The U.S. stock markets are becoming more unstable, fueling mounting anxiety about what’s likely coming. After surging to new all-time-record highs in late July, stocks plunged in a sharp pullback as the US-China trade war escalated. Stock markets’ resiliency in the face of bearish news is partially determined by how companies are faring fundamentally. The big U.S. stocks’ just-reported Q2’19 results illuminate these key indicators.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the US Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

The deadline for filing 10-Qs for “large accelerated filers” is 40 days after fiscal quarter-ends. The SEC defines this as companies with market capitalizations over $700m. That easily includes every stock in the flagship S&P 500 stock index (SPX), which contains the biggest and best American companies. The middle of this week marked 38 days since the end of Q2, so almost all the big US stocks have reported.

The SPX is the world’s most-important stock index by far, with its components commanding a staggering collective market cap of $25.8t at the end of Q2! The vast majority of investors own the big US stocks of the SPX, as some combination of them are usually the top holdings of nearly every investment fund. That includes retirement capital, so the fortunes of the big U.S. stocks are crucial for Americans’ overall wealth.

The huge ETFs that track the S&P 500 dominate the increasingly-popular passive-investment strategies as well. The SPY SPDR S&P 500 ETF, IVV iShares Core S&P 500 ETF, and VOO Vanguard S&P 500 ETF are the 3 largest ETFs in the world. This week they reported colossal net assets running $258.5b, $179.3b, and $115.8b respectively! The big SPX companies overwhelmingly drive the entire stock markets.

Q2’19 proved quite volatile in the U.S. stock markets, leading to increasing unease. The SPX surged 3.9% higher in April, hitting 4 new record closing highs. That capped an unbelievable 25.3% rocketing over just 4.2 months, a crazy move higher. That was driven by extreme Fed dovishness, as it panicked following the SPX’s severe 19.8% near-bear correction that bottomed in late December. Euphoria reigned supreme.

But the big US stocks couldn’t stay at such lofty heights, so the SPX fell on balance through May on the way to a 6.8% pullback by early June. China reneged on major trade commitments it made to the US over a year through 10 rounds of high-level trade talks. So Trump ramped tariffs on a $200b tranche of annual Chinese imports into the US from 10% to 25%. US-China trade-war news was a key market driver in Q2.

That considerable selloff was reversed by a hyper-dovish Fed riding to the rescue. First its chairman said the Fed was ready to start cutting rates again, and later top Fed officials’ collective outlook for future rates shifted from one hike to one cut. The SPX blasted 7.6% higher in a few weeks on that, achieving another new record high in late June. The US-China trade war and Fed jawboning and actions will keep fueling volatility.

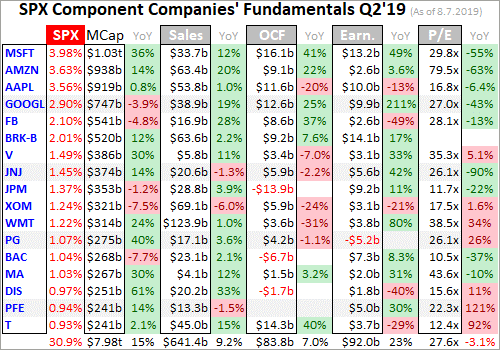

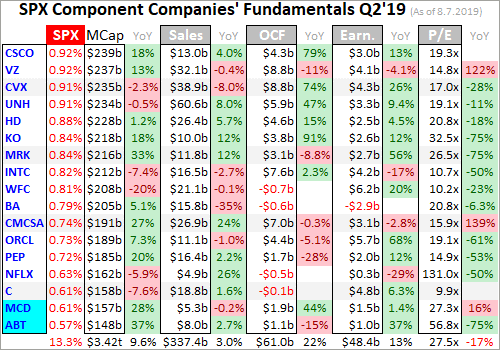

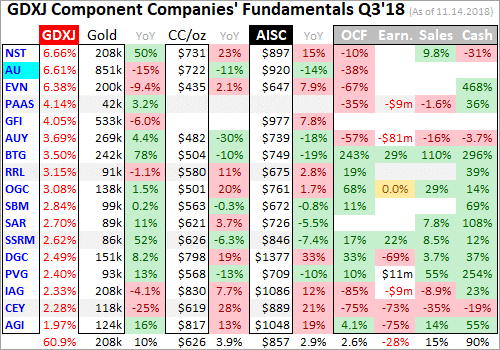

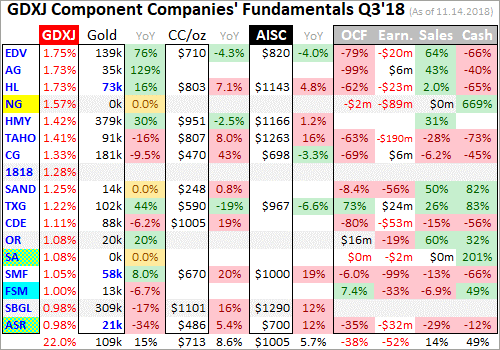

Every quarter I analyze the top 34 SPX/SPY component stocks ranked by market cap. This is just an arbitrary number that fits neatly into the tables below, but a dominant sample of the SPX. As Q2 waned, these American giants alone commanded fully 44.2% of the SPX’s total weighting! Their $11.4t collective market cap exceeded that of the bottom 439 SPX companies. Big US stocks’ importance cannot be overstated.

I wade through the 10-Q or 10-K SEC filings of these top SPX companies for a ton of fundamental data I feed into a spreadsheet for analysis. The highlights make it into these tables below. They start with each company’s symbol, weighting in the SPX and SPY, and market cap as of the final trading day of Q2’19. That’s followed by the year-over-year change in each company’s market capitalization, an important metric.

Major U.S. corporations have been engaged in a wildly-unprecedented stock-buyback binge ever since the Fed forced interest rates to the zero lower bound during 2008’s stock panic. Thus the appreciation in their share prices also reflects shrinking shares outstanding. Looking at market-cap changes instead of just underlying share-price changes effectively normalizes out stock buybacks, offering purer views of value.

That’s followed by quarterly sales along with their YoY change. Top-line revenues are one of the best indicators of businesses’ health. While profits can be easily manipulated quarter to quarter by playing with all kinds of accounting estimates, sales are tougher to artificially inflate. Ultimately sales growth is necessary for companies to expand, as bottom-line profits growth driven by cost-cutting is inherently limited.

Operating cash flows are also important, showing how much capital companies’ businesses are actually generating. Companies must be cash-flow-positive to survive and thrive, using their existing capital to make more cash. Unfortunately many companies now obscure quarterly OCFs by reporting them in year-to-date terms, lumping multiple quarters together. So if necessary to get Q2’s OCFs, I subtracted prior quarters’.

Next are the actual hard quarterly earnings that must be reported to the SEC under Generally Accepted Accounting Principles. Lamentably companies now tend to use fake pro-forma earnings to downplay real GAAP results. These are derided as EBS profits, Everything but the Bad Stuff! Certain expenses are simply ignored on a pro-forma basis to artificially inflate reported corporate profits, often misleading traders.

While I’m also collecting the earnings-per-share data Wall Street loves, it is more important to consider total profits. Stock buybacks are executed to manipulate EPS higher, because the shares-outstanding denominator of its calculation shrinks as shares are repurchased. Raw profits are a cleaner measure, again effectively neutralizing the impacts of stock buybacks. They better reflect underlying business performance.

Finally the trailing-twelve-month price-to-earnings ratios as of the end of Q2’19 are noted. TTM P/Es look at the last four reported quarters of actual GAAP profits compared to prevailing stock prices. They are the gold-standard valuation metric. Wall Street often intentionally conceals these real P/Es by using fictional forward P/Es instead, which are literally mere guesses about future profits that almost always prove too optimistic.

These are mostly calendar-Q2 results, but some big U.S. stocks use fiscal quarters offset from normal ones. Walmart, Cisco, and Home Depot have lagging quarters ending one month after calendar ones, so their results here are current to the end of April instead of June. Oracle uses quarters that end one month before calendar ones, so its results are as of the end of May. Such offset reporting ought to be banned.

Reporting on offset quarters renders companies’ results way less comparable with the vast majority that report on calendar quarters. We traders all naturally think in calendar-quarter terms too. Decades ago there were valid business reasons to run on offset fiscal quarters. But today’s sophisticated accounting systems that are largely automated running in real-time eliminate all excuses for not reporting normally.

Stocks with symbols highlighted in blue have newly climbed into the ranks of the SPX’s top 34 companies over the past year, as investors bid up their stock prices and thus market caps relative to their peers. Overall the big US stocks’ Q2’19 results looked decent, with modest sales and profits growth. But these growth rates are really slowing, and stock valuations remain near bubble levels relative to underlying earnings.

Over the past 19.3 years, I’ve written 873 of these weekly web essays. None are more challenging than these ones analyzing quarterly results. There’s so much data to collect and analyze, so much work to do. So it wasn’t until Q4’17 results that I took on this Herculean task. Understanding the fundamentals of big U.S. stocks is critical to gaming likely coming stock-market performance, so the hard work is well worth it.

Out of the 7 quarters so far in this essay series, the concentration of capital in the top 34 SPX companies has never been higher. A staggering 44.2% of the market capitalization of all 500 stocks is centralized in just 34 stocks! This compares to 41.7% in Q1’18. It is not healthy for a shrinking pool of market-darling stocks to dominate the entire US markets. That leaves market performance overly dependent on them.

Much of this ominous concentration risk comes from the beloved mega-cap technology companies. The SPX’s top 5 component stocks are Microsoft, Amazon, Apple, Alphabet, and Facebook. They commanded fully 16.2% of the SPX’s entire market cap at the end of Q2, nearly 1/6th! Thus if any one of them gets hit by bad company-specific news, it will help drag the entire stock markets lower intensifying any selling.

One of the cool perks of being a professional speculator and newsletter guy is I get to listen to financial television including CNBC and Bloomberg all day every day. That offers excellent reads on the prevailing sentiment that drives markets. Almost every professional money manager interviewed loves these elite mega-cap techs, including them in their top holdings. They are universally-held and incredibly-crowded trades.

When capital deployed in stocks becomes overly concentrated, that feeds on itself for awhile. Investors deploy capital with money managers based on their performance. If they don’t own these mega-cap techs that investment inflows have driven higher for years, they risk falling behind their peers and losing business. So money managers feel forced to buy the high-flying mega-cap techs even at lofty valuations.

Interestingly these guys try to justify their heavy mega-cap-tech holdings by claiming these stocks are less risky than the broader markets because their businesses are so strong. I can’t count the number of times I’ve heard that mega-cap techs are what to own in case of a recession. That’s total nonsense, as high-flying really-popular stocks have greater downside. The more capital invested, the more potential selling.

During that severe near-bear correction where the SPX plummeted 19.8% largely in Q4’18, these top 5 SPX stocks amplified that by 1.3x with a 24.8% average drop. When the SPX pulled back 6.8% mostly in May, MSFT, AMZN, AAPL, GOOGL, and FB averaged big 12.5% declines nearly doubling the SPX’s retreat! And during the sharp 6.0% SPX pullback since late July, their average fall of 7.8% again leveraged it 1.3x.

The serious risks of too much capital in too few stocks aside, the big U.S. stocks as a group enjoyed a solid Q2 fundamentally. Their collective revenues grew 2.7% year-over-year to $978.8b. Much of this was concentrated in those 5 mega-cap tech stocks, which averaged amazing 16.0% top-line growth compared to just 4.4% for the rest of the top 34 SPX stocks. Money managers use this to rationalize being overweight.

These elite tech market-darlings are certainly not recession-proof, despite the euphoria surrounding them. Recessions are often triggered by stock bear markets, which generate enough fear to scare both consumers and businesses into pulling in their horns and spending less. That is likely to lead to falling sales for all 5 of these mega-cap techs, which will hammer their prices sharply lower sucking in the SPX.

Businesses will cut back on their information-technology spending if they are worried about their own sales, hurting the fast-growing cloud-computing sides of Amazon, Microsoft, and Google. Companies will also cut back on their marketing spends if their own perceived prospects dim sufficiently, leading to lower revenues for Google, Facebook, and even Amazon. These high-flying stocks will really suffer in a bear market.

On the consumer side, the sales of Apple’s expensive products will plunge dramatically when consumers get worried about their own futures. They will keep their existing iPhones and iPads longer, extending the critical upgrade cycle. And most of the endless stuff Amazon sells is discretionary not essential, so those purchases will be cut back when people feel financially stressed. The top SPX stocks aren’t immune to a slowdown.

In Q2’19 these top 34 SPX and SPY stocks saw operating-cash-flow generation soar 17.0% YoY to $144.8b. Again those 5 mega-cap techs led the way, with 21.0% average growth compared to 12.9% for the rest. But these market-darling tech companies benefit heavily from the great optimism spawned by record-high stock markets. That convinces both companies and consumers to heavily buy their offerings.

The GAAP-earnings front was more interesting, with these big US stocks’ total profits up just 4.2% YoY to $140.5b in Q2’19. These were dragged down by a couple notable losses, including Procter & Gamble writing down $8.3b in a massive goodwill-impairment charge. That was an admission this company paid far too much for its Gillette shaving business, as men are shaving less and increasingly using cheaper razors.

Then Boeing suffered an ugly $3.4b loss from operations due to its ill-fated 737 MAX airplane. This is a 1960s-era airframe that was upgraded with engines far larger than ever intended in order to maximize fuel efficiency. But these wouldn’t fit under the wings, so they were mounted forward and higher. That screwed up this airplane’s center of gravity and aerodynamics, requiring computer assistance to keep flying.

Either this inherently-unstable flawed design or software bugs caused two horrific crashes killing 346 people. So the entire 737 MAX fleet was grounded, and that airplane was supposed to generate about a third of Boeing’s revenue over the next 5 years! So this company is in a world of hurt until well after this airplane is cleared to fly again. Overall SPX-top-34 profits would’ve been even higher without these losses.

While 4.2% profits growth sounds good, it is still slowing sharply. Overall SPX corporate-earnings growth rocketed 20.5% higher in 2018 largely thanks to the Tax Cuts and Jobs Act. Its centerpiece slashed the US corporate tax rate from 35% to 21%, which went effective as last year dawned. 2018’s four quarters were the only ones comparing pre- and post-TCJA earnings. This year the comparisons are all post-tax-cut.

Thanks to the stock markets’ massive corporate-tax-cut rally in 2017 and 2018, and sharp rebound on the Fed’s radical shift to dovishness earlier this year, valuations remain dangerously high. They are still up near historical bubble levels heralding new bear markets. So low-single-digit earnings growth, with the threat of actual shrinkage in future quarters, isn’t likely to be enough to support these lofty stock prices for long.

Before we get to valuations though, there’s more to consider on the big US stocks’ earnings. One of the main reasons corporations engage in stock buybacks is to artificially boost their reported earnings per share. That masks what their underlying overall GAAP profits are doing, lulling traders into complacency. Some of the companies among these top 34 had yawning gulfs between earnings per share and total profits!

The main culprits were the top 4 mega-cap US banks, JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup. Their financial reporting is mind-bogglingly complex, and full of estimates that allow them to actively manipulate their reported earnings per share. Wall Street loves the big financial stocks, which are often the most-important sector after mega-cap tech for coloring sentiment for the entire stock markets.

JPM’s EPS soared 22.5% YoY in Q2 despite total GAAP earnings only up 10.5%. BAC looked similar at 17.2% EPS growth versus 8.3% overall profits growth. WFC saw earnings per share soar 33.7% YoY despite overall earnings only rising 19.7%. And C’s 19.0% EPS surge literally tripled its 6.3% growth in hard GAAP profits! Something is really wrong here and highly misleading, eventually the truth will catch up.

Some big non-financial stocks also had magical earnings-per-share growth far outstripping underlying corporate-profits growth. Cisco’s EPS rocketed 25.0% higher despite mere 13.1% growth in the bottom-line profits on its income statement. Sooner or later there has to be a reckoning between earnings per share and actual profits, even if huge stock buybacks persist. These key profits measures have to converge.

Wall Street analysts have grown adept at using misdirection to blind investors to the adverse trends in earnings growth. Mighty Apple was a key case in point recently, reporting its Q2’19 results after the close on July 30th. This was heralded as a big beat, with EPS of $2.18 on revenues of $53.8b both exceeding expectations of $2.10 and $53.4b. By those metrics it looked like Apple was thriving, so its stock shot higher.

In after-hours trading it was up 4%+, and by the middle of the next day this monster-market-cap stock had rocketed 6.0% higher! The problem was comparing those Q2 results to estimates is totally deceptive. The analysts always lowball their guesses to ensure companies beat, stoking euphoria and complacency. But all that really matters is companies’ absolute profits and sales growth compared to their year-earlier quarters.

In hard year-over-year terms, Apple’s Q2’19 sales only eked out a 1.0% gain. That was pathetic relative to its other 4 mega-cap-tech peers, which averaged 19.7%. And Apple’s Q2’19 GAAP earnings actually plunged 12.8% YoY from Q2’18! So what Wall Street dishonestly spun into a great quarter was in reality a weaker one. Eventually stock prices have to reflect underlying fundamentals, not perma-bull propaganda.

Ominously stock prices remain dangerously high relative to their underlying corporate earnings. The big U.S. stocks averaged trailing-twelve-month price-to-earnings ratios way up at 27.5x as Q2’19 wrapped up. That is just shy of the historical bubble threshold above 28x! So the current earnings picture over the past 4 quarters certainly doesn’t justify such lofty stock prices. That greatly amplifies market downside risk.

These chronic overvaluations aren’t just concentrated in those top 5 mega-cap tech stocks, which sported 36.2x average P/Es. The rest of the top 34 were still near bubble territory averaging 25.9x. Trading at such high valuations, these stock markets are an accident waiting to happen. It’s only a matter of time until the next bear market arrives. It could be spawned by the mounting US-China trade war, or weaker profits.

Over the past several calendar years, earnings growth among all 500 SPX companies ran 9.3%, 16.2%, and 20.5%. This year even Wall Street analysts expect it to be flat at best. And if corporate revenues actually start shrinking due to mounting trade wars or rolling-over stock markets damaging confidence and spending, profits will amplify that downside. Declining SPX profits will proportionally boost valuations.

Excessive valuations after long bulls always eventually spawn proportional bear markets. And we are way overdue for the next one. At its latest all-time-record high in late July, this current monster SPX bull up 347.3% in 10.4 years ranked as the 2nd-largest and 1st-longest in all of US stock-market history! This powerful secular uptrend can’t persist near bubble valuations as corporate-earnings growth stalls or even reverses.

Bear markets are necessary to maul stock prices sideways to lower long enough for profits to catch up with lofty stock prices. These fearsome beasts are nothing to be trifled with, yet complacent traders mock them. The SPX’s last couple bears that awoke and ravaged due to high valuations pummeled the SPX 49.1% lower in 2.6 years leading into October 2002, and 56.8% lower over 1.4 years leading into March 2009!

Seeing big US stocks’ prices cut in half or worse is common and expected in major bear markets. And there’s a decent chance the current near-bubble valuations in US stock markets will soon look even more extreme. If the big US stocks’ fundamentals deteriorate, the overdue bear reckoning after this monster bull is even more certain. So big US stocks’ coming Q3’19 and Q4’19 results could prove pivotal if they’re weak.

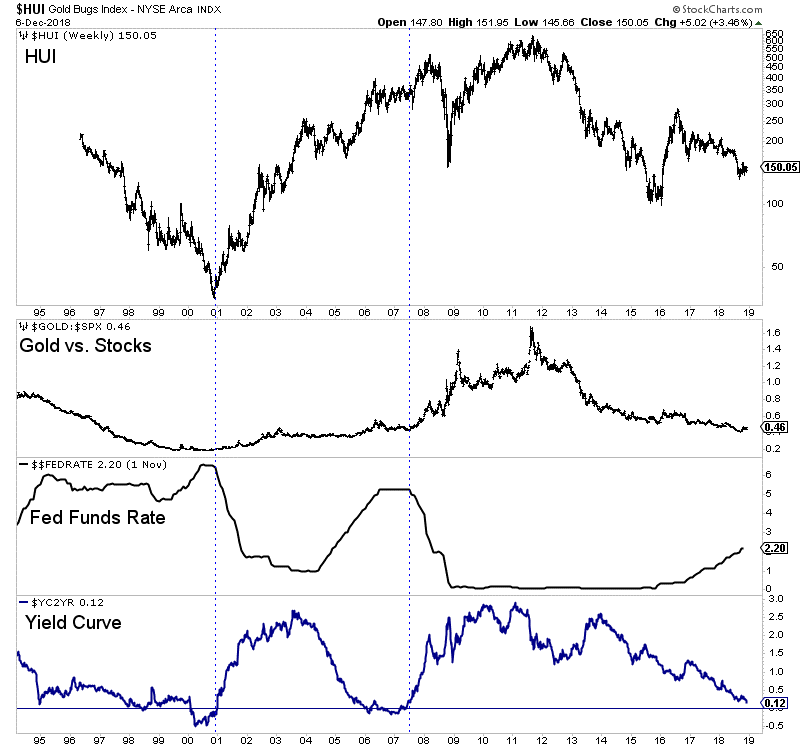

Cash is king in bear markets, since its buying power grows. Investors who hold cash during a 50% bear market can double their holdings at the bottom by buying back their stocks at half-price. But cash doesn’t appreciate in value like gold, which actually grows wealth during major stock-market bears. When stock markets weaken its investment demand surges, which happened in December as the SPX sold off hard.

While the SPX plunged 9.2% that month, gold rallied 4.9% as investors flocked back. The gold miners’ stocks which leverage gold’s gains fared even better, with their leading index surging 10.7% higher. The last time a major SPX selloff awakened gold in the first half of 2016, it soared up 30% fueling a massive 182% gold-stock upleg! Gold’s awesome decisive bull breakout in late June is already attracting traders back.

Absolutely essential to weathering bears is cultivating excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. Lately we’ve been doing this in gold stocks, buying them while out of favor earlier this year to enjoy massive gains in recent months.

This past week we realized absolute gains on gold-stock trades including 109.7%, 105.8%, and 92.0%! All our trades, analyses, and outlooks are detailed in our popular weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! Staying informed is essential for success.

The bottom line is big U.S. stocks’ latest fundamentals from Q2’19’s earnings season were decent. These elite companies enjoyed modest sales and earnings growth. But that masked serious and mounting risks. Investment capital is increasingly concentrating in the beloved mega-cap technology stocks, leaving stock markets overly dependent on their fortunes. Any slowing from them will drag the entire stock markets lower.

More ominously big U.S. stocks’ valuations remain way up near dangerous bubble territory. Their earnings aren’t justifying their lofty stock prices. The resulting downside risks are exacerbated with profits growth really slowing, and threatening to stall out entirely or even shrink in coming quarters. This is a potently-bearish situation, even before any bad news like further escalation in the US-China trade war hits stocks.

The U.S. stock markets sure feel inflectiony, at a major juncture. After achieving new all-time record highs, sentiment was euphoric heading into this week. But those latest heights could be a massive triple top that formed over 15 months. Then heavy selling erupted in recent days as the U.S.-China trade war suddenly went hostile. The big U.S. stocks just-reported Q1’19 fundamentals will help determine where markets go next.

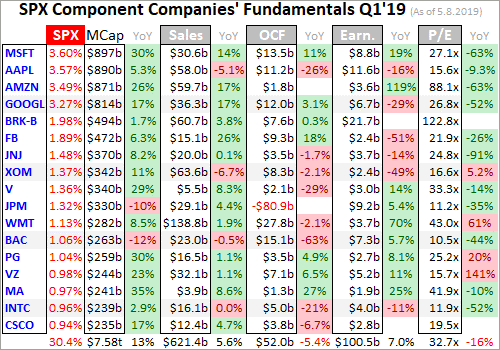

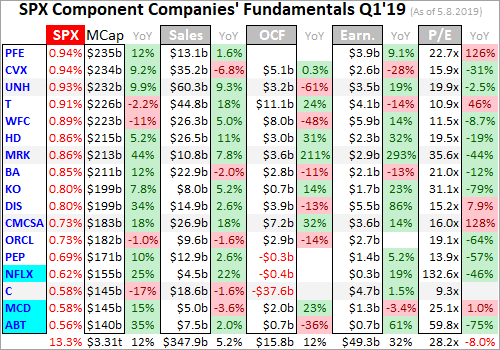

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

The deadline for filing 10-Qs for “large accelerated filers” is 40 days after fiscal quarter-ends. The SEC defines this as companies with market capitalizations over $700m. That currently includes every stock in the flagship S&P 500 stock index (SPX), which contains the biggest and best American companies. The middle of this week marked 38 days since the end of Q1, so almost all the big U.S. stocks have reported.

The SPX is the world’s most-important stock index by far, with its components commanding a staggering collective market cap of $24.9t at the end of Q1! The vast majority of investors own the big U.S. stocks of the SPX, as some combination of them are usually the top holdings of nearly every investment fund. That includes retirement capital, so the fortunes of the big U.S. stocks are crucial for Americans’ overall wealth.

The major ETFs that track the S&P 500 dominate the increasingly-popular passive-investment strategies as well. The SPY SPDR S&P 500 ETF, IVV iShares Core S&P 500 ETF, and VOO Vanguard S&P 500 ETF are among the largest in the world. This week they reported colossal net assets running $271.9b, $175.1b, and $111.5b respectively! The big SPX companies overwhelmingly drive the entire stock markets.

Q1’19 proved extraordinary, the SPX soaring 13.1% higher in a massive rebound rally after suffering a severe correction largely in Q4. That pummeled this key benchmark stock index 19.8% lower in jU.S.t 3.1 months, right on the verge of entering a new bear market at -20%. By the end of Q1, fully 5/6ths of those deep losses had been reversed. Did the big U.S. stocks’ fundamental performances support such huge gains?

Corporate-earnings growth was expected to slow dramatically in Q1, stalling out after soaring 20.5% last year. 2018’s four quarters straddled the Tax Cuts and Jobs Act, which became law right when that year dawned. Its centerpiece was slashing the U.S. corporate tax rate from 35% to 21%, which naturally greatly boosted profits from pre-TCJA levels. Q1’19 would be the first quarter with post-TCJA year-over-year comparisons.

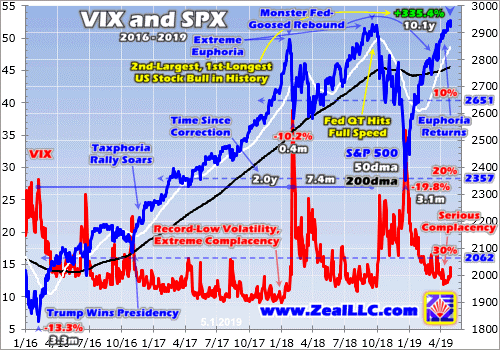

Big U.S. stocks’ valuations, where their stock prices are trading relative to their underlying earnings, offer critical clues on what is likely coming next. By late April the epic stock-market bull as measured by the SPX extended to huge 335.4% gains over 10.1 years! That clocked in as the second-largest and first-longest bull in U.S. stock-market history. With the inevitable subsequent bear overdue, valuations really matter.

Every quarter I analyze the top 34 SPX/SPY component stocks ranked by market cap. This is just an arbitrary number that fits neatly into the tables below, but a dominant sample of the SPX. As Q1 waned, these American giants alone commanded fully 43.7% of the SPX’s total weighting! Their $10.9t collective market cap exceeded that of the bottom 437 SPX companies. Big U.S. stocks’ importance cannot be overstated.

I wade through the 10-Q or 10-K SEC filings of these top SPX companies for a ton of fundamental data I feed into a spreadsheet for analysis. The highlights make it into these tables below. They start with each company’s symbol, weighting in the SPX and SPY, and market cap as of the final trading day of Q1’19. That’s followed by the year-over-year change in each company’s market capitalization, an important metric.

Major U.S. corporations have been engaged in a wildly-unprecedented stock-buyback binge ever since the Fed forced interest rates to deep artificial lows during 2008’s stock panic. Thus, the appreciation in their share prices also reflects shrinking shares outstanding. Looking at market-cap changes instead of just underlying share-price changes effectively normalizes out stock buybacks, offering purer views of value.

That’s followed by quarterly sales along with their YoY change. Top-line revenues are one of the best indicators of businesses’ health. While profits can be easily manipulated quarter to quarter by playing with all kinds of accounting estimates, sales are tougher to artificially inflate. Ultimately sales growth is necessary for companies to expand, as bottom-line profits growth driven by cost-cutting is inherently limited.

Operating cash flows are also important, showing how much capital companies’ businesses are actually generating. Companies must be cash-flow-positive to survive and thrive, using their existing capital to make more cash. Unfortunately many companies now obscure quarterly OCFs by reporting them in year-to-date terms, lumping multiple quarters together. So if necessary to get Q1’s OCFs, I subtracted prior quarters’.

Next are the actual hard quarterly earnings that must be reported to the SEC under Generally Accepted Accounting Principles. Lamentably companies now tend to use fake pro-forma earnings to downplay real GAAP results. These are derided as EBS profits, Everything but the Bad Stuff! Certain expenses are simply ignored on a pro-forma basis to artificially inflate reported corporate profits, often misleading traders.

While we’re also collecting the earnings-per-share data Wall Street loves, it’s more important to consider total profits. Stock buybacks are executed to manipulate EPS higher, because the shares-outstanding denominator of its calculation shrinks as shares are repurchased. Raw profits are a cleaner measure, again effectively neutralizing the impacts of stock buybacks. They better reflect underlying business performance.

Finally the trailing-twelve-month price-to-earnings ratios as of the end of Q1’19 are noted. TTM P/Es look at the last four reported quarters of actual GAAP profits compared to prevailing stock prices. They are the gold-standard metric for valuations. Wall Street often intentionally conceals these real P/Es by using the fictional forward P/Es instead, which are literally mere guesses about future profits that often prove far too optimistic.

These are mostly calendar-Q1 results, but some big U.S. stocks use fiscal quarters offset from normal ones. Walmart, Home Depot, and Cisco have lagging quarters ending one month after calendar ones, so their results here are current to the end of January instead of March. Oracle uses quarters that end one month before calendar ones, so its results are as of the end of February. Offset reporting ought to be banned.

Reporting on offset quarters renders companies’ results way less comparable with the vast majority that report on calendar quarters. We traders all naturally think in calendar-quarter terms too. Decades ago there were valid business reasons to run on offset fiscal quarters. But today’s sophisticated accounting systems that are largely automated running in real-time eliminate all excuses for not reporting normally.

Stocks with symbols highlighted in blue have newly climbed into the ranks of the SPX’s top 34 companies over the past year, as investors bid up their stock prices and thU.S. market caps relative to their peers. Overall the big U.S. stocks’ Q1’19 results looked pretty mixed, with slight sales growth and strong earnings growth. But these growth rates are really slowing, and valuations remain extreme relative to underlying profits.

From the ends of Q1’18 to Q1’19, the S&P 500 rallied 7.3% higher. While solid, that’s not much relative to the extreme euphoria and complacency during this latest earnings season. These stock markets could really be in a massive-triple-top scenario after this record bull run, a menacing bearish omen. The SPX initially peaked at 2872.9 in late January 2018, mere weeks after those record corporate tax cuts went into effect.

Then it quickly plunged 10.2% in 0.4 months, a sharp-yet-shallow-and-short correction. But with overall SPX earnings growth exceeding 20% YoY comparing post-tax-cut quarters to pre-tax-cut ones, this key benchmark clawed back higher and hit 2930.8 in late September 2018. That was merely a 2.0% marginal gain over 7.8 months which saw some of the strongest corporate-profits surges ever from already-high levels.

From there the SPX plummeted 19.8% in 3.1 months in that severe near-bear correction largely in Q4. This trend of slightly-better record highs followed by far-worse selloffs is troubling. By late April 2019 the SPX had stretched to 2945.8, jU.S.t 2.5% above its initial peak 15.1 months earlier. Such paltry gains in a span with record corporate tax cuts and resulting torrid earnings growth should really give traders pause.

Technically these three major record highs look like a massive triple top. The big U.S. stocks’ Q1 results are critical to supporting or refuting this bearish technical picture. The SPX/SPY top 34 did enjoy superior market-cap appreciation from the ends of Q1’18 to Q1’19, averaging 12.8% gains which ran 1.7x those of the entire SPX. That exacerbated the concentration of capital in the largest SPX stocks, the mega-cap techs.

As Q1 ended, 5 of the 6 largest SPX stocks were Microsoft, Apple, Amazon, Alphabet, and Facebook. Together they accounted for a staggering 15.8% of this flagship index’s entire market cap, closing in on 1/6th! These companies are universally adored by investors, owned by the vast majority of all funds and constantly extolled in glowing terms in the financial media. Investors think mega-cap techs can do no wrong.

Last summer these incredible businesses were viewed as recession-proof, effectively impregnable. But even if there’s some truth to that, it doesn’t guarantee mega-cap-tech stock prices will weather a stock-market selloff. During that 19.8% SPX correction mostly in Q4, these 5 dominant SPX stocks and another SPX-top-34 tech darling Netflix averaged ugly 33.3% selloffs! They amplified the SPX’s decline by 1.7x.

No matter how amazing the sales growth among the mega-cap techs, they aren’t only not immune to SPX selloffs but their lofty stock prices make them more vulnerable. Overall the SPX/SPY top 34 companies reported Q1’19 revenues of $969.3b, which was 0.9% YoY higher than the top 34’s in Q1’18. That’s not great performance considering how universally-loved and -owned these companies are among nearly all funds.

Those 6 mega-cap tech stocks did far better, enjoying order-of-magnitude-better revenues growth of 9.9% YoY! Excluding them the rest of the SPX top 34 actually saw total sales slump 1.8% lower YoY, which sure doesn’t sound like a strong economy. If this trend of stalling or slowing revenue growth continues, profits growth will have to start falling sharply in future quarters. Earnings ultimately amplify sales trends.

Even more bearish, Wall Street analysts headed into Q1’19’s earnings season expecting all 500 SPX companies to enjoy 4.7% total revenues growth. But the top 34 that dominate the U.S. stock markets did much worse at 0.9% even with mega-cap techs included. That was definitely a sharp slowdown too, as the SPX top 34 saw 4.2% YoY sales growth in Q4’18. Slowing revenue growth is a real threat to the stock markets.

Remember the SPX surged dramatically in Q1, fueling quite-euphoric sentiment leading into quarter-end. At the same time traders mostly believed that a U.S.-China trade deal would soon be signed, removing the trade-war risks. High tariffs are a serious problem for the gigantic multinational companies leading the SPX, potentially heavily impacting sales. Yet revenue growth was already slowing even before this week!

Trump had twice delayed hiking U.S. tariffs on Chinese imports from 10% to 25%, a good-faith sign giving time for real trade-deal negotiations. But his patience ran out this past Sunday after China backtracked on key previoU.S. commitments. So Trump tweeted the current 10% U.S. tariffs on $200b of annual Chinese imports would surge to 25% today, and warned that 25% tariffs were coming “shortly” on another $325b!

China will retaliate as long as high U.S. tariffs remain in effect. That will really retard U.S. sales from top-34 SPX companies in that country. Beloved market-darling Apple is a great example. This second-biggest stock in the S&P 500 did $10.2b or 17.6% of its Q1’19 sales in China! The U.S.-China trade war heating up in a serious way portends even-weaker revenues going forward for the big U.S. stocks dominating the SPX.

The total operating cash flows generated by the top 34 SPX/SPY companies looked like a disaster in Q1, plummeting 64.4% YoY to $67.8b. Thankfully that is heavily skewed by a couple of the major U.S. banks. JPMorgan Chase and Citigroup reported staggering negative OCFs of $80.9b and $37.6b in Q1, due to colossal $123.1b and $30.4b negative changes in trading assets! This seems really confusing to me.

Mega-bank financials are fantastically-complex, and no one can hope to understand them unless deeply immersed in that world. I’ve been a certified public accountant for decades now, spending vast amounts of time buried in 10-Qs and 10-Ks to fuel my stock trading. Yet even with my background and experience I can’t interpret mega-bank results. It seems weird trading assets plummeted in Q1 as the SPX surged sharply.

But rather than getting bogged down in mega-bank arcania that may be impossible to comprehend by outsiders, we can just exclude the four SPX-top-34 mega-banks from our OCF analysis. They include JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup. Without them, the rest of the SPX top 34 reported total OCFs of $163.2b in Q1’19. That was dead-flat ex-banks, up just 0.3% YoY from Q1’18’s OCFs.

So the big U.S. stocks’ operating-cash-flow generation really slowed too in Q1, stalling out compared to hefty 11.5% YoY growth in Q4’18. That’s another sign that the U.S. economy must be slowing despite the red-hot stock markets. That’s ominous and bearish considering the coming headwinds if the trade wars continue and if the stock markets roll over decisively. Future quarters’ business environments won’t be as good.

Earnings were a different story entirely last quarter, soaring dramatically among the SPX/SPY top 34. They totaled $149.8b, surging an enormous 36.1% YoY! But that was skewed way higher by Warren Buffett’s famous Berkshire Hathaway, the biggest SPX stock after the mega-cap techs. BRK reported a monster Q1 profit of $21.7b, compared to a $1.1b loss a year earlier. That accounted for 1/7th of the top 34’s total.

But Berkshire’s epic profits are due to the sharp stock-market rebound rally, not underlying operations. A new accounting rule that Warren Buffett hates and rails against at every opportunity requires unrealized capital gains and losses to be flushed through quarterly profits. Thus when the SPX plunged in Q4’18, BRK reported a colossal $25.4b GAAP loss. That was largely reversed in Q1’19 with its gigantic $21.7b gain.

Excluding the $16.1b of BRK’s Q1 profits that were mark-to-market stock-price gains, the SPX top 34’s total profits grew 21.5% YoY to $133.6b in Q1. That’s still impressive, but it masks some big problems on the corporate-earnings front. Those 6 elite mega-cap tech companies dominating the SPX actually saw their collective Q1 GAAP profits plunge 11.2% YoY! Apple, Alphabet, and Facebook suffered sharp declines.

Usually mega-cap tech stocks are the profits engine driving the entire SPX higher. If these market-darling companies that are universally-loved and -held struggled with earnings growth in Q1, what does that say about profits going forward? And again profits can be manipulated quarter-to-quarter by playing with all kinds of accounting estimates. So if anything corporate profits are overstated instead of understated.

One of Wall Street’s great farces is the game of comparing quarterly results to expectations instead of what they were in the comparable quarter a year earlier. Mighty Apple is a great example, reporting after the close on April 30th. Its Q1 earnings per share and sales of $2.47 and $58.0b came in ahead of Wall Street expectations of $2.37 and $57.5b. So Apple’s stock surged 4.9% the next day on those “great results”.

But that expectations bar had been lowered dramatically, which is the only reason Apple beat. On an absolute year-over-year basis compared to Q1’18, Q1’19 saw sales drop 5.1%, OCFs plummet 26.3%, and earnings plunge 16.4% YoY! That was quite weak, and couldn’t be considered good by any honest measure. In this recent Q1 earnings season, the fake expectations game obscured plenty of real weakness.

Yet overall SPX-top-34 profits growth still remained strong, with companies suffering drops offset by other companies seeing big jumps. But earnings can’t be considered in isolation, they are only relevant relative to underlying stock prices. Imagine you own a rental house and someone offers you $1000 a month to move in. The reasonableness of that earnings stream is totally dependent on the value of your property.

If your house is worth $100k, $1k a month looks great. But if it’s worth $1m, $1k a month is terrible. The profits anything generates are only measurable relative to the capital invested in that asset. The classic trailing-twelve-month price-to-earnings ratios show how expensive stock prices are relative to underlying corporate profits. Big SPX-top-34 earnings growth isn’t bullish if overall profits are low compared to stock prices.

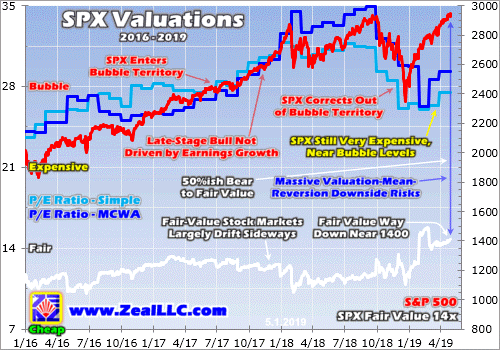

At the end of Q1’19 proper before these Q1 results were reported, the SPX/SPY top 34 component stocks averaged TTM P/Es of 30.4x. That is definitely improving compared to the prior four quarters’ trend of 46.0x, 53.4x, 49.0x, and 39.7x. But 30.4x is still dangerously high absolutely. Over the past century-and-a-quarter or so, fair value for the U.S. stock markets was 14x. Double that at 28x is where bubble territory begins.

So the big U.S. stocks were literally trading at bubble valuations exiting Q1! Their stock prices were far too high relative to their underlying earnings production compared to almost all of U.S. stock-market history. And this wasn’t just a mega-cap-tech-stock thing, with these elite companies often being bid to really-high valuations compared to other sectors. The 6 mega-cap techs we’ve discussed indeed averaged a crazy 52.0x.

But the other 28 top-34-SPX companies remained very expensive near bubble territory even excluding the tech giants, averaging 25.8x! Even the strong Q1’19 earnings growth didn’t help much. At the end of April as those Q1 results started to work into TTM P/E calculations, the SPX top 34 averaged a slightly-higher P/E of 31.0x. Literal bubble valuations with stock markets trading near all-time record highs are ominous.

Just last Friday when the SPX closed right at its highest levels in history, I wrote a contrarian essay on these “Dangerous Stock Markets”. It explained how high valuations kill bull markets, summoning bears that are necessary to maul stock prices sideways to lower long enough for profits to catch up with lofty stock prices. These fearsome beasts are nothing to be trifled with, yet complacent traders mock them.

The SPX’s last couple bears that awoke and ravaged due to high valuations pummeled the SPX 49.1% lower in 2.6 years leading into October 2002, and 56.8% lower over 1.4 years leading into March 2009! Seeing big U.S. stocks’ prices cut in half or worse is common and expected in major bear markets. And there’s a decent chance the current bubble valuations in U.S. stock markets will soon look even more extreme.

Over the past several calendar years, earnings growth among all 500 SPX companies ran 9.3%, 16.2%, and 20.5%. This year even Wall Street analysts expect it to be flat at best. And if corporate revenues actually start shrinking due to mounting trade wars or rolling-over stock markets damaging confidence and spending, profits will amplify that downside. Declining SPX profits will proportionally boost valuations.

If the big U.S. stocks’ fundamentals deteriorate, the overdue bear reckoning after this monster bull is even more certain. Cash is king in bear markets, since its buying power grows. Investors who hold cash during a 50% bear market can double their holdings at the bottom by buying back their stocks at half-price. But cash doesn’t appreciate in value like gold, which actually grows wealth during major stock-market bears.

Gold investment demand surges as stock markets weaken, as we got a taste of in December. While the SPX plunged 9.2%, gold rallied 4.9% as investors flocked back. The gold miners’ stocks which leverage gold’s gains fared even better, with their leading index surging 10.7% higher. The last time a major SPX selloff awakened gold in the first half of 2016, it soared 30% higher fueling a massive 182% gold-stock upleg!

Absolutely essential in bear markets is cultivating excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. While Wall Street will deny this coming stock-market bear all the way down, we will help you both understand it and prosper during it.

We’ve long published acclaimed weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q1 we’ve recommended and realized 1089 newsletter stock trades since 2001, averaging annualized realized gains of +15.8%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is the big U.S. stocks’ Q1’19 results were pretty mixed despite the surging stock markets. Revenues and operating cash flows only grew slightly, which were sharp slowdowns from big surges in previous quarters. While earnings somehow defied sales to soar dramatically again, that disconnect can’t persist. A slowdown looked to be underway even before the U.S.-China trade war flared much hotter this week.

Even the surging corporate profits weren’t enough to rescue super-expensive stock markets from extreme bubble valuations. They are what spawn major bear markets, which are necessary to maul stock prices long enough for valuations to mean revert lower. Make no mistake, these overvalued stock markets are still an accident waiting to happen. Stock investors should diversify, adding substantial gold allocations.

Adam Hamilton, CPA

May 15, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

These record U.S. stock-market levels are very dangerous, riddled with extreme levels of euphoria and complacency. Largely thanks to the Fed, traders are convinced stocks can rally indefinitely. But stock prices are very expensive relative to underlying corporate earnings, with valuations back up near bubble levels. These are classic topping signs, with profits growth stalling and the Fed out of easy dovish ammunition.

Stock markets are forever cyclical, meandering in an endless series of bulls and bears. The latter phase of these cycles is inevitable, like winter following summer. Traders grow too excited in bull markets, and bid up stock prices far higher than their fundamentals support. Subsequent bear markets are necessary to eradicate unsustainable valuation excesses, forcing stock prices sideways to lower until profits catch up.

This latest bull market grew into a raging monster largely fueled by extreme Fed easing. At its latest all-time record peak hit just this week, the flagship US S&P 500 broad-market stock index (SPX) has soared 335.4% higher over 10.1 years! That makes for the second-biggest and first-longest bull in US history, only possible because it gorged on $3625b of quantitative-easing money printing by the Fed over 6.7 years.

That epic 5.3x mushrooming of the Fed’s balance sheet peaked in February 2015, when the SPX was just clawing over 2100. It soon coasted to a 2130.8 topping in May 2015, before trading sideways to lower for 13.7 months without Fed QE. Modest new highs weren’t seen until July 2016, after the U.K.’s Brexit-vote surprise kindled hopes for more central-bank easing. Another surprise event drove the final third of this bull.

The November 2016 elections were a Republican sweep, with Trump winning the presidency while his party controlled both chambers of Congress. So the SPX started surging to new record highs, initially on hopes for big tax cuts soon and later on record corporate tax cuts becoming law. That ultimately propelled the SPX to 2872.9 in late January 2018 and 2930.8 in late September 2018, lofty new all-time record highs.

But paraphrasing an ancient Biblical passage from Job, the Fed gave then the Fed took away. Right after the SPX peaked, the Fed ramped its year-old quantitative-tightening campaign to full speed in Q4’18. QT was supposed to unwind a large fraction of that $3625b of QE-conjured money, shrinking the Fed’s crazy-bloated balance sheet. $50b per month of QT monetary destruction had to be this QE-fueled bull’s death knell!

Indeed the stock markets crumbled under that Fed-tightening onslaught, plunging 19.8% over the next 3.1 months into late December 2018. That severe correction was right on the verge of crossing the -20% threshold into new-bear territory. Over a third of those serious losses happened in just 4 trading days after the Fed chairman declared full-speed QT was “on automatic pilot”. By that time the SPX was very oversold.

Stock-market extremes never last long, with big and sharp mean-reversion bounces following major selloffs. The SPX reversed hard and soared into early 2019, already 12.3% higher by late January. Then the Fed’s first policy decision after that stock-crushing QT-autopilot one saw this central bank completely cave to the stock markets. It removed references to further rate hikes and declared it was ready to adjust QT.

That dovishness unleashed more waves of momentum buying. By the eve of the Fed’s next meeting in mid-March, the SPX had rocketed 20.5% above its severe-correction near-bear low. But that wasn’t good enough for the Fed, which slashed its future-rate-hike outlook while declaring it would essentially stop QT by September 2019. That is very premature, implying less than 23% of the Fed’s total QE will be unwound!

That goosed the stock markets again, helping push the SPX to an enormous 25.3% rebound-rally gain by this week. At 2945.8, it had edged 0.5% above late September’s then-record peak. With stock markets more than regaining their big losses, euphoria and complacency exploded again. These herd emotions have proven dangerous in market history, marking major toppings including terminal bulls rolling over to bears.

Euphoria is simply “a strong feeling of happiness, confidence, or well-being”. It is always accompanied by complacency, which is “a feeling of contentment or self-satisfaction, especially when coupled with an unawareness of danger or trouble”. This perfectly describes the stock markets’ sentiment-scape in recent months. Speculators and investors just love these lofty stock prices, with virtually no fear of material selloffs.

While euphoria and complacency are ethereal and unmeasurable, they can be inferred. The classic VIX fear gauge is the most-popular way. It quantifies the implied volatility options traders expect in the SPX over the next month, as expressed through their collective trades. While a high VIX reveals fear, a low one shows the direct opposite which is complacency. In mid-April the VIX revisited ominous bull-slaying levels.

This chart superimposes the SPX over its VIX sentiment indicator over the past several years or so. This monster Fed-QE-fueled stock bull sure looks to be carving a massive triple top in its terminal phase. At best in late April, the SPX had merely clawed back 2.5% over its initial peak of late January 2018. That’s terrible progress across 15.1 months where the biggest corporate tax cuts in US history greatly boosted profits.

While the first two-thirds of this monster bull were directly driven by the Fed’s extreme QE, the final third was corporate-tax-cut driven. Starting with that November 2016 Republican sweep, there was enormous anticipation of what eventually became the Tax Cuts and Jobs Act. Signed into law in December 2017, it went into effect as 2018 dawned. Its centerpiece was slashing the US corporate tax rate from 35% to 21%.

The SPX surged 19.4% in 2017 in the thrall of taxphoria hopes, driving 62 new record-high closes out of 251 trading days! The first 18 trading days of 2018 saw another 14 more, catapulting both euphoria and complacency off the charts. The VIX slumped into the 9s early that peaking month, proving that fear was nonexistent. Virtually no one expected a selloff when the SPX peaked at 2872.9, when the VIX closed at 11.1.

But just when traders were convinced stock markets could rally indefinitely with no material selloffs, the SPX suddenly nosed over into its first correction in 2.0 years. While sharp yet shallow and short at a 10.2% loss in just 0.4 months, it was a warning shot. Even with elite SPX companies’ corporate profits expected to soar 20%+ that year due to those big tax cuts, stock markets were already too high to rally much.

After that minor flash correction, the SPX started marching higher again throughout 2018. It wasn’t able to eclipse January’s maiden peak until late August, and ultimately crested merely 2.0% above it in late September. Such meager gains again suggested the corporate tax cuts were nearly fully priced in during 2017, leaving little room for additional gains. The day the SPX peaked at 2930.8, the VIX closed at 11.8.

Once again traders’ euphoria and complacency were extreme. The pressure on contrarians to capitulate was immense. But given the extreme stock-market technicals, sentiment, and valuations, I stuck to my guns warning how dangerous the stock markets were. Just a week after that all-time record high in the SPX, I published an essay warning “Fed QT is Bull’s Death Knell” one trading day before QT hit terminal velocity.

Indeed the stock markets fell hard, plunging 19.8% over 3.1 months into late December! That correction was much larger and more menacing than early 2018’s, on the edge of formal bear-market territory. And it happened despite SPX companies’ earnings actually blasting 20.5% higher year-over-year in 2018. Two corrections, including a serious one, in one of the best corporate-profits years on record should give pause.

The stock markets were due for a sharp mean-reversion rebound higher after such a steep drop. But the Fed waxing hyper-dovish and killing both its rate-hike cycle and QT really artificially extended it. Just over half the total rebound rally came after the Fed utterly surrendered to stock traders starting in late January. Many larger SPX-rally days clustered around dovish Fed announcements, they really amplified this rally.

It looked and felt exactly like a bear-market rally, the biggest and fastest ever witnessed in stock markets. The SPX soared in a symmetrical V-bounce out of late December’s deep lows. Those gains were front-loaded, fast initially but fading in recent months despite the Fed’s super-dovish jawboning. That severe near-bear correction that spawned this rally also fit the definition of a waterfall decline, an ominous omen.

They are 15%+ SPX selloffs without any interrupting countertrend rallies exceeding 5%. Since 1946 this had happened only 19 previous times. After every single past selloff, 100% of the time, the SPX retested its waterfall-decline lows! All 19 happened in bear markets. After these retests, fully 15 of the 19 were followed by new lower lows as those bears deepened. Only 4 of the 19 waterfall retests climaxed their bears.

So market history is crystal-clear in warning that the wild stock-market action of the past 7.3 months is exceedingly dangerous technically. Yet euphoria and complacency still exploded again in March and April as the SPX kept stretching skywards. By mid-April as the SPX clawed back up to 2907.4, the VIX fell back under 12.0 on close. Those were the lowest levels of fear seen since October 3rd, a bearish portent.

While that was a couple weeks after the SPX’s late-September then-record peak, this leading stock index was still just 0.2% lower. The selling that would grow into the severe near-bear correction began the very next day, and snowballed from there. Right when traders again delude themselves into believing stock markets can rally indefinitely, the hard reality of market cycles slams them like a sledgehammer to the skull.

Extreme levels of euphoria and complacency are always very dangerous, presaging major stock-market selloffs. Low VIX levels following record or near-record stock-market highs should not be trifled with, but considered a dire warning of serious downside risks. Very-high technicals breed very-lopsided sentiment, blinding traders to markets’ perpetual cyclicality. Today’s risks are compounded by near-bubble valuations.

For a century-and-a-quarter or so before the Fed’s insane QE experiment starting in late 2008, the US stock markets had averaged trailing-twelve-month price-to-earnings ratios around 14x earnings. That is considered fair-value, which makes sense. The reciprocal of 14x is 7.1%, which is a fair rate for both investors to earn to let companies use their saved capital and for companies to pay to use those same funds.

But valuations oscillate well above and below fair value in great waves that correspond with bull and bear markets. In bulls stocks are enthusiastically bid to high valuations not justified by their underlying profits. Valuation extremes start at twice fair value, 28x trailing earnings which is formally bubble territory. That necessitates bears to maul stock prices long enough for earnings to catch up, but stocks usually overshoot.

While major bull markets end above 28x, major bear markets often end between 7x to 10x. That’s the time investors should throw all their capital at the stock markets, when stocks are dirt-cheap and deeply out of favor. But instead they foolishly buy high near bull-market tops, which often leads to selling low later at catastrophic losses. The SPX valuations during this 15-month triple-top span have been scary-high.

This next chart shows the actual SPX in red, superimposed over the average trailing-twelve-month price-to-earnings ratios of its 500 elite companies. Their simple average at the end of every month is shown in light blue, and is what I’m using in this essay. The dark-blue line instead weights SPX-component P/Es by their companies’ market capitalizations. The white line shows where the SPX would be at 14x fair-value.

Remember the final third of this monster bull erupted on taxphoria after Trump won the presidency. But following trillions of dollars of QE before that, the SPX wasn’t cheap heading into November 2016. These elite stocks averaged TTM P/Es of 26.3x, just shy of 28x bubble territory. Interestingly that was about the same valuation as the 25.9x when QE ended in February 2015. Stocks had long been very expensive.

SPX corporate earnings did rise nicely in 2017, up about 16%. Republicans streamlining regulations was a factor, but more important was the widespread optimism from stock markets surging to endless new record highs. But the problem was stocks were already so overvalued that higher profits barely made a dent. At best that year the fair-value SPX at 14x hit 1296.0, a staggering 52% below the SPX’s 2017 high!

The SPX first crossed that 28x bubble threshold in late November 2016 after stocks surged higher on that Republican sweep. Valuations hung around 28x until July 2017 when they started climbing even higher. By late January 2018 just after the SPX’s initial peak, its elite companies were averaging TTM P/Es way up at 31.8x! While bubble valuations can persist while euphoria lasts, they are very dangerous for stocks.

SPX corporate-earnings growth in 2018 was amazing, exceeding 20% year-over-year thanks to those record corporate tax cuts. The four quarters of 2018 were the only ones comparing post-tax-cut and pre-tax-cut profits, an enormous one-off discontinuity. Yet damningly the valuations still didn’t retreat, in late September just after the SPX’s record peak its components were still averaging extreme 31.4x TTM P/Es.

That severe near-bear correction largely in Q4 last year certainly helped, dragging valuations back down out of bubble territory. But even at the end of December just after the lows, the SPX was still sporting a 26.1x valuation. That was near bubble territory, right around the levels just before Trump was elected. No bear market would end its predations and start hibernating while valuations remained so darned high!

In recent months many Wall Street apologists have claimed that severe correction was effectively a very-short-lived bear market since it was so close to 20% on a closing basis. They argue that means a new bull is underway that can run for years more. But bears don’t give up their ghosts after a single selloff with price-to-earnings ratios still near bubble levels. Bears ravage until valuations are mauled back under 14x.

Interestingly valuations haven’t soared back up with the massive rebound rally so far this year. By the end of April, the SPX components’ average P/E had only returned to 27.5x. That’s not greatly above the late-December levels. This was due to blowout Q4’18 earnings from SPX companies, the last quarter with profits compared across the Tax Cuts and Jobs Act. Q4’17 also rolled off, which the TCJA heavily distorted.

But 27.5x is still just under bubble territory, dangerously-expensive levels for stocks achieving record highs again. If the inevitable bear following the past decade’s enormous Fed-inflated monster bull just pushed stocks back down to 14x fair value, the SPX would have to plunge way back near 1400. That’s a heck of a long ways down from here, a 52% drop. Cutting stocks in half is right in line with bear-market precedent.

The SPX’s last bear market ran from October 2007 to March 2009, and pummeled this leading American stock index a gut-wrenching 56.8% lower in 1.4 years. That bear-market bottom birthed this current bull, when the SPX traded down to 12.6x earnings. Before that the SPX suffered another bear from March 2000 to October 2002, a 49.1% drop over 2.6 years. So 50%ish SPX losses are par for the course in bears!

Several factors could make this long-overdue next bear even worse. In 2016, 2017, and 2018, the elite SPX companies’ profits grew 9.3%, 16.2%, and 20.5% YoY. This year even Wall Street is forecasting earnings to be flat at best. There’s a real possibility they will even contract in 2019, the first year comparing post-tax-cut quarters. Stalling or shrinking corporate profits make near-bubble valuations even more extreme.

Lower profits actually push valuations even higher, increasing the valuation pressure for a major bear market. And with average month-end SPX TTM P/Es running 30.5x in 2018 at 20% profits growth, there’s no way similar high valuations will fly this year with zero profits growth. The more quarterly earnings fail to climb, the more worried traders will get over high stock prices and the more likely they will start selling.

And after the second-largest and first-longest bull market in US stock-market history, mostly driven by extreme Fed easing no less, the subsequent bear should be proportionally massive. There’s a fairly-high chance this bear won’t stop brutalizing stocks until the average SPX P/E falls near half fair-value around 7x earnings. That’s where the biggest bears in the past have ended, valuations overshot way under 14x.

Finally the Fed is going to have a hard time riding to the rescue again since it has expended all its easy dovish ammunition. It really only has three options left for another dovish surprise, and the latter two are very serious decisions. Top Fed officials’ outlook for rates in their collective dot-plot forecast can still be lowered to show cuts coming. But since these guys downplay the dot plot, that won’t mollify traders for long.

That leaves actually cutting rates or birthing QE4, which are huge course changes that the Fed can’t take lightly or revoke without panicking stock markets! With the Fed just about out of dovish rabbits to pull out of its hat, it doesn’t have many options to slow the selling when stock markets inevitably turn south again. Cutting rates or restarting QE may even exacerbate any selloff, worrying traders about what so scared the Fed.

The overdue bear market is still coming, make no mistake. Extreme technicals, sentiment, and valuations assure it. Investors really need to lighten up on their stock-heavy portfolios, and protect themselves with cash and gold. Holding cash through a 50% bear market allows investors to buy back their stocks at half-price, doubling their holdings. But unlike cash gold actually appreciates in value during bears, growing weath.

Gold investment demand surges as stock markets weaken, as we got a taste of in December. While the SPX plunged 9.2%, gold rallied 4.9% as investors flocked back. The gold miners’ stocks which leverage gold’s gains fared even better, with their leading index surging 10.7% higher. The last time a major SPX selloff awakened gold in the first half of 2016, it soared 30% higher fueling a massive 182% gold-stock upleg!

Absolutely essential in bear markets is cultivating excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. While Wall Street will deny this coming stock-market bear all the way down, we will help you both understand it and prosper during it.

We’ve long published acclaimed weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q1 we’ve recommended and realized 1089 newsletter stock trades since 2001, averaging annualized realized gains of +15.8%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is these stock markets are very dangerous. A monster bull has been topping over the past year-and-quarter, leading to extreme technicals, sentiment, and valuations. Traders’ euphoria and complacency have been running at bull-slaying levels, while valuations remain way up near perilous bubble territory. All this is happening as corporate profits flatline after surging dramatically on the corporate tax cuts.

Like after every past waterfall decline, the stock markets are due to roll over and retest their deep late-December lows. Odds are they will fail, confirming a major new bear market. And the Fed doesn’t have much dovish ammunition left to retard the heavy selling. Gold investment demand will surge as stocks finally face their reckoning after this artificially-amplified bull. That will push gold and its miners’ stocks far higher.

Prudent profit booking into strength in this gold bull market is important.

Thanks,

Morris Hubbartt

Unique Introduction For Website Readers: Send me an email to signals@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

Stay alert for our Super Force alerts, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

Frank Johnson: Executive Editor, Macro Risk Manager.

It’s time for the queen of assets to rest and consolidate. Nothing goes up in a straight line, and that’s certainly true for gold!

Please click here now. Double-click to enlarge this daily gold chart.

A pullback to about $1250 would be a healthy 50% retracement of the $100 rally from $1200 to $1300.

Gold begins 2019 with some very positive news in play. Please click here now. After a two-year hiatus, China’s central bank is back in gold market action!

The bank had been consistently buying about 15-20 tons of gold a month. When those purchases are added to buying from Russia and other central banks, they are quite price-supportive.

It’s great to see China back on the buy, and analysts in India are projecting a ramp-up in gold imports there of about 20% for the first six months of 2019.

The ECB (Europe’s central bank) is projecting higher inflation and easing growth for 2019.

The love trade is healthy, the central bank trade is healthy, and global stock markets are on the rocks.

On that note, please click here now. Double-click to enlarge. I’m a bit worried that the US stock market rally could peter out quickly.

Please click here now. Institutional money managers are cutting back their allocations to US equities, and rightly so.

The business cycle is entering the eighth and ninth innings, wage inflation is poised to spike in full-time jobs, and earnings have clearly plateaued.

Please click here now. China’s central bank and government have vastly more “wiggle room” than America’s do to stimulate the economy.

China’s stimulus is inflationary, and that’s good news for gold.

The U.S. government is shut down. That’s not a position of strength, to put it mildly. These shutdowns have happened so many times that citizens are now numb and don’t seem to care.

It’s not a good thing; the government just can’t seem to break its addiction to borrowing more and more money.

The U.S. government has been very vocal in its opposition to the modest interest rate rates from the Fed. I don’t see any economic stress from these hikes, and senior citizens have been paid nothing in their savings accounts for years.

Rate hikes are an indicator that inflation is in the air. They haven’t hurt gold, they help senior citizens, and they put pressure on banks to make business loans rather than finance stock market buybacks to enrich corporate directors.

Rate hikes do put pressure on the ability of the U.S. government to borrow ever-more money, and that pressure is good.

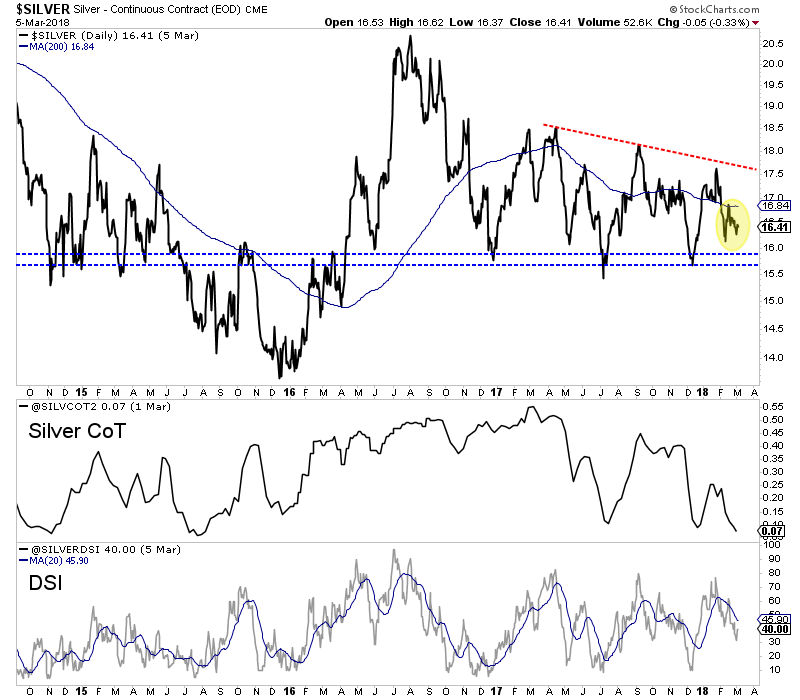

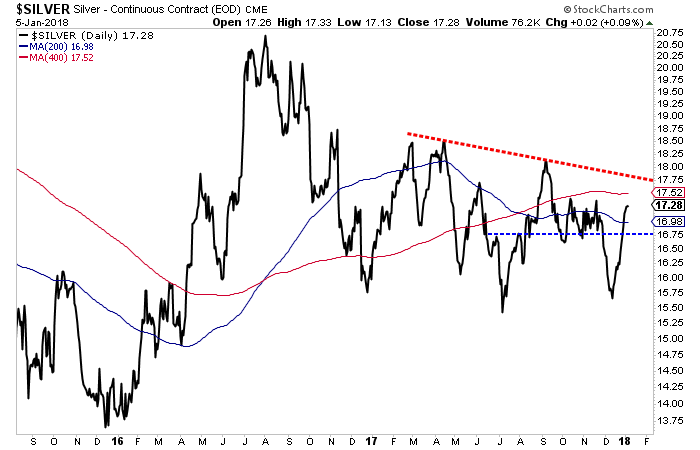

Please click here now. Double-click to enlarge this daily silver chart.

The uptrend is solid. A pullback is normal, expected, and healthy. Note the Fibonacci lines in play around the demand line of the uptrend channel.

Silver feels almost as solid as gold does right now, and that’s likely due to the growing threat of stagflation throughout much of the world.

Please click here now. Double-click to enlarge this nice GDX daily chart.

Like most sectors of the precious metals asset class, GDX is taking a breather after it successfully penetrated key resistance in the $20.70 area.

From a technical perspective, the range trade in the $20-$21.50 area has a 67% chance of being resolved with a rally to $23. The current consolidation could be the last opportunity for excited investors to buy in this price zone before GDX moves above $23 and stays there for quite a long period of time!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Silver Stocks Rock!” report. I highlight the SIL and SILJ ETF component stocks that are poised to enter January like silver bullets shot out of a golden gun! I include key tactics to keep investors on the winning side of the action… in both the short and long term!

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

The beleaguered gold stocks are recovering from their late-summer capitulation, enjoying a solid young upleg as investors gradually return. Their buying has pushed the leading gold-stock ETF near a major triple breakout technically. That event should really boost capital inflows into this sector, accelerating the rally. A major gold and gold-stock buying catalyst is likely imminent too, a more-dovish Fed this week.

The gold miners’ stocks have always been a small contrarian sector, a little-watched corner of the stock markets. But they’ve been even more unpopular than usual in recent months. That pessimistic sentiment is driven by price action, which has mostly proven poor in 2018. That’s really evident in the performance of the flagship gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF which is struggling.

As of the middle of this week, GDX was down 12.0% year-to-date. That leveraged gold’s YTD decline of 4.4% by 2.7x, which is perfectly normal. Because gold-stock earnings are heavily dependent on prevailing gold levels, gold-stock prices tend to amplify gold’s moves by 2x to 3x. That’s a double-edged sword, really profitable when gold rallies but cutting deeply when it retreats. The drawdowns are challenging to weather.

But gold stocks’ inherent leverage to gold is starting to work again on the upside, portending big gains ahead. This first chart looks at the major gold stocks’ technicals through the lens of GDX over the past several years. This sector soared in a new bull market, plunged with gold after Trump’s surprise election win goosed the stock markets, consolidated sideways to base, and then suffered an extreme capitulation selloff.

Investors and speculators often forget how explosive gold-stock upside is when gold is powering higher in an upleg. In largely the first half of 2016, GDX skyrocketed 151.2% higher in just 6.4 months! Capital just flooded back into the gold miners driven by a new gold bull’s parallel 29.9% upleg. That catapulted GDX to very-overbought levels and a 3.3-year high in mid-2016. So a normal correction got underway soon after.

GDX found support at its critical 200-day moving average, which is often the strongest support zone seen in ongoing bull markets. But that failed in November 2016 after an anomalous surprise. Trump defied the polling and odds to win the presidency while Republicans controlled both chambers of Congress. So the stock markets soared in that election’s wake on euphoric hopes for big tax cuts soon. Gold wilted on that rally.

So the gold stocks naturally followed it lower, again mirroring and amplifying its price action. After it had enjoyed stellar 5.1x upside leverage to gold in its powerful H1’16 upleg, GDX dropped 39.4% over the next 4.4 months. That leveraged gold’s own correction by 2.3x, relatively low in that usual 2x-to-3x range. GDX soon bounced sharply with gold and established a new consolidation trading range between $21 to $25.

The major gold stocks mostly meandered within that GDX range for 21.5 months. While it was vexing at times to see upside-breakout attempts fail, basing consolidations are very bullish. They provide time for bullish newer investors to acquire shares from bearish exiting ones, establishing new price norms well above previous bear-market lows. And the $23 midpoint of that GDX trading range proved relatively high.

This gold-stock bull was born out of fundamentally-absurd lows of GDX $12.47 in mid-January 2016. It peaked at $31.32 in early August that year. Oscillating around $23 on balance, GDX was basing 4/7ths up into its young bull’s entire range. The major gold stocks GDX holds were biding their time waiting for another major gold upleg to catapult them higher. They nearly broke out above $25 in early-September 2017.

But that attempt’s failure damaged psychology so traders gradually sold, this small contrarian sector left for dead. The subsequent lower highs over the next 10.4 months into mid-July 2018 formed a downward-sloping resistance line. Gold-stock prices were being compressed into a bearish descending triangle, as lower highs slumped ever closer to that major $21 support. This sector really needed a major gold rally.

Unfortunately the opposite happened this past summer, gold got hammered crushing the weakened gold stocks. The US stock markets were powering higher trying to regain record highs in July and August 2018, heavily retarding gold investment demand. On top of that the U.S. Dollar Index was surging too, both on expectations for more Fed rate hikes and an emerging-markets currency crisis led by the Turkish lira.

So gold-futures speculators started short selling gold at extreme record levels, blasting their aggregate downside bets far up into anomalous territory never before witnessed. Gold fell sharply on that record gold-futures shorting spree, dragging the struggling gold stocks down with it. So in early August GDX plunged and knifed through its longstanding $21 support. That major breakdown spawned self-feeding selling.

Gold stocks are an exceptionally-volatile sector not for the faint of heart. So it is essential to run loose trailing stop losses on gold-stock positions. While these protect investors from excessive losses, they greatly exacerbate selloffs. The lower gold stocks fell this past summer, the more stop losses were hit. These mechanical automatic sell orders then add to the downside pressure, pushing gold stocks lower still.

That vicious circle of selling begetting selling snowballed into an extreme capitulation in gold stocks, as GDX plummeted in August and early September. In just 5 weeks GDX collapsed 17.0%, far worse than gold stocks should’ve performed with gold merely slipping 1.4% lower in that span. That devastated already-shaky sentiment, leaving most investors and speculators to throw up their hands in disgust and flee.

But with GDX being pummeled to a deep 2.6-year low, the major gold stocks were wildly oversold. I explained all this in depth in an essay on gold stocks’ forced capitulation in mid-September. They were due to mean revert dramatically higher after that extreme selling anomaly. And that process has indeed been underway ever since. The gold stocks have been recovering, clawing their way out of those deep lows.