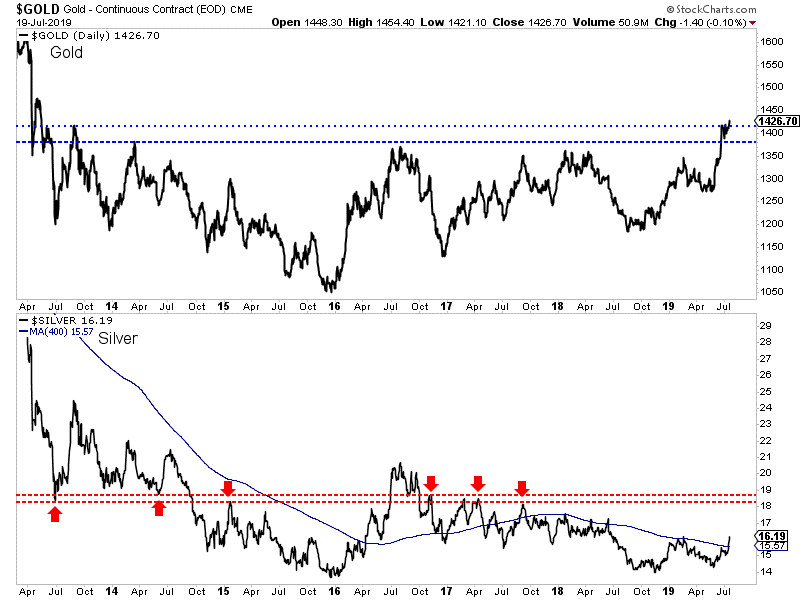

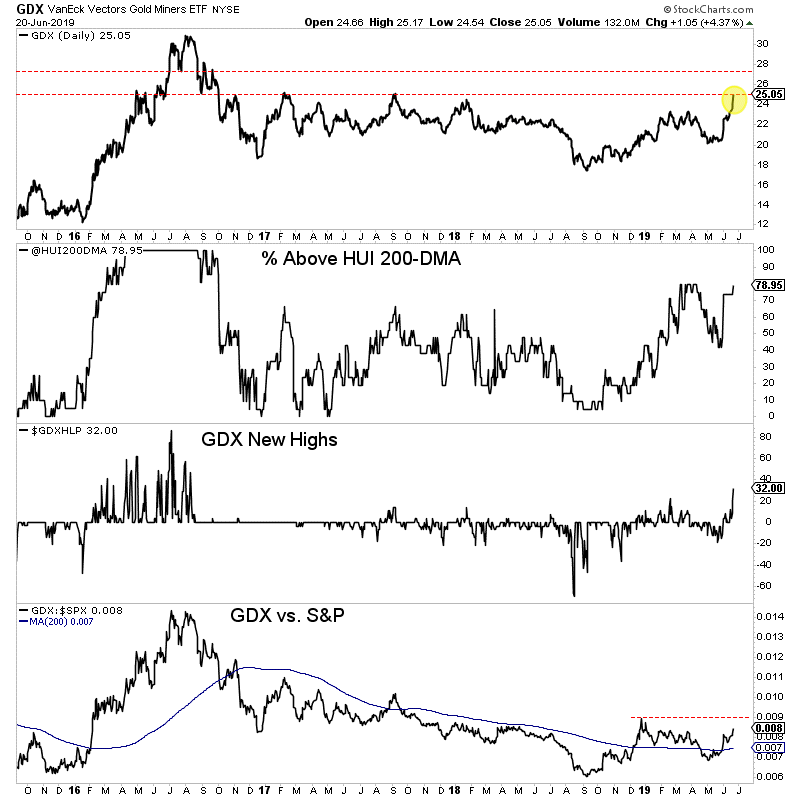

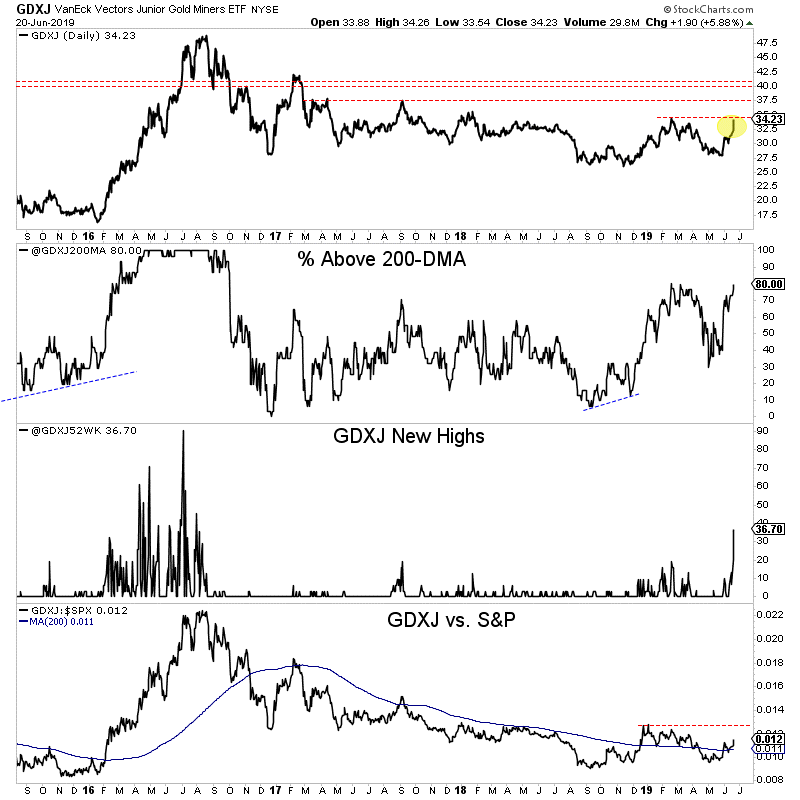

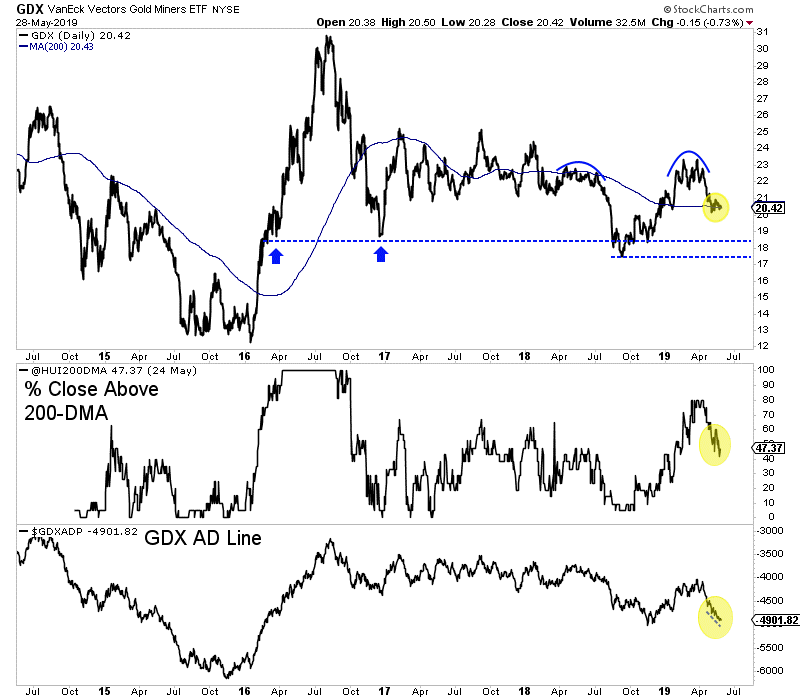

It was a huge week for the gold stocks. GDX gained nearly 7% while GDXJ surged over 10%.

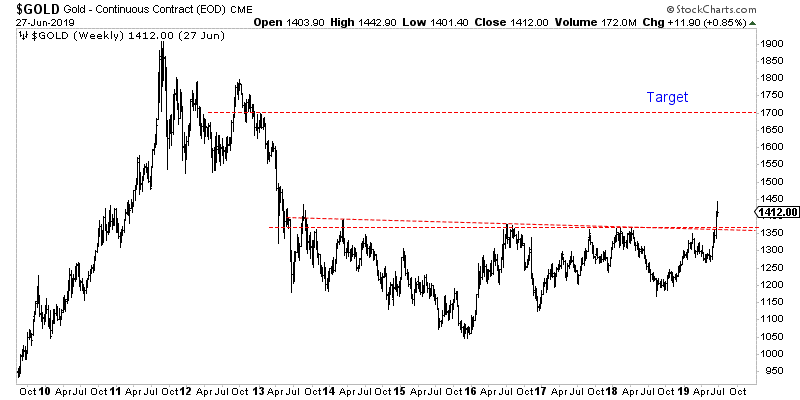

Gold hit $1450/oz after Thursday before selling off Friday. Silver met the same fate on Friday but managed to close the week up over 6% and at a new 52-week high.

Let’s take a look at the current technicals.

Gold closed the week just below $1427/oz. If it remains above $1420-$1425, then it is likely to trend towards $1475/oz, which is the only resistance between $1425 and $1525.

If Gold trades back below $1420 then there is a risk it could test $1380 again.

Silver has taken out resistance at its 400-day moving average in convincing fashion but needs to surpass its February 2019 high. Its next major resistance target is the mid $18s.

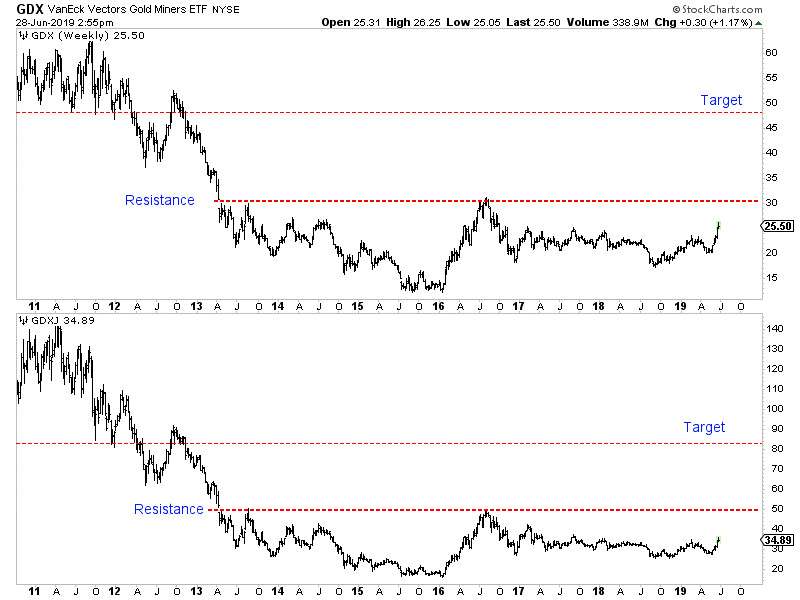

Turning to the stocks, we start with GDX which is closing in on its 2016 high. Should Gold trend towards $1475/oz then GDX would likely retest that 2016 high at $31.

Breadth remains strong and so too is GDX’ relative strength. GDX relative to the S&P made a 21-month high and relative to Gold made a 2-year high.

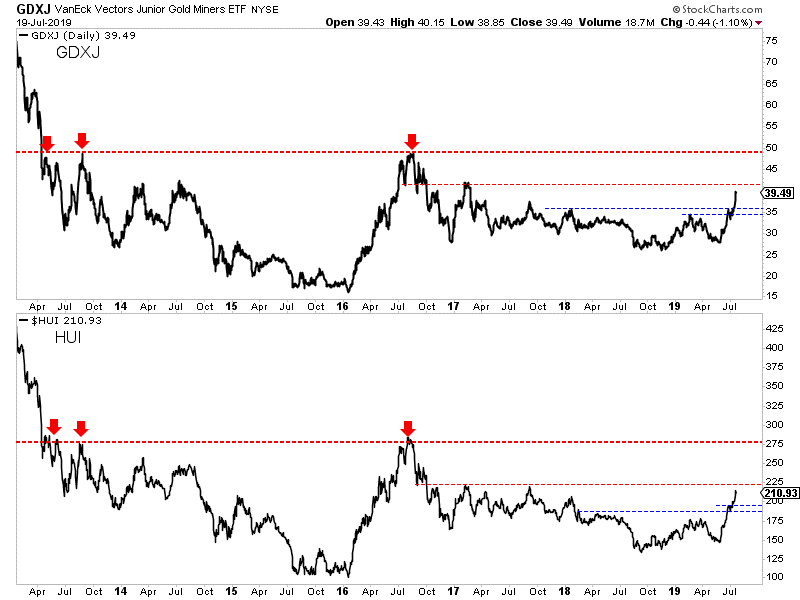

Both GDXJ (juniors) and the HUI (miners only) still have room to go before reaching their 2016 highs.

In fact, both are facing some immediate overhead resistance. For GDXJ which closed at $39.50, that resistance is at $40-$41. For HUI which closed at 211, that resistance is at 220.

The support levels are $36 for GDXJ and 195 for the HUI.

If Gold and Silver maintain current levels, then the immediate bias remains higher and GDX could soon test its 2016 high.

GDXJ and HUI have roughly 30% upside to their 2016 highs. Such a move probably requires a move in Gold to at least $1525/oz.

However, if Friday was the start of a correction then GDX could test $26 and GDXJ could test $36.

For investors in the juniors and seniors, continue to hold winners. If the sector corrects, then look to take advantage of that weakness. If metals and shares maintain these levels then focus your capital on fresh opportunities and value plays that are not overbought or extended. To learn the stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

By Jordan Roy-Byrne CMT, MFTA

July 23, 2019

The gold miners’ stocks continue to rally on balance, after a major upside breakout extended their strong upleg. That’s driving mounting interest in this recently-forsaken sector. With the latest quarterly earnings season underway, traders will soon enjoy big fundamental updates from the gold miners. They are likely to report good Q2 results, with improving operational performances supporting further stock-price gains.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 40 calendar days after quarter-ends. The gold miners generally release their quarterly reports in the latter half of that window. So Q2’19’s will arrive between late July to mid-August.

After spending decades intensely studying and actively trading this contrarian sector, there’s no gold-stock data I look forward to more than the miners’ quarterly financial and operational reports. They offer a true and clear snapshot of what’s really going on, shattering the misconceptions bred by ever-shifting winds of sentiment. Nearly all fundamental analysis is based off the data gold miners provide in quarterlies.

So for many years I’ve delved deeply into gold miners’ quarterly results. They are the dominant source of information I use to winnow down the universe of gold stocks to the fundamentally-superior ones with the greatest upside potential. Every quarter after their latest earnings season ends, I research and write essays discussing the newest results from the major gold miners, mid-tier gold miners, and silver miners.

Q2’19’s full analyses are coming starting in mid-August once that 40-day post-quarter reporting deadline has passed. But before that I eagerly dive into individual companies’ results as they’re reported, since there’s so much to digest. Even earlier soon after a quarter ends, I start thinking about what gold miners’ latest quarterly results are likely to show collectively. Their aggregate trends can be somewhat predicted.

In high-level fundamental terms, gold mining is a simple business. These companies painstakingly wrest gold from the bowels of the Earth, then generally sell all they can produce at prevailing market prices. So their profits are effectively the difference between current gold levels and operating costs. The former is easy to calculate once a quarter ends, and the latter can be reasonably estimated for this sector as a whole.

Gold’s dramatic bull-market breakout a month ago and high consolidation since have greatly improved sector psychology. But gold’s big surge came late in Q2, minimizing its full-quarter impact. The early quarter was rough, with gold slumping to a new year-to-date low near $1271 in early May. The average gold prices in April, May, and June were $1286, $1284, and $1361. Gold was mostly sucking wind last quarter.

Thus Q2’19’s overall average gold price of $1309 was just a meager 0.4% better than Q1’s $1303. So the gold miners’ latest quarterly results aren’t going to get much help from gold’s young surge. That will really change in the current Q3 if gold can hold these high levels. With Q3 about 1/5th over, gold has averaged an awesome $1407 so far! So the higher-gold boost to gold-stock earnings is coming, but not in Q2.

Gold stocks really leverage higher gold prices because their mining costs are largely fixed. Quarter after quarter mining operations generally require the same levels of infrastructure, equipment, and employees. The vast majority of any gold mine’s future cost structure is actually determined during its planning phase, when engineers decide which ore to mine, how to excavate it, and how to process it to recover the gold.

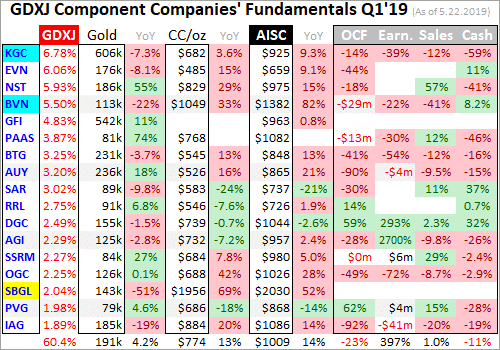

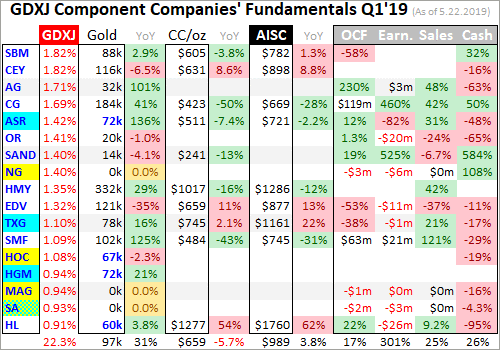

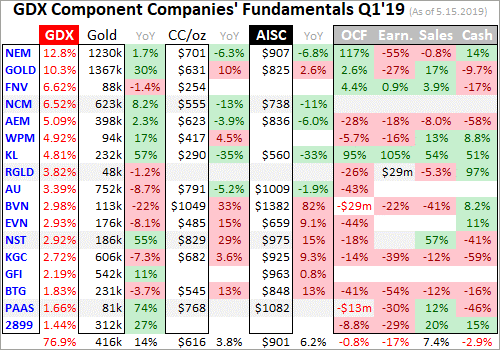

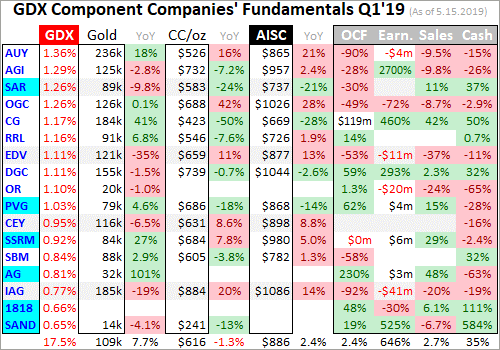

Every quarter after results I analyze the all-in-sustaining costs reported by the world’s gold miners. These are the best measure of what it really costs to produce an ounce of gold. Over the past four quarters, the major gold miners of the leading GDX VanEck Vectors Gold Miners ETF reported average AISCs of $856, $877, $889, and $893. That in turn yields a trailing-four-quarter mean of $879 per ounce, a key cost metric.

With $1309 average gold in Q2’19 and AISCs likely near $879, that implies the large gold miners as an industry likely earned $430 per ounce last quarter. That’s actually a decent improvement considering the flat quarterly gold prices. Though gold averaged a similar $1303 in Q1, the GDX miners’ average AISCs that quarter came in a bit higher at $893. That implied $410 profits, which Q2 results should easily exceed.

$430 is up 4.9% quarter-on-quarter despite the relatively-flat average gold price! This is really impressive sequential profits growth relative to the broader stock markets, where earnings are stalling out. But if that is all we could hope for, I would’ve written on a different topic this week. The gold miners’ Q2’19 earnings are likely to well exceed expectations for an entirely-different reason, portending even-higher gold-stock prices.

Most traders assume gold miners produce their yellow metal at fairly-steady rates year-round. That sure makes sense given how capital-intensive gold mining is, how individual mines’ capacities and throughputs to process ore are fixed, and how expanding mines’ outputs takes years of construction. But surprisingly global gold mine production actually varies considerably quarter-to-quarter! This should really boost Q2 earnings.

The best global gold fundamental data is published by the World Gold Council, also on a quarterly basis. These Gold Demand Trends reports are essential reading for all gold-stock speculators and investors, as these miners are ultimately just leveraged plays on gold. The latest GDT covering Q1’19 was released in early May, with Q2’s due out in early August. One key number GDTs report is world gold mine production.

That happened to run 852.4 metric tons in Q1, nearly a third of which came from the major gold miners of GDX. Analyzing global gold mine production each quarter since 2010 reveals some fascinating quarter-to-quarter output trends. Over the last 37 quarters, calendar Q1s have seen gold mined average a sharp 7.2% QoQ plunge from the immediately-preceding calendar Q4s! Not a single Q1 saw sequential output growth.

From 2010 to 2019 Q1 gold mined fell 7.2%, 6.9%, 7.6%, 11.2%, 8.8%, 3.3%, 8.7%, 5.7%, and 5.6% from the respective Q4s. These drops and their uniformity across radically-different gold-price environments is stunning. For some reason the world’s gold mines suffer universal declines in their outputs early in calendar years. Why? This curious industrywide Q1 production slump results from an interplay of several factors.

Most gold miners run their accounting on calendar years. So early in new years they have new capital budgets to spend on maintaining and enhancing their existing operations. If they temporarily shut down their mills for repairs or minor upgrades, Q1s are usually when they do it. Weather plays a role too, as the majority of the world’s gold mines are in the northern hemisphere with the majority of the world’s land masses.

Winter creates operational challenges for gold mines, ranging from extreme cold to heavy snow or rains depending on their latitudes and elevations. So in addition to short planned shutdowns to work on infrastructure, adverse weather can impair operational efficiencies. But the main reason global gold-mine outputs plunge in Q1s is due to ore-grade-management decisions made by mine managers to maximize bonuses.

Gold deposits are not homogeneous, ore grades vary widely within them. So managers must choose which ore to mine, when to run it through their mills, and how to mix it with ores from other locations. The mills that crush the gold-bearing rock into small-enough chunks to recover the metal have fixed capacities in tonnage-per-day terms. So the less gold contained in the ore processed, the less gold the mines recover.

Mine managers often choose to dig through lower-grade ores, or run lower-grade ores through their mills, in Q1s. They save the higher-grade ores for later in calendar years. They often claim these decisions are related to early-year capital budgets being spent to improve outputs later in years. But there’s probably more to it, since this happens so universally across the world’s gold mines. Incentives have to play a role.

Gold-mine managers are often partially compensated based on how their stock prices are faring. This is usually a big factor in annual bonuses calculated near year-ends. These bonuses are the most-variable part of compensation, and can greatly boost income. After long years of study and talking with some of these guys, I’m convinced they choose to take any gold-output hits early in years to engineer strong finishes.

Q1 results are reported by mid-Mays, a long way out from year-ends. That’s the least-beneficial time in bonus terms for strong output to boost stock prices. Q2 results released by mid-Augusts and Q3 results published by mid-Novembers are far-more important. So mine managers feed their fixed-capacity mills better-grade ore mixes in Q2s and Q3s, after early-year maintenance is finished and summer weather is favorable.

Thus in calendar Q2s since 2010, global gold mine output according to the World Gold Council surged an average of 5.4% sequentially from Q1s! Over the past 9 years Q2s have seen huge QoQ global-output gains of 6.7%, 7.7%, 6.3%, 7.1%, 6.1%, 5.7%, 0.7%, 4.9%, and 3.4%. There has not been a single down Q2 in this span despite wildly-different gold-price environments. Such uniformity reveals deliberate planning.

Over roughly the past decade, world gold mine production has averaged -7.2% QoQ in Q1s, +5.4% in Q2s, another hefty +5.3% in Q3s, then just +0.5% in Q4s. That Q4 stalling is pretty telling too, as those Q4 results are typically released by mid-Marches which doesn’t affect annual bonuses when those quarters were underway. The gold miners contrive their best output reporting from late Julies to mid-Novembers!

So in these upcoming Q2’19 results, the gold miners are likely to report production about 5% higher than Q1’s! That big sequential output boost really increases overall corporate earnings. And it has another key benefit of reducing all-in sustaining costs. AISCs are calculated by spreading the costs of gold mining across all ounces produced. So the more gold mined, the lower the unit costs of producing it that quarter.

A year ago in Q2’18, the GDX gold miners’ average AISCs dropped a big 3.2% sequentially from the prior quarter’s to $856 per ounce. So it is certainly reasonable to expect Q2’19’s AISCs to retreat 3% or so from Q1’s $893, which yields $866 per ounce. Subtract that from Q2’19’s average gold price of $1309, and it yields likely earnings of $443 per ounce. That is 8.0% higher quarter-on-quarter from Q1’s results!

That’s conservative too. As detailed in my essay on the GDX gold miners’ Q1’19 results, that quarter’s average AISCs were skewed higher by a single anomalous outlier. That company expects costs to greatly retreat in Q2. Excluding it, the GDX gold miners averaged considerably-lower $874 AISCs in Q1. A 3% reduction to that on higher Q2 output leaves an excellent $848 AISC target, implying big $461 profits!

That represents a major 12.4% quarter-on-quarter surge, which should excite traders anytime. And with gold-stock sentiment already growing far more bullish thanks to gold’s bull-market breakout, there’s a good chance Q2 earnings’ positive psychological impact will be amplified. As long as gold hangs in there and doesn’t sell off, the gold miners’ stocks have real potential to rally considerably on good Q2 results.

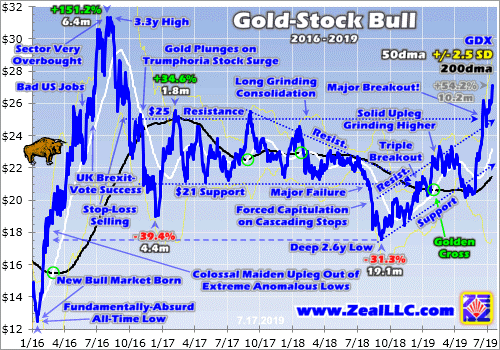

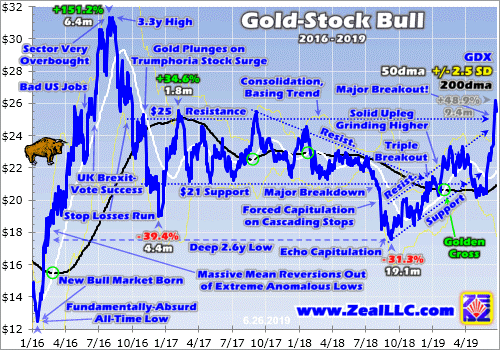

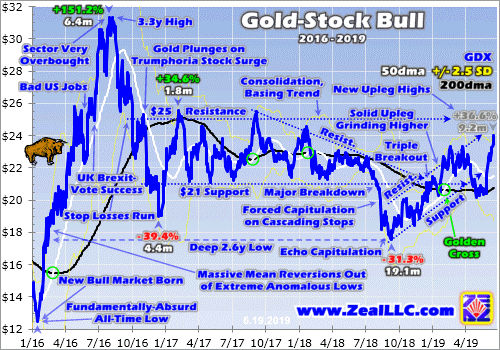

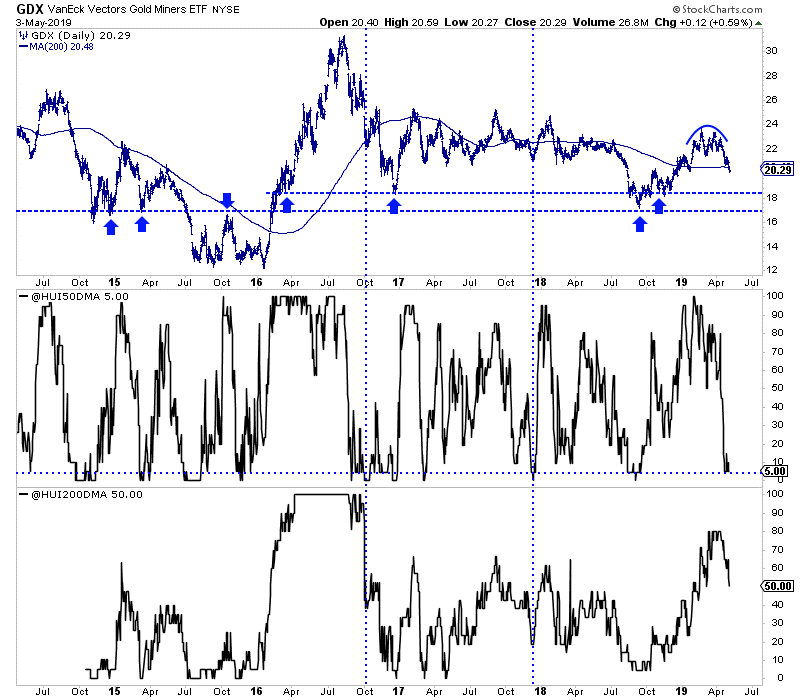

A couple charts offer some quick perspective. Gold’s breakout drove a major decisive upside breakout in gold stocks too as measured by their leading GDX benchmark. That dominant ETF is rendered in blue here, superimposed over its key technical lines. As of the Wednesday data cutoff for this essay, GDX had powered 54.2% higher in 10.2 months in its upleg to date. But gold-stock prices still remain relatively low.

Mid-week GDX hit $27.09 on close, its best levels in 2.8 years. But that remains well below gold stocks’ bull-to-date peak of $31.32 in early August 2016. The gold stocks ought to at least exceed those levels, which is another 15.6% higher from here. Good Q2 results interpreted through the lens of increasing sector bullishness should be enough to fuel a bull-market breakout. Gold argues for higher gold-stock levels.

Back in mid-2016 when GDX peaked at $31.32, gold merely hit $1365 at best. That was just after a quarter when the GDX gold miners’ AISCs averaged $886 per ounce. Gold was considerably higher this week, hitting $1425. And it has averaged $1408 for nearly a month since its bull-market breakout. So the higher prevailing gold prices this summer, and lower AISCs, should support much-higher gold-stock prices.

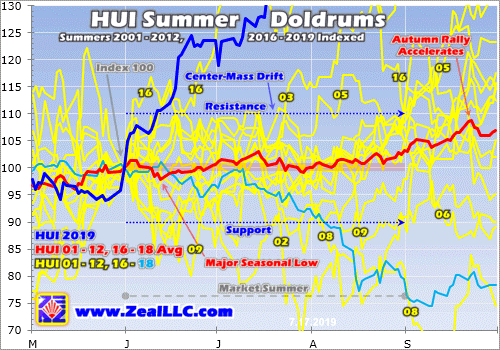

Showing just how strong gold stocks are and how unique today’s situation is, this last chart looks at gold stocks’ average performances in modern bull-market summers. I explained this indexed chart in depth in an essay on gold summer doldrums a couple weeks ago. The yellow lines show where the older HUI gold-stock index traded in past modern gold-bull-market summers, and the red line averages them together.

This year’s action is rendered in dark blue, revealing gold stocks’ best summer by far since 2016 after this gold bull’s massive maiden upleg! In the middle of this week the HUI rocketed 32.3% higher summer-to-date, literally off this seasonal chart I’ve gradually built up over the years. If there was ever a summer where gold stocks could punch out to new bull highs, this one is it. Their upside momentum is incredibly strong.

All this gold-stock bullishness aside, it is always wise to be wary when everyone else is getting excited. The potential for gold stocks to surge to new bull highs on good Q2 results is totally dependent on what gold does over the coming 6 weeks or so. While gold has shown awesome resilience in consolidating high and mostly holding $1400 over the past month, the gold selloff risk is high due to gold-futures positioning.

I wrote a whole essay last week explaining this in depth. In a nutshell, gold-futures speculators dominate short-term gold price action. Their current bets on gold are excessively-bullish, warning that their capital firepower to buy gold is nearing exhaustion. They are effectively all-in on long upside bets, and all-out on short downside bets. That leaves them vast room to sell hard on the right catalyst, pushing gold sharply lower.

There’s a chance new-high psychology can ignite enough investor gold buying to overpower and absorb any spec gold-futures selling. But realize gold-stock fortunes are still slaved to gold as always. Gold has to stay high to support new gold-stock highs. If gold materially falters and slumps into a healthy pullback or correction within an ongoing bull, the gold stocks will follow it lower regardless of how good Q2 results prove.

Buying high on strong upside momentum is always tempting, as that’s when traders feel the best about any sector. Bullishness and capital inflows soar as stocks power higher. But over time far-larger gains are won by instead buying low, adding positions when sectors are out of favor. The later you buy gold stocks in any upleg, the smaller their potential gains and the higher the odds a major selloff is looming.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In recent months well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. Mid-week their unrealized gains ran as high as 123.9%, 123.5%, and 116.5%!

To profitably trade high-potential gold stocks, you need to stay informed about the broader market cycles that drive them. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast so they can ride entire uplegs.

The bottom line is the gold miners’ just-starting Q2’19 earnings season should prove impressive. That’s no thanks to gold, as its awesome bull-market breakout came too late last quarter to push its average price significantly higher. But the gold miners are still likely to collectively report sharply-higher Q2 output, which is normal after Q1’s deep production slump. That will also naturally lead to proportionally-lower costs.

Growing production combined with lower costs at slightly-higher gold prices should yield big profits growth for the gold miners. Their Q2 results will be more closely watched and better received since psychology is shifting much more bullish in this sector. That should fuel big gold-stock buying as long as gold holds up. The yellow metal has proven resilient so far, but faces an ominous overhang of gold-futures selling pressure.

Adam Hamilton, CPA

July 22, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

- It’s the ultimate “no-brainer” that serious American GDP growth (in the 6% range or higher) can only happen by eliminating the PIT (personal income tax) for the middle class.

- QE and low interest rates incentivize pathetic levels of debt-oriented GDP growth while incentivizing the government to get more reckless with the money that is borrowed and extorted from citizens as taxes.

- Elimination of the PIT would instantly turn the debt-bombed middle class of America into a “savings and purchasing power machine”.

- With higher rates and elimination of the PIT, government would be forced to shrink, banks would eagerly loan out the savings to mainstream business, and the middle class would consume with savings rather than credit card debt.

- The bad news: The PIT won’t be eliminated, and government worship of debt, QE, low rates, and extortion is not going away.

- The good news: That means the gold price is going higher!

- To view the key buy and sell levels for gold, please click here now. Double click to enlarge.

- Gold investors should be eager buyers of gold, silver, and the miners in the $1390 gold price area or on a breakout above $1440.

- Please click here now. Double-click to enlarge this key weekly gold chart.

- The most likely scenario for gold now is a rally towards $1500-$1523, followed by a significant pullback that will probably look a lot like the late 2009 pullback.

- What actually happens is almost certainly going to depend on the actions and statements from the Fed at the July 31 meeting.

- If the Fed isn’t as dovish as expected, gold could pullback towards $1320 quite quickly. A half point cut and a dovish outlook could produce a dramatic “target overshoot” for gold. A surge to $1750 would be quite realistic in that situation.

- Whatever happens, $1390, $1360, and $1320 are all key buy zones and $1440, $1500, and $1750 are all decent profit booking targets.

- Please click here now. Double-click to enlarge this daily silver chart. Like Rodney Dangerfield, silver doesn’t get much respect, but that’s because inflation has yet to really surge.

- Having said that, the silver chart is beginning to look quite bullish. A breakout from an inverse H&S bottom pattern has occurred, and the pullback was flag-like.

- The target of both the flag and the H&S pattern is the $16.50 area highs of February.

- From a risk-reward perspective, silver is beginning to look superior to the US stock market.

- Please click here now. Double-click to enlarge this swing trade chart.

- Swing trade enthusiasts can get in on the leveraged ETF action for gold stocks and the Nasdaq with my guswinger.com service. We are also carrying a massive Barrick position. Signals are available by email (and cell phone text for traders with US cell phone numbers).

- For an analytical look at the GDX daily chart, please click here now. Double-click to enlarge. I use a 24hour chart for GDX. On this chart, a surge above $26.45 would be a fresh buy signal not just for GDX, but for most intermediate and senior gold producers.

- Please click here now. Double-click to enlarge this silver stocks ETF chart.

- Note the recent superior performance of the silver miners compared to silver bullion.

- There is an H&S bull continuation pattern forming on the chart and I believe that pattern makes an “upside blast” to my $34 target price zone highly likely.

- The bottom line for gold and silver stocks: The action is solid, and the action is now!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Ultimate Gold Market Portfolio” report. I highlight tactics to assemble a pure performance portfolio of global metal miners, with key action points for each holding!

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

Gold and gold stocks especially continue to shrug off bits and pieces of bad news.

No escalation in the trade war? The selloff lasted one day and the sector rebounded strongly the following day.

Strong headline jobs number? Again, the weakness was a buying opportunity.

This past week there was more.

The June CPI report came in hotter than expected, which could mitigate the degree the Fed eases in the future. Also, bond yields in the US have risen the entire week.

No dice.

Gold closed the week at $1412/oz while the gold stocks closed just inches from new highs on the daily charts.

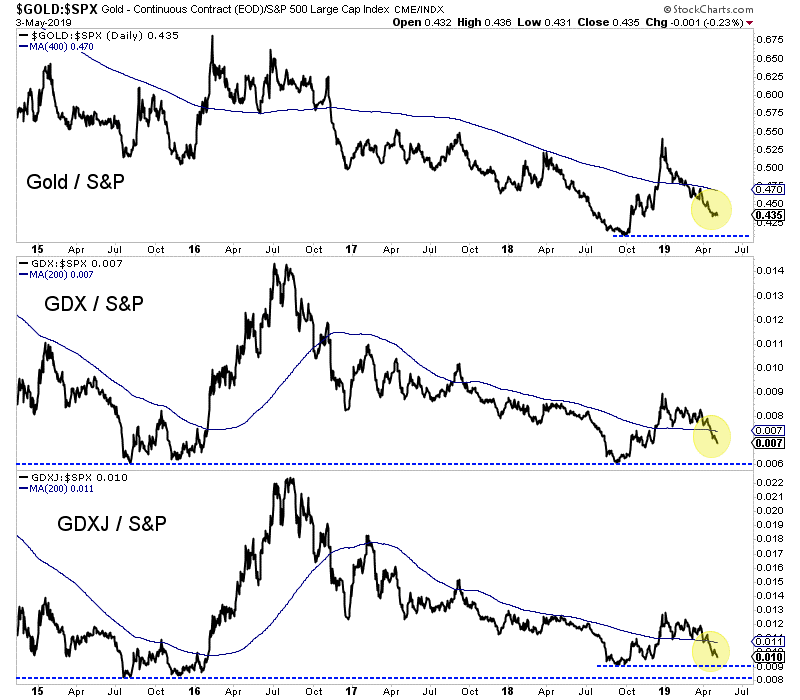

Turning to the technicals of the gold stocks, we see both underlying and relative strength.

Nearly 95% of the large miners closed above the 200-day moving average. Meanwhile GDX relative to both the S&P 500 and Gold is above a rising 200-day moving average. The GDX to Gold ratio is at a 2-year high while the GDX to S&P 500 ratio is very close to a new 52-week high.

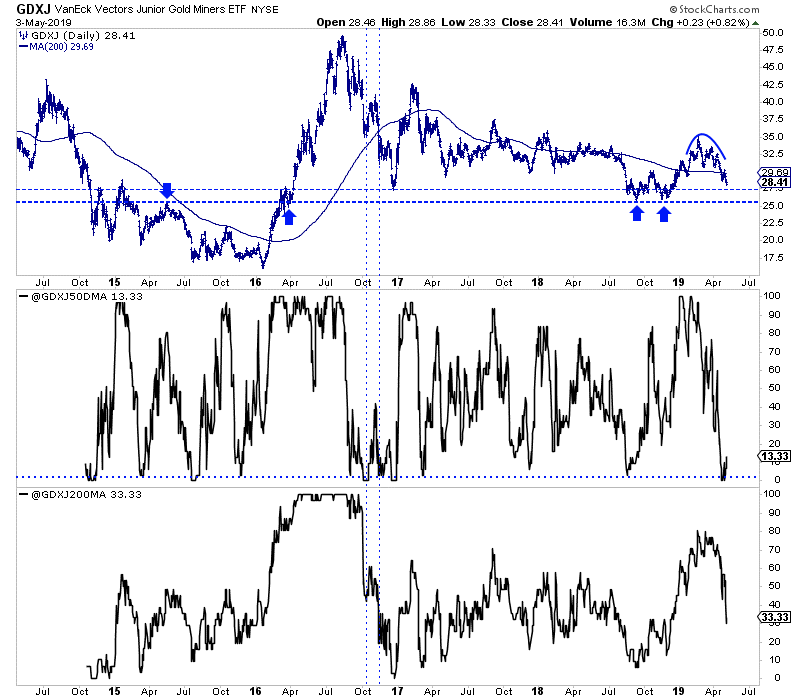

GDXJ is lagging GDX a bit but it is coming around.

90% of the ETF closed above the 200-day moving average. That is the highest reading in nearly three years.

GDXJ relative to the S&P and Gold has turned bullish and is holding above upward sloping 200-day moving averages.

The immediate upside targets for GDX and GDXJ are GDX $27.50 and GDXJ $37.50. The next level of targets would be GDX $30 and GDXJ $41.

Gold has endured some selling in the $1420-$1425/oz range but has remained bid around $1400/oz. A daily close above $1420/oz would remove much of the resistance from here to the low $1500s.

For investors in the juniors and seniors, continue to hold your winners and focus your capital on fresh opportunities and value plays that could move with the next leg higher. To learn which stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

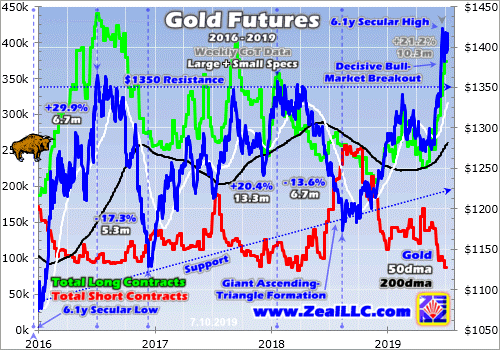

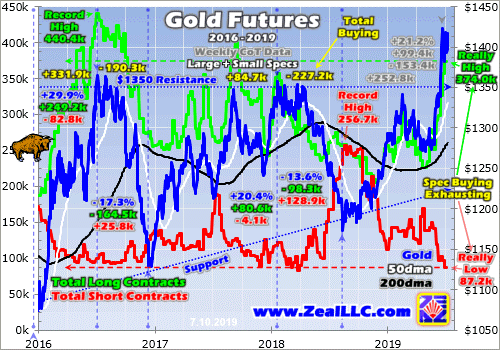

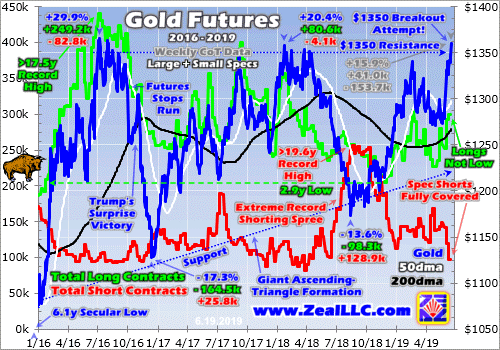

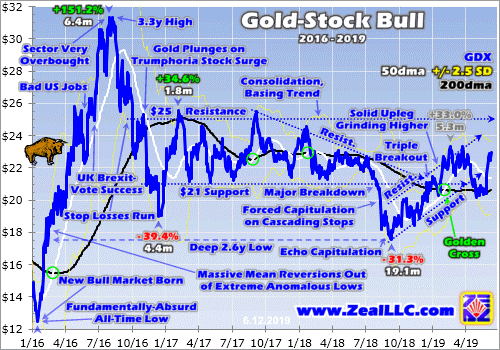

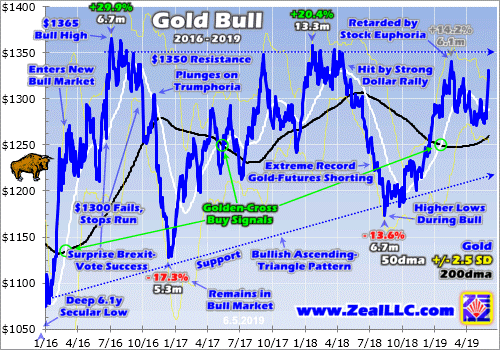

Gold surged dramatically in recent weeks, powering higher to a decisive bull-market breakout. Gold’s first major secular highs in years have really improved sentiment, with bullishness mounting. But gold-futures buying fuel is largely exhausted, after the colossal amount expended to catapult gold back over $1400. That leaves this metal at high risk of suffering a major selloff, a healthy correction in an ongoing bull market.

Even the most-powerful bull markets flow and ebb, taking two steps forward before one step back. Gold is certainly no exception. At best in late June, its current bull extended to modest 35.4% gains over 3.5 years. Those weren’t linear, the path to gold’s recent breakout high was quite volatile. It included a 29.9% upleg, a 17.3% correction, a 20.4% upleg, a 13.6% correction, and today’s upleg running 21.2% at best.

This alternating repeating bull-market pattern is simple, uplegs are inevitably followed by material selloffs often extending into correction territory. Periodic corrections are essential to keep bulls healthy, working off the excessive greed that builds as uplegs peak. That risks sucking in too much capital too soon, prematurely burning out bulls. Corrections rebalance sentiment, bleeding away greed to extend bulls’ longevity.

Even though they are inevitable, normal corrections stress out the majority of traders. The selling taints their psychology and clouds their perspectives of longer-terms trends in play. They fret bulls are dying, and sell out too early and too low. Instead corrections should be embraced, as they offer the greatest opportunities to buy relatively low within ongoing bulls! Entering near correction lows amplifies gains.

While gold’s current bull clocked in at 35.4% total in late June, its three major uplegs added up to much-larger 71.5% gains. Traders had the potential to more than double gold’s headline gains by attempting to buy relatively low later in corrections and sell relatively high later in uplegs! Although impossible to game bull-market swings’ major lows and highs precisely in real-time, trading near them really boosts capital growth.

The reason gold faces high risk for its next major selloff today is speculators’ current positioning in gold futures. Unfortunately spec gold-futures trading has a wildly-disproportional influence over short-term gold price levels. The dominant reason is the extreme leverage inherent in gold futures, which greatly multiplies that capital’s impact on gold prices. This unfair reality has sorely vexed the gold market for decades.

When a normal investor buys gold outright, $1 of capital exerts $1 of buying pressure on the gold price. That’s the way markets are supposed to work. That can be extended with margin in the stock markets, which has had a hard legal limit of 2.0x since 1974. $1 of capital using maximum margin to buy shares in the leading GLD SPDR Gold Shares gold ETF can exert $2 of buying pressure on gold. That’s still reasonable.

But gold-futures trading is way out in its own extreme realm. Each gold-futures contract controls 100 troy ounces of gold. At this Wednesday’s data cutoff for this essay, gold closed at $1417. So each contract wields gold worth $141,700. An investor would have to put up $141,700 to control that much gold, or $70,850 using stock-market-legal-limit leverage on GLD shares. Futures speculators only need $4,000!

That’s no typo, this week the CME Group only requires traders to have $4,000 cash in their accounts for each gold-futures contract they want to trade. That is absurd, enabling extreme maximum leverage of 35.4x! That means a fully-margined gold-futures speculator can exert $35 of buying or selling pressure on gold with each $1 deployed. That temporarily outguns investors, even though they have vastly more capital.

The Federal Reserve has capped stock-market leverage at 2.0x for 45 years because extreme leverage has extreme risks. At 35.4x, a mere 2.8% gold move against speculators’ gold-futures bets would wipe out 100% of their capital risked! This constant threat of ruin forces these traders’ focus to an ultra-myopic short-term span, days or weeks at most. All they can do is ride gold’s immediate momentum, piling on.

As if arbitrarily declaring $1 of gold-futures capital should have up to 35x the influence on gold prices as $1 invested outright isn’t ridiculous enough, it gets worse. Unscrupulous traders can wield gold futures’ extreme leverage like a weapon to manipulate gold prices at key technical and sentimental junctures. One way is spoofing, slamming the market with huge gold-futures orders that are canceled before being executed.

This is not theoretical. In late June the U.S. Department of Justice levied $25m of criminal fines on Merrill Lynch Commodities for this very behavior! And that’s just the tip of the iceberg for gold futures’ extreme leverage being abused to defraud normal investors. This seriously needs to be legally capped at vastly-lower levels. The DoJ’s actual press release did a great job explaining how gold-futures spoofing works.

“…beginning by at least 2008 and continuing through 2014, precious metals traders employed by MLCI schemed to deceive other market participants by injecting materially false and misleading information into the precious metals futures market. They did so by placing fraudulent orders for precious metals futures contracts that, at the time the traders placed the orders, they intended to cancel before execution.”

“In doing so, the traders intended to “spoof” or manipulate the market by creating the false impression of increased supply or demand and, in turn, to fraudulently induce other market participants to buy and to sell futures contracts at quantities, prices and times that they otherwise likely would not have done so. Over the relevant period, the traders placed thousands of fraudulent orders.” These crooks should be in prison!

Compounding gold futures’ gold-price impact, the American gold-futures price is gold’s global reference one. So gold-futures trading moving the gold price heavily influences and sometimes totally controls the entire gold market’s psychology! Investors are motivated to buy and sell gold outright based on what is happening in gold futures. It’s impossible to understand and game gold without closely watching futures.

I had to break my chart into two parts today, lest it get too busy to parse. These superimpose gold’s price through its current bull market over speculators’ gold-futures positioning. Reported weekly by the CFTC in its famous Commitments of Traders reports, specs’ long contracts or upside bets on gold are shown in green while their short contracts or downside bets are rendered in red. They usually dominate gold action.

The wildly-disproportional influence on gold prices by speculators’ gold-futures trading is critical for all investors to understand. Let’s start with this gold bull itself, the cadence of its uplegs and corrections. Its maiden upleg erupted in mid-December 2015 out of deep 6.1-year secular lows in gold, and ultimately blasted up 29.9% in 6.7 months by early July 2016. Major selloffs inevitably follow major uplegs in any bull.

So gold plunged 17.3% over 5.3 months into mid-December 2016 in a severe correction. That was way bigger than normal, greatly exacerbated by Trump’s surprise election victory in early November that year. With Republicans controlling the presidency and both chambers of Congress, stock markets soared on hopes for big tax cuts soon. That crushed gold demand, as fully 5/8ths of that correction came after the election!

While ugly, gold remained in a bull market since that massive selloff didn’t cross the -20% threshold for a new bear market. Gold quickly rebounded from those deep lows and gradually powered to another nice bull-market upleg, up 20.4% over 13.3 months leading into late January 2018. This gold bull’s second major upleg was followed by its second major correction, a 13.6% drop over 6.7 months by mid-August 2018.

That birthed today’s third major upleg, which had extended to 21.2% at best over 10.3 months by late June. This past month saw gold get exciting again after decisively breaking out of its years-long giant ascending-triangle technical formation to surge to major new bull-market and secular highs. This bull’s pattern has been upleg, correction, upleg, correction, upleg. What comes next in this series is obvious.

Gold is at high risk for another major selloff, potentially a full-blown correction over 10% again, because of speculators’ gold-futures positioning. This next chart illuminates what the specs were doing during each of this gold bull’s uplegs and corrections including today’s newest one. These hyper-leveraged traders with their outsized impact on gold prices have effectively exhausted their near-term buying, threatening big selling!

This gold bull’s initial upleg in largely the first half of 2016 was massive, the biggest in this bull so far at 29.9%. That was partially fueled by gold-futures speculators buying a staggering 249.2k long contracts and buying to cover another 82.8k short ones! There are two kinds of buying and two kinds of selling in gold futures, and each set has the same price impact on gold. Thus they can be lumped together for analysis.

Specs can buy new gold-futures contracts to establish long positions, the normal way to buy. But they also buy to cover and close previously-established short positions. The upward pressure on gold from buying longs and covering shorts is identical. On the selling side they can sell their own existing longs, or effectively borrow gold-futures contracts they don’t own to short sell them. Both types hit gold the same way.

Speculators’ total gold-futures buying in this gold bull’s first upleg ran a mind-boggling 331.9k contracts! That’s the equivalent of 1032.4 metric tons of gold. For comparison, total global gold investment demand in the first half of 2016 ran 1091.6t per the World Gold Council’s latest fundamental data. That epic spec long buying catapulted their total upside bets to an all-time-record high of 440.4k contracts as that upleg peaked!

Keep these numbers in mind. This gold bull’s greatest upleg soared 29.9% higher on 331.9k contracts of total buying by gold-futures speculators. That forced their total longs to their highest levels ever seen of 440.4k contracts. As I’ll discuss shortly, today’s latest gold upleg is skating ever closer to those extreme levels. The ice gets pretty thin in that rarefied air of likely gold-futures buying being essentially exhausted.

This gold bull’s first major correction was largely driven by specs reversing that huge long build in largely the second half of 2016. Note the green spec-longs line above collapsed symmetrically to its massive surge in the preceding upleg. Specs dumped 164.5k long contracts and short sold 25.8k more over that severe correction’s exact span. That adds up to 190.3k contracts of total selling, the equivalent of 592.0t.

During gold-bull uplegs the green spec-longs line rises while the red spec-shorts line falls. Then in following corrections that reverses, the green line falling while the red one rises. Gold-futures buying and selling is heavily driving these major bull-market cycles in gold, and that’s not going to change until regulators wake up and radically curtail gold futures’ extreme inherent leverage. Gold’s second upleg straddled 2017.

That was somewhat peculiar, as the spec gold-futures long buying of 80.6k contracts and short covering of 4.1k only totaled 84.7k. That wasn’t much considering gold’s strong 20.4% upleg gains. But realize that gold upleg effectively topped much earlier in early September 2017. Its later upleg peak was marginal. As gold challenged its $1350 bull-market resistance, total spec longs soared as high as 400.1k contracts!

This gold bull’s second correction mostly unfolded during the first half of 2018, and was a textbook-perfect example of heavy spec gold-futures selling. Their green longs line plunged by 98.3k contracts, while their red shorts line rocketed an enormous 128.9k contracts higher. That correction bottomed last August as total spec shorts soared to their own all-time-record high of 256.7k contracts! That portended the next upleg.

Back in early September, I wrote an essay on the “Record Gold/Silver Shorts!”. Published when gold still languished way down at $1196, I concluded then “gold and silver soon soared on short-covering buying following all past episodes of excessive and record short selling. There’s nothing more bullish for gold and silver than extreme shorts! … Record futures shorts are the best gold and silver buy signals available.”

Speculators’ collective gold-futures positions provide both excellent buy signals near major gold lows and excellent sell signals near major gold highs. Smart contrarians get really bullish on gold when specs are really bearish as evidenced by relatively-low longs and relatively-high shorts. And it is just as prudent to get short-term bearish on gold when specs are excessively bullish with relatively-high longs and -low shorts.

This is exactly the situation we’re in today, and it’s growing ominously extreme. This gold bull’s third upleg powered 21.2% higher at best so far as of late June, propelling this metal to a new 6.1-year secular high of $1423. This awesome decisive-bull-breakout upleg was again fueled by enormous gold-futures buying by speculators. They added 99.4k long contracts, while buying to cover a staggering 153.4k short ones!

That adds up to total buying of 252.8k contracts as of gold’s latest peak in late June, or the equivalent of 786.3 metric tons of gold! That’s relevant because it is already 76% of the total gold-futures buying that unfolded during this gold bull’s huge maiden upleg in early 2016. Back then popular gold psychology was waxing really bullish, fostering that extreme gold-futures buying. Getting that high again today is a tall order.

The current gold-futures picture is even worse. While gold hit its latest interim high in late June, the gold-futures speculators kept on buying since. The weekly CoT reports are published late Friday afternoons current to the preceding Tuesdays. So the latest data available this week is current to last Tuesday July 2nd. That saw still more big spec buying, they added another 16.5k longs and covered another 10.2k shorts.

That extends this upleg’s total spec long buying to 115.9k contracts and short covering to 163.6k, making for a larger 279.5k total. Thus today’s upleg has already seen speculators buy 84% of the gold-futures contracts that they did during early 2016’s massive maiden upleg! That doesn’t leave much room to keep on adding more longs and covering more shorts to propel gold to major news highs in the coming weeks.

As of last Tuesday, total spec longs were already way up in nosebleed territory at 374.0k contracts! Out of the last 1070 CoT weeks since early 1999, only 2.2% saw spec longs higher. And that is getting closer to their all-time-record high of 440.4k in early July 2016. While they could conceivably go higher, that’s a hard ceiling until proven otherwise. Gold-futures speculators and their capital are finite, relatively small.

Out of all the world’s traders, only a tiny fraction are willing to run extreme 35x leverage and risk ruin on being slightly wrong on gold’s near-term direction. New gold highs really don’t mint sizable numbers of new gold-futures speculators either, as the risks are so crazy. And this small pool of gold-futures traders really don’t control much capital compared to broader markets. They’d be irrelevant without their extreme leverage.

So at some point gold-futures buying pressure literally exhausts itself. All the specs who want to be long gold have already bought in, expending all their available capital firepower. We can’t know in advance if it will happen at 375k longs, 400k, 425k, or 450k, but odds are it will be somewhere around there. Once the specs are all-in, all they can do is sell to start unwinding their excessively-bullish bets. That will hammer gold.

This relatively-young gold bull has seen three prior episodes where specs liquidated high longs, as seen in the falling green line above. Those were during this bull’s two corrections and a milder pullback in late 2018. Gold fell sharply each time, and this next episode of major spec long selling won’t prove different. At their latest 374.0k levels, spec longs are really high today with little room to buy and tons of room to sell!

The near-term gold risk is compounded by the fact spec shorts are also really low, just 87.2k contracts as of the last CoT report. That’s just a hair over the lowest levels of this entire bull market, 82.5k seen in late March 2018. So spec short-covering buying isn’t likely to go much lower, and in any case has a hard limit as these downside bets get closer to zero. Like spec long buying, spec short covering is largely exhausted.

Total spec gold-futures longs approaching bull-market and all-time-record highs, coupled with total spec gold-futures shorts just over bull-market lows, is very bearish for gold over the near-term! Remember by necessity these guys are short-term momentum followers, their extreme leverage will slaughter them if they are on the wrong side of gold for long. When gold noses over, their selling will intensify and cascade.

It certainly has the potential to snowball forcing another correction-grade gold selloff over 10%, which equates to a demoralizing sub-$1281 gold price. We might get lucky, the bullish new-high psychology could retard gold-futures selling. If the normalization of specs’ gold-futures bets is very slow, gold could see a milder pullback largely consolidating high. But we can’t bet on that based on all the bull-market precedent.

The greatest hope of gold evading a big selloff on gold-futures selling is investors returning in a big way. They control vastly more capital than the gold-futures speculators, so when they are buying aggressively that can easily absorb and overpower any gold-futures selling. But while new-high psychology has spawned some investment buying, it has only been sporadic so far with euphoric US stock markets near record highs.

Meanwhile traders should prepare for the next major gold selloff, possibly this gold bull’s third correction. That means tightening trailing stop losses on existing long positions in gold and the stocks of its miners. On stoppings, cash should be accumulated and not redeployed. It is simply too risky to add material new long positions in gold and gold stocks until speculators’ extreme gold-futures positioning considerably normalizes.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In recent months well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. This week their unrealized gains ran as high as 112.8%, 105.0%, and 95.2%!

You need to stay informed about gold cycles and gold-futures positioning to profitably trade the high-potential gold stocks. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! Then you’ll be ready to buy back in relatively low for gold’s next major upleg.

The bottom line is gold is at high risk for a major selloff today. Speculators’ gold-futures positioning has grown excessively-bullish, leaving their buying firepower largely exhausted. That leaves vast room for big selling to snowball on the right catalyst. This bull’s prior episodes where specs had similar really-high longs and really-low shorts heralded major gold corrections. Extreme bets must eventually be normalized.

Such corrections are normal and healthy within ongoing bull markets, rebalancing sentiment to ensure longer lives with greater ultimate gains. These corrections should be embraced, as they yield the very best opportunities to buy relatively low within powerful bulls. Gold’s current bull is likely to run for years yet, so gird yourself for a major selloff and be ready to buy back in aggressively once it has largely run its course.

Adam Hamilton, CPA

July 15, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

- While some gold stocks (the South Africans in particular) continue to rally, bullion and most miners are staging a classic pullback after a major upside breakout.

- Please click here now. Double-click to enlarge this important monthly gold chart. The bottom line:

- Breakouts are fun. Pullbacks are not!

- My advice to investors: Wait for the pain. Wait for emotional pain to begin before pressing the buy button on a pullback.

- Please click here now. Double-click to enlarge. I’ve highlighted key support zones on this daily gold chart, and the bottom line is this:

- The current pullback could end near $1380, $1360, or it could become quite a bit deeper before finally ending in the $1330-$1250 price zone.

- I don’t believe most gold investors are really prepared to handle a deeper pullback. Nervous investors should buy put options, not so much as a financial hedge but as an emotional hedge.

- A financial hedge is not required at this point in the U.S. business cycle, but any pullback can be emotionally troublesome. Investors need to do whatever it takes to handle the change in sentiment.

- Please click here now. Double-click to enlarge. On this daily gold chart, note the large uptrend channel and Fibonacci retracement lines from the 2018 August low.

- A “power uptrend” line has snapped and gold has only corrected down to the 76% retracement line area. A deeper correction is normal and healthy after the huge surge in the price after the monthly chart bull continuation breakout.

- Please click here now. Double-click to enlarge this dollar versus yen chart.

- The gold and the yen are risk-off currencies. The upside breakout in the dollar against the yen doesn’t guarantee a deeper correction for gold, but it does make it very likely.

- What are the fundamentals behind the gold price pullback and strength in the dollar against the yen?

- For the answer to that question, please click here now. I believe that both stock market and gold investors are over-estimating the Fed’s dovishness.

- Most institutional money managers are predicting a series of rate cuts and more QE from the Fed, but that’s not what the Fed’s dot plot or its chairman are indicating lies ahead.

- Friday’s U.S. employment report was strong and Trump has seemingly finally realized that his tariff tax tantrums are doing nothing but harm to global stock markets.

- In this situation, it’s very hard to see the Fed doing anything at the July 31 meeting other than a single quarter point “insurance” cut.

- While Poland’s central bank just bought almost 100 tons of physical gold, this is likely a “one-off” purchase and India’s fresh gold import tax hike came on the same day as the strong U.S. jobs report.

- The tax hike caught bullish analysts by surprise and adds to short-term pressure on the gold price.

- Investor tactics? Well, amateur investors should generally wait for a $100/ounce gold price sale before buying gold or silver. From the $1442 area highs, that would make the $1342 area a solid entry point. There’s not much else to do on the buy side until there is a $100/ounce price sale. It’s really that simple!

- Please click here now. Double-click to enlarge this weekly GDX chart. I called the $23-$18 price zone an important accumulation zone for investors.

- Those who took my strong buy recommendation can sell a small portion of their position now, but I recommend holding at least 70% of the position for an upside journey into my first target zone of $30-$32.

- I would not do any serious selling until GDX arrives in my second target zone of $38-$40. The main driver of a rally to that target zone will be a concerning rise in inflation that occurs as US corporate earnings and GDP growth continue to soften. The bottom line: Fed doesn’t need to cut nominal rates to make real rates fall in that situation. All it needs to do is…nothing! That’s because a rise in inflation with no change in nominal rates is a cut in real rates.

- The bottom line: I expect an institutional money manager stampede into GDX and key individual miners will occur later this year as stagflation rises to essentially become… a Grim Reaper made of gold!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Junior Champions In The Pullback Zone!” report. I highlight key junior miners that seem immune to the current gold price pullback and silver price gulag. They are blasting to fresh highs and I provide investors with key tactics to play the upside action!

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

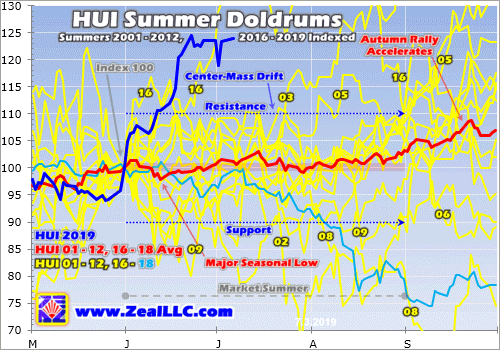

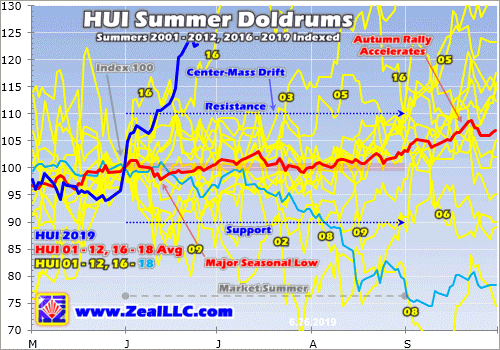

Gold’s incredible strength this summer is very unusual, as early summers are the weakest times of the year seasonally for gold, silver, and their miners’ stocks. With traders’ attention diverted to vacations and summer fun, interest in and demand for precious metals normally wane. So this entire sector tends to suffer a seasonal lull, along with the general markets. This June’s bull-market breakout is a momentous anomaly.

This doldrums term is very apt for gold’s usual summer predicament. It describes a zone in the world’s oceans surrounding the equator. There hot air is constantly rising, creating long-lived low-pressure areas. They are often calm, with little or no prevailing winds. History is full of accounts of sailing ships getting trapped in this zone for days or weeks, unable to make headway. The doldrums were murder on ships’ morale.

Crews had no idea when the winds would pick up again, while they continued burning through their limited stores of food and drink. Without moving air, the stifling heat and humidity were suffocating on these ships long before air conditioning. Misery and boredom were extreme, leading to fights breaking out and occasional mutinies. Being trapped in the doldrums was viewed with dread, it was a very trying experience.

Gold investors can somewhat relate. Like clockwork nearly every summer, gold starts drifting listlessly sideways. It often can’t make significant progress no matter what the trends looked like heading into June, July, and August. As the days and weeks slowly pass, sentiment deteriorates markedly. Patience is gradually exhausted, supplanted with deep frustration. Plenty of traders capitulate, abandoning ship.

Thus after decades of trading gold, silver, and their miners’ stocks, I’ve come to call this time of year the summer doldrums. Junes and Julies in particular are usually desolate sentiment wastelands for precious metals, totally devoid of recurring seasonal demand surges. Unlike much of the rest of the year, these summer months simply lack any major income-cycle or cultural drivers of outsized gold investment demand.

The vast majority of the world’s investors and speculators live in the northern hemisphere, so markets take a back seat to the great joys of summer. Traders take advantage of the long sunny days and kids being out of school to go on extended vacations, hang out with friends, and enjoy life. And when they aren’t paying much attention to the markets, naturally they aren’t allocating much new capital to gold.

Given gold’s dull summer action historically, it is never wise to expect too much from it this time of year. Summer rallies can happen, but they aren’t common. So expectations need to be tempered, especially in Junes and Julies. That early-1990s Gin Blossoms song “Hey Jealousy” comes to mind, declaring “If you don’t expect too much from me, you might not be let down.” The markets are ultimately an expectations game.

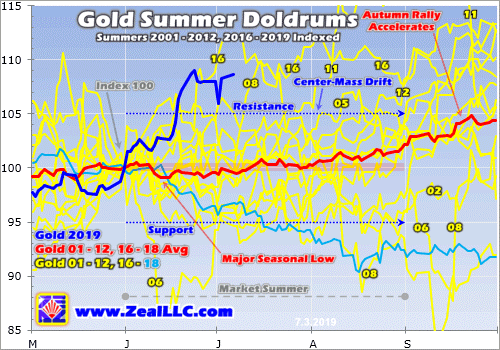

Quantifying gold’s summer seasonal tendencies during bull markets requires all relevant years’ price action to be recast in perfectly-comparable percentage terms. That is accomplished by individually indexing each calendar year’s gold price to its last close before market summers, which is May’s final trading day. That is set at 100, then all gold-price action each summer is recalculated off that common indexed baseline.

So gold trading at an indexed level of 105 simply means it has rallied 5% from May’s final close, while 95 shows it is down 5%. This methodology renders all bull-market-year gold summers in like terms. That’s necessary since gold’s price range has been so vast, from $257 in April 2001 to $1894 in August 2011. That span encompassed gold’s last secular bull, which enjoyed a colossal 638.2% gain over those 10.4 years!

Obviously 2001 to 2011 were certainly bull years. 2012 was technically one too, despite gold suffering a major correction following that powerful bull run. At worst that year, gold fell 18.8% from its 2011 peak. That was not quite enough to enter formal bear territory at a 20%+ drop. But 2013 to 2015 were definitely brutal bear years, which need to be excluded since gold behaves very differently in bull and bear markets.

In early 2013 the Fed’s wildly-unprecedented open-ended QE3 campaign ramped to full speed, radically distorting the markets. Stock markets levitated on the Fed’s implied backstopping, slaughtering demand for alternative investments led by gold. So in Q2’13 alone, gold plummeted 22.8% which proved its worst quarter in an astounding 93 years! Gold’s bear continued until the Fed started hiking rates again in late 2015.

The day after that first rate hike in 9.5 years in mid-December 2015, gold plunged to a major 6.1-year secular low. Then it surged out of that irrational rate-hike scare, formally crossing the +20% new-bull threshold in early March 2016. Ever since, gold has remained in this current bull. At worst in December 2016 after gold was crushed on the post-election Trumphoria stock-market surge, it had only corrected 17.3%.

So the bull-market years for gold in modern history ran from 2001 to 2012, skipped the intervening bear-market years of 2013 to 2015, then resumed in 2016 to 2019. Thus these are the years most relevant to understanding gold’s typical summer-doldrums performance, which is necessary for managing your own expectations this time of year. This spilled-spaghetti mess of a chart is fairly simple and easy to understand.

The yellow lines show gold’s individual-year summer price action indexed from each May’s final close for all years from 2001 to 2012 and 2016 to 2017. 2018’s is rendered in light blue. Together these establish gold’s summer trading range. All those past bull-market years’ individual indexes are averaged together in the red line, revealing gold’s central summer tendency. 2019’s indexed action is superimposed in dark blue.

While there are outlier years, gold generally drifts listlessly in the summer doldrums much like a sailing ship trapped near the equator. The center-mass drift trend is crystal-clear in this chart. The vast majority of the time in June, July, and August, gold simply meanders between +/-5% from May’s final close. This year that equated to a probable summer range between $1240 to $1370. Gold tends to stay well within trend.

Obviously this year has proven a huge exception to that normal summer rule, with gold rocketing higher to a major bull-market breakout! Gold blasted to its best early-summer performance ever seen in all modern bull-market years. Comparing this current summer’s dark-blue line to past years’ price action certainly drives home how unique, exceptional, and special gold’s breakout surge to major new secular highs has been.

Still, understanding gold’s typical behavior this time of year is important for traders. Sentiment isn’t only determined by outcome, but by the interplay between outcome and expectations. If gold rallies 5% but you expected 10% gains, you will be disappointed and grow discouraged and bearish. But if gold rallies that same 5% and you expected no gains, you’ll be excited and get optimistic and bullish. Expectations are key.

History has proven it is wise not to expect too much from gold in these lazy market summers, particularly Junes and Julies. Occasionally gold still manages to stage a summer rally, like this year’s monster. But most of the time gold doesn’t veer materially from its usual summer-drift trading range, where it is often adrift like a classic tall ship. With range breakouts either way uncommon, there’s often little to get excited about.

In this chart I labeled some of the outlying years where gold burst out of its usual summer-drift trend, both to the upside and downside. But these exciting summers are atypical, and can’t be expected very often. Most of the time gold grinds sideways on balance not far from its May close. Traders not armed with this critical knowledge often wax bearish during gold’s summer doldrums and exit in frustration, a real mistake.

Gold’s summer-doldrums lull marks the best time of the year seasonally to deploy capital, to buy low at a time when few others are willing. Gold enjoys powerful seasonal rallies that start in Augusts and run until the following Mays! These are fueled by outsized investment demand driven by a series of major income-cycle and cultural factors from around the world. Summer is when investors should be bullish, not bearish.

The red average indexed line above encompassing 2001 to 2012 and 2016 to 2018 reveals gold’s true underlying summer trend in bull-market years. Technically gold’s major seasonal low arrives relatively early in summers, mid-June. On average through all these modern bull-market years, gold slumped 0.9% between May’s close and that summer nadir. But seasonally that’s still on the early side to deploy capital.

Check out the yellow indexed lines in this chart. They tend to cluster closer to flatlined in mid-June than through all of July. The only reason gold’s seasonal low appears in mid-June mathematically is a single extreme-outlier year, 2006. The spring seasonal rally was epic that year, gold rocketed 33.4% higher to a dazzling new bull high of $720 in just 2.0 months between mid-March to mid-May! That was incredible.

Extreme euphoria had catapulted gold an astounding 38.9% above its 200-day moving average, radically overbought by any standard. That was way too far too fast to be sustainable, so after that gold had to pay the piper in a sharp mean-reversion overshoot. So over the next month or so into mid-June, gold’s overheated price plummeted 21.9%! That crazy outlier is the only reason gold’s major summer low isn’t later.

There were 15 bull-market years from 2001 to 2012 and 2016 to 2018. That is a big-enough sample to smooth out the trend, but not large enough to prevent extreme deviations from skewing it a bit. Gold sees a series of marginally-higher lows in late June, early July, and even late July. In this dataset they came in 0.0%, 0.3%, and 0.8% higher than mid-June’s initial low. And that last late-July one arrives over 6 weeks later.

So generally there’s no hurry to deploy capital right at that initial mid-June seasonal low. Gold tends to drift nearly flatlined over the next several weeks into early July, trying traders’ patience. Buying within a few trading days of the US Independence Day holiday seems to have the best odds of catching gold near its summer-doldrums lows. Investment capital inflows usually begin ramping back up after that as traders return.

On average in these modern bull-market years, gold slipped 0.4% in Junes before rallying 0.7% in Julies. After July’s initial lazy summer week, gold tends to gradually start clawing its way back higher again. But this is so subtle that Julies often still feel summer-doldrumsy. By the final trading day in July, gold is still only 0.3% higher than its May close kicking off summers. That’s too small to restore damaged sentiment.

Since gold exited May 2019 at $1305, an average 0.3% rally by July’s end would put it at $1309. That’s hardly enough to generate excitement after two psychologically-grating months of drifting. But the best times to deploy any investment capital are when no one else wants to so prices are low. Gold’s summer doldrums come to swift ends in Augusts, which saw hefty average gains of 1.9% in these bull-market years!

And that’s just the start of gold’s major autumn seasonal rally, which has averaged strong 5.7% gains between mid-Junes to late Septembers. That is driven by Asian gold demand coming back online, first post-harvest-surplus buying and later Indian-wedding-season buying. June is the worst of gold’s summer doldrums, and the first half of July is when to buy back in. It’s important to be fully deployed before August.

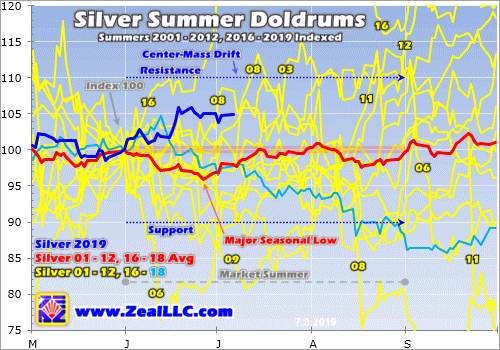

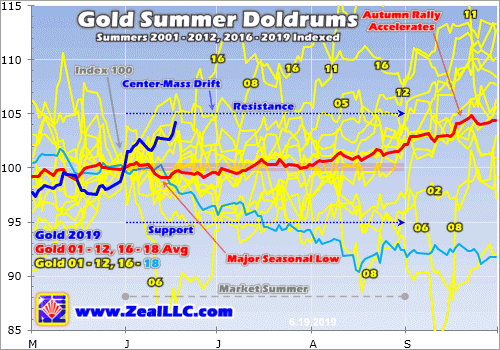

These gold summer doldrums driven by investors pulling back from the markets to enjoy their vacation season don’t exist in a vacuum. Gold’s fortunes drive the entire precious-metals complex, including both silver and the stocks of the gold and silver miners. These are effectively leveraged plays on gold, so the summer doldrums in them mirror and exaggerate gold’s own. Check out this same chart type applied to silver.

Since silver is much more volatile than gold, naturally its summer-doldrums-drift trading range is wider. The great majority of the time, silver meanders between +/-10% from its final May close. That came in at $14.56 this year, implying a summer-2019 silver trading range between $13.10 to $16.02. While silver suffered that extreme June-2006 selling anomaly too, its major seasonal low arrives a couple weeks after gold’s.

Given gold’s spectacular bull-market-breakout surge last month, silver’s summer performance this year has been utterly dismal. Normally silver amplifies gold upside by at least 2x. But silver has been bombed out and languishing for so long that investors and speculators still want nothing to do with it. Silver often acts as a gold sentiment gauge, and gold hasn’t been over $1400 long enough yet to shift psychology to bullish.

On average in these same gold-bull-market years of 2001 to 2012 and 2016 to 2018, silver dropped 4.1% between May’s close and late June. That is much deeper than gold’s 0.9% seasonal slump, which isn’t surprising given silver’s leverage to gold. Silver’s summer performances are also much lumpier than gold’s. Junes see average silver losses of 3.2%, but those are more than erased in strong rebounds in Julies.

Silver’s big 3.6% average rally in Julies amplifies gold’s gains by an impressive 5.1x! But unfortunately silver hasn’t been able to maintain that seasonal momentum, with Augusts averaging a modest decline of 0.7%. Overall from the end of May to the end of August, silver’s summer-doldrums performance tends to drift lower. Silver averaged a 0.4% full-summer loss, way behind gold’s 2.2% gain through June, July, and August.

That means silver sentiment this time of year is often worse than gold’s, which is already plenty bearish. The summer doldrums are more challenging for silver than gold. Being in the newsletter business for a couple decades now, I’ve heard from countless discouraged investors over the summers. While I haven’t tracked this, it sure feels like silver investors have been disproportionally represented in that feedback.

Since gold is silver’s primary driver, this white metal is stuck in the same dull drifting boat as gold in the market summers. Silver usually leverages whatever is happening in gold, both good and bad. But again the brunt of silver’s summer weakness is borne in Junes. Fully expecting this seasonal weakness and rolling with the punches helps prevent getting disheartened, which in turn can lead to irrationally selling low.

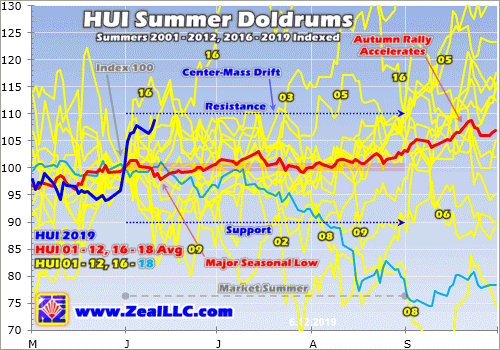

The gold miners’ stocks are also hostage to gold’s summer doldrums. This last chart applies this same methodology to the flagship HUI gold-stock index, which mostly closely mirrors that leading GDX VanEck Vectors Gold Miners ETF. The major gold stocks tend to amplify gold’s gains and losses by 2x to 3x, so it is not surprising that the HUI’s summer-doldrums-drift trading range is also twice as wide as gold’s own.

The gold miners’ stocks share silver’s center-mass summer drift running +/-10% from May’s close. This year the HUI entered the summer doldrums at 157.1, implying a June, July, and August trading range of 141.4 to 172.8. While gold stocks’ GDX ETF is too young to do long-term seasonal analysis on, in GDX terms this summer range translates to $19.43 to $23.75 this year. That’s based off a May 31st close of $21.59.

Thanks to gold’s dazzling bull-market breakout, gold stocks have defied these weak summer seasonals this year to soar to their own major decisive breakout! This high-potential contrarian sector has enjoyed its best early-summer performance ever witnessed in gold’s modern bull-market years. While I hope this incredible outperformance persists, the summer doldrums could still reassert themselves if gold retreats.

Like gold, the gold stocks’ major summer seasonal low arrives in mid-June. On average in these gold-bull-market years of 2001 to 2012 and 2016 to 2018, by then the HUI had slid 2.1% from its May close. Then gold stocks tended to more than fully rebound by the end of June, making for an average 0.6% gain that month. But there is no follow-through in July, where the gold stocks averaged a modest 0.5% loss.

Overall between the end of May and the end of July, which encompasses the dark heart of the summer doldrums, the HUI proved dead flat on average. Again two solid months of grinding sideways on balance is hard for traders to stomach, especially if they’re not aware of the summer-doldrums drift. The key to surviving it with minimum psychological angst is to fully expect it. Managing expectations in markets is essential!

But also like gold, the big payoff for weathering the gold-stock summer starts in August. With gold’s major autumn rally getting underway, the gold stocks as measured by the HUI amplify it with good average gains of 3.1% in Augusts! And that’s only the start of gold stocks’ parallel autumn rally with gold’s, which has averaged 9.3% gains from late Julies to late Septembers. Gold-stock upside resumes in late summers.

Like much in life, withstanding the precious-metals summer doldrums is less challenging if you know they’re coming. While outlying years happen, they aren’t common. So the only safe bet to make is expecting gold, silver, and the stocks of their miners to languish in Junes and Julies. Then when these drifts again come to pass, you won’t be surprised and won’t get too bearish. That will protect you from selling low.

The precious-metals sector radically bucked its seasonal-slump trend this year, surging to a record start. Gold began blasting higher on May’s final trading day, and that sharp rally carried into early June. New trade-war tariff threats were ramping up market fears, driving the US stock markets to selloff lows following late April’s all-time record highs. So traders remembered diversifying with gold and flocked back to it.

In mid-June gold’s gains accelerated after the Fed reversed its future-rate outlook from hiking back to cutting. That propelled gold to its first new bull-market highs in 3.0 years, with it surging to a 5.8-year secular high on that late-June breakout day. That momentum fed on itself and carried gold back over $1400 for the first time since early September 2013. Those awesome $1400+ levels have mostly held since.

The gold miners’ stocks naturally leveraged gold’s gains, enjoying their own epic early-summer action. The precious-metals sector is doing wildly better than last summer, when gold rolled over in mid-June on a sharp US dollar rally. Hyper-leveraged gold-futures speculators watch the dollar’s fortunes for trading cues. Hopefully gold’s huge early-summer gains can hold, and it consolidates sideways in coming weeks.

Gold’s massive and exceptional June rally was mostly fueled by speculators buying enormous quantities of gold futures. That has largely exhausted their available capital firepower, and left their collective bets on gold exceedingly bullish. These positions must be partially unwound with selling, which forces gold into a high consolidation at best and a sharp selloff at worst. So gold isn’t out of the summer-doldrums woods yet.

The inevitable coming gold-futures selling could be largely offset by investment buying. Investors are radically underinvested in gold after the second-largest and first-longest stock bull in US history, giving them big room to buy to reestablish normal portfolio allocations. Since they love chasing winners, gold’s powerful new-high psychology is starting to attract them back. Their return could dwarf gold-futures selling.

Given gold’s long-established lackluster summer-doldrums performance record, it is probably not prudent to chase this rally with gold-futures speculators effectively all-in longs and all-out shorts. But the metal and its miners’ stocks can be accumulated aggressively on any significant weakness. All portfolios need a 10% allocation in gold and gold stocks! Far-more upside is coming after recent overboughtness is worked off.

One of my core missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with superior fundamentals and upside potential. The trading books in both our popular weekly and monthly newsletters are currently full of these better gold and silver miners. Mostly added in recent months as gold stocks recovered from selloffs, their unrealized gains were already running as high as +105% this week!

If you want to multiply your capital in the markets, you have to stay informed. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q1 we’ve recommended and realized 1089 newsletter stock trades since 2001, averaging annualized realized gains of +15.8%! That’s nearly double the long-term stock-market average. Subscribe today and take advantage of our 20%-off summer-doldrums sale!

The bottom line is gold, silver, and their miners’ stocks usually drift listlessly during market summers. As investors shift their focus from markets to vacations, capital inflows wane. Junes and Julies in particular are simply devoid of the big recurring gold-investment-demand surges seen during much of the rest of the year, leaving them weak. Investors need to expect lackluster sideways action on balance this time of year.

This summer has proven an epic exception, with gold rocketing to its first major bull-market breakout in years! That has catapulted both the metal and its miners’ stocks to their best early-summer performances in gold’s modern bull-market years. But the summer doldrums could still reassert themselves as specs’ excessively-bullish gold-futures bets are bled off. So enjoy these big anomalous gains, but remain wary.

Adam Hamilton, CPA

July 8, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

- Major fundamental processes and events create the large chart patterns seen on the monthly charts. It’s important for gold and stock market investors to stay focused on the big picture, both technically and fundamentally.

- To view the big technical picture for gold, please click here now. Double-click to enlarge.

- Since 2001, my proprietary weekly chart signals system has only generated five buy signals for gold bullion. Note the similarity of the latest one with the 2009 signal.

- The current signal happens with India just days away (July 5) from a possible gold tariff tax cut as part of its new budget, and the July 31 Fed meeting only a month away.

- I’ve put the odds of a gold tariff tax cut at about 50%. To view key news related to the US business cycle, please click here now. The Dow gave back most of its early morning gain yesterday, after rising on the news that Trump would temporarily halt his tariff tax bombing runs on the stock markets, corporations, and working class of America.

- Over the long term, the only way for conservative governments to compete with handouts-focused liberals at the voting polls is with working class tax cuts. By refusing to cut income taxes for America’s working class, Trump risks losing the 2020 election.

- He is now rumoured to be considering a capital gain tax cut (for stock market elitists) instead of an income tax cut for the poor. That’s going to drive more blue-collar voters towards the democrats.

- With US corporate earnings and America’s working class now looking a lot like drowning passengers on the Titanic, gold is the obvious “choice of champions”.

- To view another key big picture chart for this mighty asset, please click here now. Double-click to enlarge.

- After a major upside breakout from an enormous bullish chart pattern, a pullback is expected and normal. The bigger the chart pattern is, the bigger the pullback can be.

- Gold could easily pull back to the $1320-$1250 price zone before roaring on towards my $1550 and $2000 price targets. That shouldn’t bother investors because this type of pullback action is typical after a major breakout.

- Regardless, a shallow pullback would obviously be preferred by most gold market investors and that’s also a realistic scenario.

- Please click here now. Double-click to enlarge. There is a bull flag in play on the daily gold chart.

- A cut in India’s gold tariff tax on Friday would be the likely catalyst for an upside breakout from the flag pattern. If there is no cut, a deeper correction would likely ensue. In that scenario, gold would probably pull back to at least $1360, but more likely to $1320-$1250 by the July 31 Fed meet.

- Please click here now. There’s a lot of talk about the gold versus silver ratio right now. Silver investors should exercise caution before racing in to buy silver just based on the level of the ratio. Here’s why:

- If Trump blows the 2020 election, America could quickly become a socialist state. Stock markets would incinerate and silver (an industrial metal) could fall further against gold on the ratio chart until inflation became obvious.

- Also, the monsoon season in India isn’t going well. It’s a mini-disaster now, and it could soon become a full disaster. If the crop harvest is horrific, Indian farmers won’t have additional money to buy physical silver bullion.

- They will likely just buy the gold they need to meet their needs for religious festivals and weddings. That will put even more upside pressure on the gold/silver ratio.