Lithium stocks were hot a year ago, now they’re not. Brine projects in Argentina commanded rapt attention, now no one cares. Clay-hosted Lithium projects were non-starters 2-3 years ago, now they’re in the “maybe” column. Clay-hosted Lithium projects are “unconventional,” meaning untested, and therefore difficult or impossible to fund. However, “unconventional” need not mean difficult to move forward or impossible to fund. What if I told you about a company with a project that had relatively low-grade Lithium, is pre-PEA, and is located in southern Arkansas? Sounds attractive, right? No, it sounds highly….. “unconventional.” Last I checked, Arkansas was not in the heart of the Lithium Triangle.

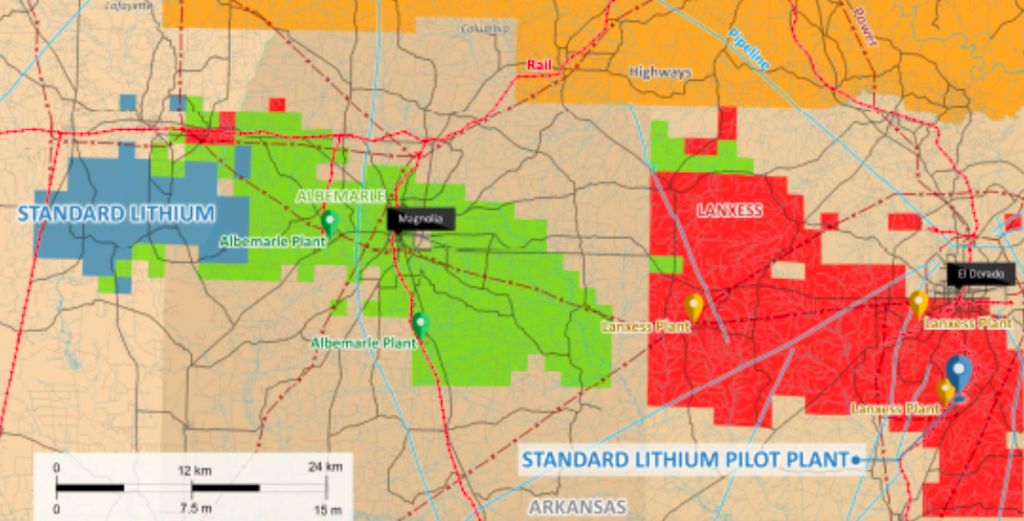

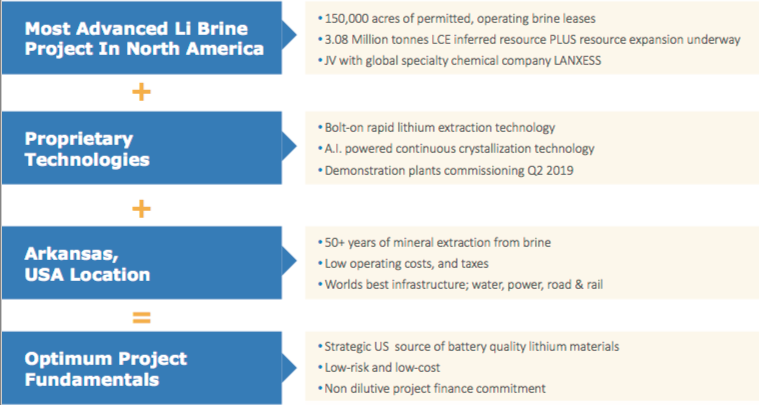

Sometimes unconventional is not all bad. Standard Lithium (TSX-V: SLL) / (OTCQX: STLHF) is a company like no other, and that’s a good thing. Although pre-PEA (PEA now underway), Standard’s 150,000 acre Arkansas Lithium project, called the LANXESS project, has been de-risked in a surprising number of important ways. For instance, while other mining juniors talk about being near, “past producing mines,” the LANXESS project is currently in operation, at massive commercial scale — but producing Bromine from brine, not Lithium (yet). It is a past-producer, but also a present & future producer!

The LANXESS project is hardly early-stage. All of the project’s infrastructure is in place and currently in use. Power, rail, gas, water, tanks, chemicals, pumps, tankers, trucks, drilling equipment, wells, roads, pipelines, etc. 24/7/365, dozens of wells are pumping billions of gallons of brine (salty water), annually, containing Bromine, Lithium and other elements, through 3 nearby processing facilities. The LANXESS project happens to be smack in the middle of North America’s largest brine production & processing facilities. These facilities have been in operation for decades.

Think about the risks avoided here. The Project is in the U.S., thousands of experienced workers are in place working, there’s no discovery or resource expansion risk (the resource is already large enough), the Project is by and large already permitted, it’s in environmental compliance. There’s local community support (no Aboriginal or First Nations issues).

Year-round operations, port access in the Gulf of Mexico, workers go home each night (no fly-in / fly-out). Best of all, the Project is in commercial-scale operation right now, albeit for Bromine. These are logistical items that Lithium companies in Argentina & Chile, not to mention Australia & Canada, would die for, milestones that can take years and hundreds of millions of dollars to obtain.

Not only are operations in place at a large commercial scale, but pumping history, hydrology & geology is all readily available to Standard Lithium for review. This and other data enabled the Company to estimate a 3.1 M metric tonne Lithium Carbonate Equiv. (“LCE“) Inferred resource at the LANXESS project. So, we can be reasonably certain that there’s considerable resource size. However, to be safe we await the Inferred resource being converted to Measured & Indicated, which is expected later this year.

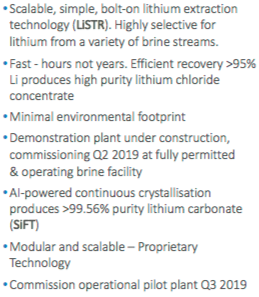

One might think that pulling Lithium out along with the Bromine would be straightforward, it’s not, it proved to be quite a technical challenge. However, a challenge on the verge of being solved, as Standard Lithium is operating a mini pilot plant that has already produced battery-grade Lithium Carbonate. However, this process needs to be scaled up very significantly.

I’ve mentioned several ways in which the Company’s Project is de-risked, taking that theme to a whole new level is a prospective JV with LANXESS (hence the project name). Standard Lithium signed a MOU with LANXESS in May 2018 and a JV term sheet in November. LANXESS is a giant German chemical conglomerate that would provide substantial help on the technical, operational, sales / marketing and R&D fronts.

Assuming reasonable project economics, LANXESS has committed to finance 100% of the commercialization of the Project. LANXESS’, (through its wholly-owned subsidiary) Great Lake Chemicals, operations in Southern Arkansas encompass more than 150,000 acres, 10,000 brine leases & surface agreements and 250 miles of pipelines. LANXESS extracts brine from wells located throughout the area and transports it to 3 Arkansas processing plants through a network of pipelines.

Executing the JV would be huge, LANXESS would own a majority of the Project, but funding is without question the largest risk factor these days. LANXESS funding would be the biggest de-risking event of them all. Several world-class brine projects in Argentina are all but stalled due to a lack of project funding. That’s even though those projects are “conventional” proposing to use conventional solar evaporation ponds. And then there’s Quebec’s Nemaska Lithium, they were billed as fully-funded, until they found a ~C$400M hole in their funding basket. Nothing against Nemaska, Lithium projects are complex and unique. Delays and cost over-runs are the norm.

Standard Lithium’s processing technology, if operating at commercial scale, would process enormous volumes of brine in days vs. over a year for solar evaporation ponds. The technology is designed to be easily and conveniently scalable, it’s modular. If need be, the Company could plan production based on market conditions. Management is not going to run into a ~C$400M cap-ex problem, the amount of operating data available is immense and remember, most of the infrastructure is already in place.

So, what does all of this mean for Standard Lithium? Assuming LANXESS comes on board (LANXESS named Standard Lithium and the Arkansas lithium project during the opening minutes of their 4th Quarter earnings call), they have many risk factors covered, including the biggest risk, project funding. Instead of facing the daunting task of having to raise hundreds of millions in equity capital to fund a commercial development, the Company is probably looking at raising closer to C$25M over the next 18 months. They just closed an C$11M bought deal financing.

Risk Factors

The main risk factor is scaling their proprietary technology from pilot to commercial-scale. With regard to this risk, I think it’s a question of when, not if, the Company achieves this milestone. A moderate delay would be disappointing but would not deliver a fatal blow. Standard Lithium hopes to eventually reach a run-rate of ~20,000 tonnes/yr. LCE. That will likely take several years, after first achieving limited commercial production potentially as early as 2021. Ultimately, production of 30,000+ tonnes/yr. LCE for decades is a possibility, by optimizing the well fields and tapping into the Company’s nearby TETRA Project area.

What might the mid-year PEA show? We don’t know yet, but we can make some educated guesses. Cap-ex? In Argentina, the average Lithium brine project cap-ex requirement from among 6 well known projects is C$540 M. The LANXESS project will be built in stages, so the cap-ex will be substantially lower. Remember, most of the infrastructure is already in place and in operation.

Op-ex should be on the low side as well. For example, the Company has ready access to some of the cheapest chemical reagents in the world. And, the Lithium operations will be sharing some costs with the Bromine operations. Brine exits the Bromine operations at 70 degrees Celsius, so no extra energy needs to be added as it enters the Lithium facilities. Management’s goal is to be in the bottom quartile on the cost curve.

Look at “conventional” brine producer Orocobre Ltd., it’s in year 4 of commercial operation, but is still running at ~70%-80% of nameplate capacity. This is no knock on Orocobre, they were the first new brine project in Argentina in 20 years, it just demonstrates how very difficult each unique brine (chemistry) project is. And the weather, it has been surprisingly rainy this year and last, which is bad news for solar evaporation ponds. Global warming?

In the early-to-mid 2020s there will be fierce competition for scarce resources in Argentina (labor, executives with brine project building experience, consultants, water, power, mining services & equipment, environmental work & construction activities (at 4,000 meter elevations), access to governmental agencies for permits & approvals). Among the 6-10 brine projects in Argentina at PEA-stage or more advanced, several might never reach production. Several others could be delayed by 1,2,3,4 years in reaching nameplate capacities of 20k-35k tonnes/yr. LCE.

Conclusion

Standard Lithium (TSX-V: SLL) / (OTCQX: STLHF) will not be fighting for scarce resources, (another risk avoided) there should be no operating or infrastructure bottlenecks, the weather is not a factor. There won’t be cost blowouts. If a Bank Feasibility Study calls for first production in mid-2021, and LANXESS is committed to project finance, operations & off-take, it will likely happen pretty much on time and on budget.

For hard rock producers in western Australia my understanding is that the situation is a lot better, but we could still see bottlenecks as many hard rock producers try to ramp up supply at the same time. Instead of companies failing, perhaps we will see a wave of M&A in western Australia.

That higher degree of certainty is worth a lot in the wild west of Lithium project development. And, if the brine projects in the Lithium Triangle can’t deliver close to nameplate capacity in the early-to-mid-2020’s, there’s going to be tremendous demand for Standard Lithium’s output, and Lithium prices will likely be high. Who knows, maybe even the “unconventional” clay-hosted Lithium producers will have their day in the sun?

March 29, 2019

Peter Epstein

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Standard Lithium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Standard Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Standard Lithium and the Company was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

by Peter Epstein

CEO Robert Mintak has 2 unconventional lithium projects in the U.S., one of which he believes is de-risked more than most lithium projects around the world due to infrastructure, permitting, jurisdiction and other key factors. While Robert can’t know for sure until Standard Lithium releases a Preliminary Economic Assessment (PEA), it seems likely that cap-ex will be low compared to conventional brine projects. For reasons explained below, op-ex is likely to be in the bottom half of the industry cost curve. The Company’s goal is to be in the bottom quartile.

Standard Lithium is on a clear path to signing a JV with giant German chemical company, LANXESS. If the JV is consummated, LANXESS will be committed to funding commercial development. This would be a tremendous de-risking event for the project and for Standard Lithium. Funding has been a huge challenge for lithium brine projects around the world. Please continue reading to learn more about this unique U.S. lithium project which could reach initial production in 2 years, 2021.

Peter Epstein: Please explain Standard Lithium to readers who are unfamiliar with your company:

Robert Mintak: We are an integrated technology and specialty chemical company. We are listed on the TSX-V as a mining exploration company but we are not exploring, you won’t see any new mineral discovery announcements coming any time soon. Our business model is simple and somewhat unconventional compared to our peers, we believe the fastest way to go into production and to limit investor risk is to form strategic partnerships that allow us to piggyback off the existing infrastructure and investment of massive operating commercial brine assets in the USA.

I have been involved in the lithium sector for the better part of the past decade. My experience and successes in the lithium sector have been in forging strategic relationships and partnerships with large multinational companies and stakeholders. Previous to Standard Lithium at Pure Energy I brought POSCO, Tenova Bateman, SRI and Tesla to the table, at Standard Lithium we have continued that dynamic with the agreements and partnerships executed including NYSE listed Tetra Technologies and of course our announced planned JV with LANXESS.

Epstein: How is your proprietary process different from lithium brine operations like those found in Argentina?

Mintak: First, I would like to state that the project drives the process. Every lithium brine project globally is by and large wholly unique. Not only the chemistry of the brine, when developing the process flow sheet, as a project builder you need to consider access to and cost of, chemical reagents, water, power.

Permitting, extraction & re-injection of brine, access to land and a skilled workforce arefundamental considerations before you even begin bench-scale testing. Trying to force an extraction technology on a project is akin to the square peg round hole analogy.

Going back to your question, our patent-pending selective extraction, technology, we call “LiSTR” vis-a-vis a typical Argentine brine project that would use either solar evaporation ponds or a modified version of solar evaporation with ion exchange. As I mentioned, the project drives the process.

Mintak: It rains in south Arkansas, the land is hilly and forested, evaporation ponds are not an option. There has been significant work done over the years, by researchers, universities, large chemical companies etc. on lithium extraction processes and so we stand on the shoulders of giants or as we like to say, ‘we are boldly going where others have already gone’.

A unique advantage in south Arkansas is access to large volumes of raw brine to process test. Unlike our peers, we can literally open a spigot and fill large IBC’s or totes with brine and ship to our facility for process testing. We do not need to permit a well, or get extraction permits. This cut months off the development timeline and allowed us to test a number of existing extraction processes including, but not limited to; solvent extraction, a variety of ion exchange resins, nanofiltration, and floatation.

Through this test work, we have developed a proprietary process that uses a solid ceramic adsorbent material with a crystal lattice that is capable of selectively pulling Li + ions from the waste brine after it has gone through the bromine-extraction step. The ceramic adsorbent materials are mounted in stirred-tank reactors that contain brine. In the second step, the adsorbent releases the Li + ions for recovery. Importantly, the Li-extraction process takes advantage of the fact that the brine leaves the bromine process heated to ~70°C.

This means that no additional energy is required, the reaction kinetics for the adsorption is suitable. The process is capable of reducing the time required for Li extraction from many months (with the evaporation ponds) to hours, and is capable of producing a high-purity lithium chloride solution for further processing into battery quality compounds. The LiSTR process is designed to be scalable at each stage, from bench scale – mini-pilot- demonstration – commercial. We are using technologies and processes used in other industries, we are not reinventing the wheel, just turning it.

Epstein: How might your cap-ex compare to that of lithium brine projects? For instance, there are 6 projects at PEA-stage, or more advanced, with an average cap-ex of C$540M:

Mintak: We have not published a PEA, so I cannot comment directly on cost comparisons other than pointing to the existing infrastructure at the project. The well-fields are in place and currently producing and circulating 125 million barrels of brine annually. The pipelines are in place, as is power and water. Road and rail is at the site. This is a bolt-on technology to existing chemical plants.

Epstein: How might your op-ex/tonne compare to that of lithium brine projects?

Mintak: Again, we have not yet published a PEA, but we are targeting the lowest quartile cost of production for lithium carbonate. We have confidence that this is achievable as the primary cost inputs are very attractive in south Arkansas, power and water are plentiful and inexpensive. Chemical reagents are produced in or shipped in close proximity to south Arkansas, the region is well connected to the Houston shipping channel. At the project level, we can leverage the buying power of a global chemical company when procuring materials and service agreements.

Epstein: Please describe who LANXESS is. In what ways (if any) is LANXESS already helping you?

Mintak: LANXESS is a global specialty chemical company based in Cologne, Germany. They operate 74 chemical plants around the world, 19,000 employees. 2017 revenue around $11 billion. They acquired Chemtura in 2017 for $2.57 billion which included the Arkansas bromine business.

Current land operations in southern Arkansas encompass more than 150,000 acres, 10,000 brine leases, and surface agreements and 250 miles of pipelines. Their three bromine extraction plants currently employ approximately 500 people and they process and reinject 125 million barrels of brine annually (over 5 billion gallons)

We have signed a binding MOU and a general term sheet for a planned JV with LANXESS for the phased development of the south Arkansas project with the goal of producing battery quality lithium materials on a mass scale from brine that is a by-product of existing bromine production facilities run by LANXESS and from 30,000 acres of undeveloped brine leases that Standard Lithium holds.

As part of the binding MOU, we will locate and operate our pilot plant at one of LANXESS’ chemical plants in south Arkansas. We will connect the plant into their brine pipeline system, post bromine extraction, and demonstrate (on a continuous basis) our selective lithium extraction process. We will also be locating our AI-powered lithium carbonate crystallization pilot plant at the site in south Arkansas.

The MOU we have struck with LANXESS allows us to leverage their massive infrastructure investment to de-risk our processing technology without having to spend 10’s of millions of dollars on resource development and the years of time that would entail. The planned JV with LANXESS includes a commitment from them for commercial project financing (subject to proof of concept and a positive PFS). That is a very important differentiator between Standard Lithium and our peers.

Epstein: In addition to LANXESS, you have been working with a number of other parties, please explain.

Mintak: As a development company, managing the runway and executing on our business plan requires strategic planning. We have taken the stance that we can accomplish more and in a more cost-effective manner, through strategic partnerships and agreements. In south Arkansas, we secured the only available large brine lease package with our agreement with NYSE listed Tetra Technologies.

For our pilot plant development, we are working with two global brands, Salt Works Technologies in Richmond B.C. and Zeton in Burlington Ontario. For analytics and research, we are working with two professors from the fine chemical/pharma departments at the University of British Columbia.

Epstein: What’s the status of your pilot plant, and what are the next steps?

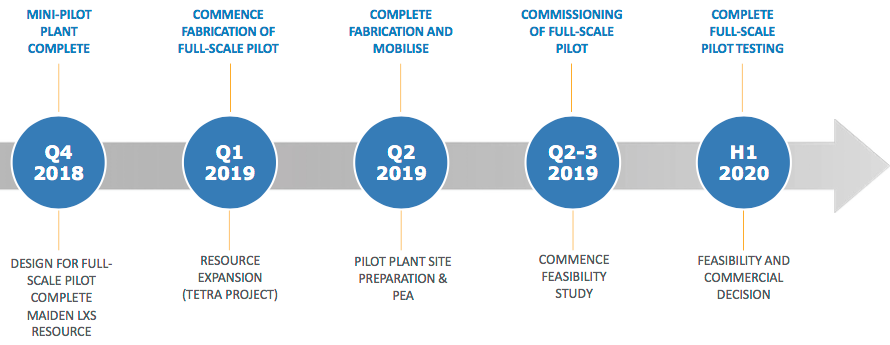

Mintak: Two pilot plants. We have two pilot plants in development. “LiSTR”, the selective extraction demonstration pilot plant is under construction in Burlington Ontario. Zeton is a global leader in pilot plant construction. The plant will be shipped from Zeton to south Arkansas in Q2 of this year and will be located at LANXESS’ Southern Bromine Extraction plant.

The site has virtually everything required to operate in place; steam, water, power, and the demo plant will connect to the existing brine feed and disposal pipeline system. We intend to run this plant in a continuous operating state, not in a batch process. We expect to run the plant through Q3/4 of 2019 and Q1 of 2020. The results of this work will feed into a Feasibility study targeted to be completed in Q2 2020.

The second pilot plant is our “SiFT” Lithium Carbonate Crystallisation Pilot Plant which is being built by Saltworks Technologies Inc., at their facility in Richmond, British Columbia, Canada. The crystallisation technologies used today in the industry were developed in the mid-twentieth century and are suited for producing technical grade compounds. As higher and higher purity compounds are needed by cathode makers the industry needs to evolve.

Mintak: The SiFT process has been developed by Prof. Jason Hein at the University of British Columbia and introduces advances and technologies from the pharma and fine chemical world to the lithium battery material world. It integrates Artificial Intelligence (AI) enabled high-speed, multi-image photo-microscopy and computer image recognition for crystal size and shape that acts like an auto-pilot, continually monitoring and optimizing the process. We have an operating prototype pilot plant that we are currently testing. The next step is to build a demonstration-scale plant that we will ship to Arkansas in the Q3 of 2019.

Epstein: Most conventional brine projects are planned for about 20,000-30,000 tonnes of Lithium Carbonate Equiv. (“LCE)/yr. Will your project be able to scale up to that range?

Mintak: Yes, that is an achievable production target based upon current commercial brine production volumes, with an expansion opportunity from our undeveloped brine leases.

Epstein: Please describe Standard Lithium’s near-term catalysts.

Mintak: The immediate near-term catalysts to watch for are a PEA in late Q1 or early Q2 and of course, our pilot plant(s) being moved to site and commissioned in the first half of this year. Investors can also expect further details on our strategic agreement with LANXESS.

Thank you Mr. Mintak for a detailed review of Standard Lithium (TSX-V: SLL) / (OTCQB: STLHF).

Peter Epstein – January 25, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Standard Lithium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Standard Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares in Standard Lithium and it was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic. [ER] may buy or sell shares in Standard Lithium and other advertising companies at any time.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

Ironbark Zinc Ltd. Ironbark Zinc Ltd. |

IBG.AX | +8,400.00% |

| Eden Energy Ltd |

EDE.AX | +100.00% |

Romios Gold Resources Inc. Romios Gold Resources Inc. |

RG.V | +50.00% |

| Euromax Resources Ltd. |

EOX.V | +50.00% |

| Reedy Lagoon Corp. Limited |

RLC.AX | +50.00% |

| Mount Burgess Mining NL |

MTB.AX | +50.00% |

| PJX Resources Inc. |

PJX.V | +45.45% |

| Midlands Minerals Corp. |

MEX.V | +42.86% |

| Playfair Mining Ltd. |

PLY.V | +33.33% |

| Terrain Minerals Limited |

TMX.AX | +33.33% |