It was a rough week for investors in stocks and stocks of all kinds. The S&P 500 lost 5%. Emerging Markets also lost 5%. Gold Stocks, which had weakened before the broader equity market have been hit hard. They (GDX, GDXJ) also lost 5% last week. The HUI Gold Bugs Index (which excludes royalty companies unlike GDX) lost 7%. After a strong start to the year, gold stocks have essentially given back all their gains. Nevertheless, we remain extremely optimistic on gold stocks over the next 12-18 months as trends in the economy and stock market should begin to support Gold after the second quarter.

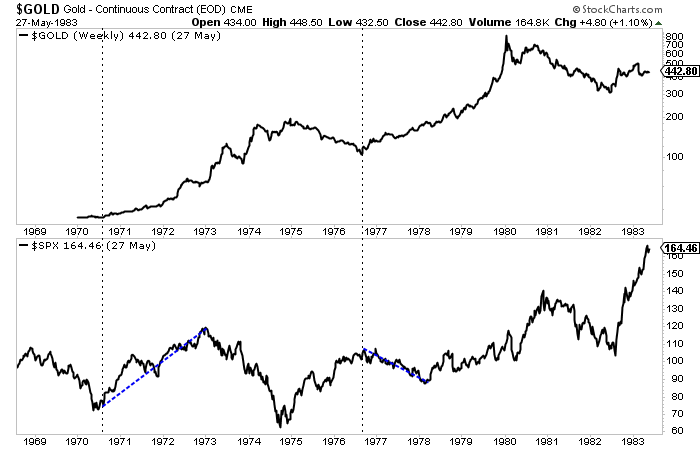

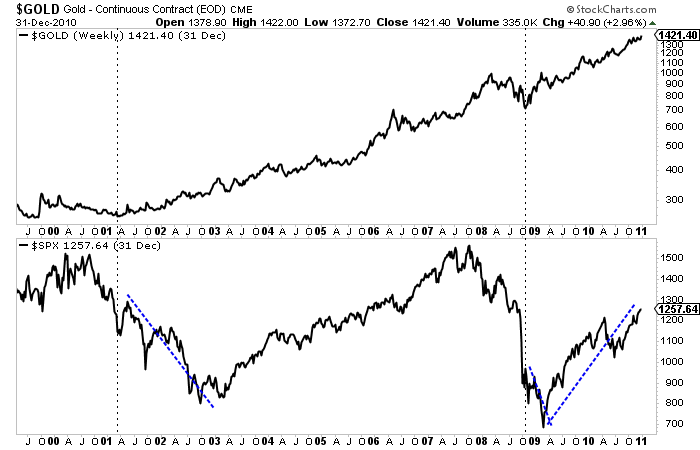

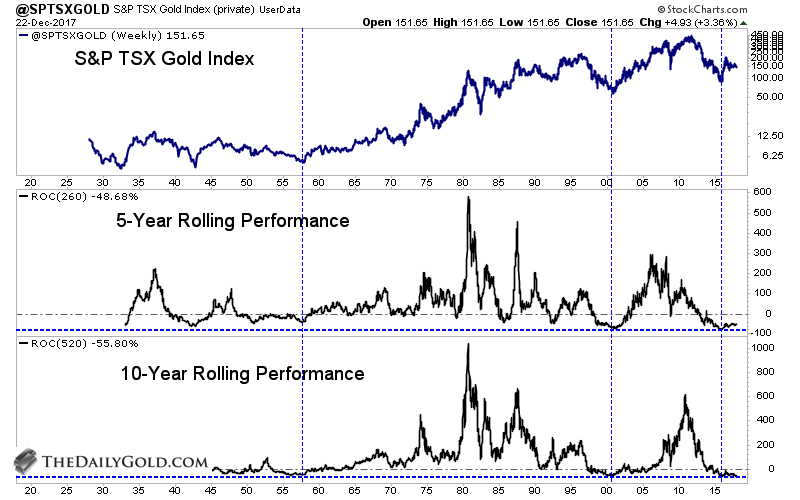

Historically speaking some of the best performance in Gold and gold stocks occurred during or after a bear market in stocks. The best examples can be found in the 1970s and 2000s as the charts show. Gold surged after the bottom in stocks in 1970 and continued to perform very well during the 1973-1974 bear market. After a brief but sharp bear in 1975-1976 Gold rebounded strongly as the S&P 500 began a mild bear market in 1977. Years later Gold emerged from a significant bottom in 2001 while the stock market endured its worst bear market in a quarter century. Gold continued to perform even after the market bottom in late 2002. Gold emerged from the global financial crisis before the stock market but continued to make new highs after the stock market bottomed in March 2009.

This performance is not just random. It makes quite a bit of fundamental sense. As we know, Gold is driven by falling or negative real rates. Typically policy makers in response to a recession or bear market will pursue policies that lead to falling or negative real rates. These policies are not reversed until the economy gains strength. Gold can also benefit from inflationary recessions, which we saw in the 1970s. Perhaps we are headed for that outcome at somepoint but I digress.

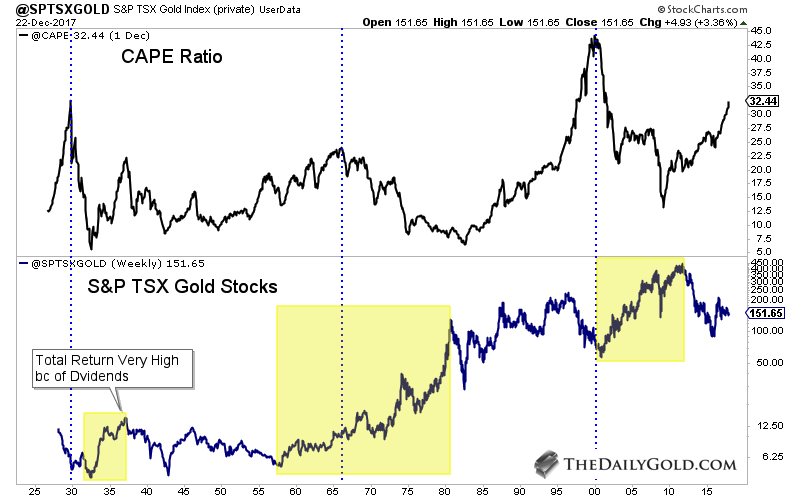

The best comparison to today may be the mid 1960s. Although the Gold price was fixed until 1971, we can use gold stocks to study the macro picture of the 1960s and how it may relate to today.

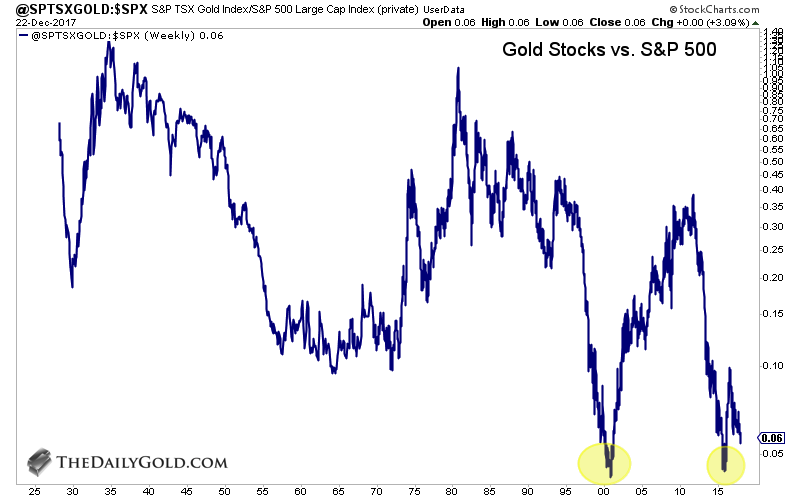

Gold stocks and the stock market were positively correlated during the 1960s but gold stocks dramatically outperformed and especially from 1964 to 1968. That outperformance accelerated after 1963 as inflation and bond yields began to rise to higher and higher levels in the years ahead. That would soon negatively impact the stock market in both nominal and real terms. The Dow peaked in 1966 while the S&P 500 did not peak until 1973 (as it made marginal new highs in 1969 and 1973). In real terms stocks would peak in 1966 or 1968 (depending on which index you use).

Economic fundamentals appear to be headed in a direction that is bullish for Gold and gold stocks and less positive for the stock market. While inflation has yet to be unleashed, the markets are showing that inflationary pressures are forming. This will impact corporate margins (which are extremely high) as well as profits. Higher inflation also leads to higher bond yields which means higher costs to service debt. That is a problem for the economy and equity market due to the debts that have piled up in recent years.

So the question now is where is the threshold for when inflation and bond yields start affecting the economy and stock market in a way that is favorable for precious metals?

With respect to the 1960s and 1970s, the answer would be 1964.

When precious metals begin and sustain outperformance against the stock market it will signal that the threshold or inflection point has been reached. That outperformance will also go a long way in helping Gold make its major breakout.

It is not yet time for Gold and gold stocks to shine but it is getting very close. Gold remains in a bullish consolidation pattern that should give way to a breakout later in the year. Meanwhile, gold stocks and Silver are lagging badly but that does not have us concerned. The next few months could prove to be the best buying opportunity in precious metals since the end of 2015. Quality juniors that are bought on weakness over the medium term should deliver fantastic returns over the ensuing 12 to 18 months. To follow our guidance and learn our favorite juniors for 2018, consider learning more about our premium service.

The unnaturally-tranquil stock markets suddenly plunged over this past week. Volatility skyrocketed out of the blue and shattered years of artificial calm conjured by extreme central-bank distortions. This was a huge shock to the legions of hyper-complacent traders, who are realizing stocks don’t rally forever. With stock selling unleashed again, herd psychology will start shifting back to bearish which will fuel lots more selling.

As a contrarian student of the markets, I watched stocks’ recent mania-blowoff surge in stunned disbelief. On fundamental, technical, and sentimental fronts, the stock markets were as or more extreme than their last major bull-market toppings in March 2000 and October 2007! I outlined all this in an essay on these hyper-risky stock markets on 2017’s final trading day. The ominous writing was on the wall for all willing to see.

January’s extreme surge in the US stock markets made this selloff case even more likely. Mid-month in another essay I warned, “The stock markets are now dangerously overbought, implying a major selloff is probable and imminent. … Such extremes are very unusual and never sustainable for long, signaling major selloffs looming.” So the fact these crazy stock markets finally rolled over wasn’t a surprise at all.

But I was awestruck at the sheer violence of what happened last Friday and the subsequent Monday, it was very odd. Even though the countless market extremes argued strongly for a major selloff, they tend to be much more gradual initially off bull-market peaks. So it was fascinating to watch all this unfold in real-time with my data feeds and CNBC. Students of the markets live for anomalous exceedingly-rare events!

The igniting catalysts were multilayered. The US flagship S&P 500 broad-market stock index (SPX) had blasted to a dazzling new all-time record high on Friday January 26th. It was stretched a mind-boggling 14.0% over its key 200-day moving average, which itself was high and steeply rising! The 8.9-year-old stock bull that had powered 324.6% higher felt unstoppable. Traders were universally convinced it would continue.

But just a couple trading days later on Tuesday January 30th, significant selling emerged. That morning Amazon, Berkshire Hathaway, and JP Morgan declared they were going to form a healthcare company. That unanticipated news way out of left field crushed the major healthcare stocks, hammering the SPX 1.1% lower. That was actually a significant down day by recent standards, the worst seen since mid-August.

With euphoric bullish psychology dented, Jobs Friday arrived a few trading days later on February 2nd. That official monthly US jobs report saw a modest headline beat, but the big news came on the wages front. Average hourly earnings beat expectations by climbing 2.9% year-over-year, the hottest read on wage inflation since June 2009. That triggered inflation fears with the 10-year Treasury yield already at 2.78%.

Higher prevailing interest rates are a huge problem for bubble-valued stock markets. The SPX had just left January with its 500 elite component stocks sporting a simple-average trailing-twelve-month price-to-earnings ratio way up at 31.8x! Historical fair value is 14x, twice that at 28x is formal bubble territory. In a higher-rate environment, extreme valuations are far harder to tolerate. So the stock markets sold off.

A week ago Friday the SPX slid all day long to close at a major 2.1% loss. That proved its biggest down day since way back in September 2016, before Trump won the election and the resulting extreme stock rally first on Trumphoria and later on taxphoria. Something was changing, the unnaturally-low volatility regime was crumbling. That left speculators and investors alike very nervous heading into last weekend.

It had been an all-time-record 405 trading days since the SPX’s last 5% pullback, unbelievably extreme. So that selloff really struck a nerve, I started to hear from casual acquaintances I hadn’t spoken to for years. At a friend’s Super Bowl party Sunday night, once the guests I didn’t know found out what I do for a living I felt like a celebrity. We spent the first quarter talking about the markets, people were really concerned.

Monday the 5th was extraordinary, a record day in some respects. SPX futures were down less than 1% in pre-market trading, nothing wild. But once the US stock markets opened, the selling started gradually snowballing. It greatly intensified around 3pm, with the SPX plunging from -2.3% to -4.5% on the day in literally 11 minutes! There was no news at all, it simply looked and felt like cascading stop-loss selling.

All prudent traders put trailing stop-loss orders on their stock positions. They are an essential measure to manage risk. Once a stock falls a preset percentage from its best level achieved during a trade, that position is automatically sold. In big stock-market selloffs, as stop losses are sequentially hit they feed into the ongoing selling. The more stocks fall, the more stops triggered, the more sell orders fuel the maelstrom.

The SPX bounced a bit, but still plunged a whopping 4.1% on close Monday! That was a serious down day by any standard, actually the worst since way back in mid-August 2011 which followed Standard & Poor’s downgrading US sovereign debt. Everyone takes notice when stock markets suffer their biggest daily drop in 6.5 years. That really changes collective psychology, shattering the euphoria rampant in January.

But amazingly that SPX plunge wasn’t the most-interesting thing Monday. The implied volatility on SPX options is tracked in the famous VIX fear gauge. It skyrocketed a stupendous 125.8% higher that day, its largest daily spike ever witnessed! That wreaked colossal havoc in the short-volatility market. Since Trump’s election win, more traders and capital have flocked to bet on the idea that volatility will keep falling.

Students of market history knew that was an absurd bet before Monday’s spike. Stock-market volatility has always been cyclical, just like stock prices. Exceptionally-low or -high volatility levels always mean revert back to normal. So betting that the record-low stock volatility in recent months would keep going even lower was a foolish, suicidal bet even before Monday. That epic VIX spike totally gutted these guys.

There are, or were, extraordinarily-risky inverse-VIX exchange-traded notes. These were designed to rally when volatility fell, some even with leverage which traders liked to further amplify with their own margin. One of the leading inverse-VIX ETNs was XIV, which is VIX spelled backwards. It had closed at $129.35 per share on Thursday February 1st, but by this Tuesday it had imploded 94.3% in a termination event!

All these inverse-VIX ETNs were shorting VIX futures, so they had to become massive buyers on that sharp SPX selloff to close out those devastated positions. On Monday the banks sponsoring these crazy ETNs had to buy an extreme record 282k VIX futures contracts! That catapulted the VIX itself to 50.3 on Tuesday morning, about as high as it ever gets outside of actual crashes and panics. What a wild ride!

That begs the question what happens next? This stock-market-selling and volatility shock happened at a time when stock markets were already very precarious. Such an extreme event has to start altering herd psychology. This first chart looks at the SPX superimposed over the VIX during the last few years, both on a closing basis. Once serious selling starts out of toppy stock markets, it usually portends much more coming.

This week’s stock selling unleashed emerged in some of the most-toppy stock markets ever witnessed. Again the average SPX-component TTM P/E leading into it was a bubble-valued 31.8x! Again the SPX had stretched 14.0% above its 200-day moving average, some of the most-overbought conditions seen in all of SPX history. The SPX had rocketed vertically for most of January in popular-mania-grade euphoria.

The future impact of stock selling being unleashed really depends on the market conditions that birthed that selling spike. If stock prices were near multi-year lows leading into selling spikes, with valuations lower than their historical average of 14x earnings, these events can mark selling climaxes before major reversals higher. But unfortunately the exact opposite was true leading into our current sharp SPX plunge.

Coming out of what looked and felt like a mania blowoff top, this past week’s serious selling is surely an ominous omen. Stock markets can’t rally forever, yet that’s exactly what they seemed to be doing since Trump’s surprise election victory. Between Election Day and late January’s latest record high, the SPX had soared 34.3% higher in just 1.2 years! And that span was incredibly extreme with record-low volatility.

Again as of last Friday it had been an all-time-record 405 trading days without a single 5% peak-to-trough SPX pullback. That’s 1.6 years! Nothing like that had ever happened before. Technically a pullback is a 4%-to-10% selloff in the stock markets on a closing basis. The last pullbacks were minor, a 4.8% one in late 2016 following a 5.6% one in mid-2016. Those were the last material selloffs in the SPX before this week.

Periodic selloffs to rebalance sentiment are essential to keeping stock bulls healthy. The longer markets go without significant selloffs, the more greed and complacency multiply. Traders forget that stocks fall too, and their hubris leads them to take all kinds of excessive risks. Like betting that record-low volatility will persist indefinitely. The leveraged speculation eventually gets so extreme that it threatens the entire bull.

My favorite analogy on this is forest fires. Officials love to suppress natural wildfires to protect structures. But the longer firefighters put out every little wildfire, the denser forest underbrush gets. This fuel source grows out of control, eventually leading to a conflagration far too extreme to put out. Rather than having a bunch of smaller wildfires to keep fuel in check, suppression eventually guarantees a super-destructive hell fire.

Periodic pullbacks and corrections in stock markets allow the underbrush of greed to be burned away before it gets thick enough to become a systemic risk. Traders naively believe levitating stock markets are less risky, but the opposite is true. The longer a span without a serious selloff, the higher the odds one is coming soon. Normal healthy bull markets actually suffer 10%+ corrections once a year or so to keep balance.

It’s been 2.0 years since the last actual SPX correction, which bottomed in early 2016. The lack of both smaller pullbacks and larger corrections let complacency grow unchecked into greed, euphoria, and even hubris recently. And these emotional extremes have to be mostly burned away for this bull to have any hope of eventually heading higher. The only thing that can eradicate widespread greed is major stock selloffs.

After Monday’s serious 4.1% plunge, the SPX was still only down 7.8% since its peak just 6 trading days earlier. While that is unusual speed to see such a decline, it still only ranks towards the high end of mere pullback territory. We hadn’t even hit a correction yet at 10%, and they can stretch as high as 20%. The SPX’s last corrections ran 12.4% over 3.2 months in mid-2015 and 13.3% over 3.3 months into early 2016.

Given the extreme overvalued and overbought conditions leading into this past week’s plunge, there’s no way even that was enough to rebalance away the euphoric sentiment. So it’s all but certain the SPX will grind lower in the coming months, heading down well over 10% into deep correction territory. At 10% the SPX would merely be back to early-November levels, merely erasing the recent mania-blowoff surge.

If this correction approaches 20% as it really ought to, that would drag the SPX all the way back down to 2298. Those levels were first seen just over a year ago in late January 2017. That would reverse the lion’s share of the entire past year’s taxphoria rally, wreaking tremendous sentiment damage. But don’t forget corrections tend to take a few months, not a few days. So the selling is way more gradual than Monday’s.

That extreme 50 VIX spike Tuesday morning must be considered. Again that’s about as high as the VIX ever gets in normal corrections, implying the immediate selling pressure should have abated. The only times higher VIX levels are briefly seen is after crashes and panics. A crash is a 20%+ drop in just two trading days from very-high stock-market levels. This past week’s Friday-Monday selloff wasn’t even close.

Crashes are exceedingly rare in history, and next to impossible today given the widespread use of stock-market circuit breakers. They effectively close markets for a time after intraday selling milestones are hit. Today the SPX has levels triggered at 7%, 13%, and 20% intraday declines. The trading halts depend on when these declines occur within a trading day, before or after 3:25pm. They would slow crash-grade plummets.

Panics are steep 20%+ selloffs within two weeks, extreme but much slower than crashes. They tend to cascade from lows out of late-stage bear markets to climax them. They are very rare too, with 2008’s being the first formal one since 1907. The VIX can temporarily soar above 50 in crashes and panics, but those extremes never last for long. In normal market conditions, a 50 VIX spike should mark an absolute bottom.

But the problem this week is Tuesday’s extreme VIX spike was the result of panic buying of VIX futures to liquidate those inverse-VIX ETNs. That has never happened before. Without that dynamic, the VIX likely wouldn’t have gone much above 30. That too implies this stock-market selloff still has plenty of room to run. So the stock selling unleashed is likely to persist over a few months at least, despite the VIX spike.

Given the extremes in these stock markets in late January, I still suspect the odds heavily favor a new bear market over 20% instead of a bull-market correction. I presented this compelling SPX-bear case in late December, and don’t have room to rehash it here. Normal bear markets tend to cut stocks in half over a couple years or so, 50% SPX losses. That works out to a gradual average selling pace of 0.1% per day.

The last couple SPX bears give an idea of what to expect in the inevitable next bear after such an epic stock bull. The SPX fell 49.1% over 2.6 years ending in October 2002, and 56.8% over 1.4 years that climaxed in March 2009. A 50% SPX loss, which is conservative since bears tend to be proportional to their preceding bulls’ sizes, would drag this index back to 1436. That’s September-2012 levels, a long way down!

No one knows whether this stock selling unleashed will culminate in a bull-market correction under 20% or a new bear market over 20%. But either way, speculators and investors ought to swiftly boost their anemic portfolio allocations to gold. The record-high stock markets in recent years have led to radical gold underinvestment. Gold tends to rally on balance when stocks fall, it’s the ultimate portfolio diversifier.

As this final chart shows, after the last SPX correction ending in early 2016 gold surged into a major new bull market. Hyper-complacent stock traders suddenly realized that they needed to own gold to diversify their stock-heavy portfolios. That gold bull has persisted, powering higher in a strong uptrend ever since despite this past year’s extreme taxphoria stock-market rally. A new SPX correction will work wonders for gold.

That last SPX correction into early 2016 wasn’t large at just 13.3%. Yet that was still enough to motivate complacent investors to flock back to gold. Their heavy buying catapulted gold 29.9% higher in just 6.7 months! Gold turned on a dime from deep 6.1-year secular lows because a major stock-market selloff finally convinced investors to up their meager gold allocations. Every investor should have 5% to 10%+ in gold.

Just a week ago that ratio was likely only running around 0.14% based on the values of that leading GLD gold ETF and the collective market capitalizations of the 500 SPX companies! So with gold allocations essentially zero late in an extreme stock bull, there’s vast room for massive capital inflows into gold in the coming years as investors rebalance their portfolios. Gold thrives for a long time after major stock selloffs.

The gold buying isn’t instant when the SPX falls though, as traders need time to process the drop and its likely implications. Back in early 2016 stock investors really didn’t start aggressively buying GLD shares until the SPX suffered multiple big down days. The SPX fell 1.5%, 1.3%, 2.4%, and 1.1% on separate trading days in a single week before gold buying resumed. More big SPX losses soon accelerated these inflows.

If you don’t have a significant gold allocation in your portfolio, you ought to get buying. It can be done with physical gold bullion or GLD shares. If you want to leverage gold’s bull market that will accelerate following a major stock selloff, consider the stocks of great gold miners. They tend to amplify gold upside by 2x to 3x due to their fantastic profits leverage to gold. The precious-metals sector thrives after stock selloffs!

Finally the stock selling unleashed is likely just beginning due to what the major central banks are doing this year. The Fed’s unprecedented quantitative-tightening campaign to start reversing its trillions of dollars of QE liquidity injected that levitated stocks for years is accelerating throughout 2018. At the same time the European Central Bank slashed its own QE campaign in half until September, when it may cease entirely.

Between the Fed’s QT and ECB’s QE tapering, global stock markets face central-bank tightening running $950b in 2018 and another $1450b in 2019 compared to 2017 levels! This will certainly strangle this QE-inflated monster stock bull. So on top of everything else this week’s sharp selloff portends, the euphoric stock markets were already in serious trouble from record extreme central-bank tightening. Got gold yet?

Absolutely essential in falling markets is cultivating excellent contrarian intelligence sources. That’s our specialty at Zeal. After decades studying the markets and trading, we really walk the contrarian walk. We buy low when few others will, so we can later sell high when few others can. While Wall Street will deny the coming stock-market bear all the way down, we will help you both understand it and prosper during it.

We’ve long published acclaimed weekly and monthly newsletters for speculators and investors. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of the end of Q4, all 983 stock trades recommended in real-time to our newsletter subscribers since 2001 averaged stellar annualized realized gains of +20.2%! For only $12 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today!

The bottom line is the stock selling unleashed this week isn’t over. Given the fundamental, technical, and sentimental extremes around January’s record highs, a sub-10% pullback isn’t enough to eradicate the euphoria. At best a major correction approaching 20% is necessary, and those tend to run a few months or so. This week’s extreme VIX spike to levels that usually mark major bottoms was artificial, not normal.

And after such an extreme bull market largely driven by record central-bank easing, the odds really favor this selloff eventually growing into a 20%+ new bear. Especially with the major central banks starting to aggressively pull their liquidity in 2018. Whether a major bull correction or major new bear market, gold tends to thrive after major stock-market weakness. That leads investors to buy gold to re-diversify their portfolios.

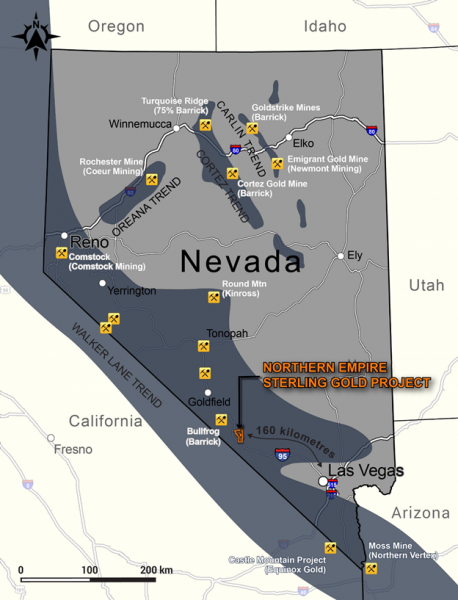

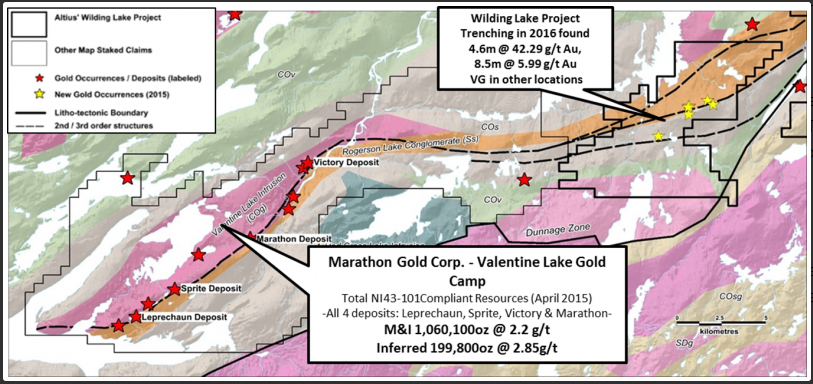

While most gold investors are familiar with the Carlin Trend – the largest gold-producing region in the United States – there are other, less explored parts of Nevada starting to attract a lot of attention. Specifically, the Walker Lane Gold Belt where company-making discoveries are being drilled.

Located in southern Nevada, Walker Lane has some of the most important mining districts in North America including Comstock, Tonopah, Goldfield, Bullfrog and Aurora. Estimated to host over 50 million gold ounces, the region is being actively explored by Kinross and Barrick at the producing Round Mountain Mine, Gryphon Gold at the Borealis Mine, and Newcrest Mining at the Redlich project.

Unlike the Carlin Trend, where most gold projects are mining ore less than a gram per tonne, Walker Lane is starting to stand out on its own merits with exceptional high-grade assays.

High-grade gold mine open for expansion

Northern Empire Resources (TSXV: NM; USOTC: PSPGF) is a well-financed gold exploration and development company focused on an emerging gold district in the Walker Lane Trend. The Sterling Gold Project hosts four distinct deposits, including a fully permitted, open-pit mine. The Sterling Mine is one of the highest-grade heap leach mines in the western United States.

Situated 185 kilometres (two-hour drive) northwest of Las Vegas, on the eastern flank of the Bare Mountains, Sterling features five past-producing open pit and two underground gold mines. Drilling, surface mapping and sampling on the project suggests that the historic deposits are open for expansion and there is potential for new discoveries. The property still has infrastructure in place from 2015 when the Sterling Mine was last in production.

A history of success: $3B in takeout value

Along with having an outstanding property with exploration upside, Northern Empire also features a management team with an exceptional record of creating value for shareholders. Led by Executive Chairman Douglas Hurst and Michael Allen, President and CEO, the Northern Empire board has created over $3 billion in takeout value, including Newmarket Gold, acquired for $1 billion by Kirkland Lake, Kaminak Gold, acquired by Goldcorp for $520 million, International Royalty Corp, bought by Royal Gold for $700 million, Rainy River Resources, bought by Newgold for $310M, and Underworld Resources, purchased by Kinross Gold for $138 million.

Currently sitting at a $80-million market capitalization, Northern Empire has a cash balance of $18 million, having recently completed a $15 million bought deal financing that included no warrants. In fact, the company raised $35 million in 2017 with no warrants.

The gold junior is coming off a successful 2017 drill campaign and will aggressively drill known mineralized zones in 2018 to expand resources and explore for new deposits on its 125-kilometre land package.

709,000 ounces inferred, plus newly staked ground

The story of Northern Empire began in May 2017 when it acquired the Sterling Gold Project in Nye Country from Imperial Metals for $10M. The $20 million acquisition financing included an investment by global precious metals producer Coeur Mining, which earned an 11.6% stake in the company.

Northern Empire is backstopped by the low risk, permitted heap leach Sterling Mine; majors have an appetite for high margin, high grade assets. The main event, however is the blue-sky potential north of Sterling, where more ounces are ripe for exploration. In particular the focus is on the SNA deposit, which has Carlin-type mineralization adjacent to the Mother Lode deposit owned by Corvus Gold.

Between 1980 and 2000, nearly 200,000 ounces were pulled from Sterling’s three open pits and two underground mines. The run of mine ore was placed on heap leach pads, where gold recoveries averaged 88%.

Total inferred resources at the project are 709,000 ounces with an average grade of 2.23 grams per tonne gold – which is high for a deposit in Nevada where most deposits are lower-grade.

Northern Empire has all the permits required to operate the Sterling Mine. In May 2016 the mine was permitted to restart operations, with the Bureau of Land Management finding that the mine would not have significant environmental impacts.

Over the last six months the company has been aggressively expanding the property, having staked an additional 489 claims in June, thereby increasing its original land position by 50%. Another 261 claims were staked in October, which further solidified Northern Empire as the dominant landholder in the Bare Mountains, a district which includes the past-producing Sterling, 144, Daisy, Secret Pass, Gold Ace, Mother Lode deposits, and Bullfrog Mine.

Four jewels in The Crown

Exploration is focused on the Crown Block of deposits just 7 kilometres north of the Sterling Mine. For the first time the Crown Block has been consolidated in a contiguous land package under one ownership. The Crown Block hosts four primary targets: Daisy deposit, Secret Pass deposit, SNA deposit and the Shear Zone target. The mineralization follows the same East-West detachment fault structure that hosted Barrick’s Bullfrog Mine, which produced 2.3 million ounces of gold at an average grade of 3.2 grams per tonne (“g/t”).

Glamis and Rayrock previously operated the Daisy Mine, which included Daisy, Secret Pass, and Mother Lode pits, and produced 104,000 ounces of gold between 1997 and 2001. When gold dipped below $300, the mine was closed down.

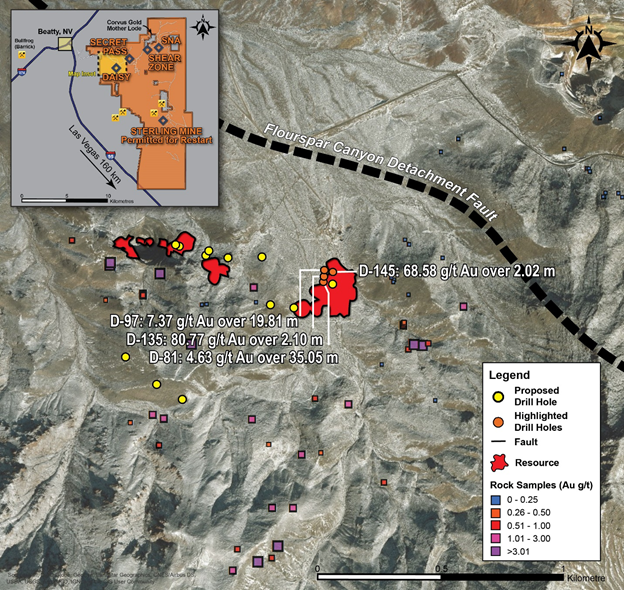

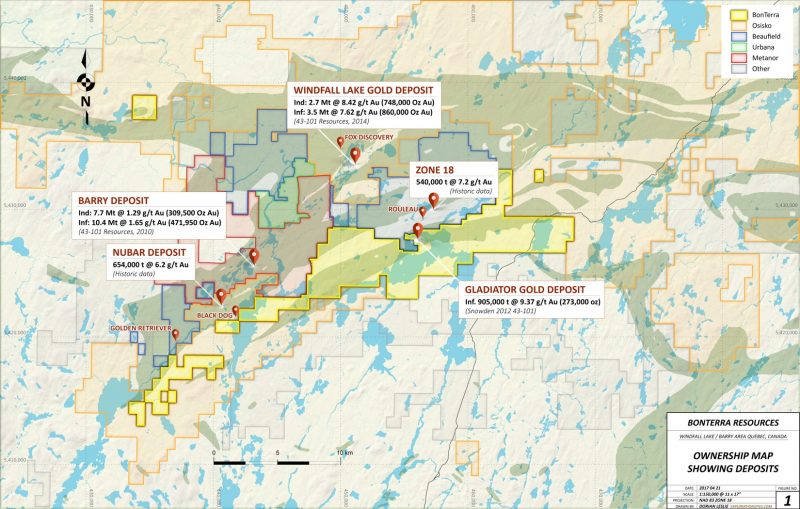

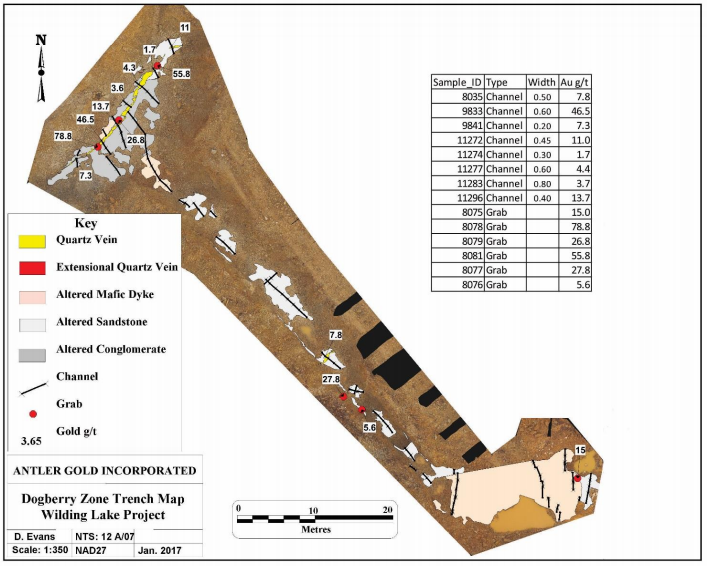

(image 2) Daisy Deposit map of drill holes

A total of 160 holes were drilled at Secret Pass which was previously mined in the 1990’s. Significant drill intercepts beyond the existing pit indicate potential resource expansion. Drill hole D-320 on the eastern edge of the historical pit intercepted 1.02 g/t gold over 77.7 metres.

SNA lies on a north-south structure that hosts Carlin-type mineralization which is open for expansion. Historically 149 holes were drilled at SNA. The Shear Zone is on the upper level of an epithermal vein and indicates potential for bonanza grades at depth. Past discoveries of mineralization were not followed up on.

2017 drilling confirms resource model, opens up new opportunities

In August 2017 Northern Empire initiated the first phase of an exploration program designed to confirm and expand the inferred resources at the Sterling Gold Project. Historic drill holes from the Daisy deposit include 68.58 g/t Au over 2.02 m, 7.37 g/t Au over 19.81 m, 80.77 g/t Au over 2.10 m, and 4.63 g/t Au over 35.05 m.

Of the planned 5,200 metres of drilling, over half was focused on the Sterling Mine, where Northern Empire outlined a pit-constrained inferred resource of 231,000 gold ounces grading 3.67 g/t. The work provided confidence in the resource, tested for extensions along strike and provided metallurgical samples prior to Northern Empire beginning economic studies.

The 52-hole drill program, 25 of which were reverse circulation holes and 27 that were diamond-drilled, started with the Daisy and Secret Pass deposits within the Crown Gold Project. The company also performed an evaluation of the entire project and flew a geophysical survey to identify new targets.

The Daisy deposit hosts an inferred mineral resource of 174,000 gold ounces at an average grade of 2.12 g/t gold, while the Secret Pass inferred resource is 188,000 ounces of gold at an average grade of 1.65 g/t.

The drills then moved to the Sterling Mine to complete infill, resource expansion, and exploration drilling.

“This round of drill results supports our resource model of the Sterling deposit, as well as the location of the underground workings. Sterling was known to be a narrow, high grade deposit with excellent metallurgy. Of note, are the occasional broader zones of mineralization, such as 12.19 metres of 8.37 g/t gold, as well as previously unacknowledged lower grade mineralization being identified by Northern Empire’s drilling; both of which may represent real opportunities within the Sterling deposit. Also, our early exploration of the area to the west and south of the Sterling deposit has yielded interesting results.”

Assay results from another seven holes reported in early December highlighted shallow, high-grade oxide gold at the Sterling Mine, with several holes hitting significant mineralization at the edges of the resource model, indicating the deposit remains open for expansion. Notable drill intercepts included 10.0 metres of 14.59 grams per tonne, 9.05 metres of 8.66 g/t, and 7.59 metres of 8.25 g/t.

2018 drilling year-round: in progress

As the calendar turns to a new year, Northern Empire is making plans for a 15,000-metre drill program it announced mid-December; the drills have already begun turning. In this new phase, drilling will be focused on infill and expansion of the Sterling Mine, Daisy, Secret Pass and SNA deposits, as well as testing high-priority exploration targets. Drilling will be completed with both core (diamond drilling) and reverse circulation rigs.

This area of Southern Nevada is accessible 12 months a year and Northern Empire will be aggressively working all year round. In early 2018 the company will turn its attention to the Crown Block, where drilling will begin on the SNA deposit where Northern Empire has identified the potential for a large Carlin-type deposit. This work will be targeting north-south structures exiting the Mother Lode pit, adjacent to the north and owned by Corvus Gold, and where historic drill holes such as ML088, drilled on the company’s property, returned 10.67 metres grading 4.13 g/t starting at 60.96 metres, and 28.96 metres grading 1.76 g/t starting at 100.58 metres.

Indeed an exciting aspect of this round of drilling is the close proximity of Corvus Gold’s drills on that company’s Mother Lode project, just metres away from Northern Empire’s holdings. Mother Lode produced 34,000 ounces at an average grade of 1.8 g/t in the late 1980s but closed due to low gold prices. In December Corvus announced it has expanded the sediment-hosted Mother Lode gold system to at least 450 metres along strike.

Corvus Gold’s exploration program at Mother Lode has received a major response from the market, with the stock more than doubling over the past year (+126%); most of the gain has been in the last three months and can likely be attributed to its success at the Mother Lode.

Since Northern Empire is the dominant land holder, and owns all the land surrounding Mother Lode, any extension of Mother Lode beyond Corvus Gold’s tight boundaries is likely to add ounces to Northern Empire’s Sterling Gold Project.

Drilling will also be completed at the Daisy and Secret Pass deposits with the goals of upgrading and expanding the resources, collecting metallurgical samples, and testing exploration concepts. On September 18 and October 4, 2017, the company announced drill results for Daisy and Secret Pass, highlighted by 47.24 metres of 1.47 g/t gold at Daisy and 82.30 metres grading 1.25 g/t at Secret Pass.

Conclusion

Northern Empire has an impressive assemblage of both past-producing gold mines and enticing exploration targets at its Sterling Gold Project in one of Nevada’s most promising gold mining regions: The Walker Lane Trend.

With the gold price powering above $1,330 per ounce, mineral-rich gold companies are rising in valuation once again, so what better time to get in on an exciting gold play that appears to offer investors ample upside? Northern Empire has the property, the treasury and the team to make it happen.

About the Author:

With over a decade of journalistic experience working in newspapers, trade publications and as a mining reporter, Andrew Topf is a seasoned business writer. He holds degrees in journalism and political science, and earned a Masters from the London School of Economics.

Technically and fundamentally, gold is poised to resume its magnificent rally that is taking investors into what I call a “bull era”.

The next FOMC meeting announcement is tomorrow. I expect the Fed to strongly signal more rate hikes and ramped up quantitative easing.There’s an outside chance that bank deregulation is addressed, but that’s likely going to happen in the next meeting.

Regardless, everything the Fed is doing is positive for inflation, negative for government bonds, and negative for the dollar.

Please click here now. Nothing is more terrifying to institutional bond market analysts than the prospect of significant inflation.

The US government is on the ropes. Rates are rising, QT is creating bond market liquidation, and wages are starting to surge. The inability of the US government to finance itself in an inflationary environment means rate hikes and QT are negative for both the bond market and the dollar.

Please click here now. Double-click to enlarge this key short term gold chart.

Even though gold has rallied more than $100 an ounce in a very short time frame, the pullback action is very positive. It’s taking the shape of a small positive wedge formation. Solid Chinese New Year demand is likely behind the positive nature of this soft pullback. Global gold investors should be buyers at $1328, $1310, and $1300, with a bigger focus on gold stocks than bullion.

During deflationary times, bullion is the leader.During the inflationary times that are beginning now, mining stocks are poised to dramatically outperform bullion.

Global growth with inflation and the end for the great global bond market should create at least a decade of gold stock outperformance against gold. These stocks are essentially poised to enter a period of growth much like Main Street America experienced in the 1950s.

While all the current news is very positive for gold market investors, the best news of all may be coming on Thursday. Please click here now. On Thursday, India’s national budget is announced and a duty cut may finally happen!

Gold’s uptrend against US government fiat ended in 2011 – 2012 as India began increasing the import duty aggressively. This essentially put millions of jewellery workers on the bread line and shuttered hundreds of thousands of small jewellery shops.

The bottom line is that Indian government duty hikes basically nuked Western gold mining stock enthusiasts and put the survivors in a horrifying gulag.

For the past several years, jewellers have begged the government to begin reducing the duty. Unfortunately, the government has shown no interest in announcing even a tiny cut.

Until now. While the commerce department has called for a duty cut for years, this is first time the all-powerful finance department has addressed the issue in a positive way. So, a cut on Thursday is not a “done deal”, but the odds of it happening are now vastly higher than at any time since the import duty peaked at 10% in 2013.

Jewellers and dealers are not buying gold in any size now, because they are anticipating the government will finally give them a cut. That’s created some gold price softness over the past week. I’ve suggested that a duty cut could be the catalyst that blasts gold over the $1370 area highs. In turn, that would usher in the start of a rally to massive resistance at $1500.

For gold, a duty cut in India has truly gargantuan ramifications. It is the equivalent of a corporate tax cut in America. It restores confidence amongst citizens and shows that the government understands not just sticks, but carrots. When citizens feel good they are more productive. GDP grows, bringing the government more tax revenues. Thursday could be a truly epic win-win day for gold and all its global stakeholders. Are investors prepared?

Please click here now.Institutional money managers are starting to see the myriad of inflationary lights flashing that I predicted were coming.

Money velocity is starting to rise. The upturn is subtle, but it’s there! As Powell takes over the Fed and ramps up QT, I expect money velocity to surge aggressively from the 60-year lows that it sits at now. As this happens, gold stocks should essentially “run rickshaw” over bullion.

Also, key Chinese gold mining stocks that I use (and own) as key lead indicators for Western miners are staging what can only be described as massive long term chart breakouts.

Please click here now. Double-click to enlarge this GDX chart.

In the summer of 2017, I outlined the $23 – $18 price zone as a key buying area for all gold stock enthusiasts. Investors who took my recommendation are looking good now.

Note the return line that I’ve highlighted on the chart. The price is almost there now. Solid rallies often begin from these technical return lines.

Chinese “Golden Week” holidays begin around Valentine’s Day. That’s still two weeks away. Gold markets close for a week, and the price usually softens. The jobs report is this Friday. Gold typically rallies in the days following the report. A duty cut, gold-positive statements from the Fed, and post jobs report market strength could see GDX reach my $25 – $26 target by Valentine’s Day.

From there a significant market correction would be expected, followed by a major surge to multi-year highs. Please click here now. Double-click to enlarge this GDX weekly chart. In 2018, GDX should surge out of the significant symmetrical triangle that I’ve highlighted. With powerful institutions buying, it should easily reach my $30 – $32 target zone. Gold stocks investors are basically sitting on an inflation-themed money train that the Fed is going to turbocharge with rate hikes, QT, and bank deregulation. All aboard!

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

If a week is a long time in politics, six months is an age in a public company. And as 2017 Full Year Production Results & 2018 Guidance is published today, ordinary shareholders at Petropavlovsk (LSE: POG) may be beginning to question if the intentions behind last year’s messy coup were entirely honest.

To recap: after an astonishing 20-year run at Petropavlovsk, in which veteran gold-bug Peter Hambro weathered the storms of a collapsing gold price and an increasingly impatient shareholder base, the City mainstay finally returned the company to its first profit in January 2017. Shortly thereafter, he was booted out of his own company by a rag-tag bunch of mining dilettantes, with distressed debt funds Sothic and M&G playing monkey, and Renova Group grinding the sorry organ.

We covered each twist and turn of the dispute here at Mining Feeds, exploring the real intentions of Renova Group, the rumours surrounding dormant assets in their portfolio and the toothless City Takeover Panel that wouldn’t know a takeover by stealth if it slapped them in the chops. Shrugging off allegations of impropriety, the repeated justification for the brazen coup, parroted by all three activist shareholders, was that ‘corporate governance’ issues had fallen short of the mark at Petropavlovsk under the leadership of Messrs Hambro and Maslovskiy. A justification made early and repeated often.

Speaking to the Financial Times, City AM, The Times and Reuters, M&G and Sothic repeatedly criticised corporate governance failings at Petropavlovsk and called for greater transparency at board level. [1], [2] Shareholders took them at their word and at the company’s AGM, the old board were fired. Not that a single one of the new Directors turned up to grab the baton, of course. So, it has now been seven months since they took over: how are shareholders being rewarded?

In short, they’re not.

The first act of the new board was to claim credit for Petropavlovsk’s best results: a 166% lead in H1 profits, a 150% increase in net cash from active operations and a 20% boost to sales. The trouble was, the ‘strong set’ of results praised by new Chairman Ian Ashby were solely due to the efforts of the outgoing board. As Alistair Osborne in The Times of London concluded at the time, perhaps the intentions of the insurgents weren’t quite as honourable as claimed. “Corporate governance? Yeah, right.” [3]

Shortly afterwards, Renova Group promptly sold up their controlling stake in Petropavlovsk to an interesting entrepreneur from Kazakhstan. So, having kicked up a shareholder storm at Petropavlovsk, stacked the board with a bunch of directors who don’t know the first thing about mining and given next-to-no indication of how they intended to grow the company they’d fought so hard to control, Renova cut and ran. Exemplary corporate governance…

Kenes Rakishev, the Kazakh businessman who bought Renova’s stake, fortunately has quite a bit of experience in mining having been a part of Central Asia Metals Plc (AIM:CAML), a copper, zinc and lead production and exploration company, for several years.[4]

But in fairness to the new board at Petropavlovsk, they are nothing if not consistent. Not content with claiming credit for the company’s first profits since 2015, they promptly pushed the company back into worrying territory with a sorry set of H2 production results. Announcing with some aplomb that the company had boosted production by as much as 10%, Ian Ashby failed to note that the company’s H2 production results were a whole 11% lower than the impressive results of the first half of 2017.[5] So, a downturn in fortunes presented as cause for celebration? The new board is fast being characterised by new standards for deceit, not transparency.

So, what good news can come of the mess? Well, in interviews given to Reuters, The Daily Telegraph and the Financial Times, new investor Kenes Rakishev has proposed bringing back some of the top team responsible for the recovery at Petropavlovsk. Ahead of a visit to London to meet shareholders earlier this month, Rakishev told reporters of his wish to reinstate former CEO, Pavel Maslovskiy.[6] And to boot, his wishes for the company have already attracted plaudits from industry influencers, with Investors Chronicle praising Rakishev’s ‘conviction bet’ for possible rebranding and M&A action.[7]

The loyalty of Petropavlovsk’s ordinary shareholders has hardly been rewarded by the activism of its majority owners in the past 12 months, and that will sting. Rakishev is an exciting new prospect for Petropavlovsk’s fortunes, and we will be watching his next steps at the company with hopeful anticipation.

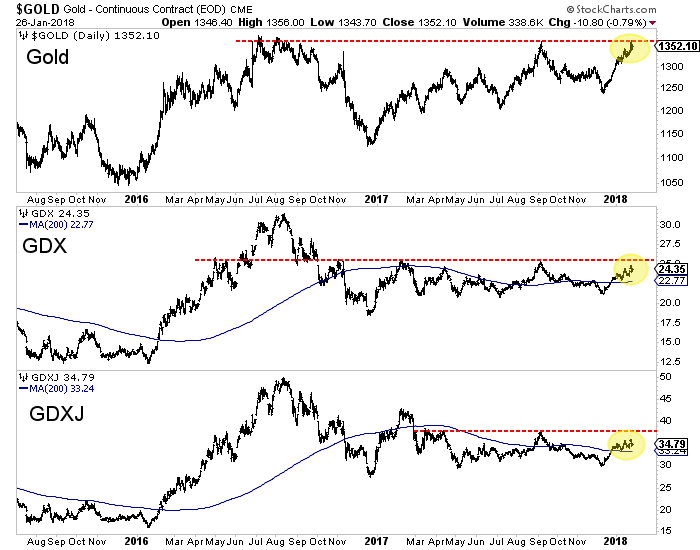

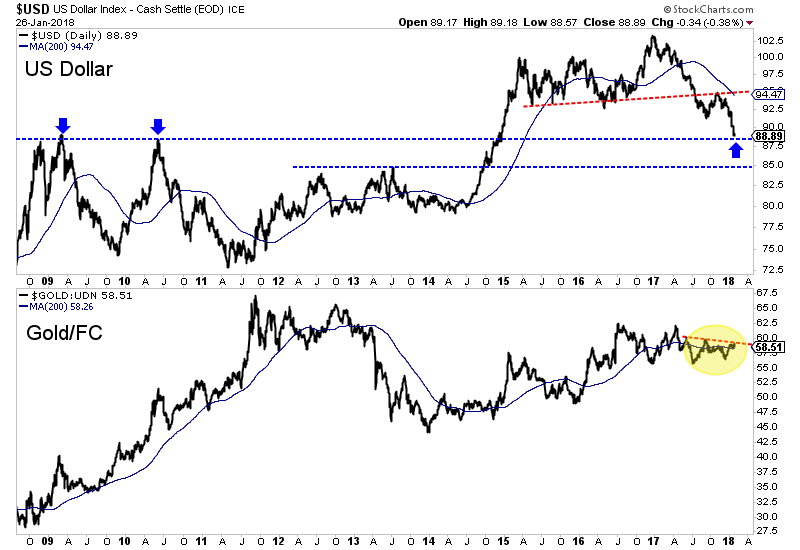

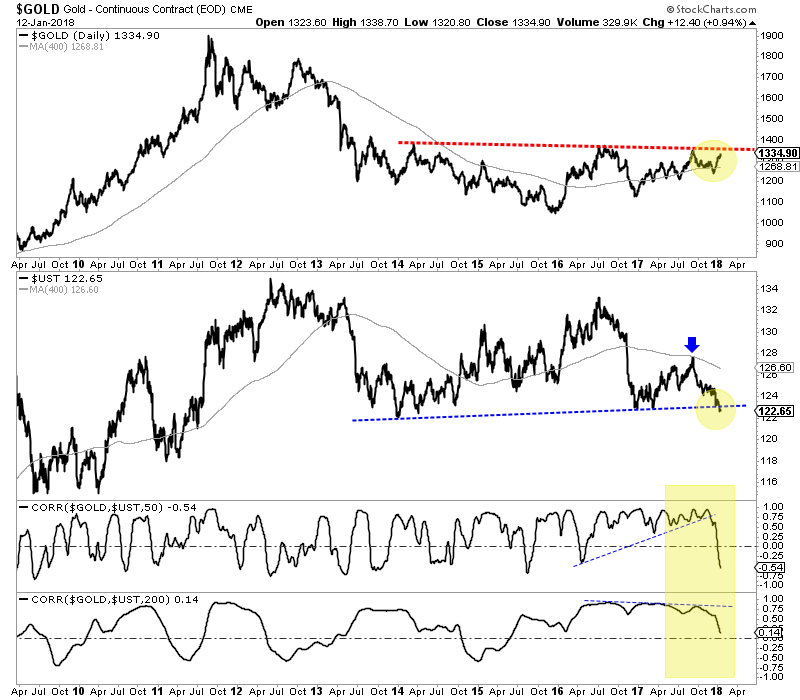

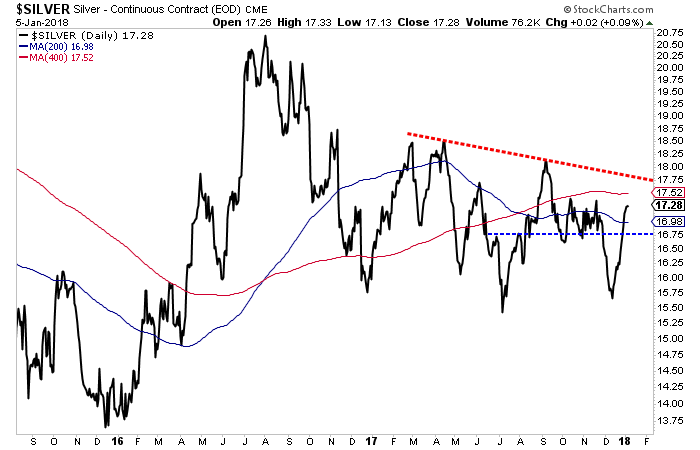

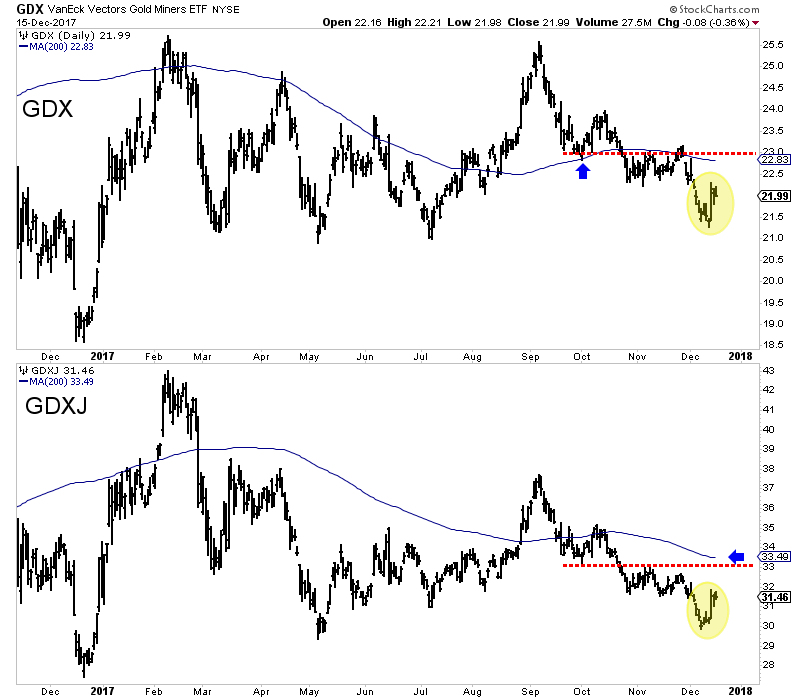

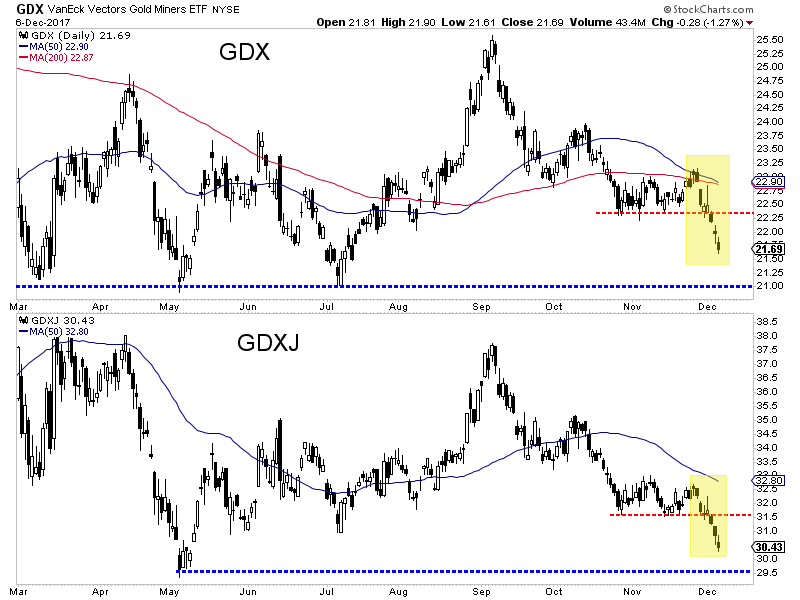

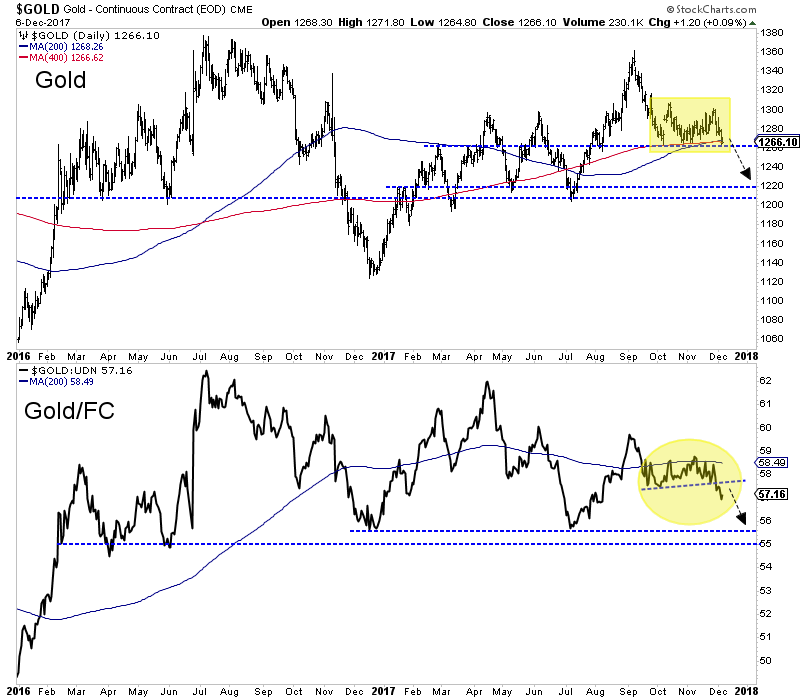

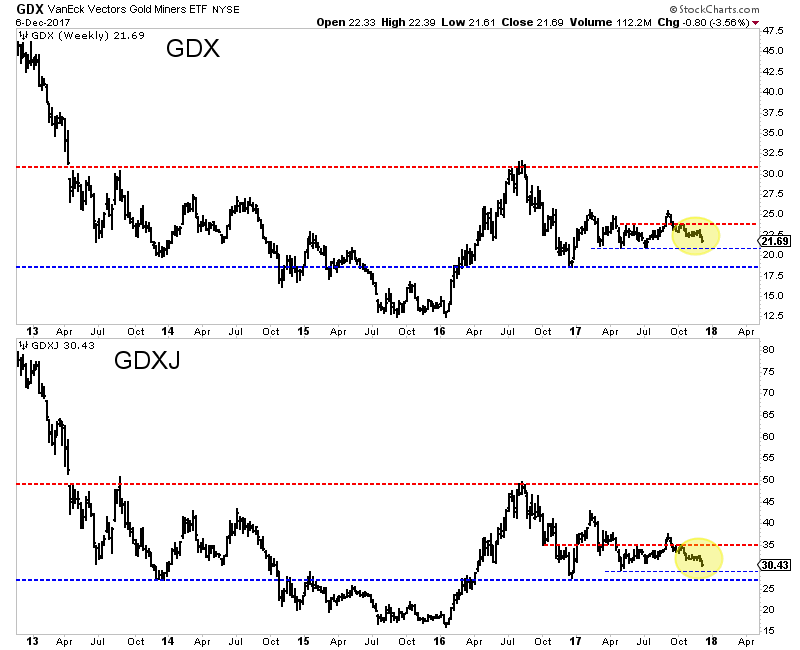

Gold and gold stocks have enjoyed an excellent rebound since their December lows. Over the past six weeks Gold rebounded from a low of $1238 all the way to $1365 in recent days. The miners meanwhile rebounded nearly 18% (GDX) and 21% (GDXJ). However, these markets are approaching important resistance levels and at a time when sentiment is becoming stretched and the US Dollar has become very oversold.

Take a look at the charts of Gold, GDX and GDXJ. Gold has reached the September 2017 highs while GDX came within 2%-3%. GDXJ is lagging but came within less than 5%. Another round of buying over a few days should be enough to push the miners to resistance.

Recent strength in Gold and gold stocks is mostly due to weakness in the US Dollar which is very oversold and approaching important support. On Friday, the US Dollar Index touched 88, which marks the 2009 and 2010 peaks and is the only real support between the low 80s and the low 90s. We also plot Gold against foreign currencies (Gold/FC) which tells if Gold is rising in real terms or if its rising due to the US Dollar weakness. Gold/FC failed to break above key resistance. That signals that over the short-term, Gold would be vulnerable to a bounce in the US Dollar.

Some sentiment indicators suggest the rebound in precious metals could be in its later innings. Thursday the daily sentiment index for Gold hit 91% bulls. Friday, the daily sentiment index for the greenback hit 10% bulls. The CoT’s are not as extreme. Gold’s net speculative position (relative to open interest) is 40% bulls. The 2011, 2012 and 2016 peaks were around 55% bulls. Meanwhile, Silver’s net speculative position is at 26% bulls.

Gold and gold stocks have enjoyed a great rebound since the Fed rate hike but technicals and sentiment suggest they are due for a pause or correction. The miners and Gold are very close to the resistance levels we noted in a recent editorial. Recent strength has been driven mostly by weakness in the US Dollar which is very oversold and testing support. Meanwhile, the daily sentiment index has reached short-term extremes for Gold and the greenback. The odds appear to favor a pause in this rebound or a short-term correction. That is great news for anyone who missed the rally as it would setup a decent buying opportunity before a major breakout. We continue to seek the juniors that are trading at reasonable values but have fundamental and technical catalysts that will drive increased buying. To follow our guidance and learn our favorite juniors for 2018, consider learning more about our premium service.

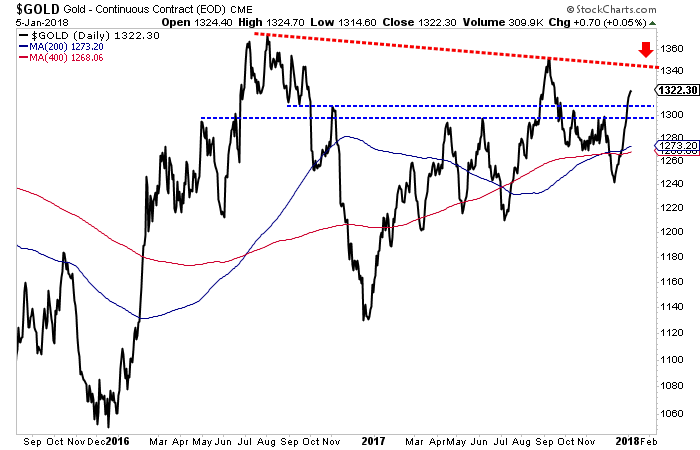

Gold’s strong upleg accelerated this week, powering to major new breakout highs. Speculators rushed to buy gold futures following surprising weak-dollar comments from the US Treasury Secretary, which hit the US dollar hard. That boosted gold to critical technical levels that should really intensify the shift back to bullish psychology. This mounting gold breakout confirms gold’s bull market is very much alive and well.

While this week’s surge put gold on many more traders’ radars, it has actually been picking up steam for 6 weeks now. Gold’s latest major interim low of $1242 came a couple days before the Fed’s latest rate hike in mid-December. The gold-futures speculators who dominate this metal’s short-term price action have always had a deep and irrational fear of Fed rate hikes. Historically gold has thrived in rate-hike cycles!

Leading into that fifth rate hike of this current cycle, these hyper-leveraged traders aggressively dumped longs and ramped shorts at record levels. That battered gold lower while exhausting potential selling. So once the Fed hiked as expected, and didn’t up its 2018 rate-hike forecast from the prior quarter’s three more, these excessively-bearish traders started buying back in. This pattern was seen around past rate hikes.

So two trading days after this latest rate hike when gold was still at $1256, I published an essay outlining why that hike was so bullish for gold. It concluded, “…Fed rate hikes are bullish for gold, and this week’s is no exception… After each past December rate hike which gold-futures speculators sold aggressively into, gold dramatically surged in the subsequent months.” And that’s indeed exactly what happened since.

By the final trading day of 2017 gold had already surged 4.9% out of its pre-rate-hike interim low. Those strong gains continued in this young new year despite these extreme mania stock markets retarding gold investment demand. By this Tuesday, gold’s new upleg extended to an 8.0% gain over nearly 6 weeks. Since the Fed’s rate hike, gold had rallied on 19 out of 27 trading days. Upleg momentum was already building.

Every January the ultra-exclusive World Economic Forum is held in Davos, Switzerland. It attracts the world’s most powerful people, from CEOs to top political leaders to billionaires. The financial media flocks to the Swiss Alps to interview these leading movers and shakers. One of this year’s attendees is Steven Mnuchin, Trump’s Treasury Secretary. He gave an interview in Davos which shocked currency traders.

Mnuchin told reporters, “Obviously a weaker dollar is good for us as it relates to trade and opportunities.” That’s certainly true, as it’s easier for American companies to export around the world when their goods are less expensive due to a lower dollar. But Treasury secretaries have a long tradition of never saying anything about the dollar beyond that they “support a strong-dollar policy”. So Mnuchin’s candor was unexpected.

Mnuchin had made similar comments last year that didn’t affect markets as much. But the combination of this past year’s strong dollar downtrend and a couple more developments that day triggered big US dollar selling. The US had just slapped tariffs on imported solar panels and washing machines hours earlier. Trump’s Commerce Secretary Wilbur Ross spoke alongside Mnuchin at that Davos conference.

Ross warned more trade measures were coming. When asked about trade wars he replied, “Trade wars are fought every single day… So a trade war has been in place for quite a little while, the difference is the US troops are now coming to the rampart.” There’s no more efficient way to boost exports and execute trade wars than jawboning the local currency lower. All this together really struck home for currency traders.

So the US Dollar Index plunged 1.0% on Wednesday following those comments, hitting its worst levels in 3.1 years. Incidentally this past year’s dollar weakness shouldn’t have surprised anyone. Back in late December 2016 when dollar euphoria reigned as the USDX traded at a 14.0-year secular high, I wrote an essay on the unsustainability of those extremes. I warned of “a major topping underway” before a new bear.

With the USDX failing below 90 on those Mnuchin and Ross comments, speculators started flooding into gold futures. After closing near $1341 in US trading Tuesday, gold surged as high as $1352 in overnight action. Those gains extended in the US on Wednesday, with gold blasting up 1.3% to $1358. That was a very important level technically and psychologically, confirming gold’s forgotten bull market is alive and well.

This chart looks at this young gold bull superimposed over speculators’ collective positions in both long and short gold-futures contracts. The Fed’s five rate hikes of this tightening cycle are also highlighted, showing how bullish they’ve proven for gold. This week’s $1358 gold levels are a major upleg breakout, and right on the verge of being a major bull-market breakout. Investors will certainly take notice of this.

Gold’s bull was born in despair in December 2015 the day after the Fed’s first rate hike in 9.5 years. The gold-futures speculators had freaked out leading into that FOMC meeting, fleeing longs while rushing to add shorts. That hammered gold to a 6.1-year secular low. Just a few trading days before that hike when gold was despised, I published deep research showing how gold thrived during past Fed-rate-hike cycles.

Futures speculators were betting the other way, expecting gold to collapse once the Fed ended ZIRP. It didn’t take them long to realize the error in their ways though, as they quickly started buying to cover their excessive shorts while flooding into new longs with a vengeance. So gold soared 29.9% higher over the next 6.7 months, well exceeding the +20% new-bull threshold! That initial bull upleg peaked at $1365 in July 2016.

After such a blistering run, gold needed to take a breather and consolidated high for over a quarter. But that rolled over into a severe correction on two separate events. First gold-futures stops were run which blasted this metal back down to its 200-day moving average. After that gold bounced sharply, but that was truncated by Trump’s surprise election win in early November 2016. That unleashed epic Trumphoria.

Stock markets surged on hopes for big tax cuts soon from the newly-Republican-controlled government. That led futures speculators and investors alike to flee gold, crushing it sharply lower. By mid-December 2016 the day after the Fed’s second rate hike of this cycle, gold had plunged 17.3% to $1128. That was not a new bear though, as it fell shy of the necessary 20% loss. But psychologically it may as well have been!

That exceedingly-anomalous gold plunge in late 2016 mostly driven by the post-election stock-market surge wreaked tremendous sentiment damage. The investors who started getting excited about gold in the first half of 2016 abandoned it, assuming that sharp rally was a flash in the pan. And with the stock markets powering relentlessly higher all throughout 2017 on taxphoria, gold receded into the market shadows.

A couple weeks ago I wrote an essay delving into the selloff dynamics between stock markets and gold. Gold is a unique asset that tends to rally when stock markets sell off materially, making it the ultimate portfolio diversifier. Thus investors tend to view it as the anti-stock trade. It was actually the last stock-market correction in early 2016 that fueled gold’s powerful upleg early that year. Stocks greatly affect gold.

While gold can still rally when stock markets happen to be climbing, investors simply feel no need to diversify their stock-heavy portfolios. So they largely forget gold. Thus gold sentiment for much of 2017 remained nearly as bearish as at those deep late-2016 lows. Investors remembered gold spiraling lower after the election, and that continued to shape their opinions and outlooks on gold regardless of price action.

Gold actually fared really well in 2017 considering the extreme stock-market rally. Last year gold still powered 13.2% higher, very impressive considering the concurrent huge 19.4% S&P 500 surge! This gold bull’s second upleg enjoyed a 19.5% gain over 8.7 months leading into early September. Gold was able to peak at $1348 before that upleg failed after stock markets surged again following a new wave of taxphoria.

Even though gold never entered a bear market, that interim-high level was problematic for sentiment. While close, September 2017’s $1348 remained decisively below July 2016’s $1365. For key technical levels I consider decisive to be 1% beyond the previous extreme. So even though a 19.5% gold upleg is nothing to sneeze at, especially in extremely-euphoric stock markets, it wasn’t enough to change psychology.

Without a new bull-market high, gold stayed out of the financial-news headlines. The investors that had fled this leading alternative investment in the wake of Trump’s election win saw nothing to get gold back on their radars. The legions of gold bears could argue that the secondary lower top confirmed gold was in a downtrend. Technical analysis is something of a Rorschach test, often reflecting analysts’ own biases.

That gold bearishness really intensified heading into this latest Fed rate hike in December 2017. As that month dawned, it had been 16.8 months since gold’s initial bull-market high. Gold’s chance to break out a few months earlier had failed. So as you can see above, gold-futures speculators fled in terror from long positions while also ramping shorts. This latest gold-futures liquidation hit all-time record highs.

Gold-futures speculators’ collective positions are reported once a week in the CFTC’s Commitments of Traders reports. They are current to each Tuesday. In the CoT week ending December 12th on the eve of the Fed’s fifth rate hike of this cycle, speculators dumped an astounding 49.9k long contracts while adding 20.5k new short ones! That was the largest selling on record out of 989 CoT weeks since early 1999!

These traders’ collective bets had run to such hyper-bearish extremes that they had to mean revert after whatever the FOMC did in mid-December. And that has indeed happened. But as long as gold prices just meander within that giant trading range established in the first half of 2016, it will be difficult to shift psychology back to bullish. This week’s strong gold surge on that dollar weakness is starting to change that.

Gold’s $1358 close in US trading Wednesday was 0.7% above its early-September peak. While not quite at that 1%+ threshold for a decisive breakout yet, this is still a major higher high. Gold has been carving higher lows periodically ever since late 2016 when that post-election selloff exhausted itself. But higher lows don’t spark excitement outside of existing gold investors, higher highs are necessary for that.

Gold needs to close over $1361 to see a decisive breakout above the last upleg’s peak. It has traded above that level intraday in both Asian and American trading since Wednesday’s close. It’s only a matter of time until $1361+ sticks on a closing basis. That’s going to finally confirm higher highs to go along with the past 13.3 months’ higher lows. But the real prize remains a decisive breakout to new bull highs.

The new gold bull again peaked at $1365 in early July 2016 within a couple weeks of the UK’s Brexit vote. That unexpected outcome of the British people voting to take back their sovereignty from the unaccountable European Union bureaucrats was such a shock to the markets that major central banks rushed to declare they were ready to print money if necessary. Stocks rallied sharply on hopes for more easing.

The S&P 500 had been drifting sideways to lower without a single new bull-market high for 13.7 months before that. Gold $1365 in July 2016 happened the very trading day before the S&P 500 finally climbed to its first new record high. With stock markets apparently off to the races again, gold demand waned as investors weren’t interested in diversifying. A single close above $1365 will finally confirm gold’s bull persists!

But if gold just touches those bull-to-date highs and fades, bearish technical analysts can easily dismiss it as a double or triple top. In order for gold to garner financial-media attention and attract investors’ gazes back to it, a decisively 1%+ breakout is necessary. That happens at $1379. Gold is so close to a major upside breakout to new bull highs, which will conclusively prove to all investors its current bull market still lives.

That will really start shifting psychology away from the overwhelmingly-bearish levels it’s been stuck at since late 2016. In a normal year gold’s strong 2017 rally would’ve gone a long way to restore bullish sentiment. But again gold was overshadowed last year by the extreme stock-market surge, which stole all the limelight. The blind spot investors harbor for gold will start fading when new bull-market highs are seen.

The exact timing is unknowable and not really important. Gold could power over $1379 within days, or it might take weeks. Investment gold buying will flare again really boosting gold once these extremely-euphoric mania-blowoff stock markets finally roll over. Stock selloffs are great for gold, and even a minor one will easily catapult it to decisive new bull highs. That will dispel the fog of bearishness plaguing gold.

$1400+ gold may seem high after a multi-year bear market followed by a couple years of drifting low in this stock-market-surge-interrupted bull market, but it’s really not. Gold first climbed above $1400 in November 2010 and largely stayed there until June 2013. Over that 2.6-year span gold averaged $1595! And it went as high as $1894 in August 2011. Gold is nowhere near historical extremes, still relatively low.

At best gold’s young bull was only up 29.9% over 6.7 months by mid-2016. That’s trivial as far as gold bulls go, a rounding error. During gold’s last secular bull between April 2001 to August 2011, gold soared 638.2% higher in 10.4 years! Today’s young gold bull would still be tiny even if it saw gold doubled, taking it to $2102. That would still be well below gold’s inflation-adjusted real high from January 1980.

As I’ve been arguing continuously since late 2016, this young gold bull ain’t over yet! Major central banks around the world have conjured many trillions of dollars out of thin air which have levitated world stock markets. That really depressed gold demand. But once these QE-bloated markets inevitably roll over on this year’s new Fed and ECB tightening, a record flood of flight capital will likely seek the ultimate hedge of gold.

Investors can play gold’s ongoing mean-reversion bull in physical gold bullion or the leading GLD SPDR Gold Shares gold ETF. But the coming gold gains will be really amplified by the gold miners’ stocks. As gold rises, gold miners’ profits grow much faster. Thus major gold-stock prices usually leverage gold’s upside by 2x to 3x. Smaller gold miners can double that again. Gold stocks yield life-changing gains in gold bulls.

In essentially the same span of that last gold bull ending in late 2011, the HUI gold-stock index rocketed 1664.4% higher! Last week I wrote an essay explaining why the parallel flagship GDX VanEck Vectors Gold Miners ETF was on the verge of a major $25 upside breakout on strong earnings potential. There’s no doubt investors will flood into gold stocks as gold psychology changes, ultimately driving incredible gains.

While every investor needs to have a 5%-to-10%+ portfolio allocation to gold for diversification purposes, great gold stocks should be added on top of that. The beaten-down and left-for-dead gold miners’ stocks are deeply undervalued today with gold still out of favor. This is the only sector in all the stock markets likely to power much higher when everything else heads lower. Great gold stocks are essential to own today!

At Zeal we’ve literally spent tens of thousands of hours researching individual gold stocks and markets, so we can better decide what to trade and when. As of the end of Q4, this has resulted in 983 stock trades recommended in real-time to our newsletter subscribers since 2001. Fighting the crowd to buy low and sell high is very profitable, as all these trades averaged stellar annualized realized gains of +20.2%!

The key to this success is staying informed and being contrarian. That means buying low before others figure it out, before gold’s bull-market breakout becomes apparent. An easy way to keep abreast is through our acclaimed weekly and monthly newsletters. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. For only $12 per issue, you can learn to think, trade, and thrive like contrarians. Subscribe today, and get deployed in the great gold and silver stocks in our full trading books!

The bottom line is this gold bull’s third upleg is breaking out. This week gold closed above the peak from its second upleg, and is close to a decisive breakout. That puts gold within spitting distance of its bull-to-date high of $1365 from July 2016. Once gold powers decisively above those levels, it will confirm to all that gold’s bull is very much alive and well. That will work wonders to shift psychology back to bullish again.

Impressively gold is doing all this with stock markets still at mania-blowoff record highs. Gold investment demand explodes once stock markets roll over, which is what ignited and fueled this gold bull’s strong initial upleg in early 2016. So when the long-overdue and inevitable material stock-market selling finally arrives, gold’s advance will really accelerate. Get long before this major bull-market breakout changes everything!

The good news for gold keeps flowing, with institutions around the world stepping up to the buy window ever-more frequently.

They are clearly embracing gold as a key portfolio holding for the long term.The bottom line: institutional respect for gold as a portfolio diversifier has never been stronger than it is right now.

On that exciting note, please click here now. Standard Chartered bank carries serious institutional weight. Their gold market analysis projects a surge to five-year highs. This kind of positive analysis that continues to emanate from major banks is bringing more institutions into gold.

Please click here now. Germans are now the most aggressive gold buyers in Europe.

While SPDR fund buying was soft in 2017, German institutions bought about 50 tons of gold… in just one physically backed gold fund! Deutsche Boerse reports that family offices and individuals are starting to join institutions on the buy. I expect record demand in Germany in 2018.

I’ve predicted that Trump would unveil inflationary tariffs in America, and that’s in play as of this morning. Please click here now. I’ve coined the term “Trumpflation” to describe what is coming, and what is coming is very positive for gold.

Trump sees a huge cash cow for the government as solar energy becomes a gargantuan industry. The citizens get hit hard… unless they own a diversified portfolio of gold stocks!

I’ve also predicted a major partnership between blockchain and gold will emerge, creating a significant rise in global demand for the world’s greatest metal.

On that note, please click here now. Rob Martin is head of market infrastructure for the World Gold Council.

In this interview he does a great job in explaining how gold backed cryptocurrency tokens will be exempted from onerous government regulation on cryptocurrencies that are not backed with gold.

Please click here now. A tidal wave of tokenized gold, silver, and industrial metal offerings is coming. Are investors prepared?

The LBMA in London is prepared. The LBMA runs the world’s largest market for physical gold. This morning they announced they are considering employing blockchain technology to strengthen gold supply chain integrity.

If it happens, I expect markets in China, Dubai, and India to quickly follow the London leaders. Any action that increases the integrity of the supply chain increases institutional respect for the asset class. As noted, the good news for gold just keeps rolling!

Bitcoin itself has been soft since the CBOE five-coin futures contract was launched. Tom Lee was head of equities for JP Morgan and wisely sold stocks in 2016 after entering at the March 2009 lows.

Tom views the US stock market not as overvalued, but as fully valued. I see it as slightly overvalued, with real risk exceeding potential reward.

The similarities between today’s market and the market of 1929 are eerily similar. I don’t know if the market is poised for a repeat of that horrific past. I do know that when power players like Tom Lee call the market fully valued, it’s usually a good time to book some profits.

Regardless, Tom eagerly embraced bitcoin in 2016 and has never looked back. He’s a very calm and rational man whose views are widely followed in the institutional investor community. Tom says his team are “aggressive bitcoin buyers” in the $9000 area, with a five-year target of $125,000 per bitcoin.

My blockchain focus now is still bitcoin, but also the “alt coins”. I highlight the most exciting action for both with my www.gublockchain.com newsletter. My long term bitcoin target is a little higher than Tom’s ($500,000), but even at $30,000 most investors should be sporting a very big smile!

I expect the bitcoin price will likely remain soft until the CBOE futures expiry onFebruary 14. The $10,000 – $8,000 price area appears to represent very good value for new bitcoin investors.

Please click here now. Gold’s technical action is glorious.

A pennant breakout was immediately followed by flag-like action, and an upside breakout is in play this morning. Also, note the decent support zones I’ve highlighted at $1328, $1320, $1300, and $1270. In a negative scenario, these are all key buy zones.

Gold looks poised to take a major battering ram to the $1370 area highs that were created by Modi’s infamous cash call-in. A move above $1370 opens the door for a charge towards $1500!

Please click here now. GDX is starting to show some impressive technical action. New investors who are stop loss enthusiasts could use $22.90 as their maximum risk price. Others can employ put options if nervous.

Regardless, GDX appears to be poising for a charge to my $25 – $26 price area. I expect 2018 will be ultimately be remembered as the year gold stocks begin a long term bull cycle against bullion. I’m predicting that over the next five years they will go nose to nose with bitcoin, in the battle to be the performing asset class in the world!

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

The world’s leading gold-stock ETF is nearing a major upside breakout from key technical levels. GDX is getting closer to challenging and powering above $25. That would accelerate the sentiment shift in this deeply-undervalued sector back to bullish, enticing investors to return. Good operating results from the major gold miners in their upcoming Q4’17 earnings season could prove the catalyst to fuel this GDX $25 breakout.

The classic way to measure gold-stock-sector price action is with the HUI NYSE Arca Gold BUGS Index. But the HUI benchmark is being increasingly usurped by the GDX VanEck Vectors Gold Miners ETF as the gold-stock metric of choice. GDX is used far more often than the HUI in gold-stock analyses these days, both online and on financial television. I haven’t seen the HUI mentioned on CNBC for years now.

GDX does have major advantages over the HUI. Most importantly it is readily tradable as an ETF and with options. GDX’s component stocks and their weightings are also regularly updated by elite gold-stock analysts, keeping it current. The HUI is rarely if ever updated to reflect company-specific changes in the ranks of the world’s top gold miners. GDX is dynamic where the HUI is effectively static and outdated.

GDX also has limitations as a gold-stock metric though. It was only born in May 2006, so that’s the limit of its price history available for analysis. And because its managers are paid 0.51% of its assets each year to maintain this ETF, GDX is not as pure of measure of gold-stock performance as a normal index. Over a decade that adds up to a substantial 5% difference. Nevertheless GDX’s popularity continues to grow.

This week GDX had $7.7b in assets under management, dwarfing its direct competitors. That was 21x larger than the next-biggest 1x-long major-gold-stock ETF! GDX’s sister GDXJ Junior Gold Miners ETF weighed in at $4.7b, but that generally includes smaller gold miners. GDX is the undisputed king of the gold-stock ETFs. As a contrarian speculator, I watch GDX’s price action in real-time all day every day.

For an entire year now, GDX has meandered in a relatively-tight trading range between $21 to $25. As gold stocks periodically fell even deeper out of favor, this ETF slumped down near $21 lower support. Then as they inevitably rallied back out of those lows, GDX climbed back up near $25 resistance. That made for a roughly-20% gold-stock price range, certainly narrow by this sector’s standards and tough to trade.

This GDX chart over the past couple years or so highlights 2017’s gold-stock consolidation. With this unloved sector neither rallying nor falling enough to get interesting, investors mostly abandoned it over the past year. So gold stocks largely drifted sideways on balance, which certainly proved vexing for the few remaining contrarian speculators and investors. A GDX $25 breakout would greatly improve psychology.

Last year’s gold-stock performance per GDX was very poor. This ETF’s price climbed 11.1% in 2017, which is better than a kick in the teeth. But gold’s impressive 13.2% gain last year well outpaced the gold stocks’ performance. Normally the major gold miners’ stocks amplify gold advances by 2x to 3x, so GDX should’ve powered 26% to 40% higher in 2017. Gold stocks are only worthwhile if they outperform gold.

That’s because gold miners face many additional operational, geological, and geopolitical risks compared to just owning gold outright. So if the gold stocks don’t outperform gold, they simply aren’t worth owning. Seeing them lag the metal which drives their profits for essentially an entire year is extremely anomalous. It’s a reflection of the entire global markets proving extremely anomalous in 2017, an exceedingly-weird year.

Gold stocks normally perform much more like 2016 than 2017. A couple years ago GDX rocketed 52.5% higher in one of the best major-sector-ETF performances in all the stock markets. That greatly amplified 2016’s underlying 8.5% gold advance by 6.2x. All those gains rapidly accrued in that year’s first half, as GDX skyrocketed 151.2% higher in 6.4 months on a parallel 29.9% gold upleg! Gold stocks can really move.

But last year as extreme record-high stock markets and the even-more-extreme bitcoin popular speculative mania stole the spotlight from gold, gold stocks were largely left for dead. Speculators and investors alike wanted nothing to do with classic alternative investments when everything else proved much more exciting. Thus GDX hasn’t been able to decisively break out above its $25 upper resistance, despite trying.