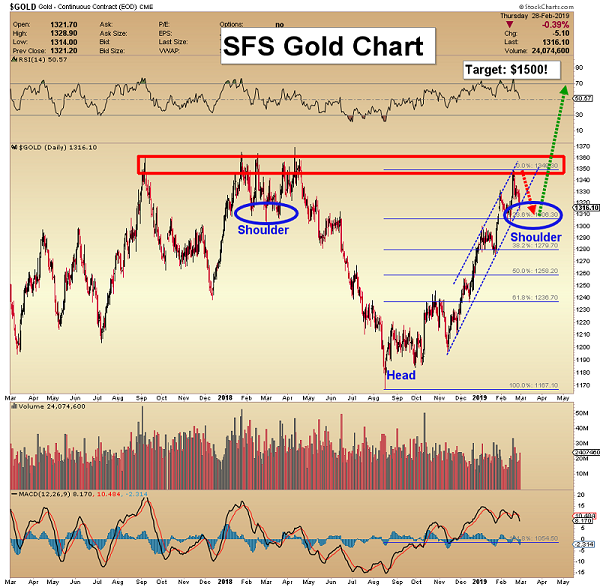

Here are today’s videos and charts (double-click to enlarge):

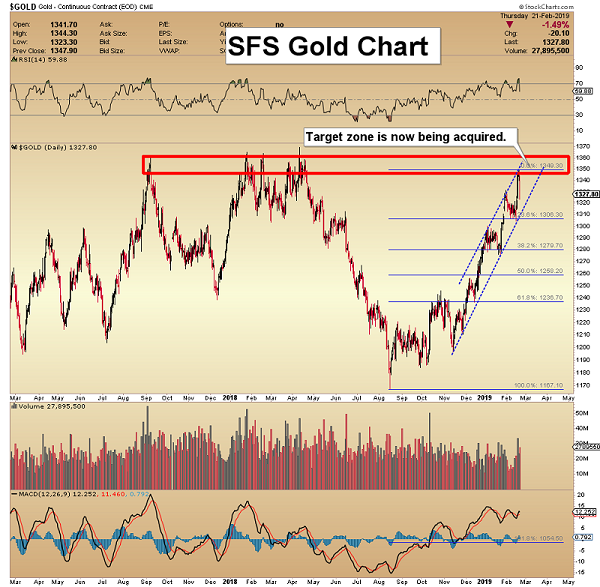

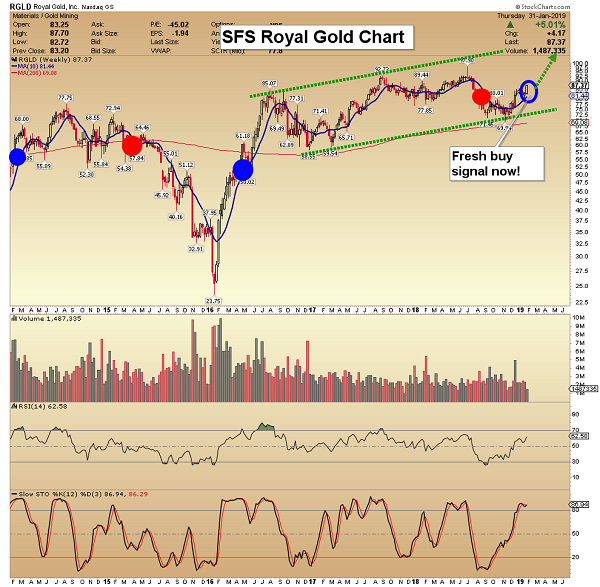

SFS Key Charts, Signals, & Video Analysis

I’m quite excited about the pullback in gold because the fundamentals are getting better and the technical action is healthy.

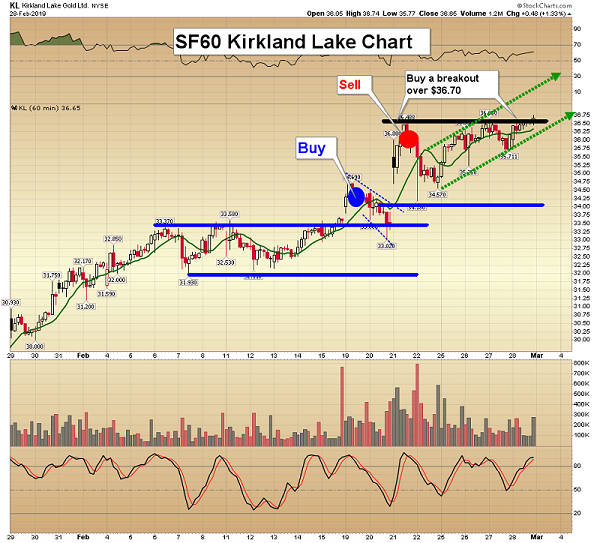

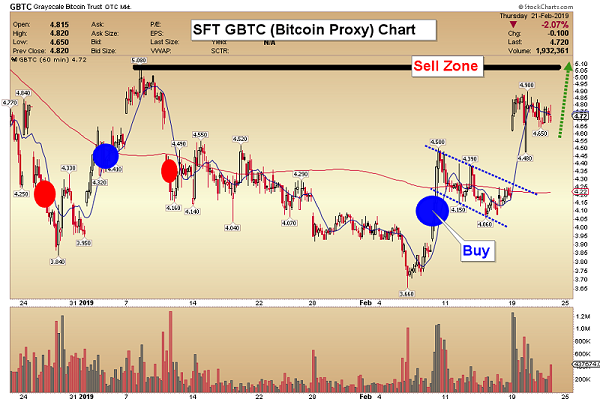

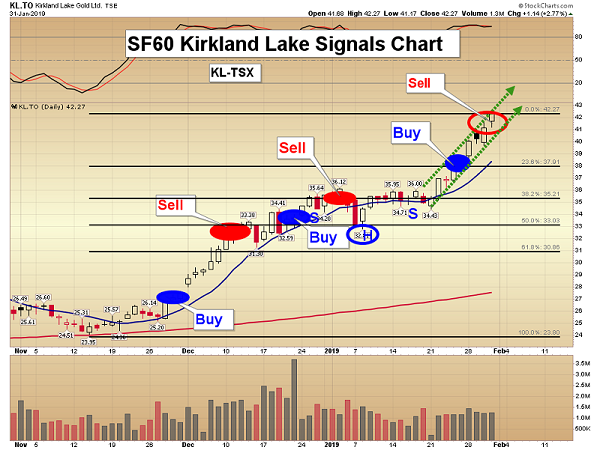

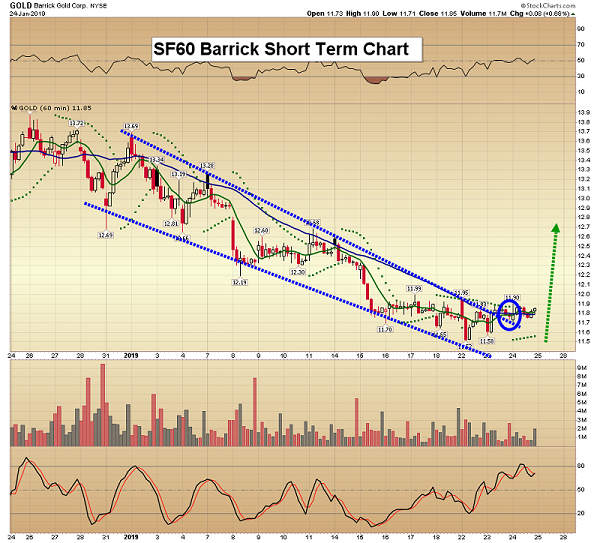

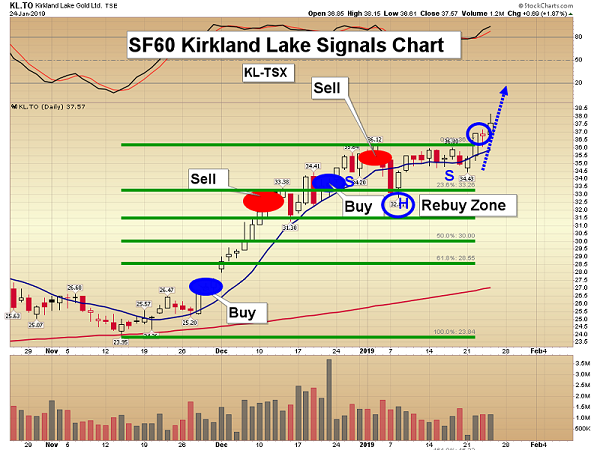

SF60 Key Charts, Signals, & Video Analysis

Kirkland is a leader in the gold stock sector and it’s now in one of the important Investor’s Business Daily growth stock indexes.

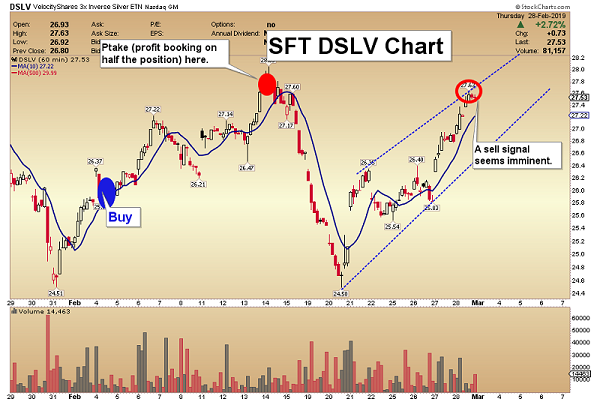

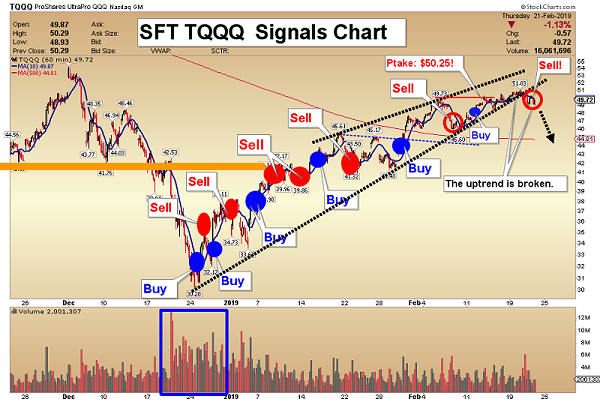

SF Trader Key Charts, Signals, & Video Analysis

Our positioning into DUST was timely!

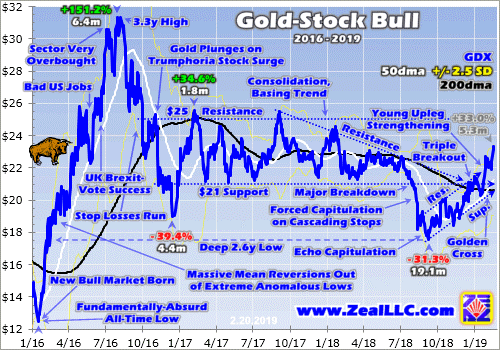

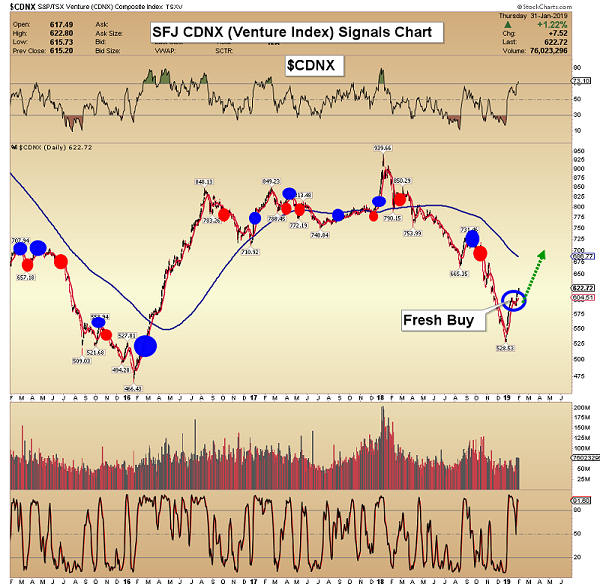

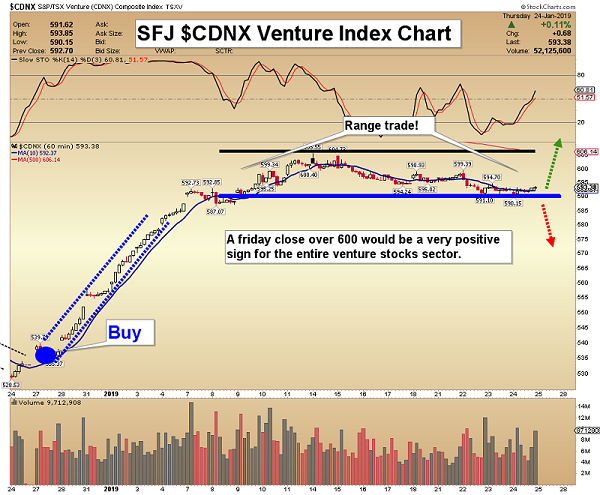

SFJ Key Charts, Signals, & Video Analysis

Prudent profit booking into strength in this gold bull market is important.

Thanks,

Morris Hubbartt

Unique Introduction For Website Readers: Send me an email to signals@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

Stay alert for our Super Force alerts, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

Email:

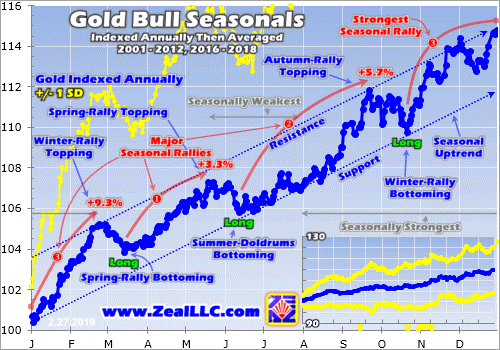

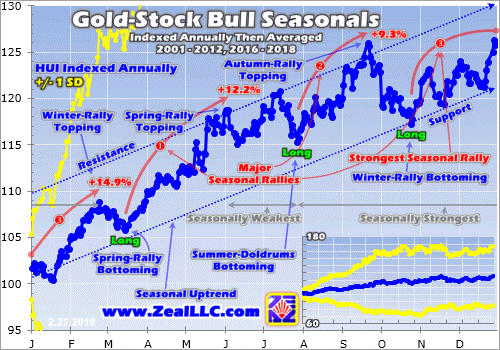

The gold miners’ stocks have been climbing higher on balance, enjoying a solid upleg that is gathering steam. That’s fueling improving sentiment, driving more interest in this small contrarian sector. This gold-stock upleg is likely to grow in coming months, partially because of very-favorable spring seasonals. The gold stocks’ second-strongest seasonal rally of the year typically unfolds between mid-March to early June.

Seasonality is the tendency for prices to exhibit recurring patterns at certain times during the calendar year. While seasonality doesn’t drive price action, it quantifies annually-repeating behavior driven by sentiment, technicals, and fundamentals. We humans are creatures of habit and herd, which naturally colors our trading decisions. The calendar year’s passage affects the timing and intensity of buying and selling.

Gold stocks exhibit strong seasonality because their price action mirrors that of their dominant primary driver, gold. Gold’s seasonality generally isn’t driven by supply fluctuations like grown commodities experience, as its mined supply remains fairly steady year-round. Instead gold’s major seasonality is demand-driven, with global investment demand varying dramatically depending on the time in the calendar year.

This gold seasonality is fueled by well-known income-cycle and cultural drivers of outsized gold demand from around the world. The seasonal gold year starts in late July as Asian farmers begin reaping their harvests. They plow some of their surplus income into gold. That’s soon followed by the famous Indian wedding season in autumn, with its heavy gold buying for brides’ dowries during marriage-auspicious festivals.

After that comes the Western holiday season, where gold jewelry demand surges for Christmas gifts for wives, girlfriends, daughters, and mothers. Following year-end, Western investment demand balloons after bonuses and tax calculations as investors figure out how much surplus income the prior year generated for investment. Then after that Chinese New Year gold buying flares up heading into February.

These understandable cultural factors drive surges of outsized gold demand between late summer and late winter. But interestingly there is one more gold-demand spike in spring. Over the years I’ve seen a variety of theses explaining this mid-March-to-late-May gold rally, but nothing definitive like for the rest of the year’s seasonality. As silly as it sounds, I suspect spring itself is the reason for this demand surge.

Sentiment exceedingly influences investing, which requires optimism for the future. Investors won’t risk deploying their scarce capital unless they believe it will grow. And the glorious expanding sunshine and warming temperatures of spring naturally breed optimism. The vast majority of the world’s investors are far enough into the northern hemisphere that spring has a major psychological impact, buoying their spirits.

Since it is gold’s own demand-driven seasonality that fuels the gold stocks’ seasonality, that’s logically the best place to start to understand what’s likely coming. Price action is very different between bull and bear years, and gold remains in a young bull market. After being crushed to a 6.1-year secular low in mid-December 2015 on the Fed’s first rate hike of this cycle, gold blasted 29.9% higher over the next 6.7 months.

Crossing the +20% threshold in March 2016 confirmed a new bull market was underway. Gold corrected after that sharp initial upleg, but normal healthy selling was greatly exacerbated after Trump’s surprise election win. Investors fled gold to chase the taxphoria stock-market surge. Gold’s correction cascaded to mammoth proportions, hitting -17.3% in mid-December 2016. But that remained shy of a new bear’s -20%.

Gold’s last mighty bull market ran from April 2001 to August 2011, where it soared 638.2% higher! And while gold consolidated high in 2012, that was technically a bull year too since gold just slid 18.8% at worst from its bull-market peak. Gold didn’t enter formal bear-market territory at -20% until April 2013, thanks to the crazy stock-market levitation driven by extreme distortions from the Fed’s QE3 bond monetizations.

So the bull-market years for gold in modern history ran from 2001 to 2012, skipped the intervening bear-market years of 2013 to 2015, and resumed in 2016 to 2019. Thus these are the years most relevant to understanding gold’s typical seasonal performance throughout the calendar year. We’re interested in bull-market seasonality, because gold remains in its latest bull today and bear-market action is quite dissimilar.

Prevailing gold prices varied radically throughout these modern bull-market years, running between $257 when gold’s last secular bull was born to $1894 when it peaked a decade later. All these years along with gold’s current bull since 2016 have to first be rendered in like-percentage terms in order to make them perfectly comparable. Only then can they be averaged together to distill out gold’s bull-market seasonality.

That’s accomplished by individually indexing each calendar year’s gold price action to its final close of the preceding year, which is recast at 100. Then all gold price action of the following year is calculated off that common indexed baseline, normalizing all years regardless of price levels. So gold trading at an indexed level of 105 simply means it has rallied 5% from the prior year’s close, while 95 shows it’s down 5%.

This chart averages the individually-indexed full-year gold performances in those bull-market years from 2001 to 2012 and 2016 to 2018. 2019 isn’t included yet since it remains a work in progress. This bull-market-seasonality methodology reveals that gold’s spring rally is its last push higher before the summer doldrums arrive. While this is gold’s smallest seasonal rally of the year, the gold stocks greatly leverage it.

During these modern bull-market years from 2001 to 2012 and 2016 to 2018, gold’s spring rally tended to start in mid-March on average. From that major seasonal low following the winter rally, gold often starts grinding higher before its gains accelerate through April and much of May. This spring rally has generally run its course by late May. Across the 15 bull years in this study, gold averaged modest spring rallies of 3.3%.

This spring rally unfolds rapidly, with an average duration of just 2.2 months. That makes it the smallest and shortest of gold’s three major seasonal rallies, falling way behind the champion 9.3% winter rally that precedes it and the strong 5.7% autumn rally that follows the summer doldrums. Nevertheless, it is still well worth trading. 3.3% gains do really make a difference, and naturally about half of years exceed this mean.

On average gold’s spring-rally bottoming occurred on March’s 10th trading day, which will be the 14th this year. If today’s seasonals stay true to form, gold will slump in the first couple weeks of March. But that seasonal pullback between the winter and spring rallies is pretty modest, averaging just 1.3% over a few weeks at most. The resulting mid-March lull in gold prices spawns an excellent gold-stock buying opportunity.

Gold’s average seasonal performances in March, April, and May during these modern bull-market years ran -0.3%, +1.6%, and +0.6%. While even April is just gold’s 6th-best month of the year, it still has an outsized impact on gold-stock prices. This has to be sentiment-driven. Optimism runs high in the spring anyway, and plenty of bullish psychology lingers following gold stocks’ strong winter rally in preceding months.

This year’s spring gold rally has excellent potential to come in on the large side. Gold investment demand surged in Q4’18 as global stock markets crumbled. They are likely rolling over into a long-overdue major bear. When investors start worrying its next major downleg is brewing, they will again flood into gold to continue diversifying their stock-heavy portfolios. Surging gold investment demand propels gold strongly higher.

That may push gold to the verge of a major decisive breakout to new bull highs! At best in February, gold hit $1341 on close. Assuming a 1.3% early-March seasonal pullback before a typical 3.3% spring rally, gold would hit $1367. That’s just above its bull-to-date peak of $1365 seen way back in early July 2016. Investor and speculator interest in gold, and capital inflows into it, will explode as new bull highs are achieved.

And as goes gold, so go gold stocks. Gold stocks also exhibit strong seasonality, which is of course the direct result of gold’s own seasonality. Since gold-mining costs are largely fixed when mines are being planned, fluctuations in gold’s price flow directly into amplified moves in gold-mining profits. Higher gold prices drive much-higher earnings for the gold miners, which attract in more investors to bid up stock prices.

The ironclad historical relationship between the price of gold, gold-mining profitability, and therefore gold-stock price levels is exceedingly important to understand. If you need to get up to speed, I wrote an essay looking at gold-stock price levels relative to gold early last month. Fundamentally gold stocks are leveraged plays on gold, and greatly outperform in the spring on gold’s seasonals and general optimism.

This next chart applies this same bull-market-seasonality methodology used on gold directly to the gold stocks. It looks at the average annual indexed performance in the flagship HUI NYSE Arca Gold BUGS Index in these same bull-market years of 2001 to 2012 and 2016 to 2018. Using the HUI is necessary because the popular GDX VanEck Vectors Gold Miners ETF was only born in May 2006, missing bull years.

That was halfway into the last secular gold-stock bull, which ran from November 2000 to September 2011. Over that long 10.8-year span, the HUI skyrocketed a life-changing 1664.4% higher on gold’s parallel 638.2% bull! Gold-stock prices naturally mirror and amplify gold action since it dominates gold-mining earnings. That’s true across entire secular bulls, within individual uplegs, and even in calendar-year seasons.

Gold stocks’ seasonal spring rally is much stronger than gold’s, buttressing that spring-optimism-drives-stock-buying thesis. Between mid-March and early June, the gold stocks have averaged hefty 12.2% rallies in these 15 modern bull-market years. That makes for exceptional 3.7x upside leverage to gold’s 3.3% seasonal spring rally! Interestingly this is gold stocks’ best seasonal leverage to gold’s gains by far.

While the HUI averaged 14.9% surges during gold’s winter rally, that only made for 1.6x upside leverage to gold’s big 9.3% gain. And the HUI’s 9.3% average gain during gold’s autumn rally also only amplified gold’s 5.7% gain by 1.6x. So while the gold-stock spring rally’s 12.2% average gains rank second out of these three seasonal rallies, it offers the most bang for the buck in gold-stock upside compared to gold!

Like gold, the gold miners’ stocks suffer a seasonal slump from late February to mid-March. That has averaged 2.7% in these modern bull-market years. So don’t be worried into selling if we see a typical early-March slump in this sector. That’s usually just a mild pullback before gold stocks’ strong spring rally gets underway. Any seasonal weakness is a great opportunity to add new gold-stock trades relatively low.

The gold stocks’ post-winter-rally pre-spring-rally lull tends to bottom on March’s 11th trading day, which will be the 15th this year. From there the HUI surges 12.2% higher on average over the next 2.7 months into early June. Interestingly the gold stocks tend to top a couple weeks after gold peaks in late May. That’s likely the result of momentum fueled by spring optimism and strong gains since the prior summer.

Assuming this year’s gold-stock seasonals conform to their bull-year precedent in coming months, some impressive levels are coming before summer. If the HUI first retreats 2.7% from its February peak into mid-March before powering 12.2% higher into early June, we are looking at 193.0 heading into this year’s summer doldrums. Those would be the best gold-stock levels since February 2018 on merely normal seasonals.

But this year’s spring seasonal rally has real potential to grow much larger than usual. Of course if gold’s own spring rally becomes outsized due to stock-market-selloff-driven surging gold investment demand, the gold miners’ stocks will leverage those gains. And the higher gold stocks climb, the more bullish their psychology. Speculators and investors alike love chasing momentum and piling into winning trades en masse.

More importantly this sector’s strengthening fundamentals should support bigger seasonal gains. Gold’s price averaged $1228 in Q4’18. While the gold miners are still finishing reporting their results for last quarter and full-year 2018, odds are their collective all-in sustaining costs will remain flat. Every quarter I wade through the latest results of the major gold miners of GDX, and usually publish the Q4 ones in mid-March.

Over the last four fully-reported quarters ending in Q3’18, the GDX gold miners averaged AISCs of $858, $884, $856, and $877. That makes for an $869 mean, but let’s round that to $875 for easier calculations. At Q4’s average gold price of $1228 and $875 AISCs, the major gold miners of GDX and the HUI likely earned profits near $353 per ounce last quarter. But so far in Q1, the average gold price has surged to $1305!

With AISCs this quarter likely to be stable too around that usual $875, the gold miners are likely earning profits of $430 per ounce so far in Q1. That is a massive 21.8% higher quarter-on-quarter! If investors expect Q1’19 earnings to come in this strong, there’s no way gold stocks will merely see a seasonally-average spring rally. Strong operational results in both Q4 and Q1 reporting should fuel a major gold-stock bid.

Seasonal spring rallies can balloon very large in rising-gold-price environments, which drive excellent fundamentals for the gold miners. The last example happened in spring 2016, when the HUI powered 32.3% higher within its normal spring-rally span! That was just a fraction of a monster 182.2% upleg that skyrocketed over just 6.5 months. Gold-stock buying is fast and furious when momentum fuels enthusiasm.

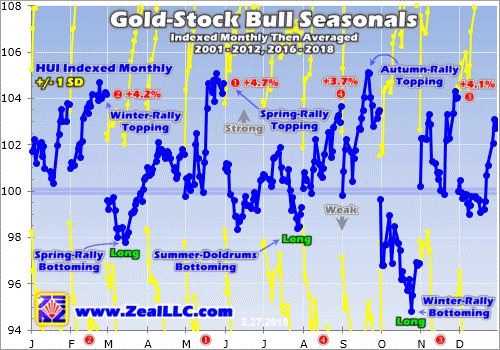

This last chart breaks down gold-stock seasonality into even-more-granular monthly form. Each calendar month between 2001 to 2012 and 2016 to 2018 is individually indexed to 100 as of the previous month’s final close, then all like calendar months’ indexes are averaged together. Slicing up seasonal tendencies this way shows May has actually averaged gold stocks’ strongest month of the year in modern bull-market years!

During the 15 Aprils in these modern gold bull-market years, the gold stocks as measured by the HUI saw average gains of 1.6%. But the lion’s share of the spring-rally gains came in May, where average gains nearly tripled to 4.7%! For decades if not longer, May has been one of the best and most-important months to be heavily long gold miners’ stocks. Only February and November have managed to rival it.

The key to gold stocks’ spring rally is to get your capital deployed by mid-March, when gold stocks swoon to their spring-rally bottoming. In intra-month terms the initial gains are often fast in late March as gold stocks rebound out of their seasonal lull. But then the spring rally tends to slow down in mid-April, which invariably discourages impatient and short-sighted traders. The real gains come in May, when gold stocks surge.

Of course the standard seasonality caveat applies that these are mere tendencies, not primary drivers of gold or gold stocks. Seasonal tailwinds can be easily drowned out by bearish sentiment, technicals, and fundamentals. Seasonality doesn’t always work, especially when it doesn’t align with the primary drivers of sentiment, technicals, and fundamentals in that order. Thankfully that certainly isn’t the case this year.

Gold-stock sentiment is growing increasingly bullish as this sector’s solid upleg gathers steam. Seeing higher lows and higher highs on balance further feeds into positive psychology, and traders love to chase momentum in rallying sectors. Mounting stock-market fears of a young bear getting underway should continue to push gold investment demand higher. The resulting higher gold prices really boost mining profits.

Outsized gold-stock gains during this spring-rally timeframe are fully justified fundamentally when gold itself is rallying. When sentiment, technicals, fundamentals, and seasonals all align behind gold stocks, they often surge dramatically higher. Unfortunately most speculators and investors won’t realize this until most of the spring-rally gains have already been won. Buy low in mid-March instead of buying high in early June!

While you can ride gold stocks’ spring rally higher in GDX, the major miners dominating it are struggling to grow their production. Far-better gains will be won in smaller mid-tier and junior gold miners with superior fundamentals. The best are increasing their output through new mine builds and expansions, which also lowers their costs further boosting their profits. Their upside potential utterly trounces that of the GDX majors.

The earlier you get deployed, the greater your gains will be. That’s why the trading books in our popular weekly and monthly newsletters are currently full of better gold and silver miners mostly added in recent months. The gains we won in 2016 were amazing the last time American stock investors returned to gold. Our newsletter stock trades that year averaged +111.0% and +89.7% annualized realized gains respectively!

The gold-stock gains should get really big as today’s young gold and gold-stock uplegs grow. The gold miners are the last undervalued sector in these still-expensive stock markets, and rally with gold during stock-market bears unlike anything else. To multiply your wealth in the stock markets you have to do your homework and stay abreast, which our newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. You can subscribe today for just $12 per issue!

The bottom line is gold stocks often experience a strong spring rally seasonally. This is driven by gold’s own seasonality, where outsized investment demand arises at certain times during the calendar year. Gold usually enjoys a solid spring rally likely driven by the universal optimism this season brings. And since gold drives gold miners’ profitability, their stock prices naturally follow it higher while amplifying its gains.

This year’s coming spring rally is due to start in mid-March, with great potential to grow much larger than normal. Gold-stock sentiment is slowly improving as this sector’s current upleg continues grinding higher on balance. And higher gold prices driven by renewed investment demand on stock-market-selloff fears is really boosting gold-mining earnings. All this with strong seasonal tailwinds should fuel an outsized spring rally.

Adam Hamilton, CPA

March 4, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Back in 2013 I recall having a bearish view on the stock market due to extremely bullish sentiment readings. The market completely ignored that, made a major breakout through 13 year resistance and continued running for years.

Lesson learned.

Turning to Gold, we find something similar during major breakouts in 2005, 2007 and 2009. In the chart below we plot Gold along with its net speculative position (as a percentage of open interest) and the widely followed daily sentiment index.

In August 2005 and the start of 2006, the net speculative position in Gold reached (excluding 2004) what were the highest levels since the start of the data in 1987.

In late 2007, the net speculative position was not at an extreme but the daily sentiment index spent quite a bit of time around 90% bulls immediately prior to Gold breaking out to a new all time high.

Both the net speculative position and daily sentiment index were very elevated in the fall of 2009, immediately prior to Gold breaking out above its 2008 peak. The net speculative position then was at its second highest level since 1987.

As of February 5, when the Gold price closed at $1319/oz, the net speculative position in Gold was 27% of open interest. Gold gained $30/oz since then but that is well below the 55%-60% peak levels seen in 2016, 2012, 2009 and 2004-2006.

While that is encouraging, history shows that if and when Gold breaks its resistance ($1375-$1400/oz) sentiment indicators figure to be close to bullish extremes. When a market is coming out of a bad bear market or on the cusp of a multi-year breakout, bullish sentiment isn’t necessarily bearish.

In fact, a market that cannot register bullish sentiment extremes is one that may not be strong enough to breakout.

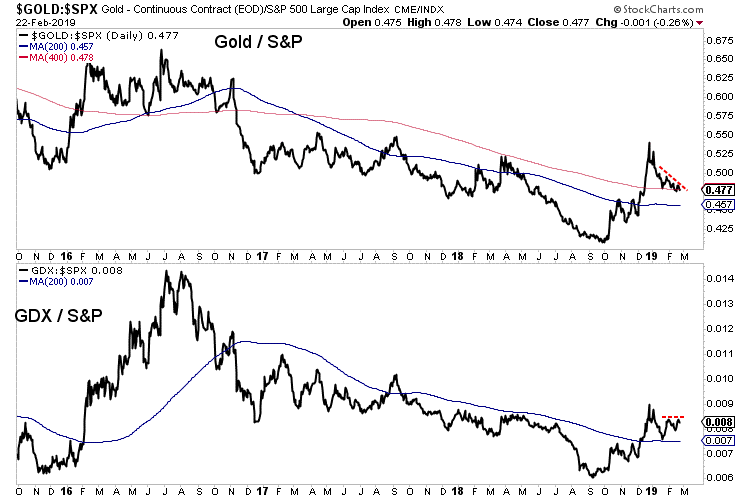

Circling back to the present, the one thing that can prevent Gold from breaking out is renewed underperformance against the stock market. In the chart below we plot Gold and GDX against the S&P 500.

Precious metals stopped outperforming the stock market in late December and the Gold to S&P 500 ratio appears weak and likely to weaken further.

The S&P 500 recently cleared its moving average resistance and its advance decline line hit a new all time high. These things suggest higher prices in the near future and that, rather than bullish sentiment would provide resistance to Gold over the next few months.

Although Gold will not break resistance in that scenario, we should keep an eye on the gold stocks which have shown improving breadth and relative strength. Plenty of great values remain and there is still plenty of time to position yourself to take advantage. If a huge breakout is coming later in the year then the next few months may be your last chance. To learn what stocks we are buying and have 3x to 5x potential consider learning more about our premium service.

- The biggest driver of major markets right now is the possibility of a U.S.-China trade deal.

- On that note, please click here now. The U.S. government’s wild launch of tariff taxes caused global markets to swoon in the first half of 2018. Gold and the Chinese stock market were hurt more than a lot of other markets.

- Gold has done well with QE, QT, falling rates, and rising rates, but tariff taxes hurt the Chinese economy. That put a damper on the growth of Chinese gold demand.

- The Chinese stock market is now rallying in anticipation of a trade deal, but even if there is no deal (unlikely), the Chinese government has embarked on a significant stimulus program.

- U.S. money managers are getting more interested in the Chinese stock market because of that stimulus. A trade deal that includes more intellectual property protection would create a huge U.S. stock market rally. More importantly, it would create a huge rally in the Chinese market and that would increase gold demand significantly.

- If the Fed hikes or signals that QT is going back to auto pilot mode, institutional money managers will buy gold because of growing concerns about the U.S. government’s ability to finance itself, and because the Fed’s move would hurt low interest rate loans for U.S. stock market buybacks. A situation like September 2018 would occur, with gold rallying and stock markets tanking.

- On the other hand, a pause in hikes and an earlier-than-expected end to QT is also viewed as good news for gold.

- Additionally, even without a trade deal, China’s economy is becoming consumer-oriented, and that means more imports and less exports. In turn, that means less need for the purchase of U.S. government debt.

- A trade deal would speed up this process.

- The U.S. government’s ability to finance itself without foreign government purchases of its bonds is becoming a significant concern for powerful money managers like Larry Fink of Blackrock.

- The bottom line: A trade deal is good for stock markets and gold, but it likely flips the U.S. government’s financial situation out of the fry pan… and into the fire!

- Clearly, the current global-macro situation is extremely positive for gold. What about the technical situation? For the answer to that question, please click here now. Double-click to enlarge this daily gold chart.

- It really doesn’t matter whether gold makes a beeline for my new $1400 target immediately, or whether there’s a “pitstop” in the $1300-$1280 support zone.

- It doesn’t matter because the big picture fundamentals and technicals are outrageously positive, so there’s no need for fear amongst investors.

- Please click here now. Double-click to enlarge. The higher-price implications of the technical action on this weekly gold chart are obvious. The $1000/ounce price zone is major support, $2000 is resistance, and $3000 is the target price!

- The world’s need for dollars is declining, for a multitude of reasons. Please click here now. Whether it’s caused by the simple but gargantuan growth of the Chinese and Indian economies, or the U.S. government’s “My way or the highway” approach to sanctioning Russia, bank and government entities around the world are steadily distancing themselves from the dollar.

- Gold is the best way for individuals, banks, and governments to do that. The buy programs of emerging central banks are only in their infancy, and the tonnage being bought is consistently rising.

- As somebody who aggressively bought the U.S. stock market right into the October 2008-March 2009 lows, I can assure the Western gold community that there is no event to fear in the current gold market. The market is rock-solid.

- The rise of the Eastern economies is a titanic force that is creating both de-dollarization and demand growth for gold. Citizens of the East view gold as the best investment asset from both a risk and reward perspective. Their view is now being adopted by more and more Western money managers. In time (and not much time), this positive view of gold will also be the view of the average American citizen. Gold bashers like Warren Buffett prospered in the fiat era, but that era is waning fast. A new bull era is being born and all roads lead to gold.

- Please click here now. Double-click to enlarge this interesting GDX chart. Merger-mania is underway in the gold and silver mining stocks and there’s “bull flag mania” on the daily GDX chart!

- Larger gold mining entities are required to service the global demand growth for gold. I’ve predicted that Chinese miners, banks, and industrial companies will ultimately be involved in mergers with Western mining companies.

- In the coming years, gold miners could become as important as the giant base metal miners.

- Please click here now. Double-click to enlarge. That’s another look at the GDX daily chart, with the support zones highlighted. Mining stock enthusiasts should be buyers of their favourite miners any time GDX trades at a support zone.

- Gold stock investors should understand that the current market is not like the early 2000s, 2007, or 2016. This is a market like the 1970s, and the upside fun… has only just begun!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Gold Stocks Merger Mania!” report. I highlight ten fabulous gold miners that are ripe to be taken over, with key buy and sell points for each stock! Email me today, and I’ll send it to you today!

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Feb 26, 2019

Here are today’s videos and charts (double-click to enlarge):

SFS Key Charts, Signals, & Video Analysis

SF60 Key Charts, Signals, & Video Analysis

SF Trader Key Charts, Signals, & Video Analysis

SFJ Key Charts, Signals, & Video Analysis

Thanks,

Morris Hubbartt

Unique Introduction For Web Readers: Send me an email to signals@superforcesignals.com and I’ll send you my “Hot Off The Press” junior miners free report, and 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

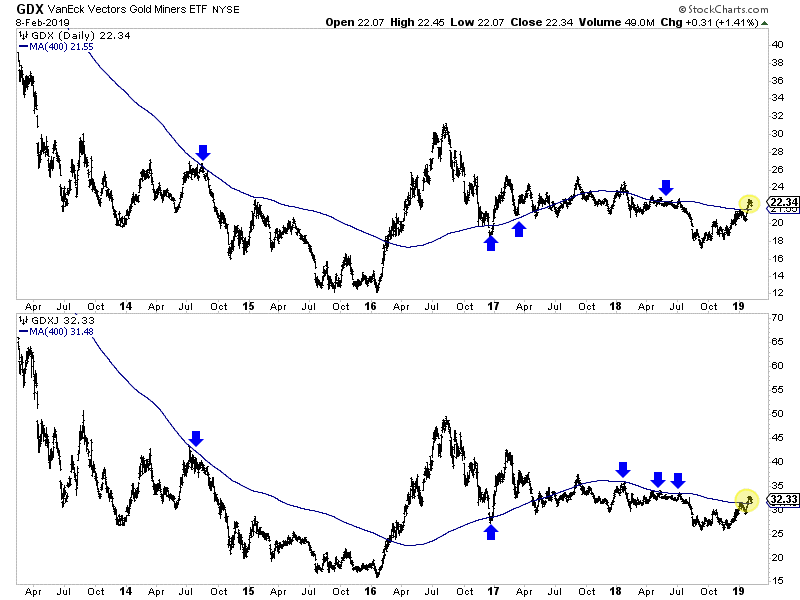

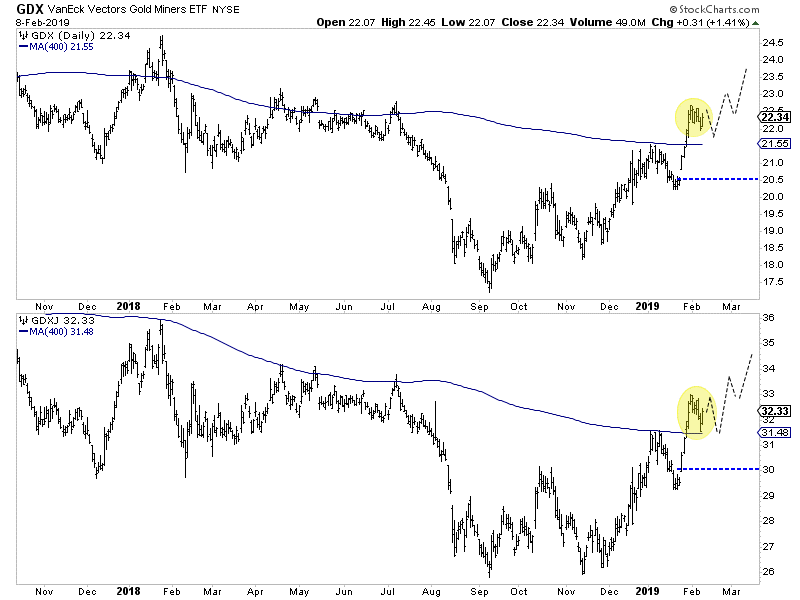

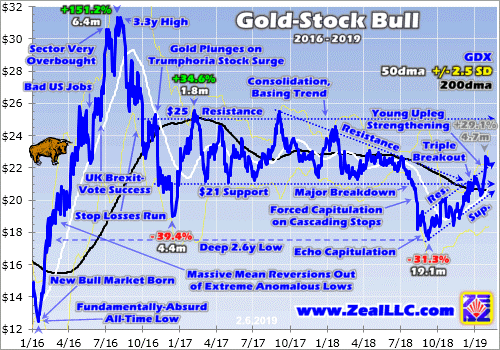

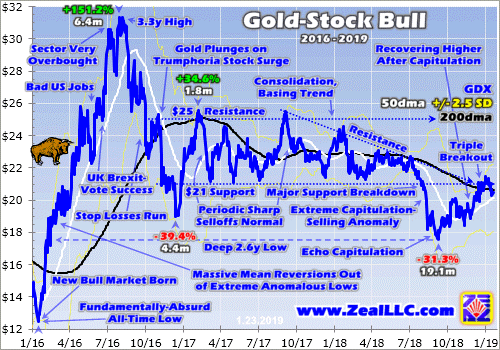

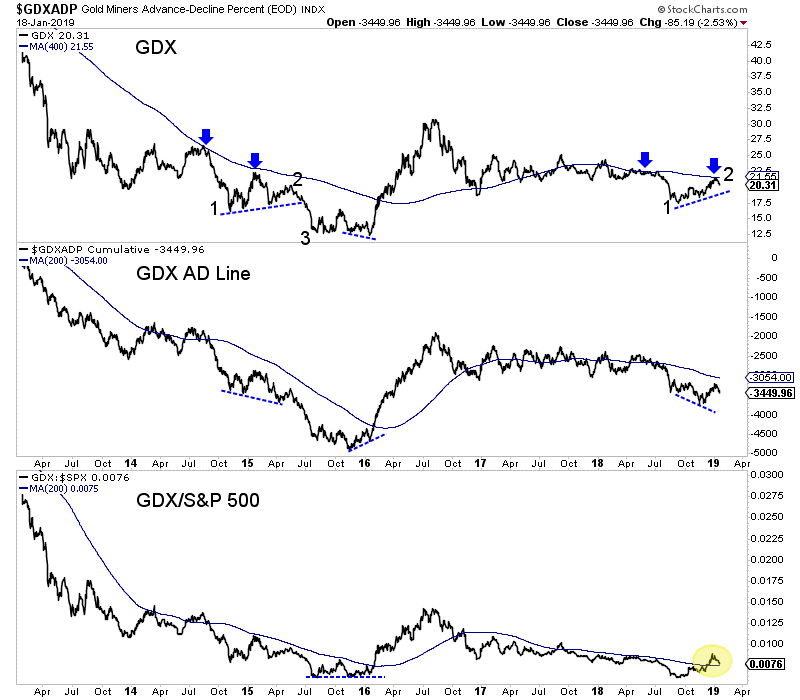

The gold miners’ stocks surged strongly last week, blasting to new upleg highs. The mounting gains are naturally driving more interest in this small contrarian sector, shifting sentiment towards bullish. Despite their accelerating rally, gold stocks still remain fairly low technically and deeply undervalued relative to gold. So their strengthening upleg likely has plenty of room to run considerably higher in coming months.

The gold miners’ stocks are ultimately leveraged plays on gold, which overwhelmingly drives their profits. The much-maligned yellow metal has enjoyed a strong upleg since mid-August, when record gold-futures short selling pounded it to a deep 19.3-month low of $1174. Gold has been gradually powering higher on balance ever since, surging near $1341. That makes for 14.2% gains over 6.1 months, an excellent run.

Gold miners’ earnings are amplifying these higher gold prices, driving this parallel gold-stock upleg. This is readily evident in the most-popular gold-stock benchmark, the GDX VanEck Vectors Gold Miners ETF. Launched back in May 2006, GDX has an insurmountable first-mover lead. This week its net assets of $11.1b were a whopping 50.6x larger than the next-biggest 1x-long major-gold-miners-ETF competitor!

The gold stocks as measured by GDX have certainly capitalized on gold’s advance. Between its own brutal 2.6-year low in early September and this week, GDX has surged 33.0% higher in 5.3 months. That works out to gold stocks leveraging gold’s gains by 2.3x in recent months. That is right in line with the 2x to 3x usually seen historically in the major gold miners. Many smaller gold miners are doing even better.

As this upleg was being born and growing, I wrote multiple essays explaining what was happening and why it was important to get heavily long gold stocks. We filled the trading books in our newsletters with great smaller gold and silver miners with superior fundamentals to the majors. Our unrealized gains this week were already running 60%+ on multiple trades! This young gold-stock upleg is even now quite lucrative.

While it is always better to buy in earlier than later, GDX’s 33.0% upleg to date remains relatively small. In essentially the first half of 2016, GDX soared 151.2% higher in just 6.4 months in its last major upleg! Really-big uplegs are par for the course in the volatile gold-stock sector. Gold stocks’ last secular bull ran from November 2000 to September 2011. Half of that was in the pre-gold-stock-ETF era before GDX’s launch.

During that long 10.8-year span, the classic HUI NYSE Arca Gold BUGS Index skyrocketed an incredible 1664.4% higher! That life-changing secular bull consisted of 12 separate uplegs. One was an anomaly, the mean reversion out of 2008’s first stock panic in a century. Excluding that behemoth, the 11 normal ones averaged hefty gains of 80.7% over 7.9 months. So GDX’s recent run is nothing by this sector’s standards.

At this stage all gold stocks have really done is regain their sharp late-summer losses. This GDX chart over the past few years or so illuminates the gold-stock technicals. The major gold miners’ stocks have merely climbed back up into their multi-year consolidation basing trading range. The lion’s share of this upleg’s gains are most probable as GDX breaks out above longstanding resistance, likely in coming months.

For fully 21.5 months leading into August 2018, GDX consolidated in a well-defined trading range from $21 lower support to $25 upper resistance. That sideways grind bled away bullish psychology, leading many traders to abandon this drifting sector. By late last summer not many were left, and most of them were soon driven out too. August’s extreme record gold-futures short selling spawned a washout in gold stocks.

Because this sector is so volatile, running loose trailing stops is essential for managing risk. The lower gold was hammered, the more selling pressure mounted in its miners. That forced them to stop losses, unleashing more mechanical selling and fueling a vicious circle. Gold stocks cascaded lower in a brutal forced capitulation into mid-August, and a secondary echo capitulation bashed them lower still in early September.

GDX’s $21 support was shattered as this benchmark ETF plunged to $17.57 by mid-September. Several days later I published an essay Gold-Stock Forced Capitulation explaining all this right in those depths of bearish despair. I concluded “…the aftermath of capitulations is exceedingly bullish. … The technicals and sentiment spawned by capitulations are so extreme they usually birth massive uplegs and entire bull markets.”

With GDX just plunging to an extreme and unsustainable 2.6-year low, we were aggressively buying great gold stocks and recommending them to our newsletter subscribers. Being bullish when everyone else was bearish was the right call of course. The gold stocks started powering higher in their upleg persisting to today. I did my best to let speculators and investors know about the great upside opportunities in this sector.

Since that forced-capitulation essay, I’ve published 23 more weekly essays on subsequent Fridays. Fully 14 of those were about gold stocks, exploring their deep undervaluation relative to gold, their excellent technicals, and strong fundamentals. If you want to multiply your wealth in the stock markets, you have to pay attention all the time. Most traders make the costly mistake of ignoring sectors until they get exciting.

I’ve been trading stocks for over three decades now, and doing it full-time professionally to earn a living for two-thirds of that long span. One of the most-important lessons I’ve learned is it’s critical to always keep plugged in. If you are not following the markets, you are missing great opportunities. The only way to buy low before later selling high is staying abreast of beaten-down sectors, especially when they are despised.

The gold stocks kept marching higher on balance after that anomalous forced capitulation, carving higher lows and higher highs. In mid-October with GDX under $19 I explained why gold stocks were Stocks’ Last Cheap Sector. I concluded, “These gold miners’ stock prices are wildly undervalued relative to the metal which drives their profits. So they are overdue for a massive mean reversion and eventually overshoot.”

This new gold-stock upleg mostly drifted sideways in November, discouraging even early contrarians. I did my usual quarterly analyses of the newest Q3’18 results of the major gold miners of GDX and mid-tier gold miners of the GDXJ Van Eck Vectors Junior Gold Miners ETF. This critical fundamental homework proved “…the major gold miners’ fundamentals remain far stronger than implied by their left-for-dead stock prices.”

While few traders cared about gold stocks in this upleg’s initial few months, December’s action started to change that. Gold surged 4.9% higher to $1282 that month as the US stock markets rolled over into a severe near-bear correction. Down 19.8% at worst since its late-September peak, the flagship S&P 500 broad-market stock index plunged 9.2% in its worst December since 1931 in the midst of the Great Depression!

The gold miners’ stocks ignored the burning stock markets to follow gold higher and leverage its gains like usual. GDX blasted up 10.5% that month, amplifying gold’s strong advance by a solid 2.1x! Finally this young gold-stock upleg was getting big enough to attract traders’ attention. I continued to do my best to spread awareness, writing about an imminent Gold-Stock Triple Breakout in mid-December with GDX near $20.

This leading gold-stock benchmark was on the verge of breaking out above three major upper-resistance zones simultaneously. These included the old $21 support of its consolidation basing trend, a downward-sloping resistance line from a bearish descending-triangle technical pattern, and most importantly GDX’s key 200-day moving average. Gold stocks’ improving technicals were on the verge of getting far more bullish.

I concluded, “Three major GDX resistance zones have converged just above current levels. Once the gold stocks surge decisively over, the technically-oriented traders will take notice. They will likely start chasing the momentum accelerating the gains, with buying begetting buying.” That indeed came to pass. By early January that super-bullish upside triple breakout in GDX had already become a fait accompli.

I wrote another essay Gold-Stock Upleg Breaking Out to explain the huge upside potential the gold stocks had after clearing those essential technical hurdles. I concluded this gold-stock upleg “is now surging in a major upside breakout that should unleash a flood of new buying. With gold climbing on balance too, everything is in place to fuel a major gold-stock upleg.” There were many opportunities to buy gold stocks low.

January was a roller-coaster month for gold stocks, with GDX rallying then swooning then surging to big new upleg highs at month-end. But on balance this leading gold-stock benchmark continued carving both higher lows and higher highs. In late January I explained why Gold-Stock Upleg Pauses were nothing to worry about. All major uplegs flow and ebb, surging two steps forward before slumping one step back.

Speculators and investors needed to remember that “Uplegs don’t shoot higher in straight lines, pullbacks within them are normal and expected. They serve to rebalance sentiment keeping uplegs healthy.” Then in early February GDX flashed one of the most-powerful buy signals of all, the fabled Golden Cross. That is when its 50dma crosses back above its 200dma soon after a major secular low in GDX, a wildly-bullish omen.

But gold stocks again retreated in early February after surging in late January, again worrying traders who lacked perspective. So a couple weeks ago with GDX just over $22, I published another essay showing Gold Stocks Gather Steam. It explained that rare Golden Cross buy signal and concluded, “All this has really started to shift sentiment back to bullish, which will attract in lots more capital to chase the momentum.”

That indeed proved correct again. The more you study markets, the deeper you understand them and the more sense their seemingly-capricious rhythms make. The more your market experience and knowledge grow, the higher the odds you can figure out what’s most likely next. If you aren’t in a position to watch markets full-time for decades, it’s essential to spend a little time and money to learn from someone who is and has.

I started investing in stocks when I was 12 years old, using money earned from summer jobs. I had very little market knowledge in those early years. So I subscribed to a few financial newsletters written by market experts with vastly more experience and wisdom than me. Their hard-earned insights from long decades of study kept me on the right track to gradually grow my meager capital at the time. I loved those guys!

Universally in life, the more time anyone spends doing anything the better they get at it. Success is often directly proportional to time on task. So if you can’t or don’t want to devote your life to trading, you need to diligently and consistently learn from those who have. Being right on this gold-stock upleg is no big deal, as it’s been garden-variety and in line with precedent so far. It has been both predictable and gameable.

After drifting lower in the first half of February, GDX started surging again late last week. Heading into last weekend the major gold stocks enjoyed solid 1.0% and 1.3% daily rallies per this ETF. Those were directly driven by gold climbing 0.5% and 0.7% after slumping to its own mid-month lows. While US stock markets were closed Monday, that gold-stocks-rallying-and-amplifying-gold trend really accelerated on Tuesday.

After edging up to a new upleg high last Friday, gold continued climbing modestly in foreign trading over the long weekend in the U.S. By Tuesday morning gold-futures speculators were seeing gold at its best levels in 10.1 months. So they apparently rushed to buy, catapulting gold 1.5% higher to $1341! GDX surged 3.2% that day, leveraging gold’s advance by 2.1x. That momentum drove another 1.0% rally Wednesday.

But despite the major gold stocks climbing 33.0% in 5.3 months as of the middle of this week, they remain fairly low technically. At $23.36, GDX was merely back up to the middle of its old multi-year consolidation basing trend between $21 to $25. Traders aren’t going to get really excited until GDX powers decisively above $25 for the first time since mid-2016. While improving, gold-stock psychology is still relatively bearish.

I suspect GDX will challenge $25 in the next few months. Though this sector often experiences a seasonal lull into mid-March, gold stocks then enjoy a strong spring rally. As long as gold continues slowly climbing on balance, the gold stocks have excellent upside potential. Remember GDX’s last major upleg soared 151.2% in essentially the first half of 2016, and the prior secular gold-stock bull’s uplegs averaged +80.7%!

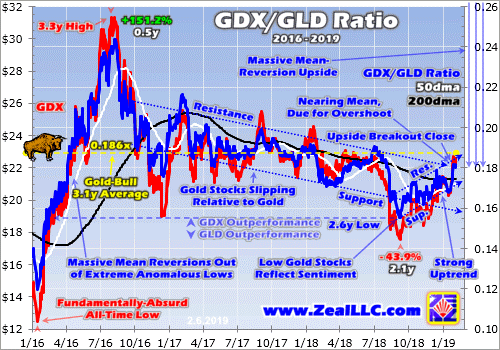

While the major gold miners’ technicals and sentiment both support bigger gains to come, perhaps the most-bullish argument of all comes from the fundamental side. The gold stocks remain relatively low compared to prevailing gold prices, the metal which directly drives their profits. They need to mean revert much higher to regain normal levels compared to gold. A simple ratio of gold stocks to gold illustrates this.

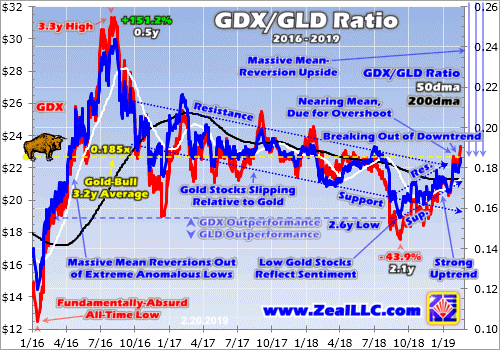

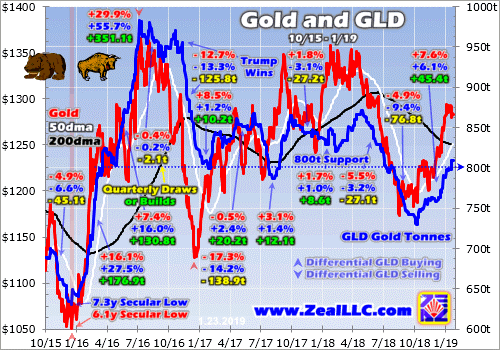

The GLD SPDR Gold Shares is the world’s dominant gold ETF. Dividing GDX’s daily close by GLD’s daily close yields the GDX/GLD Ratio, a great fundamental proxy for gold-stock valuations. Hammered to the low side by gold stocks’ late-summer forced capitulation, the GGR is just now regaining average levels for recent years’ gold bull. But mean reversions rarely stop at the averages, instead overshooting proportionally.

I explained this chart in depth a couple weeks ago in another essay, so just a brief update today. This Wednesday the GGR clawed back up to 0.185x, which is exactly at the 3.2-year average since today’s gold bull was born in mid-December 2015. At worst in mid-September, the GGR plunged to a deep 2.6-year secular low of 0.155x. That was 0.030x under this bull’s mean, portending a proportional overshoot higher.

Before this gold-stock upleg gives up its ghost, the odds really favor the GGR surging back to 0.215x. At this week’s gold-upleg-to-date high of $126.70 in GLD, that implies GDX near $27.25. That would be a powerful breakout above that old $25 consolidation-trend resistance line, and would catalyze a lot more trader interest in this small sector! It would extend this current gold-stock upleg’s gains to a more-normal 55.1%.

But if gold keeps rallying like it ought to as these overvalued and overbought US stock markets roll over again, the potential gold-stock upside is far greater. $1400 gold is just 4.4% above this week’s levels, not a stretch at all. That would be a new bull-market high exceeding July 2016’s $1365, generating serious excitement to attract in new traders. At a proportional-overshoot 0.215x GGR, that leaves GDX near $28.50.

That’s still not particularly high, as GDX traded over $31.25 in early August 2016 in its own gold-bull-to-date peak. With speculators and investors actually excited about gold stocks then, the GGR hit 0.244x. Apply that to $1400 gold, and the GDX target climbs above $32.25. That would grow this upleg to +84%, right in line with the prior secular bull’s average. Make no mistake, the gold-stock upside from here is still big!

And that’s just this upleg, not the entire gold-stock bull. In the 2 years before 2008’s stock panic radically changed the markets, the GGR averaged 0.591x. In the 2 years after of 2009 and 2010, the GGR was still far higher than recent levels averaging 0.422x. Plug in the much-higher historical GGRs seen when gold stocks were far more popular, and higher gold prices, and GDX’s potential upside in this bull gets huge.

The best gains in today’s mounting gold-stock upleg are likely still yet to come. While you can play it in GDX, the major gold miners dominating this ETF are really struggling to grow their production. And that problem is even worse in the newly-merged super-majors, further retarding GDX’s performance. So the best gains will be won in smaller gold miners with superior fundamentals that are still expanding their outputs.

The earlier you get deployed, the greater your gains will be. That’s why the trading books in our popular weekly and monthly newsletters are currently full of better gold and silver miners mostly added in recent months. The gains we won in 2016 were amazing the last time American stock investors returned to gold. Our newsletter stock trades that year averaged +111.0% and +89.7% annualized realized gains respectively!

Coming gold-stock gains should be similarly huge as today’s strengthening gold and gold-stock uplegs grow. To multiply your wealth in the stock markets you have to do your homework and stay abreast, which our newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. You can subscribe today for just $12 per issue! That’s a trivial pittance for decades of hard-won market experience, knowledge, wisdom, and ongoing research.

The bottom line is gold stocks just surged higher again, their upleg getting stronger on balance. GDX continues to carve higher lows and higher highs, fueling improving sentiment. More traders are getting interested in this sector and bringing in more capital, driving gold stocks higher to strengthen a virtuous circle of buying. Gold-stock technicals, sentiment, and fundamentals all argue for bigger gains to come.

This current upleg remains relatively small by sector precedent. And gold stocks are just regaining their bull-average levels relative to gold, with lots of room to rally on a proportional mean overshoot. While a seasonal lull nears, mid-upleg pullbacks or consolidating drifts are normal and healthy. This gold-stock upleg is likely to grow a heck of a lot bigger in coming months’ major spring rally. Get deployed if you aren’t yet!

Adam Hamilton, CPA

February 25, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Galway Metals (GWM.V, GAYMF) is a Canadian exploration stock with two prospective projects located in strategic locations. Fundamentally, some things stand out.

1. Insiders

Over 30% of outstanding shares are in the hands of management and insiders. High quality management as both CEO and Chief Geo come from Kirkland Lake Gold (KL.TO) where they also held management positions. Another reputable insider is Wesdome’s (WDO.TO) CEO Duncan Middlemiss, who has an advising role at Galway Metals. Connections like these could be important in a later stage should

exploration continue in the current direction.

In the past year, 5 insiders have been buying their own stock, of which CEO Robert Hinchcliffe invested the highest amount. Through 2018, he bought $285,000 worth of stock in the open market and another $100,000 in a private placement. Other insiders put in between $25,000 and $88,000 of their own money into Galway Metals.

Insiders are dedicated as well. When looking at their personal holdings, the biggest part of this is held in GWM shares. Data like this can be retrieved on marketscreener.com. Management in this business usually has seats on more than one company’s board, which means they hold more than just one stock. Therefore, it’s interesting to see the weight of these. Allocations at Galway Metals show conviction: CEO 89%, VP 73%

and Chief Geo 47%.

2. History

Galway Metals was spun out of the Galway Resources takeover by AUX in 2012. At the time, Galway Resources was sold for $340M. Management is largely the same since then, so they’re experienced in growing an exploration stage company to one that’s prepared for production. Galway Resources (GWY) shareholders received a 47% premium in that deal.

3. Projects

Galway Metals has 2 projects in Eastern Canada in mine friendly jurisdictions in areas where infrastructure such as roads, railways and mills are closeby. Both projects have an existing resource for both gold and industrial metals. One million ounces of gold have been mapped to date and if we add the other metals, there’s 1.8 million gold equivalent ounces. These past years there has been a resource upgrade yearly, and this year as well, they will upgrade their existing resources on both projects

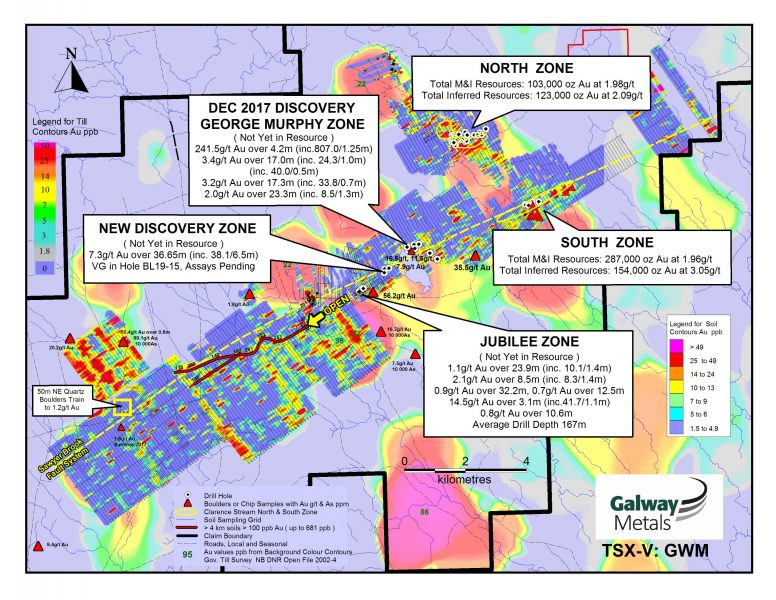

Clarence Stream

Located in mining friendly New Brunswick and in the proximity of a processing mill and (rail)roads nearby. Management hints that this project can represent a new gold district in Canada. Findings to date continue to prove this out: This project has 5 discovered zones thus

far on the main NE-SW trend with high possibility for new discoveries going by soil anomalies. Galway just announced assays from their fifth and new discovered zone: 7.3g/t over 36.7m (38.1g/t over 6.5m). A 50m stepout has been drilled which intersected visual gold twice. Results from this are pending.

This new discovery is in the middle of two known zones (Jubilee and George Murphy) that are 2km apart. Galway controls 65km of this main NE-SW trend and management believes this shares the same structure and has similar geology as Marathon’s (MOZ.TO) Valentine Lake project. Only 5km have been drilled and all zones are open in every direction. Wide mineralization at shallow depths with grades which would make this suitable for open pit mining.

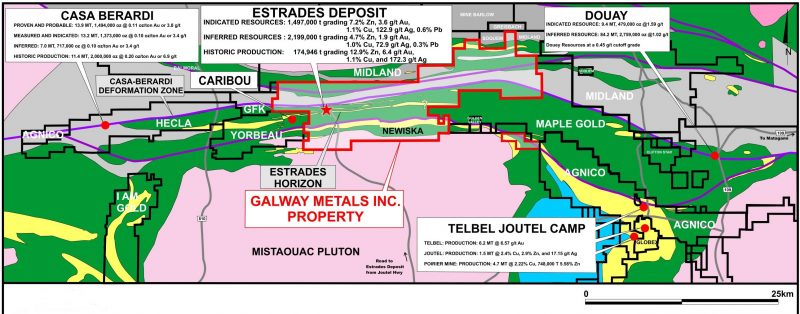

Estrades

Polymetallic project that saw production in 1990-1991:174,946 tonnes grading 6.4 g/t Au, 172.3 g/t Ag, 12.9% Zn and 1.1% Cu. Previous owner stopped production when metals prices dropped in 1991. Since then this former mine has been dormant for over 25 years. Located in mining friendly Québec with multiple deposits, active and historic mines in

the proximity. 31km of strike hosting 3 mineralized trends which hold a resource that’s high in Zinc (20.75% ZnEq) and Gold (11.28g/t AuEq).

Just like the Clarence Stream project, this is currently being drilled so news from here should flow in coming weeks.

4. Cashed up

All that drilling costs money. Therefore, it’s interesting to know that Galway has about $7M in the bank after a recently closed private placement (in which 4 insiders participated), which means they can continue this aggressive exploration. Galway Metals doesn’t have any debt. Also of importance is that chief geo and vice president bought warrants with an execution price of $0.50, which -when executed- will add $750,000 to the treasury.

5. Catalysts 2019

Two catalysts this year for a revaluation. Catalyst # 1: Exploration success and new discoveries on Clarence Stream and Estrades. On Clarence stream, investors have a couple of pending results to look

forward to from drill cores that showed visual gold as well as future step-out holes from current zones. Catalyst # 2: Resource upgrade 2019 including the new zones. Management pointed at a resource upgrade this year that will – for the first time- include 2 new zones at Clarence Stream.

6. Comparables and valuation

When looking at other Eastern Canadian companies that share this continent scale trend, it’s easy to see their Clarence Stream project is favourably located in between known multi million ounce gold camps.

Similarities with Oceanagold’s Haile mine, which is an open pit mine that shares shallow depth in combination with high grades. Another similar case is Atlantic Gold over in Nova Scotia. This has the same

widespread gold occurrences on their property and built a central processing facility that’s currently being fed by the surrounding deposits.

Galway is not yet at this stage and management may not have the intention to mine it themselves. Just going by similar geological features and challenges, it’s positive to see nearby succeeded projects.

As valuation goes, when looking at the only metric we can currently apply – which is the enterprise value on a proven gold ounce basis- we’re sitting at $17.4/oz whereas this sector’s (pre feasibility) average is $52/oz. Noteworthy that this number is based on the current resource, that only holds 2 of the 5 zones at Clarence Stream.

7. In Closing

As said in the intro, Galway has a lot going for it. Two catalysts this year that will continue to get fed from multiple fronts. Galway has a rather tight share float (107M) and they don’t need to collect funds any

time soon, meaning that their share price will benefit with a leverage effect when exploration continues to deliver. Management is experienced, respected, committed and on the buying side. Not to be taken for granted in any sector. Eastern Canadian gold deposits are on the rise and going by the fundamentals there’s good potential that this too will turn out to be a multi million ounce deposit, eyed by producing mining companies. Going by the EV/oz metric, there should be plenty of room for upside.

Jonas De Roose

February 22, 2019

Author Jonas De Roose is a Belgian retail investor in precious and base metals stocks with a drive for research and learning. He has a background in business development and marketing. He owns shares in Galway Metals and his article is not intended as investment advice. This article is based on his findings and based on his personal opinion. If you have suggestions regarding this company feel free to contact him at jonasderoose@hotmail.com.

- As U.S. markets re-open after the holiday, the world’s “queen of assets” continues her glorious ascent to higher prices. Please click here now. Double-click to enlarge this magnificent short term gold chart.

- The rise above $1332 ushers in my new short-term target: $1355!

- Please click here now. Gold is well on its way to becoming a mainstream asset like stocks and bonds.

- The reason for that is the “citizen wealth effect” created by the relentless rise of China and India. These gold-oriented nations are well on their way to becoming the most gargantuan economic empires in the history of the world.

- It’s simple mathematics: There are eight Chindians for every American, and about half of the Chindians are under the age of 35.

- It’s an unstoppable force that I refer to as, “The Gold Bull Era”.

- In the West, gold has been traditionally bought only when major stock, bond, currency, and real estate markets get into trouble.

- In contrast, Chindian citizens view gold as the “ultimate asset”, meaning they buy it in both good times and bad.

- This view is beginning to gain acceptance amongst Western analysts and money managers and I’m predicting it will continue to do so for many decades.

- Gold’s role as ultimate asset was showcased in the September-December period when it rose while U.S. stock markets tumbled.

- Most gold bugs were stunned by the incredible price action, and even more stunned as the GDX gold stocks ETF soared too!

- Now, gold is rallying while U.S. stock markets rise, and most analysts are again somewhat shocked as their attempted top calls for gold fail repeatedly.

- This type of “win-win” price action is unique to gold and I’ll boldly state that it is essentially here to stay!

- Please click here now. Double-click to enlarge. On this daily chart, gold looks like a freight train that cannot be stopped.

- From a big picture technical perspective, this type of daily chart action is expected and normal. To understand why I say that, please click here now. Double-click to enlarge what I consider to be the greatest weekly chart in the history of markets.

- Gold appears to be rallying from the final right shoulder in a multi-shouldered inverse H&S bull continuation pattern. Incredibly, that pattern itself appears to be just the head of a much more gargantuan pattern with a target price of $3000!

- In this situation, the current “freight train” technical action being showcased by gold on the daily chart is perfectly normal.

- Please click here now. Double-click to enlarge this key GDX daily chart. A spectacular bull flag breakout occurred on Friday.

- In pre-market action this morning, the price is gapping higher.

- Please click here now. Double-click to enlarge. That’s another look at GDX on a short-term chart.

- With the bull flag breakout now in play, stop-loss enthusiasts can now raise their protective profit-locks from $20.10 to $21.75.

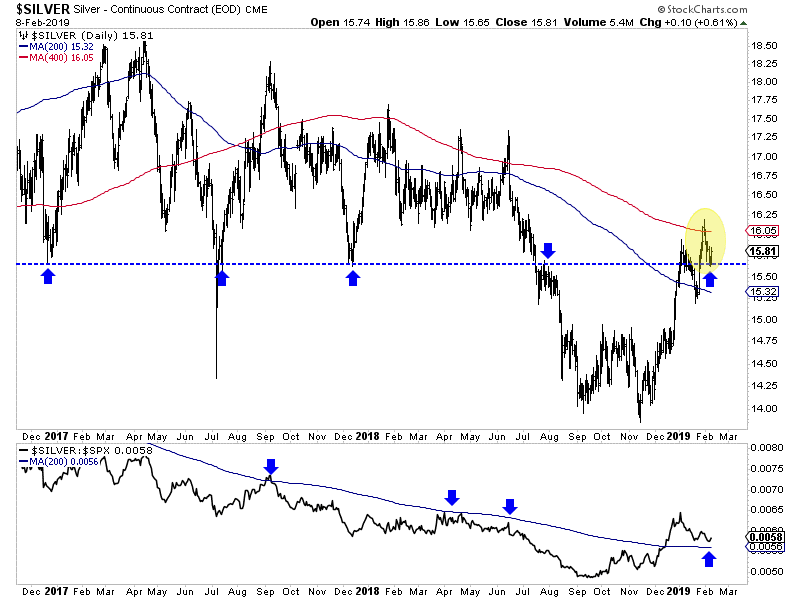

- Please click here now. Double-click to enlarge this silver stocks ETF chart.

- A classic staircase chart pattern is developing. Traders can raise protective stop-loss orders from $24 to $26.

- I recommend that all investors carry some silver and associated miners in their portfolios and the $26 stop-loss level for SIL-NYSE allows investors to board this precious metals “freight train” with minimal risk and maximum potential reward!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Golden Cogs In The Bull Era Wheel!” report. I highlight six of the hottest mining stocks in the world that are poised to lead the sector in 2019, with pinpoint tactics to help traders and investors get richer!

Thanks!!

Stewart Thomson

Graceland Updates

Email:

Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

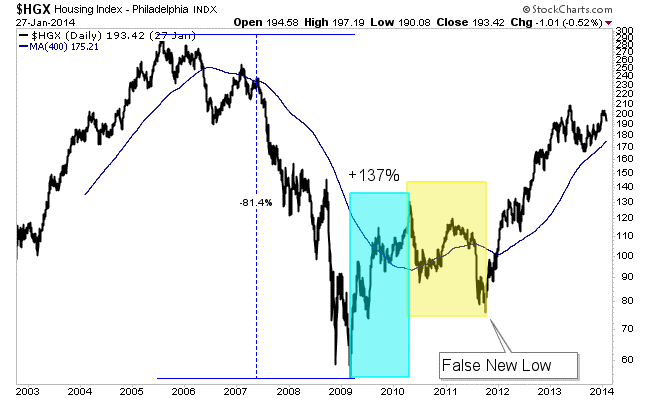

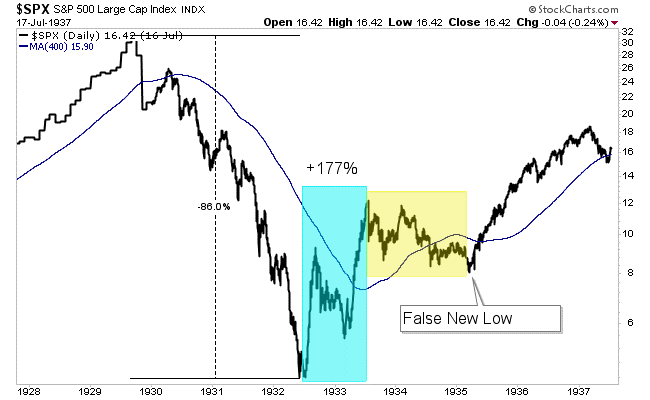

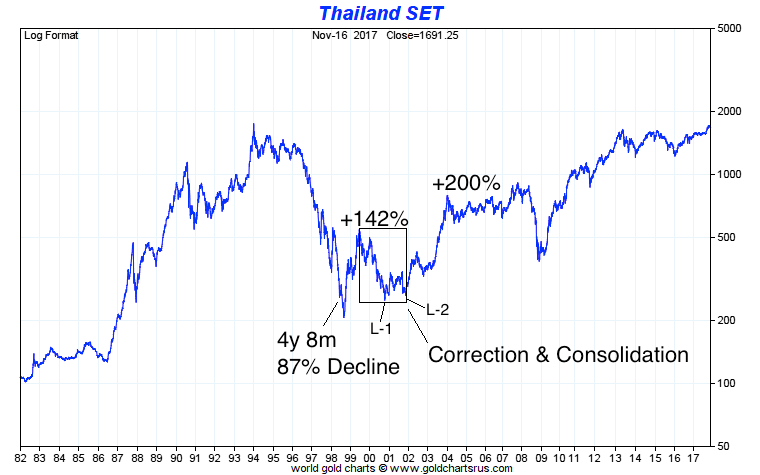

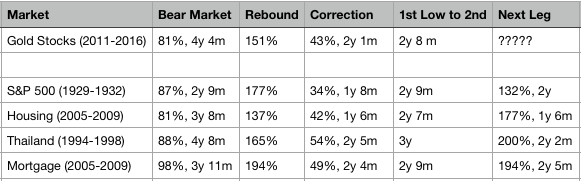

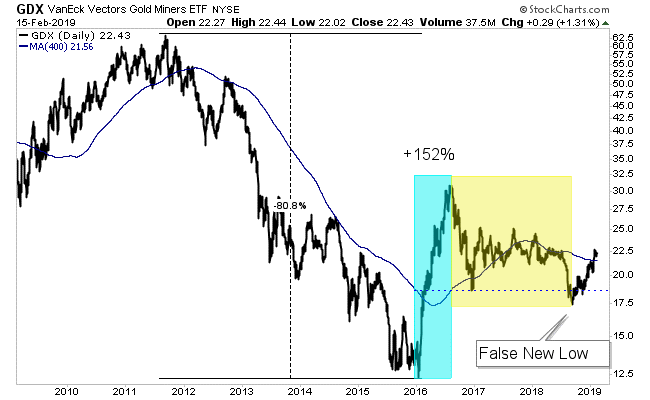

Roughly one year ago and prior to that we observed that the gold stocks could be following the recovery template from what we deemed a “mega bear market.”

We define that as a bear market that is over two and a half years in time and over 80% in price. It cuts both ways.

The gold stocks from 2011 to January 2016 had declined more than 80% and for more than four years. It was a textbook mega bear market.

The sharp recovery in 2016 quickly faded and left us wondering if there was a historical comparison.

Turns out, there are three strong and relevant comparisons.

The housing sector declined 81% from its peak in 2005 to the market bottom in March 2009. Then it rebounded 137% before correcting 42% over 18 months. The correction ended with a false new low.

The S&P 500 crashed nearly 90% over a nearly three year period. Then it rebounded 177% before correcting for 20 months. That correction also ended in a false new low.

Thailand from 1994 through 2000 is quite similar to the gold stocks from 2011 through 2016. Before its 200% move higher from 2002 through 2003, Thailand corrected 54% over a 2-year and 5-month period.

Note that its final low at the end of 2001 could have been a false new low if not for the initial sharp correction down to L1.

The template for a recovery from a mega bear market is as follows.

Following the bear market low, a sharp rally begins that lasts only six to twelve months. Then the market endures a significant correction that lasts a minimum of 18 months and ends with a breakdown to new lows (which ends up being a false move).

Then the major wave higher begins.

Here is the data on those three examples, another one (Mortgage sector) and the gold stocks (GDX).

Note how the time between the bear market bottom and the correction low (for the gold stocks) is almost identical to three of the four examples. Also, note how the second leg higher surpassed the initial rebound in each example (ex S&P 500).

Here is how GDX stacks up (visually) with the others. Its rebound (and potentially second leg higher) began after the false breakdown in September.

Last week we asked the question whether gold stocks would correct or consolidate in a bullish fashion. The evidence now favors a bullish consolidation. As a result, we are looking at potential near-term upside targets of $1350-$1360 for Gold, $25 for GDX and $37 for GDXJ.

The short-term trend is healthy and this historical comparison is table-pounding bullish. We’ve been increasing our exposure and will continue to do so. Plenty of great values remain and there is time to position yourself to take advantage. To learn what stocks we are buying and think have 3x to 5x potential consider learning more about our premium service.

February 20, 2019

by Jordan Roy-Byrne

The world’s two biggest gold miners both announced mega-mergers over the past 5 months or so. These huge deals briefly garnered some interest in the usually-forgotten gold-stock sector, and fleeting praise from Wall Street analysts. But gold-stock mega-mergers are bad news for gold-miner shareholders on all sides. They reveal the serious struggles of major gold miners, and really retard future upside in their stocks.

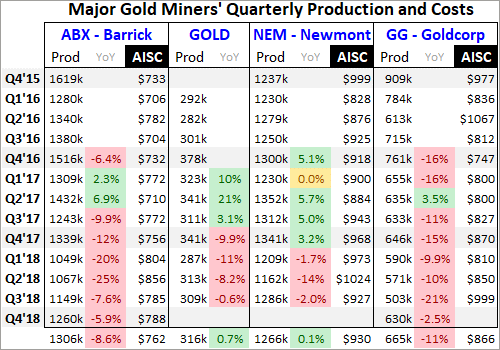

For decades the largest gold miners in the world have been Newmont Mining (NEM) and Barrick Gold (ABX). These behemoths have long dwarfed all their peers in operational scope. While the gold miners are in the process of reporting Q4’18 results now, their latest complete set remains Q3’18’s. As after every quarterly earnings season, I analyzed them in depth for the major gold miners of GDX back in mid-November.

The GDX VanEck Vectors Gold Miners ETF is the world’s leading and dominant gold-stock investment vehicle. In Q3 alone NEM and ABX mined a staggering 1286k and 1149k ounces of gold! To put this in perspective, the average of the next 8 largest gold miners rounding out the top 10 was just 508k ounces. Newmont and Barrick have long been in a league of their own, with commensurate market capitalizations.

In mid-November NEM and ABX were worth $17.1b and $14.9b, granting them massive 11.0% and 9.5% weightings within GDX. These two gold giants alone accounted for over 1/5th of GDX! That gives them outsized influence in not only that ETF, but in the entire gold-stock sector. GDX is the sector benchmark of choice for gold stocks these days, so the fortunes of NEM and ABX stocks really affect overall performance.

Gold-mining stocks are generally divided into three tiers based on their production. Anything over 1000k ounces annually is considered a major, which works out to 250k per quarter. NEM and ABX produced so much gold in Q3 they exceeded this threshold by a colossal 5.1x and 4.6x! They are really super-majors. Mid-tier gold miners produce between 300k to 1000k ounces every year, while juniors are under 300k.

Back on September 24th, 2018, Barrick Gold shocked the gold-stock world. It announced it was merging with Randgold (GOLD), which was really an all-stock acquisition of GOLD by ABX worth $6.5b. Barrick shareholders would own 2/3rds of the new combined company, while Randgold’s would own the rest. To avoid confusion, this essay uses the classic ABX and GOLD stock symbols to represent Barrick and Randgold.

ABX had been Barrick’s ticker for decades, but was just recently abandoned on January 2nd. With this mega-merger finished, the new company took over the excellent GOLD symbol going forward. That is a wise decision, as anyone who types “gold” into any brokerage account will see Barrick Gold. Years ago before Randgold got that coveted symbol, another major miner had it and really seemed to benefit from it.

In Q3 Randgold was the 10th-largest gold miner in the world producing 309k ounces. Added on top of Barrick’s 1149k, the new combined 1458k would take back the top-gold-miner crown from Newmont which produced 1286k that quarter. Apparently size matters a lot when you’re a gold-mining executive. But with both ABX and GOLD suffering chronic declining production, that mega-merger reeked of desperation.

Newmont’s leadership wasn’t happy with losing the pole position among global gold miners. So it soon got to work on looking for a mega-merger of its own. On January 14th, NEM announced it was acquiring major miner Goldcorp (GG) in an all-stock deal worth $10.0b! That looked like one-upmanship taking it to Barrick. NEM and GG shareholders would own about 2/3rds and 1/3rd of the new combined colossus.

Goldcorp was the world’s 7th-largest gold miner in Q3’18, producing 503k ounces of gold. Added on to Newmont’s 1286k, that creates a new monster running at an unprecedented 1789k-ounce quarterly rate! If bigger is better, these new combined super-major gold miners ought to be the best seen in history. But unfortunately in gold mining that isn’t true, and these new giants will likely fare worse than if they hadn’t merged.

In their merger announcements, the CEOs of all 4 of these major gold miners tried hard to sell their deals as wonderful news for shareholders. They argued that synergies and cost savings would make these new combined titans more effective at producing superior returns for their shareholders going forward. And as always with any large merger, Wall Street analysts universally applauded these mega-mergers as good.

Sadly the opposite is likely true, these deals are bad news for all the owners of Newmont and Barrick as well as former owners of Goldcorp and Randgold. These new giant super-majors are even bad news for the gold-mining sector as a whole. The odds are really high that their stocks will really underperform the smaller major, mid-tier, and junior gold miners in coming years. That will hurt this entire sector on multiple fronts.

Contrary to their CEOs’ marketing propaganda, none of these four major gold miners approached these deals from positions of strength. They’ve all been struggling with weakening production and rising costs. Gold mines are wasting assets that are constantly depleting, and it is increasingly challenging to find new gold to mine economically at the scale and pace the majors need. These mergers didn’t solve that core problem!

This table looks at the quarterly production, its year-over-year change, and all-in sustaining costs per ounce mined of Barrick, Randgold, Newmont, and Goldcorp during today’s secular gold bull. It started in late Q4’15 out of deep 6.1-year secular lows in gold. Barrick deleted Randgold’s old website, so there is no Q4’15 GOLD data. And as of Wednesday afternoon NEM and GG hadn’t yet reported full Q4’18 results.

Barrick and Newmont didn’t just effectively dilute their shareholders by 50% for some relatively-meager cost-saving synergies, but because they can’t grow their production internally. ABX’s gold mined each quarter has been falling sharply on balance for years! It has seen brutal YoY drops as high as 25.5%, which ought to be impossible for a world-class gold major. 7 of the last 9 quarters have seen big declines.

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses.

And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost for its first four quarters as a merged company, and then waning production will again be unmasked.

While the new giant Barrick will have more capital to develop new gold mines and expand existing ones, it seems unlikely that will be enough to turn this super-major around. Barrick and Randgold operated about 12 and 4 gold mines respectively pre-merger. So bringing another few online in coming years might not move the needle enough to outpace depletion. And it takes over a decade to permit and build new mines.

The entire gold-mining industry has been greatly starved of capital largely since 2013, with 2016 being a modest exception. Thus the big investments necessary to find new large-scale gold deposits and slowly advance them to mine builds have been severely lacking. So this whole industry’s pipeline of new gold to mine has been crippled, all but pinched shut. Declining miners merging does little to solve this problem.

Newmont has fared way better than Barrick in recent years, actually enjoying strong production growth on balance from Q4’16 to Q4’17. But this past year even mighty NEM has started to suffer from waning gold production. It averaged 5.9% YoY declines in the first three quarters of 2018. I suspect NEM is just a little behind ABX in rolling over into depletion outpacing mining growth. ABX’s merger forced NEM to act.

While Goldcorp was long celebrated as the world’s best major gold miner, it has been struggling for years with slowing production. Over the last 9 quarters GG only saw one modest production gain, with its gold mined dropping a colossal 11.0% YoY each quarter on average! So although GG produces about twice as much gold as Randgold, it might be a worse acquisition target due to its faster pace of shrinking production.

Like ABX and GOLD, it’s hard to imagine combining two more weakening majors NEM and GG will yield a way to stop and reverse their falling production. Again for their first four quarters together this new giant Newmont will appear to see big annual production growth. But once that post-merger comparison rolls past, the declining gold across all its mines will again be revealed. Mega-mergers can’t negate mine depletion.

Randgold didn’t even bother reporting industry-standard all-in sustaining costs, which is why they’re not included above. But its cash costs were often on the high side, so it’s likely the new combined company will drag overall mining costs higher. Barrick’s major-leading low AISCs aren’t likely to last with GOLD’s mines thrown in the mix, which means higher costs and lower overall profitability for Barrick going forward.

Newmont should benefit more from Goldcorp’s lower cost structure. NEM averaged $975 AISCs in the first three quarters of 2018, way higher than the $877 average in Q3’18 among the GDX gold miners. GG’s AISCs averaged $886 over that 9-month span, so the new combined Newmont should benefit from lower costs. But that may not last long, as weakening production eventually pushes per-ounce costs higher.

Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. So slowing production yields fewer ounces to spread mining’s big fixed costs across. If these new super-major gold behemoths can’t arrest their depleting production, their costs will inevitably rise in the future hurting profitability. Again these mega-mergers didn’t solve that problem.

So it looks like the managements of Barrick and Newmont just issued $6.5b and $10.0b of new stock so they could report big merger-driven production surges for a single year! Once those pre- and post-merger year-over-year comparisons pass, the vexing waning-production problems at all four of these predecessor gold miners will again become apparent. But that’s not even the biggest reason these mergers are bad news!

Even before these mergers as apparent in mid-November when I analyzed Q3’18 results, both Newmont and Barrick already had very-large market capitalizations of $17.1b and $14.9b. That again granted them massive 11.0% and 9.5% weightings in GDX. Like most stock indexes and ETFs, GDX’s components are weighted by market cap. Goldcorp and Randgold ranked 6th and 7th then in market cap and weightings.

Adding NEM and GG together as of mid-November would catapult their market cap and GDX weighting to $25.1b and 16.0%. Adding ABX and GOLD together yields a similar $22.3b market cap and 14.5% total GDX weighting. So these two super-majors alone could account for a crazy 30.5% of GDX’s weighting! That is almost scarily concentrated, although we don’t yet know how GDX’s managers will deal with this.

As of this week the new combined Barrick only has an 11.1% GDX weighting, while Newmont is at 8.2% since its mega-merger is not yet consummated. It will be interesting to see whether the new companies’ weightings going forward are kept in market-cap proportion or somehow limited. I hope it’s the latter, as many of the other gold miners in GDX have far-better growth prospects than these new super-majors.

ETF weightings aside, higher market caps create plenty of problems of their own. I’ve written essays in the past on picking great gold stocks, and surprisingly market capitalization is the single most important factor for future gains. The gold stocks with the largest market caps usually significantly underperform their smaller peers. These new super-majors are so darned big that they really compound this problem.

In mid-November when I analyzed the GDX miners’ Q3’18 results, the average market cap of its top 34 component stocks was $4.3b. Excluding NEM and ABX, that fell to $3.5b. It takes proportionally more capital inflows, investors buying shares, to push a larger stock higher than a smaller one. If the super-majors are worth $24b, it takes 6x as much buying of their stocks to drive the same gains as on a $4b company!

Imagine the different forces involved turning a supertanker versus a tugboat. The bigger any stock in the stock markets, the more inertia it has and thus the more capital is needed to overcome that and move the stock. And market-cap issues are not just a size thing in gold stocks. Smaller major, mid-tier, and junior gold miners have way fewer gold mines and much-lower production, which makes it far easier to grow output.

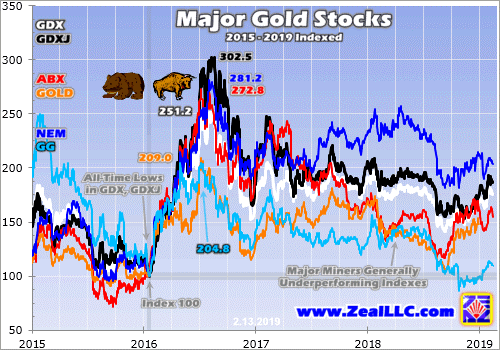

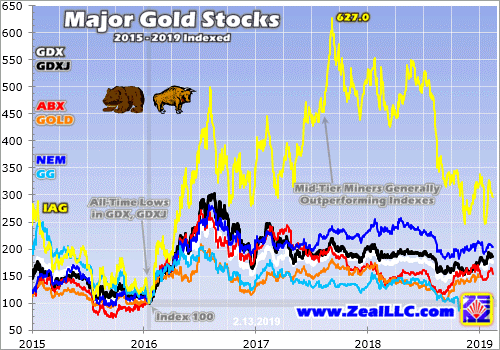

While Newmont is a temporary exception since it was bucking the major trend and growing production in 2017, Barrick, Randgold, and Goldcorp all really underperformed their sector in recent years. This chart looks at the indexed performance in ABX, GOLD, NEM, and GG stocks compared to the leading sector ETFs of GDX and the smaller GDXJ which largely tracks mid-tier gold miners under 1m ounces annually.

Both GDX and GDXJ fell to all-time lows back in mid-January 2016 when this gold-stock bull was born. So all 6 stocks are indexed to 100 as of that day, revealing their relative performance since. Despite their heavy weighting in GDX, the major gold miners generally lag their key sector benchmarks. ABX, GOLD, and GG have really struggled in recent years as their managers failed to stem big production declines.

This chart is pretty damning, showing why the managers of Barrick and Newmont are desperate to show rising production even if only for a year after their wildly-expensive mega-mergers. ABX and GOLD have both been really underperforming their peers, scaring investors away while putting serious pressure on managements to turn things around. NEM resisted that, but its production started to decline too in 2018.

And GG has been a basket case, actually managing to fall below its deep secular lows of early 2016 in recent months! That’s a sad fate for what was the world’s best major gold miner for many years. NEM buying this dog is likely to drag down NEM’s stock performance to some midpoint between what it has done and how GG has fared. For the most part the largest gold miners haven’t been good investments.