Yes, I believe the uranium sector is well poised for a rebound. In part, this resurgence began in mid-2010 when the price of uranium moved off its recent lows from the 2008 financial crisis and surged back into the mid $70/lb. range. This significant price momentum from $40/lb. to $70/lb. began to generate strong interest in the junior uranium sector once again. In March 2011, however, the world was hit with the unpredictable and tragic tsunami in Japan which sent the uranium sector back to the price levels of 2008.

One year later, the uranium sector is finally beginning to recover. The smart money, contrarian investors, are already buying high quality undervalued junior uranium stocks. To make money in this business, you need to be early and one step ahead of other investors and can’t always follow the trends. That being said, however, every investor has to allow a reasonable time frame for his or her investment to grow. In my view, patient investors who buy junior uranium stocks now at the heavily discounted price levels (or hold their current positions) and hang on for 1-2 years, will see a significant return on their investment.

Speaking on demand, where do think future demand for uranium will originate from and why?

It is no secret that future demand for uranium and nuclear power will be controlled through the developing socioeconomic transformation of Asia. As emerging world superpowers in support of nuclear power, China, India, Korea, and Russia will be the primary drivers of uranium demand over the next twenty years. Notably as well, we have recently seen expressed support of nuclear power from several G20 nations, including the United States, Britain and France. We expect Brazil to have a significant impact on demand as well. Brazil is emerging as an economic powerhouse and will require a substantial amount of energy to supplement its growth.

With a rapidly increasing global dependence on nuclear power, demand for uranium, which is the main energy source used in fueling nuclear power, is expected to soar in the next 5-10 years and we expect to see a significant increase in the uranium spot price. There are hundreds of nuclear reactors planned or proposed in the world today and given the world’s current levels of uranium production, this will result in a massive supply shortage of uranium.

Nuclear power is once again gaining global support as the only clean, affordable, reliable and GHG emission-free source of energy that can realistically supply the demand for energy worldwide. The world’s population is expected to reach 8 billion by 2030 and consequently, demand for clean energy sources will rise. Other renewable energy sources, such as wind, hydro and geothermal, cannot meet this global demand and thus, the world is gradually turning to nuclear power. Nuclear power is far more affordable than any non-renewable energy source such as coal, oil and natural gas. We expect this reliance on nuclear power to have a positive impact on uranium exploration companies, including Uracan.

The bottom line is that nuclear power is the most efficient, powerful and cleanest form of energy available. Nuclear power will likely play a major role in the growth and urbanization of this planet for decades to come. The demand for uranium will outstrip supply creating a substantial discrepancy for the amount of uranium available globally, resulting in significant upward momentum for uranium spot prices. Quality projects in stable countries, such as Canada, will benefit from this growth. In my view, Uracan is well positioned to capitalize on this opportunity.

This interview was featured in the article Uranium Stocks to Watch in 2012 – CLICK HERE to read more.

When the USSR collapsed Russia inherited over a thousand tons of weapons-grade uranium and a massive nuclear refining and fabricating infrastructure – 40% of world total. During the twenty year Megatons to Megawatts Program Russia will convert 500 tonnes of highly enriched uranium (HEU – uranium 235 enriched to 90 percent) from dismantled Russian nuclear weapons into low enriched uranium (LEU – less than 5 percent uranium 235) for nuclear fuel and sell it to the US. The terms of the Megatons to Megawatts Program also required that the HEU be converted to LEU in Russian nuclear facilities.

The United States established a government corporation – United States Enrichment Corporation (USEC) to purchase and transport the LEU to the US. Russia designated Tekhsnabeksport (“Tenex”) a commercial subsidiary of its Ministry of Atomic Energy (MinAtom) to implement their side of the program.

The Megatons to Megawatts program had, as of August 2011, down-blended 425 tonnes of HEU – equivalent to 17,000 nuclear warheads. The twenty year program to down-blend 500 tonnes of weapons grade Russian HEU into fuel for nuclear reactors will eliminate the equivalent of 20,000 warheads by the time it comes to an end in 2013. Nuclear warheads that were once on Russian ICBMs aimed at American cities are now providing 50% of the electricity produced by America’s nuclear power plants.

Russian stockpiles of weapons grade material being down-blended for civil nuclear reactors has filled a very large part of global uranium demand. This has exerted significant downward pressure on uranium prices. Long term low uranium prices, which just starting to climb before the Japanese nuclear accident, seriously affected mining activity.

The world’s uranium miners currently produce 40 million pounds less than the world’s nuclear power plants need – this figure doesn’t include the power plants under construction or the hundreds in planning stages. According to the World Nuclear Association, China is currently building 26 reactors with plans for dozens more, the UK has plans to build eight more, Russia has 10 reactors under construction, 14 planned, and another 30 proposed. India has 6 reactors under construction, 17 planned, and another 40 proposed.

A host of other countries plan to build nuclear capacity, or expand upon their existing nuclear power capacities – emerging markets such as Brazil, Saudi Arabia, United Arab Emirates, Turkey, and Vietnam as well as developed nuclear markets such as South Korea, Canada and France. Some believe that Germany’s decision to close all of its reactors will be reversed and the Japanese closing all of their reactors is unlikely.

The Megatons to Megawatts Program, according to the USEC, was supplying roughly 50% of the US’s LEU demand. Mining accounted for 8% with the rest coming from other sources (rapidly depleting utility and government stockpiles).

A ten year replacement contract, signed in March 2011, will see Tenex continue to supply low-enriched uranium (LEU) from Russian commercial enrichment activities to the USEC after the Megatons to Megawatts program finishes. Under the terms of the contract, the supply of LEU to the USEC will begin in 2013 and ramp up until it reaches a level, in 2015, that is approximately one-half the level currently supplied by TENEX to the USEC under the Megatons to Megawatts program. There is an option clause to increase the quantities up to the same level of supply as the Megatons to Megawatts program.

Unlike the Megatons to Megawatts program, the LEU supplied under this new contract will come from Russia’s commercial enrichment activities rather than from down-blending of weapons grade material.

Because the allowed amount of Russian enriched uranium imports into the US is strictly limited through 2020, USEC will deliver only a portion of the enriched uranium to US utilities. Most of the enriched uranium will be delivered to USEC’s customers outside of the US in both existing and emerging markets. The uranium sourcing for the new contract is extremely significant.

The U.S. has 104 nuclear reactors operating, this is the largest fleet of nuclear reactors in the world making the U.S. the world’s largest uranium market. In 2010 the US nuclear reactor fleet required between 51 to 55 million pounds of uranium. The mined supply of uranium in the U.S. in 2010 was about four million pounds. The U.S. is producing only about eight percent of the required amount of uranium to keep the existing U.S. nuclear fleet running.

Russia doesn’t have a lot of domestic uranium, although the country does have almost half the worlds refining and processing capabilities. Russia is in the process of tying up uranium supply:

- Russia’s Rosatom, its nuclear agency, and Kazatomprom, Kazakhstan’s national nuclear development corporation, have set up a joint venture to market uranium and together will dominate the global uranium market;

- Russia and Mongolia, in April 2008, agreed to cooperate in identifying and developing Mongolia’s uranium resources. Further bilateral agreements were signed in August 2009 and December 2010. Russian legislation was signed into law in early 2011 ratifying establishment of a joint, limited liability company called Dornod Uran – 49% owned by ARMZ;

- ARMZ Uranium Holding Co. (AtomRedMetZoloto) is a Russian uranium mining company, its wholly owned by Atomenergoprom, a part of Rosatom, Russia’s state-owned atomic energy monopoly. Rosatom owns a 51 percent interest in Canada’s Uranium One (TSX: UUU);

- In December 2010 ARMZ made a $1.15 billion takeover bid for Australia’s Mantra Resources Ltd. Mantra had the Mkuju River project in southern Tanzania, which is expected to be in production in 2013 at 1400 tU/yr.

What conclusions can be drawn? Let’s consider the facts:

- The price of commercially mined uranium will no longer be depressed by a steady stream of HEU down-blends into the marketplace – the legacy feedstock kitty is going to come to an end. There is already an imbalance between mined supply and demand – the demand for uranium is higher than the supply. This difference is currently being met from the decommissioning of nuclear warheads but the Megatons to Megawatts Program is ending in 2013;

- Emphasis to meet growing demand will be on mined uranium but the world is already short 40m tonnes of mined uranium;

- Many of the world’s developing and developed countries will start or continue to build nuclear power plants further increasing the demand for mined uranium supply;

- Low uranium prices means there hasn’t been significant investment in new mines, lower prices make new projects less attractive – this will constrain the supply of uranium going forward;

- The Russians are tying up supply, soon they will be the dominant player in the global uranium market;

- Resource Nationalization, Country Risk and Security of Supply will mean areas of the globe will be off limits to western miners and countries will increasingly be looking after their own interests. Access to uranium deposits in safe, stable and secure environments will become increasingly dear;

- Many companies will find it challenging to get permits for uranium mines because of negative public sentiment.

RBC Capital Markets believes there is not enough uranium production from current or planned mines to; satisfy current reactor needs, meet new reactor start up initial core requirements (3x normal load for startup), and to build inventories for new reactors. RBC estimate there will be a global uranium shortfall of over 70 million pounds by 2020 and the uranium market will require substantial new sources of uranium to fuel the projected growth in the global nuclear reactor fleet.

Cameco Corp. (TSX:CCO) officially commenced its $520 million hostile bid for Hathor Exploration Ltd. (TSX:HAT) today. On Friday, Cameco announced that it was planning the hostile bid after discussions concerning a friendly merger failed to ratify a deal. The bid, an all-cash offer of C$3.75 per share, represents a 40 percent premium on Hathor’s closing price of C$2.67 on Thursday and a 33% over Hathor’s 20-day volume-weighted average trading price. According to the company’s press release, Hathor shareholders must tend their shares to Cameco’s offer before it expires at 5:00 p.m. PST on October 31, 2011, unless the offer is extended or withdrawn.

Cameco, Canada’s top uranium producer, is looking to expand its output in the Athabasca basin. And this is welcome news to shareholders of Hathor Exploration. Hathor controls the coveted Roughrider deposit, an exploration stage uranium project near Cameco’s Rabbit Lake mill in Northern Saskatchewan. The Roughrider summer drill program commenced on June 7th, 2011 and results were received back from Saskatchewan Resource Council (SRC) on August 15th, 2011. The program extended the Far East Zone of the deposit.

Hathor Exploration is undertaking a preliminary assessment of options for development of its Roughrider deposit and expects commencing full scale economic scoping for the project later in 2011. On Monday, Hathor’s management team urged shareholders to wait for the official bid, and to not act until it had reviewed the offer and responded.

Uranium prices fell from $73 a pound in January 2011 as governments around the world reviewed nuclear plans following the Japanese tsunami crisis in March. But according to data compiled by Bloomberg, China and India are planning atomic power developments that will more than double global production even after Japan’s nuclear disaster. China and India are predicted to lead a 46 percent increase in uranium consumption by the world’s five biggest atomic-power developers by 2020. Currently, the uranium spot price is $50.50.

After the worst 3 month period for uranium miners since the ‘great recession’ is it finally time for a sector rebound? Last week, China reported their trade surplus expanded to $13.05 billion in May and strong imports eased fears of a slowdown in the world’s second biggest economy. Today, data out of China showed inflation accelerated to its fastest level in almost three years, and China’s industrial output grew 13 percent from a year ago. Its central bank, in an effort to curb inflation, later increased the reserve requirement ratio for commercial lenders by 50 basis points.

To some, these actions confirmed that amid efforts to prevent China’s economy from overheating growth was still robust. Peter Cardillo, chief market economist at Avalon Partners in New York, said the data is a sign that perhaps China’s economy “can avoid a hard landing, and that’s cheering the markets.” The DOW is up over 1% today and commodity prices across the board rallied after what has been a six week bull market in pessimism.

According to Stephen Massocca, managing director at Wedbush Morgan in San Francisco, “Investors are very susceptible to any kind of news and since we are very oversold here, we could see the market instantly bounce back if we get anything remotely good.”

With global growth affirmed, at least for now, some think the biggest price drop of uranium in two years may be ending. Uranium prices fell from $73 a pound in January 2011 to a recent low of $55 as governments around the world reviewed nuclear plans following the Japanese tsunami crisis in March. But recently, it was reported that China and India plan atomic power developments that will more than double global production even after Japan’s nuclear disaster. China and India will lead a 46 percent increase in consumption by the world’s five biggest atomic-power developers by 2020, according to data compiled by Bloomberg. Morgan Stanley forecasts the price per pound of uranium will climb to $64 by the end of in 2011. Currently, the uranium spot price is $56.

While uranium is off 23.3% from pre-tsunami highs, uranium stocks are down even more. Cameco (TSX: CCO) reached a high of around $44 per share in early 2011 and now trades at just over $24; a decline of 45.5%. Paladin Energy (TSX: PDN) which hit highs of $5.60 in January and can now be had for $2.67; a 52.3% decrease.

But two yellow cake miners were hit even harder. Denison Mines (TSX: DML) touched a high of $4.40 in February is now trading for under $1.80 per share; a drop of 59.1%. While shares of Uranium One (TSX: UUU) which were trading for just under $7 a share earlier this year are now being traded for $2.85; a 59.3% selloff.

The Japanese disaster, now approaching its one month anniversary, continues to be the only topic of discussion for investors in uranium stocks.

The spot price of Uranium fell 10%, to $60 per pound immediately after the earthquake and tsunami created a nuclear incident at the Fukushima reactor, sending low levels of radiation drifting south to Tokyo. Uranium prices eventually fell as low as $49.25 (U.S.) per pound. Perhaps a lesser known fact amongst casual observers is that uranium prices have almost completely recovered. By March 24th, the price of uranium was back to $61.13.

What’s behind the speedy recovery? Many analysts point to a lack of real options for replacing nuclear energy, which supplies 13.5 per cent of the world’s electricity generation. Independent analyst Peter Strachen says the situation will “…basically blow over in the next 12 to 18 months, as people realize that there’s no real alternative in the short to medium term, for large, baseload power supply.” Strachen points to a number of new plants being built in India, China and Brazil.

Analysts with The Bedford Report agree. They say that China is currently in the process of quadrupling its uranium consumption to fifty to sixty million pounds a year, and says it plans to build ten nuclear power plants a year for the next decade. Even as the Japanese crisis hit its darkest hour, with the crisis at the Fukushima Daiichi nuclear power plant still not contained, the Obama administration said that “nuclear power will remain a key component of America’s energy mix, despite worldwide anxiety over the safety of reactors.” The US currently has 104 reactors in 31 states.

Raymond James mining analyst Bart Jaworski talked to the Globe and Mail recently about what he believes is the opportunity the disaster has created for investors to buy quality uranium stocks at a discount. He said “We expect this situation to be no different than what happened after the Three Mile Island (1979) and Chernobyl (1986) accidents, where reactor growth continued quite strongly due to the large amount of reactors already in construction phase.”

Two of Jaworski’s favorite picks are Cameco (TSX:CCO) and Paladin Energy (TSX:PDN). Cameco is down just over 19% since the Japanese disaster, from $36.32 on March 11th to $29.25 on April 6th. Paladin Energy is down about the same percentage, from $4.66 on March 11th to $3.82 on the close today. A look at other TSX listed uranium plays reveals similar, or better, numbers. Denison Mines (TSX:DML) has forfeited a shade over 20% of its pre-Japan price, First Uranium (TSX:FIU) is down just 8%.

And then there’s Uranium One (TSX:UUU). Despite a modest recent rally, the Vancouver based miner is still down nearly 33% since the Japanese quake, from $5.96 on March 11th to $4.04 on April 6th.

In early March, Uranium One reported record annual revenue of $327 million for 2010 after it sold 6.9 million pounds of uranium at an average price of $48 per pound. The company increased its cash on hand to $315 million from just over $148 million the year prior.

Sort through Uranium One’s recent financials and you’ll soon find a staggering loss of $148.2 million, or twenty four cents a share in the fourth quarter of 2010. The company was hit by a one time $113.5 million writedown at its Honeymoon Uranium project in Australia. Excluding the writedown, Uranium One actually earned a penny a share in the quarter.

And while the Japanese nuclear incident was bad news for all uranium miners, it may have ultimately affected Uranium One positively in at least one way. At the time the Japanese crisis hit, the company was in negotiations to buy Mantra, an Australian uranium miner with projects in Africa. ARMZ, a subsidiary of Russia’s atomic energy agency that owns a controlling stake in Uranium One, had offered to buy Mantra for (AUS) $8 per share, but after the crisis lowered the offer to (AUS) $7.02 a share, valuing the company at just over a billion dollars. In late March, Mantra’s board of directors advised shareholders to accept the revised agreement “after taking into consideration the current global equity market conditions and increased uncertainty for the uranium sector”.

Shares of Saskatchewan’s Cameco (TSX:CCO), the world’s largest publicly traded uranium company were, predictably, walloped after the Sendai earthquake and tsunami of March 11th. On Monday, March 14th, the first day of trading after the Japanese catastrophe, shares of Cameco were down $4.62 to $31.70. The stock hit a recent high of over $43 in mid-February.

Canadian uranium stocks such as Mega Uranium (TSX:MGA), Paladin Energy (TSX:PDN) and UEX Corp. (TSX:UEX) were part of a worldwide sector selloff. Investors were no doubt taking stock of the fact that Japan accounts for more than 10% of the world’s uranium demand, but also that the event could slow the worldwide growth of nuclear power.

Uranium is a radioactive element and a critical component in the production of electricity through nuclear power. Cameco is the world’s second largest uranium producer, accounting for 16% of world production, and it sells 10 to 15 percent of that uranium to Japan.

In light of the fact that Japan soon had eleven of its fifty-four reactors off-line, the perceived effect on demand was swift. But a near-global reassessment of nuclear power as a safe energy source was not far behind. Germany and Switzerland decided to immediately freeze the development of nuclear power facilities while they assessed safety procedures. Venezuela, on Tuesday, halted its nuclear program outright.