There is a clear point of cyclical investment plays: buy when then market is down, sell when the market is up. The downside? No one really knows when the dawn is about to break, and for investors in Sierra Leone’s mining sector, it’s only getting darker out there.

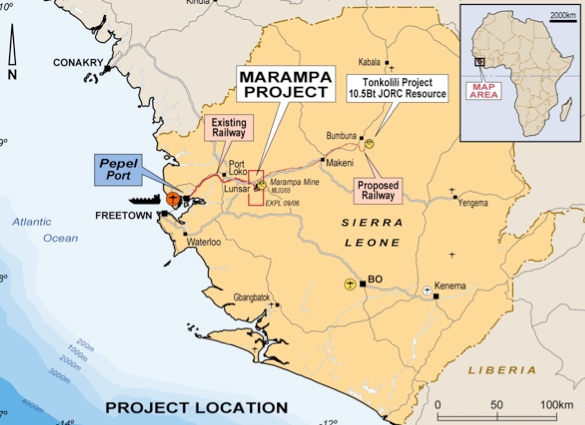

Recent weeks have brought news of mismanagement, assault, creative accounting and fleeing investors from the Marampa iron-ore project in Sierra Leone. There, Gerald Metals, a US-based commodities group, have struggled to reward investor confidence by failing to remove Marampa from care and maintenance despite the improvement in iron ore prices. Earlier in the year, Gerald’s key partners Shanghai Pengxin Investment Co Ltd. pulled out. Voting with their chequebooks, a number of Gerald’s lead creditors also jumped ship last week.

The problems for Marampa could only be getting worse. To market its product, Gerald Metals has sold investors on a promise of producing a higher grade of steel through a joint-venture with another local mine. In addition to relying on the rail network built to support the Tonkolili mine, Gerald Metals has trumpeted an agreement to blend the output from Marampa with that of Tonkolili to produce a higher quality, and higher value product. It was a very good idea.

The trouble: Tonkolili’s owners are now in almost as much trouble as Gerald.

In an email to investors at the tail end of 2017, Tonkolili’s operators, Shandong Iron & Steel Group Co, a Chinese outfit, explained that the company was going through a period of ‘financial hardship’ and would be suspending operations [1]. Shandong took ownership of Tonkolili in the wake of the collapse of its previous owner, African Minerals. The mine was placed in care and maintenance in 2014 as a result of Shandong, then owners of just 25% of Tonkolili, cutting the purse strings just as the mine required expansion. Shortly afterwards, Tonkolili’s owners went into administration and Shandong snapped up the remaining 75% at a fire-sale price [2].

But just like Gerald Metals’ at Marampa, Shandong have failed to deliver as majority owners of a previously minority share. Talk on the ground in Freetown suggests that not only is Shandong in financial difficulty, the company hasn’t actually been exporting anything out of Sierra Leone for almost four months. All the while, a half-laden ship is left anchored and rusting at Pepel Port at a demurrage cost in excess of $15,000 per day.

Of course, the issues we are seeing at Shandong and at Gerald Metals point to a much more worrying concern. What is going on with the due diligence procedures that the Government of Sierra Leone undertakes in the tendering process for mining licences? In an economy desperately in need of stable management of staple assets, the Government does not have the luxury of entrusting the state’s greatest resource pots to incompetent operators. Marampa and Tonkolili are two of the country’s biggest potential revenue earners: one is run by an accountant and his investors are leaving in droves; the other is quicker to cut and run than to stay and fight.

Oddly, spirits at these companies remain high. A punchy press release issued before Christmas by Brendan Lynch, CFO of Gerald Metals and formerly of collapsed Indian group Zamin Ferrous, thanked banks for their ongoing support of the Marampa project. But that faith, and indeed those thanks, may be short-lived.

Even with credit lines secured, if diminished, Gerald’s investors must now surely need to be reassured that the problems at Tonkolili will not affect assurances given over Marampa. It is hard to see how concrete pledges over any production targets, jobs or revenue projections can be given with the chief means of export and refinery in such dire straits. And there’s more to come. The full force of the Cape Lambert law suit is yet to be seen, and with Gerald Metals still needing to raise more than $50 million of investment to restart work at Marampa, the creditors will have reason to worry. One of those creditors, Dr. Adesola Adeduntan, the CEO of First Bank of Nigeria, recently met with President Bai Koroma [3]. If any assurances were given over the state of Government checks and balances on the private sector, examples like Marampa give plenty of reasons for that confidence to wear thin.

And as these questions begin to mount, and answers fail to convince, we cannot ignore the spectre of the authorities should their attention be drawn once again to Sierra Leone. It would be naïve to suggest that the Serious Fraud Office (SFO) and National Crime Agency (NCA) based out of the United Kingdom will not have any irregularities on their radar following the summer’s bribery drama at Sierra Rutile [4]. All foreign investors in Sierra Leone must toe a very careful line.

So as news this week tells us that Sierra Leone’s Ministry of Finance and Economic Development is planning to set up a task force to help the government ‘better manage revenue received’ from its mining sector, we may well ask where its priorities should fall. Given recent performance issues, I believe its first task should be looking at failing assets under foreign ownership. It is a scandal that is robbing the country of development, the people of jobs and the government of revenues that it badly, badly needs. Perhaps then there’ll be fewer smiles at Gerald Metals and Shandong when a little accountability comes knocking.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

|

SXL.V | +50.00% |

|

ADE.V | +50.00% |

|

RKR.V | +50.00% |

|

ERA.AX | +50.00% |

|

GTR.AX | +50.00% |

|

ILC.V | +33.33% |

|

CRD.V | +33.33% |

|

MTX.V | +33.33% |

|

CASA.V | +30.00% |

Golden Minerals Company Golden Minerals Company |

AUMN | +29.50% |