GoGold Resources (GGD.TO, C$0.71) is a company with assets in Mexico, both a producing and an exploration-stage project. Led by a management team that has over 27 years of experience in the country. The team developed 4 projects/companies that eventually got sold with at a good to hefty premium. Examples are: Gammon Gold ($1.5B merge with Alamos), Mexgold (sold for $375M), Nayarit ($80M, bought for $40M) and recently, the Santa Gertrudis project they sold to AEM for $96M (bought for $11M).

CEO Brad Langille is the second largest shareholder and holds 9.5% of outstanding shares. Biggest shareholder is Fred George, who was founding member of Gammon Gold. He led the development of the Ocampo project from exploration stage to one of the biggest silver and gold projects in Mexico, currently operated by Minera Frisco. Fred George owns about 14% of outstanding shares. Management combined owns over 30%.

Financial position is strong as they had C$9M in liquidity (cash + Metalla shares) at the end of the second quarter. After finishing the sale of the Santa Gertrudis project, they decided to pay off their remaining debt which leaves them debt-free.

Parral

After the sale of Santa Gertrudis, GoGold has two projects left. One of them is the young producing heap leaching mine of Parral, which is right next to the Mexican city of Chihuahua. This mine started its fifth year and is currently on a record streak: For the second consecutive quarter a beat in production and well on its way to reach 1.8Moz of silver equivalent. AISC is declining and currently sits at US$13.61/oz. Their realized silver price for the quarter was US$14.55, which gave them a 6.9% margin in Q2. As silver is a lot higher now than in Q2, we can assume a conservative realized price of US$17/oz for Q3. If AISC remains the same, their margin would rise to 24.9% or an increase of 261% quarter over quarter.

In June of this year, the company announced the build of a SART installation at their Parral mine. This will help lower costs of heap leaching and provide a saleable copper concentrate. This plant will see its first full operational quarter in Q1 of 2020. This should give a substantial decrease in AISC and add some revenue through the copper concentrate.

Their Parral mine will allow them to internally finance their exploration. Shareholders are protected from dilution through capital raises. In coming quarters, production will continue to rise towards 550-600Koz AgEq. Q2 saw 440Koz so we can expect further “records” in coming headlines. During my contact with management I received the following words:

“The cashflow we produce form Parral will fund our operations, G&A, and our exploration at Los Ricos and this is why we say we are a self-funding junior and do not need to raise money for the foreseeable future.”

Parral has a remaining mine life of 8 years and the proportion silver/gold in dollar value is about 55% silver and 45% gold. So despite of what you might read in their name, GoGold is mostly a silver producer.

Los Ricos

The Los Ricos project is my main reason to hold GoGold in my portfolio. The project has seen commercial production between 1908-1929. Production has been terminated at the start of the Great Depression. At the time of production, they kept track of the production data. Through this data we learn that the project was mined to a depth of 500m on different levels. Average values of 800g/t silver and 4g/t gold.

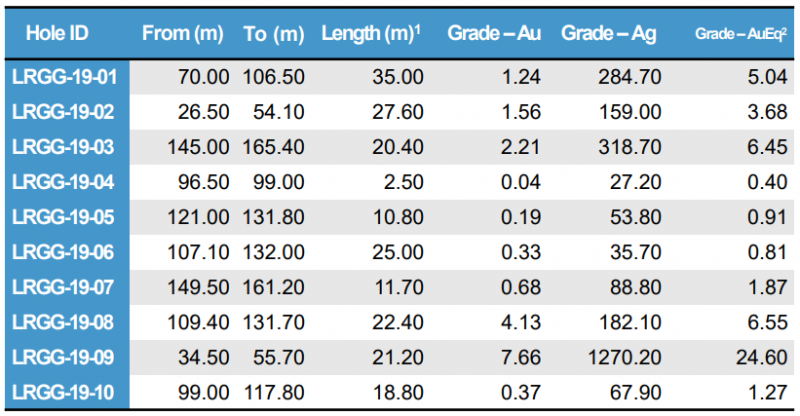

The project has about 65 historic drill results, which GoGold is trying to confirm with their own drill program. Up until today, they are succeeding well in this. Best hit: 21m of 7.66g/t gold and 1,270g/t silver (or 21m of 24.6g/t AuEq). Below I added the results of the first 10 drill holes by GoGold. Note that these are all 10 of them and not one has been left out mysteriously. By now the project has expanded to 37 drill results. I looked at all of these: Not one miss and on average thick mineralization with high values of gold and silver.

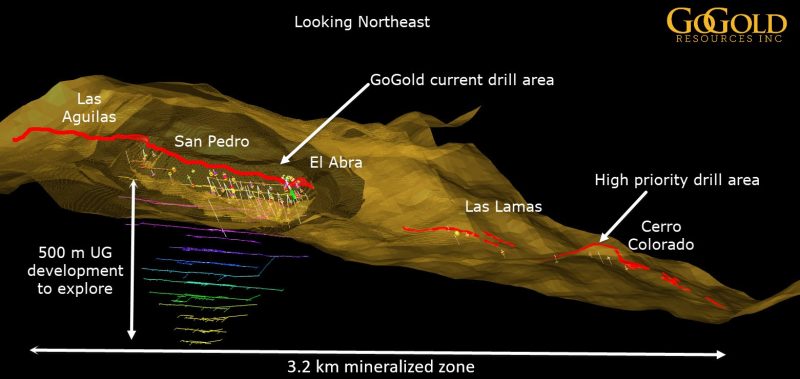

I recently felt an urgency to buy this company and this had nothing to do with silver taking off. In May, the company announced trenching results from a 3.2km strike. In this news release, GoGold told investors they would move a drill to the Cerro Colorado zone. This area has the ‘high priority drill area’ tag attached in the image below. Cerro Colorado is at the end of this strike and 1,500m away from the edge of the main zone.

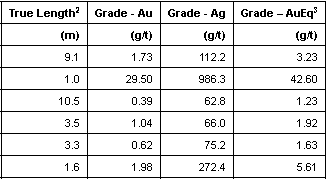

These first results of the Cerro Colorado zone seem to point to a big system. All 7 of these drill results show more high grade and thick gold and silver mineralization. As you can see in the image (above), there’s the ‘Las Lamas’ zone in between that 1,500m stepout. Below you find the results of the trenching GoGold did there. Management confirmed they would drill that target as well.

Since GoGold purchased the Los Ricos project, their share price has tripled. The silver price is largely a cause of this, but nonetheless an outperformance in the silver space. The Los Ricos project is a mere 6 months in their posession and the market is starting to notice. Should be, considering these drill results and potential. CEO Brad Langille recently noted that he’s been following this project for over 8 years and feels this is the most exciting project of his carreer. Talk is cheap of course, but seeing he upped his stake by 500,000 shares this year, is reason to take note.

The company is working on a maiden resource for Los Ricos, which they plan on delivering in the first quarter of 2020. Recently, they uploaded a VRIFY model on their website (link: https://gogoldresources.com/properties/los-ricos). CEO Langille wants to roll out this project on the Precious Metals Summit and Denver Gold Forum. Personally I believe this company will get some interest over the course of the next weeks. These presentations should be the start of this.

CEO Langille sees the Los Ricos project as an open pit mine with multi million ounces of high grade gold and silver. According to him this will be of similar, if not bigger size than the Ocampo mine which he helped build and eventually was valued at US$750M. Again, quotes like these are only to be given weight if supported by elevated insider ownership and preferably insider open market purchases. I see both here.

There’s only 1 analyst following this. HC Wainwright that has a current price target of C$0.80/share. Note that this is based on a realized silver price of US$15/oz, gold price of U$1,300 and doesn’t ascribe any value to the Los Ricos project.

Conclusion

- I upped my stake in this company after their Cerro Colorado drill results. I’m comfortable here because of the following reasons:

- Management with proven track record and a lot of their own money in the company

- A producing asset which is seeing rising production and margins

- No need for financing so no dilution

- Big players have to buy in the market, which was confirmed by management

- Los Ricos could be a world class deposit

- Lots of catalysts nearby:

exploration results - promotion of Los Ricos

- rising earnings at ParrJonas De Roose

September 18, 2019

- Is the gold price reaction over?

- Well, since the rally began in the $1170 area, corrections have not lasted very long.

- After rallying to the $1566 area, gold has pulled back to about $1500. Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10gold1.png Double-click to enlarge. Strong trend line support is already in play.

- Investors need to keep an open mind; it’s possible that the $1500 area is now support rather than resistance, and gold is set to rally towards the $1600-$1700 area.

- Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10gold2.png Double-click to enlarge. Note the lows in the $1526 area in the 2011-2012 timeframe.

- Those lows may now be functioning as support as gold reacts from the $1566 area highs. Also, $1500 is a key round number that may now be functioning as support rather than resistance for institutional money managers.

- Indian festival buying may be picking up as well. Indians have been waiting for a decent pullback for months, and now it is here.

- Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10trustydusty.png Double-click to enlarge this GDX swing trade chart.

- I recommend that most gold investors should consider allocating some capital to a swing trade program.

- My guswinger.com system has been in DUST-NYSE as GDX been “spanked”, and it’s now time to book solid profit on at least a portion of the position.

- Note the key low on the GDX chart at $27.61. If it’s violated, GDX could decline to the $26.04 area. Having said that, proper tactics can reduce investor risk dramatically.

- My suggestion to core position enthusiasts is to buy some gold stock now, and more if there is a deeper reaction. A stop order can be placed just under the $27.61 low.

- Investors who don’t like stops can also buy the $27.61 area…with very small size.

- Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10gdx1.png Double-click to enlarge. If the inverse H&S bottom on this weekly GDX chart is legitimate, the current reaction is likely to be very shallow and may already be ending.

- The target of the pattern is about $50. The biggest risk investors face now is not drawdowns, but rather missing out on a major run higher in most of the world’s quality miners!

- Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10trade1.png The global economy continues to weaken, and politicians do nothing but spend, borrow, and beg for more QE and negative rates.

- That’s pouring gas on the fire. Negative rates and QE incentivize governments to go even deeper into debt.

- Please click here now: “In the next credit cycle downturn, then, the generally lower credit quality of today’s speculative-grade population means that the default count could exceed the Great Recession peak of 14% of all rated issuers….” – Christina Padgett, Moody’s VP, Sep 9, 2019.

- This is spectacular news for gold!

- Please click here now: https://gracelandupdates.com/wordpress/wp-content/uploads/2019/09/2019sep10gdxj1.png Double-click to enlarge this GDXJ chart.

- As expected, GDXJ looks a bit more vulnerable than GDX in the short-term. Having said that, it’s important for investors to be as open to a surge above $43 as to a pullback to $33-$35.

- An upside breakout would open the door to a massive run higher, and whether investors pay a “ticket price” of $33 or $43 for their GDXJ ride really doesn’t matter.

- The rise of China and India is not going away. The decline of the West is not going away. These forces are destabilizing the dollar and ushering in a bull era for gold, silver, and associated miners.

- It’s no longer as important to avoid price reactions as it is to stay invested and buy breakouts. As stagflation grows, this gold market will become very similar to the 1970s market… on a much bigger scale!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Super Seniors On The Move” report. I highlight key senior miners that are trading under $20 that are showcasing fabulous relative strength versus the gold ETFs. I include important wealth building tactics for investors!

Stewart Thomson

September 11, 2019

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

A few weeks ago we wrote that precious metals were at risk of a correction.

First, they powered higher. But last week they ran into technical resistance levels that date back well beyond only a few years.

This is true for Gold, Silver as well as the miner ETFs: GDX and GDXJ.

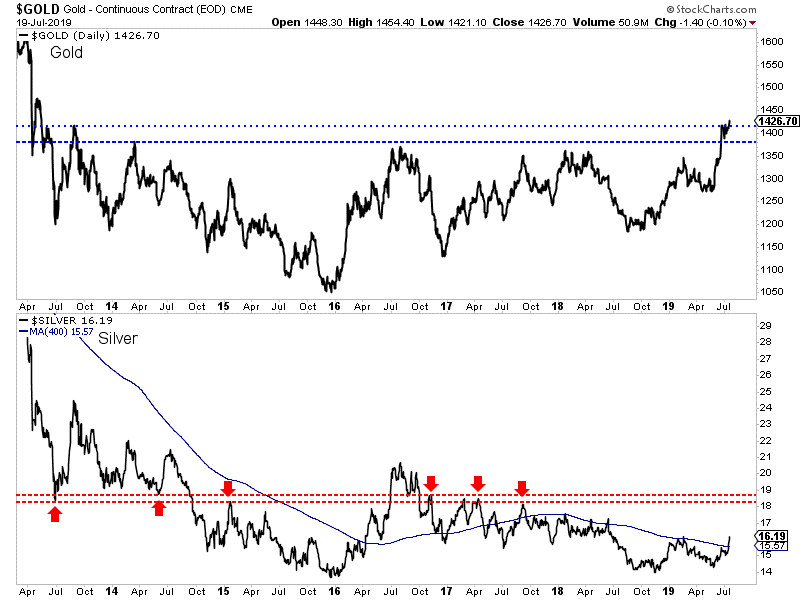

Starting with Gold, we can see that it has struggled to get through $1550/oz. That’s not a surprise as we pointed out this level as resistance since Gold surpassed $1370/oz.

The combination of multi-year resistance at $1550/oz and the current high net speculative position could force Gold down to a retest of $1400/oz.

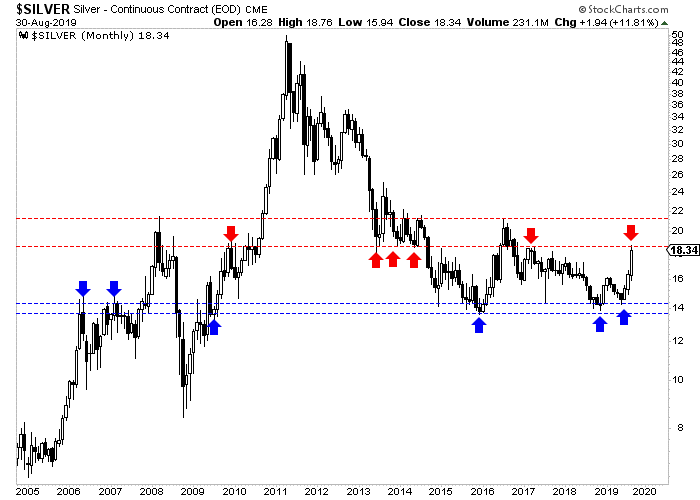

Meanwhile, Silver has been the strongest component of the sector in the short-term.

It closed the month of August right at major resistance in the mid $18s, which as you can see, has been a key level for the last 11 years. A monthly close above $18.50 would be significant but it may not happen until October or November.

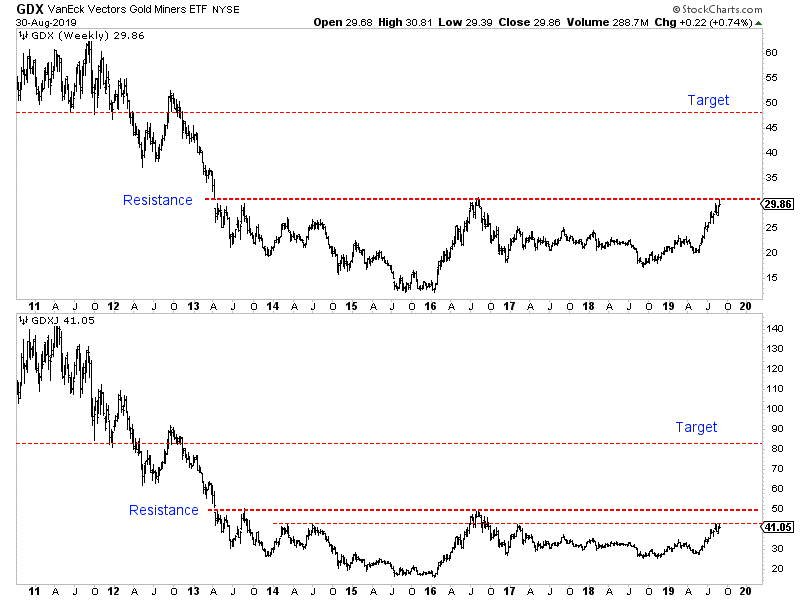

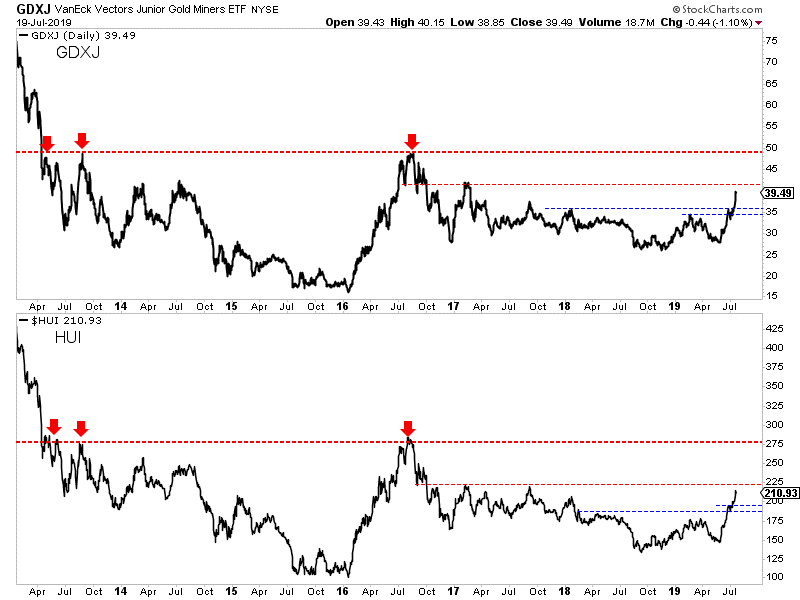

Turning to the stocks, we see that GDX has reached its 2016 high and 6-year resistance. A correction or consolidation for weeks or even a few months would be perfectly normal.

GDXJ has lagged much like Silver as it has yet to reach its 2016 high near $50. However, it is dealing with important resistance at $42 which dates back to 2014.

As summer winds down, the excitement in precious metals is building.

The retail crowd is looking to jump back in for the first time in years and the same can be said for many institutions.

In the big picture, this is the time to jump back in. You do want to get in before the sector makes its next break higher and before GDX and GDXJ surpass multi-year resistance.

However, the immediate risk appears to be to the downside.

Gold, Silver and gold stock ETFs all are at multi-year resistance levels. A correction and consolidation is perfectly normal and should be expected here.

If you missed the recent run then don’t panic. It’s best to exercise patience and wait for weakness. Better value and new opportunities will emerge. To learn the stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

By Jordan Roy-Byrne CMT, MFTA

September 5, 2019

Back during the bear market years (it’s nice to be able to write that now), I regularly would compare the declines in Gold, Silver and gold stocks to their past history. It gave us a visual representation of just how bad the forever bear market was and helped us decipher when it might end.

Thankfully that is all behind us.

Now it’s time to compare recent bullish moves to past iterations.

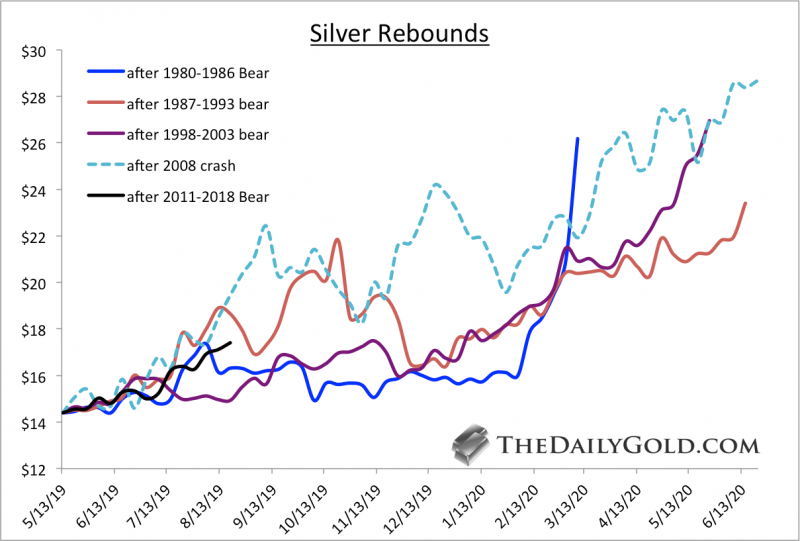

First is Silver.

The recent low in Silver has several good comparisons, which include the lows in 1986, 1993 and 2003. We also included the 2008 low.

If Silver’s rebound were simply an average of the four rebounds shown then it would reach nearly $24 by the end of March 2020.

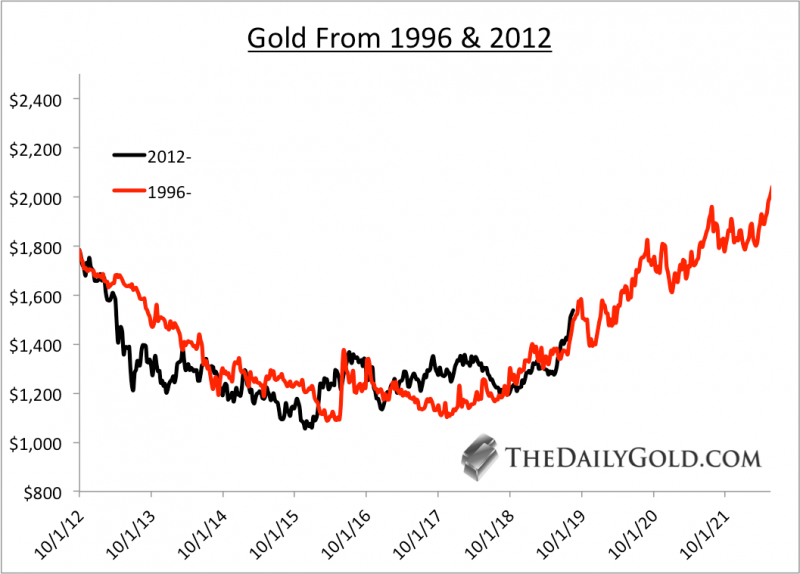

Gold is tricky because there is not an obvious bull comparison. Its major lows were essentially in 1970, 1985 and 1999 to 2001.

However, when we consider the preceding bear market, the best comparison to the recent bear and current bull is the late 1990s and early 2000s.

Mind you, we aren’t forecasting or predicting that 2003 to 2006 will be duplicated over the next three years. It’s possible, but we are simply arguing that the 2012 to 2019 period most resembles 1996 to 2003.

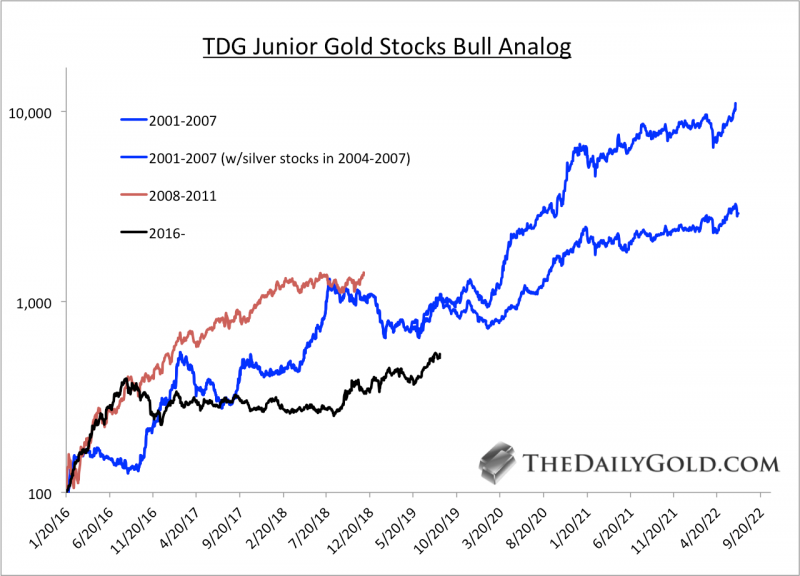

Turning to the gold stocks and specifically the junior gold stocks, here is how the 2016 bottom compares to the bottoms in 2001 and 2008.

Note that the basket of 20 stocks we used is quite strong compared to GDXJ. In other words, we erred on the side of positive performance.

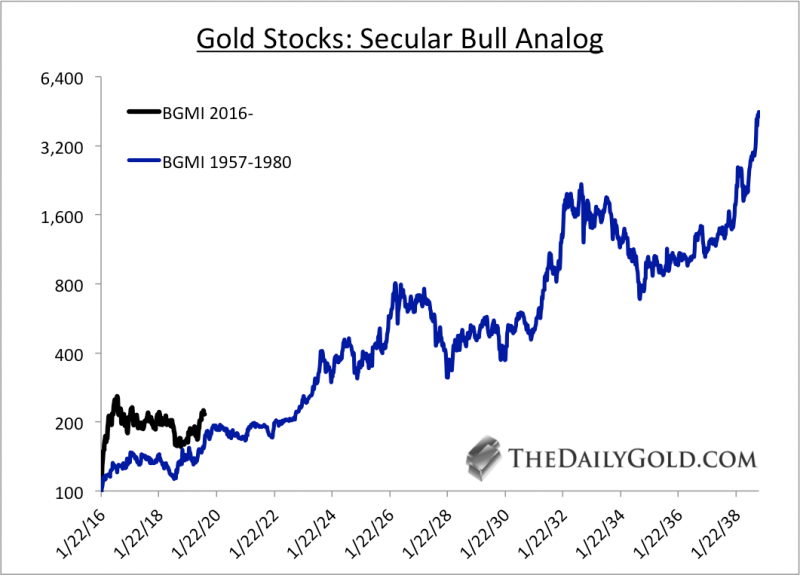

In our new book (available at TheDailyGold.com), we argue that the 2016 low in gold stocks was very similar to the 1957 low.

There are numerous similarities between today and the early to mid 1960s. That includes the gold stocks and their incredible long-term value at the start of a major inflationary cycle.

Below we compare the 1957 and 2016 lows with data from the Barron’s Gold Mining Index, which appreciated over 40-fold from its 1957 low to the peak in 1980.

As you can see, if Gold remains in a real bull market then significant upside potential remains in place across the precious metals complex.

Fundamentally, Gold could remain in a bullish trend until the next economic recovery gains traction. That could be anywhere from a few to four years away.

If gold continues to follow the pattern of the early 2000s then it could reach $3000/oz by the start of 2023.

Jordan Roy-Byrne CMT, MFTA

August 28, 2019

- A year ago, I predicted that any U.S. stock market sell-off would be accompanied by a dramatic surge in the price of GDX an GDXJ.

- That’s exactly what happened; the stock market tanked and key gold stocks soared.

- This year, I’m predicting that any major U.S. stock market crash will again be accompanied by the soaring price of the gold producers…

- But I’m also predicting that most CDNX-listed junior explorers are set to soar too!

- Please click here now. America’s top money printing cheerleader (President Trump) brags that his government essentially has the Chinese government cowering in a corner. He claims they are ready to throw in the white towel in the trade war. Reality check:

- It’s obvious that major money managers are becoming very concerned about these tariff taxes.

- Please click here now. Double-click to enlarge this horrifying U.S. stock market chart.

- On the one hand, private enterprise must be respected. Great companies exist and prosper in the socialist nations of Europe and in China. They will continue to prosper.

- The drive of entrepreneurs must never be underestimated, even in the harshest conditions.

- On the other hand, when governments unveil growth-negative policies like tariff taxes and money printing, stock markets can experience dramatic declines. These declines are usually temporary, but they are very painful.

- Please click here now. Double-click to enlarge this important gold stocks versus gold chart.

- I call it the “Just buy” chart, because there really isn’t much else to do here except buy, buy, and buy!

- That’s especially true for core position enthusiasts. Gold stocks are incredibly cheap compared to gold bullion.

- Also, I believe investors can make the most money in the market buying when their analysis has gone awry. On that note, please click here now. Double-click to enlarge my “Golden Beeline” chart.

- Many gold analysts have tried to “top call” gold since the rally from about $1167 began. This has been a mistake and I believe it will continue to be a mistake in the months ahead.

- A gargantuan bull continuation pattern is forming on the weekly gold chart. It’s an inverse H&S pattern with a potential neckline in the $2000 area.

- This is not a time to sell gold or top call it. It’s a time to buy, sit back, and watch those positions fly! Here’s why:

- Institutional money managers are adding gold to their portfolios. These are not highly leveraged hedge funds gambling on the COMEX.

- They are unleveraged institutions. They are serious players who understand the destructive nature of the Trump tariff taxes. These taxes are being implemented as the business cycle peaks and with relentless ramp-up of U.S. government spending and debt.

- This horrifying scenario has superstar managers like Ray Dalio predicting serious inflation and potential rioting in the streets.

- Please click here now: Top money managers are concerned that stagflation is emerging as the Fed is forced to print money and cut rates to offset the taxes. They are not buying gold, silver, and the miners for a “quick flip”. This is long-term allocation.

- Please click here now. Double-click to enlarge this fabulous GDX chart.

- Profit-lock enthusiasts can buy a breakout over $30 and place a stoploss at $27.50. A move above $30 opens the door for a violent surge to $37-$39.

- From there, core positions can be added on a pullback to about $30. Nervous investors can buy put options to manage their emotions, but everyone else should be in “Buy & Fly!” mode alongside the institutional money managers. Today’s Superman is a man of gold and looking at GDX today, I believe he would say… Up, up, and away!

Special Offer For Website Readers: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “Golden Junior Rockets!” report. I highlight junior miners trading under $2/share that are beginning to soar, with key buy and sell prices for each stock.

Thanks,

Stewart Thomson

Graceland Updates

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

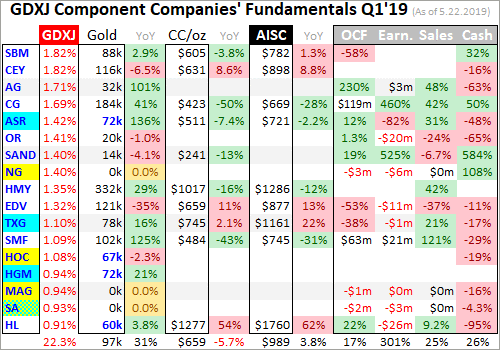

The mid-tier gold miners’ stocks have soared in recent months on gold’s decisive bull-market breakout. They are this sector’s sweet spot for stock-price upside potential, with room for strong production growth which investors love. That’s an attractive contrast to the stagnating major gold miners. The mid-tiers’ recently-reported Q2’19 results reveal whether their fundamentals justify their strong surge this summer.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

The global nature of the gold-mining industry complicates efforts to gather this important data. Many mid-tier gold miners trade in Australia, Canada, South Africa, the United Kingdom, and other countries with quite-different reporting requirements. These include half-year reporting rather than quarterly, long 90-day filing deadlines after year-ends, and very-dissimilar presentations of operating and financial results.

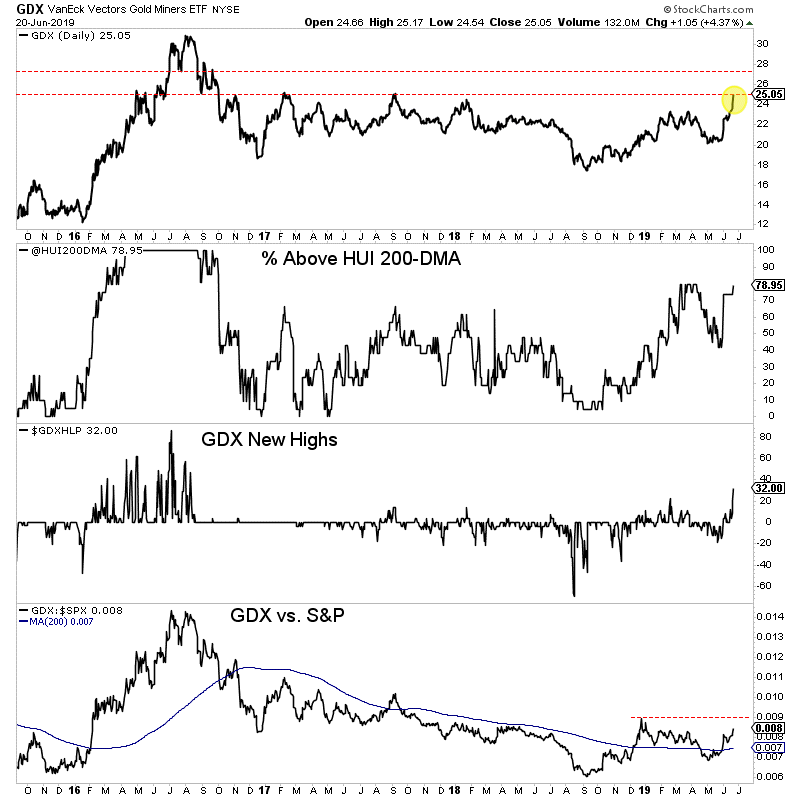

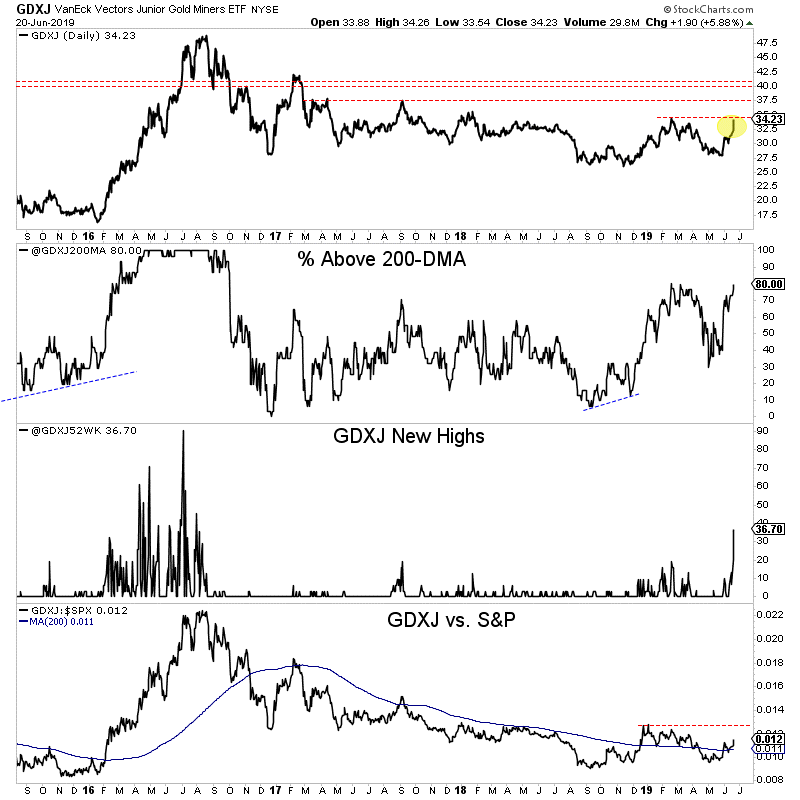

The definitive list of mid-tier gold miners to analyze comes from the GDXJ VanEck Vectors Junior Gold Miners ETF. Despite its misleading name, GDXJ is totally dominated by mid-tier gold miners and not juniors. GDXJ is the world’s second-largest gold-stock ETF, with $4.5b of net assets this week. That is only behind its big-brother GDX VanEck Vectors Gold Miners ETF that includes the major gold miners.

Major gold miners are those that produce over 1m ounces of gold annually. The mid-tier gold miners are smaller, producing between 300k to 1m ounces each year. Below 300k is the junior realm. Translated into quarterly terms, majors mine 250k+ ounces, mid-tiers 75k to 250k, and juniors less than 75k. GDXJ was originally launched as a real junior-gold-stock ETF as its name implies, but it was forced to change its mission.

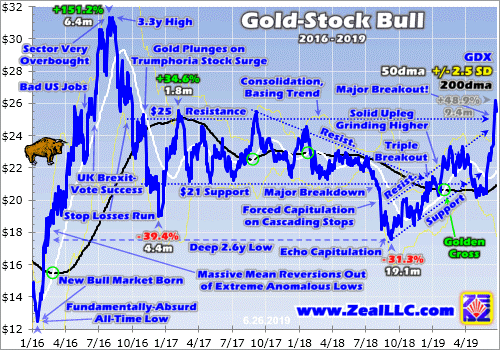

Gold stocks soared in price and popularity in the first half of 2016, ignited by a new bull market in gold. The metal itself awoke from deep secular lows and surged 29.9% higher in just 6.7 months. GDXJ and GDX skyrocketed 202.5% and 151.2% higher in roughly that same span, greatly leveraging gold’s gains! As capital flooded into GDXJ to own junior miners, this ETF risked running afoul of Canadian securities laws.

Canada is the center of the junior-gold universe, where most juniors trade. Once any investor including an ETF buys up a 20%+ stake in a Canadian stock, it is legally deemed a takeover offer. This may have been relevant to a single corporate buyer amassing 20%+, but GDXJ’s legions of investors certainly weren’t trying to take over small gold miners. GDXJ diversified away from juniors to comply with that archaic rule.

Smaller juniors by market capitalization were abandoned entirely, cutting them off from the sizable flows of ETF capital. Larger juniors were kept, but with their weightings within GDXJ greatly demoted. Most of its ranks were filled with mid-tier gold miners, as well as a handful of smaller majors. That was frustrating, but ultimately beneficial. Mid-tier gold miners are in the sweet spot for stock-price-appreciation potential!

For years major gold miners have struggled with declining production, they can’t find or buy enough new gold to offset their depletion. And the stock-price inertia from their large market capitalizations is hard to overcome. The mid-tiers can and are boosting their gold output, which fuels growth in operating cash flows and profitability. With much-lower market caps, capital inflows drive their stock prices higher much faster.

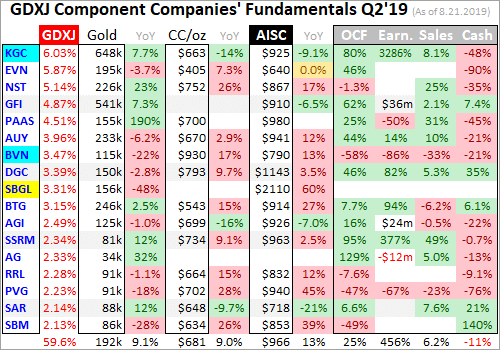

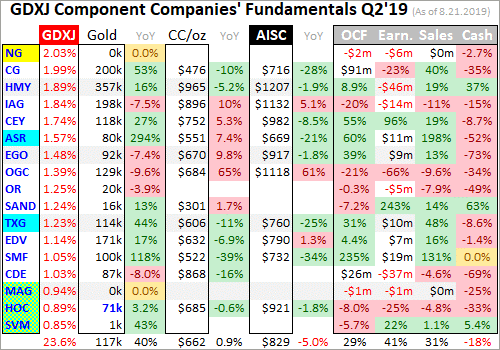

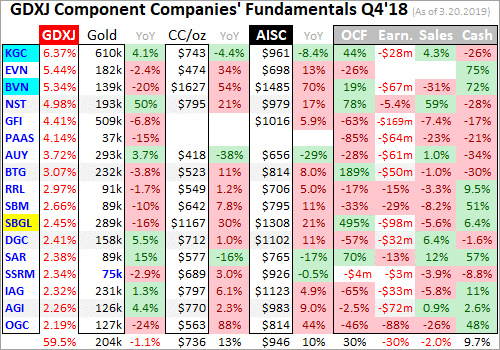

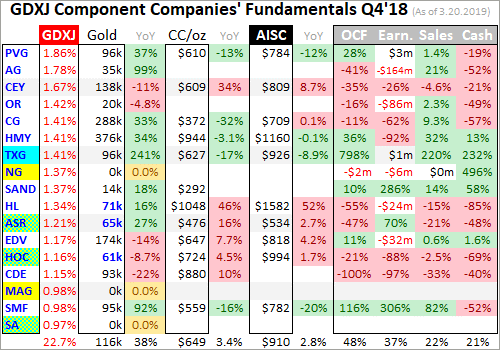

Every quarter I dive into the latest results from the top 34 GDXJ components. That’s simply an arbitrary number that fits neatly into the tables below, but a commanding sample. These companies represented 83.2% of GDXJ’s total weighting this week, even though it contained a whopping 70 stocks! 3 of the top 34 were majors mining 250k+ ounces, 24 mid-tiers at 75k to 250k, 5 “juniors” under 75k, and 2 explorers with zero.

These majors accounted for 12.8% of GDXJ’s total weighting, and really have no place in a “Junior Gold Miners ETF” when they could instead be exclusively in GDX. These mid-tiers weighed in at 60.9% of GDXJ. The “juniors” among the top 34 represented just 6.6% of GDXJ’s total. But only 1 of them at a mere 0.9% of GDXJ is a true junior, meaning it derives over half its revenues from actually mining gold.

The rest include 2 primary silver miners, a gold-royalty company, and a gold streamer. GDXJ is actually a full-on mid-tier gold miners ETF, with modest major and tiny junior exposure. Traders need to realize it is not a junior-gold investment vehicle as advertised. GDXJ also has major overlap with GDX. Fully 29 of these top 34 GDXJ gold miners are included in GDX too, with 23 of them also among GDX’s top 34 stocks.

The GDXJ top 34 accounting for 83.2% of its total weighting also represent 39.8% of GDX’s own total weighting! The GDXJ top 34 mostly clustered between the 10th- to 40th-highest weightings in GDX. Thus nearly 5/6ths of GDXJ is made up by almost 4/10ths of GDX. But GDXJ is far superior, excluding the large gold majors struggling with production growth. GDXJ gives much-higher weightings to better mid-tier miners.

The average Q2’19 gold production among GDXJ’s top 34 was 157k ounces, a bit over half as big as the GDX top 34’s 299k average. Despite these two ETFs’ extensive common holdings, GDXJ is increasingly outperforming GDX. GDXJ holds many of the world’s best mid-tier gold miners with big upside potential as gold’s own bull continues powering higher. Thus it is important to analyze GDXJ miners’ latest results.

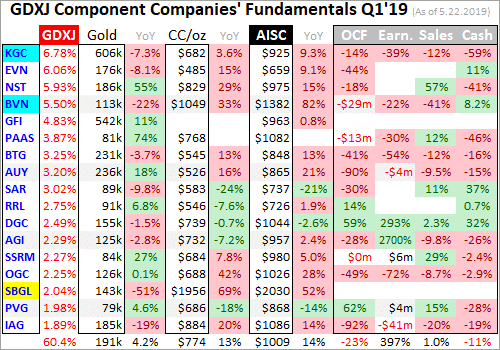

So after each quarterly earnings season I wade through all available operational and financial reports and dump key data into a big spreadsheet for analysis. Some highlights make it into these tables. Any blank fields mean a company hadn’t reported that data as of this Wednesday. The first couple columns show each GDXJ component’s symbol and weighting within this ETF as of this week. Not all are U.S. symbols.

19 of the GDXJ top 34 primarily trade in the U.S., 5 in Australia, 8 in Canada, and 2 in the U.K. So some symbols are listings from companies’ main foreign stock exchanges. That’s followed by each gold miner’s Q2’19 production in ounces, which is mostly in pure-gold terms excluding byproducts often found in gold ore like silver and base metals. Then production’s absolute year-over-year change from Q2’18 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drive profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. In cases where foreign GDXJ components only released half-year data, I used that and split it in half where appropriate. That offers a decent approximation of Q2 results.

Symbols highlighted in light blue newly climbed into the ranks of GDXJ’s top 34 over this past year. And symbols highlighted in yellow show the rare GDXJ-top-34 components that aren’t also in GDX. If both conditions are true, blue-yellow checkerboarding is used. Production bold-faced in blue shows any rare junior gold miners in GDXJ’s higher ranks, under 75k ounces quarterly with over half of sales from gold.

This whole valuable dataset compared with past quarters offers a fantastic high-level read on how mid-tier gold miners are faring fundamentally as an industry. This last quarter was interesting, as gold’s awesome breakout surge to major new secular highs didn’t get underway until just before quarter-end. So the mid-tier gold miners had to contend with flat gold prices, with Q2’19’s average of $1309 merely 0.2% higher YoY.

The shuffling in the ranks of GDXJ’s top 34 components continued over this past year, with major gold miner Kinross Gold added. It, Gold Fields, and Harmony Gold really should be shifted exclusively into GDX since their production is way into major-dom. Gold miners of that scale just defeat the purpose of a “Junior Gold Miners ETF”, retarding its upside potential and eroding traders’ confidence in its managers’ competence.

Most of the other new additions are good though, including mid-tiers Buenaventura, Alacer Gold, and Torex Gold. While Hochschild Mining was technically a junior last quarter, it will likely soon grow into a mid-tier mining 75k+ ounces of gold quarterly. But there’s one GDXJ component that reported such an extreme quarter that it skews most of the year-over-year comparisons. That is South Africa’s Sibanye-Stillwater.

SBGL is actually a primary platinum-group-metals miner, which drove nearly two-thirds of its implied revenue based on average metals prices in Q2! Its shrinking South African gold operations are a total mess, just emerging from a 5-month-long strike organized by a violent Marxist union. That crippled its gold mines, and left at least 9 people dead! Sibanye-Stillwater also has to fight South Africa’s absurdly-corrupt government.

Even though that hellish strike ended in mid-April, very early in Q2, SBGL’s gold production plummeted a catastrophic 47.9% YoY last quarter! That catapulted its all-in sustaining costs to a ridiculous $2110 per ounce, up an extreme 60.5% YoY from already-high levels. This shocking anomaly needs to be excluded in GDXJ comparisons. I wouldn’t invest in this company if it was the last miner on earth, it is a nightmare.

Production has always been the lifeblood of the gold-mining industry. Gold miners have no control over prevailing gold prices, their product sells for whatever the markets offer. Thus growing production is the only manageable way to boost revenues, leading to amplified gains in operating cash flows and profits. Higher production generates more capital to invest in expanding existing mines and building or buying new ones.

Thus gold-stock investors have long prized production growth above everything else, as it is inexorably linked to company growth and thus stock-price-appreciation potential. In Q2’19 these GDXJ-top-34 gold miners collectively produced 5.0m ounces of gold. That was actually down 1.2% YoY, which is worse than the 0.7% shrinkage the top 34 GDX majors reported last quarter after being adjusted for mega-mergers.

But excluding SBGL’s mayhem, the rest of the GDXJ top 34 actually managed to grow their total output by an impressive 1.7% YoY to 4.9m ounces! That not only trounced the majors, but narrowly bested the world’s aggregate production growth in Q2. According to gold’s leading fundamental authority, the World Gold Council, total world output grew 1.6% YoY last quarter to 28.4m ounces. The mid-tiers are thriving.

The GDXJ mid-tiers were able to enjoy strong production growth because this ETF isn’t burdened with many struggling major gold miners that dominate GDX. Again GDXJ’s components start at the 10th-highest weighting in GDX. The 9 above it averaged colossal Q2 production of 585k ounces, which is 3.7x bigger than the GDXJ top 34’s average! Gold mining’s inherent geological limitations make it very difficult to scale.

The more gold miners produce, the harder it is to even keep up with relentless depletion let alone grow their output consistently. Large economically-viable gold deposits are getting increasingly difficult to find and ever-more-expensive to develop, with low-hanging fruit long since exploited. But with much-smaller production bases, mine expansions and new mine builds generate big output growth for mid-tier golds.

The majors don’t only face that large-base growth problem with their production scales, but also with their stocks’ market capitalizations. The GDXJ top 34 companies averaged $2.5b in the middle of this week, compared to $6.9b in the GDX top 34 when I analyzed their Q2 results last week. With the mid-tiers generally around a third as big as the majors, their stock prices have much less inertia restraining them.

With gold returning to favor since late June’s awesome decisive bull-market breakout, the mid-tier-filled GDXJ is already outperforming the major-dominated GDX. Since its year-to-date low in late May, GDXJ surged as much as 52.1% higher by early August! That was considerably better than GDX’s 46.2% rally in the same timeframe. The longer gold-bull uplegs persist, the bigger the mid-tier outperformance grows.

The mid-tier gold miners continue to prove all-important production growth is achievable off smaller bases. With a handful of mines or less to operate, mid-tiers can focus on expanding them or building a new mine to boost their output beyond depletion. But the majors are increasingly failing to do this from the super-high production bases they operate at. As long as majors are struggling, it is prudent to avoid them.

Also interesting on the mid-tier production front was silver. Last quarter the GDXJ-top-34 miners’ silver output blasted 42.8% higher YoY to 28.2m ounces! Some of these companies indeed saw exploding silver production, led by Yamana Gold’s rocketing up 65.8% YoY to 2.2m ounces and SSR Mining’s soaring a similar 55.8% YoY to 1.5m ounces. But new GDXJ-top-34 components drove most of the silver growth.

Buenaventura and Hochschild Mining produced 5.5m and 4.3m ounces of silver last quarter, and they weren’t in GDXJ’s top 34 in Q2’18. Excluding them, the rest of these mid-tier gold miners actually saw their total silver output slump 5.1% YoY. I’ll discuss the serious challenges silver mining faces in next week’s essay, which will wade through the results of the top silver miners of the leading silver miners’ ETF.

In gold mining, production and costs are generally inversely related. Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring about the same levels of infrastructure, equipment, and employees. So the higher production, the more ounces to spread mining’s big fixed costs across. Thus Q2’19’s solid production growth among the GDXJ top 34 ex-SBGL should’ve yielded proportionally-lower costs.

There are two major ways to measure gold-mining costs, classic cash costs per ounce and the superior all-in sustaining costs per ounce. Both are useful metrics. Cash costs are the acid test of gold-miner survivability in lower-gold-price environments, revealing the worst-case gold levels necessary to keep the mines running. All-in sustaining costs show where gold needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q2’19 these top-34-GDXJ-component gold miners that reported cash costs averaged $672 per ounce. That actually rose a sharp 6.6% YoY, and was worse than the GDX-top-34 majors’ $641 mean.

Sibanye-Stillwater didn’t report Q2 cash costs, so that wasn’t a factor. But a couple of other anomalous situations dragged up this average. Buenaventura has been struggling with weaker production, resulting in extreme $930 cash costs last quarter. And Harmony Gold, a South African miner facing that country’s miserable operating environment, had even-worse $965 cash costs in Q2’19! Those are crazy-high.

Excluding them, the rest of the GDXJ top 34 averaged $650. That’s towards the lower end of the GDXJ-top-34 average range of $612 to $730 in the 13 quarters I’ve been advancing this deep-quarterly-results research thread. As long as cash costs remain far below prevailing gold prices, which was certainly true in Q2, the gold miners face no existential threat. Gold returning to favor is really widening that key survival gap.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain gold mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current gold-production levels.

These additional expenses include exploration for new gold to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee gold mines. All-in sustaining costs are the most-important gold-mining cost metric by far for investors, revealing companies’ true operating profitability.

The GDXJ-top-34 AISC picture in Q2’19 looked much like the cash-cost one, with average AISCs surging 6.1% YoY to $941 per ounce. That was on the higher side of the past 13 quarters’ range from $855 to $1002, but way below Q2’s average gold price of $1309. That implies GDXJ’s mid-tier gold miners were already earning sizable $368 profits last quarter. But this AISC read was heavily skewed by SBGL’s mess.

Again that cursed gold miner’s AISCs skyrocketed 60.5% YoY to an unbelievable $2110! That was as high as I’ve ever seen, and SBGL tried to bury this deep in its Q2 reporting. The strike was blamed, even though it ended in early Q2. But remove that wild outlier from the pool, and the rest of the GDXJ-top-34 gold miners averaged AISCs of $896 per ounce. That’s actually right in line with the GDX top 34’s $895.

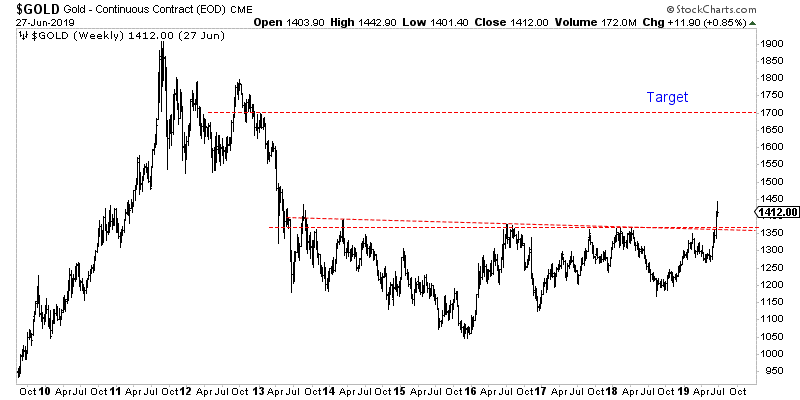

With gold rocketing back over $1500 earlier this month to hit 6.3-year secular highs, it is easy to assume the gold miners must be thriving fundamentally. And they likely are. But realize the lion’s share of the recent huge gold gains didn’t start until late June when gold decisively broke out to new bull-market highs. So these Q2 results don’t yet reflect these new higher gold prices. But Q3’s are on track to look spectacular.

Gold’s lofty $1446 average price so far this quarter is a whopping 10.5% higher quarter-on-quarter than Q2’s! So the current likely profitability of the gold miners post-gold-breakout is far higher than seen last quarter. Assuming the GDXJ top 34’s average all-in sustaining costs hold flat near $941 this quarter, that implies Q3 profits running $505 per ounce. That’s up a massive 37.2% QoQ from what was seen in Q2!

This incredible profits leverage to gold is what makes gold stocks so alluring during major gold uplegs. Their earnings grow so darned fast, 3.5x gold’s advance in this example, that big stock-price gains are usually fundamentally-justified. In Q2’19, GDXJ averaged $30.46 per share. That’s when you should’ve been buying gold stocks, when they were low and out of favor. I explained their bullish outlook in early April.

So far in Q3 which is more than half over, GDX has averaged $38.43 which is 26.2% higher QoQ. That is still lagging big expected profits growth among mid-tier gold miners this quarter given the much-higher prevailing gold prices. So gold stocks’ strong gains in recent months are fundamentally-righteous, supported by underlying earnings growth and sustainable as long as gold holds over $1446 into quarter-end.

The mid-tier gold miners reported good accounting results last quarter even before gold reignited. The GDXJ top 34’s total revenues soared 23.0% YoY to $6.6b! While that is certainly overstated given the new inclusion of major gold miner Kinross Gold, without it the rest of these companies still saw strong 7.3% YoY growth. That’s impressive given Q2’19’s dead-flat average gold price, up a trivial 0.2% YoY.

These strong operations drove exploding operating-cashflow generation, with the GDXJ top 34’s total blasting 44.2% higher YoY to $2.3b! Even without KGC they still rose 23.6% YoY. And these elite mid-tier gold miners were investing some of this new capital in expanding their mines, which investors always like to see. Their collective cash hoards sunk 12.6% YoY to $6.0b, which remains healthy given mid-tiers’ sizes.

The GDXJ top 34’s profits under Generally Accepted Accounting Principles radically improved as well. Together they earned $291m last quarter, which was a colossal improvement from Q2’18’s $410m loss. Even though $384m of that resulted from an impairment charge by a single component miner that quarter, the mid-tiers’ profits picture still greatly improved. And that was even with last quarter’s still-anemic $1309 gold.

Imagine how awesome these numbers will look in this current quarter given all the gold fireworks since the end of Q2! The mid-tier gold miners generally report their results 4 to 6 weeks after quarter-ends, so Q3’19 fundamental performance will be revealed in the first half of November. As long as gold sentiment remains decent, these Q3 results should really impress and attract in legions of new investors to this sector.

That being said, gold and gold stocks have soared really far really fast this quarter. Sentiment quickly grew greedy as really-overbought levels were reached. Couple that with today’s menacing overhang of huge potential gold-futures selling, and a healthy bull-market correction is likely. But now is the time to do your homework before buying lower later, to ferret out the high-potential gold miners with superior fundamentals.

All portfolios need a 10% allocation in gold and its miners’ stocks! This is more important than ever with gold finally waking up from its long slumber while lofty central-bank-goosed stock markets are looking increasingly precarious. The better mid-tier gold miners are the place to be. Unlike the majors, they are actually growing their production and have far-higher upside coming from lower-market-capitalization bases.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In the first half of 2019 well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. We’ve recently realized big gains including 109.7%, 105.8%, and 103.0%!

To profitably trade high-potential gold stocks, you need to stay informed about the broader market cycles that drive gold. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast so they can ride entire uplegs.

The bottom line is the mid-tier gold miners are thriving fundamentally. Their Q2 results were good, even before gold’s powerful bull-market breakout. They are growing production while holding the line on costs. That means their earnings will soar as gold powers higher on balance in its resurgent bull market. That will support much-higher gold-stock prices in the future, and attract traders back to this long-neglected sector.

Gold’s bull market will flow and ebb as always, so gold-stock positions should be accumulated relatively low in post-selloff troughs. There’s no need to buy high at crests when everyone is excited. But you have to prepare in advance, monitoring the markets and researching the gold miners to be ready to pounce at opportune times. Capital allocations should be focused on mid-tier gold miners with superior fundamentals.

Adam Hamilton, CPA

August 26, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Corrections are inevitable, but current conditions support a prolonged rally in the gold market, TD Securities says in an equity research report.

“Before we restate our bullish thesis for precious metals, we should acknowledge that positioning in the gold market is at extreme levels, with Comex net longs near all-time highs and trading volumes at near double the averages of last year,” the report says.

This type of market posture, with everyone enthusiastically lined up in one direction, often precedes a reversal and a gold correction now could be exacerbated by the magnitude of the move required to restore normalcy to the market, TD says.

Of course, the macro picture is anything but normal. TD notes that there is now broad consensus around the idea that the deteriorating U.S. and global economic outlook will mean that Fed Chair Powell’s ‘mid-cycle adjustment’ in July will turn into an extended cutting cycle, with the bond market pricing in 25-50 bps of cuts by year-end.

TD Global Rates, which called for cuts ahead of the market, is calling for 50 bps of additional easing in 2019, followed by an additional 75 bps of easing in 2020. In many countries, real rates are already negative, and the discussion is around tiering (allowing more deeply-negative yields), QE, and the potential for competitive currency devaluation, TD says,

Despite Rally, Gold Equities Undervalued vs. Gold

The GDX (large-cap) index has rallied around 35% YTD, while the GDXJ (small-cap) is up only about 31% despite having outperformed its larger brother since the beginning of June. Gold, for reference, is up around 19% YTD.

Despite this, gold equities as measured by the S&P/TSX Gold Index are lagging their historical relationship to gold, both when compared with the most recent peak in 2016 and with the peak of the last bull market in 2011, TD notes.

Rotations Key to Maximizing Returns in Prolonged Rally

In a note published in June, TD called the technical breakouts of both gold and silver from their downtrends (corrections within the bull market that began in early 2016). Both metals rallied strongly from that point, with gold up 15% and silver up 16% since then.

TD had also forecast at that time that silver will lag and then outperform gold on a continuation of the rally. Indeed, we saw the gold/silver ratio climb to multi-decade highs above 93 in mid-July before falling to 86 and since then partially retracing that move.

TD’s preferred name for high beta and liquidity, which was highlighted in the June note, was First Majestic Silver, which has rallied approximately 59% since then, strongly outperforming its peers.

TD will publish more on the gold/silver ratio when the retracement/consolidation pattern is complete as TD analysts ultimately expect much stronger gains in silver before the precious metals bull market is over.

Last week was another strong one for the precious metals sector.

Gold gained a whopping $51/oz or 3.5%. The gold stocks (GDX, GDXJ) advanced by roughly 6%. Silver gained 4%.

Momentum in the sector began to build once Gold surpassed resistance at $1420-$1425/oz. We had noted the lack of resistance from $1425 to $1525-$1550/oz.

Gold has not reached $1550/oz yet but as it inches higher, some technical and sentiment indicators are urging caution.

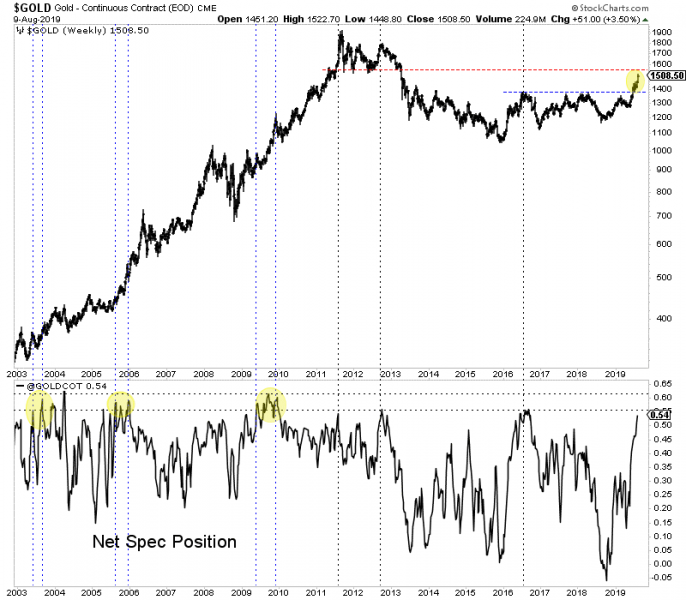

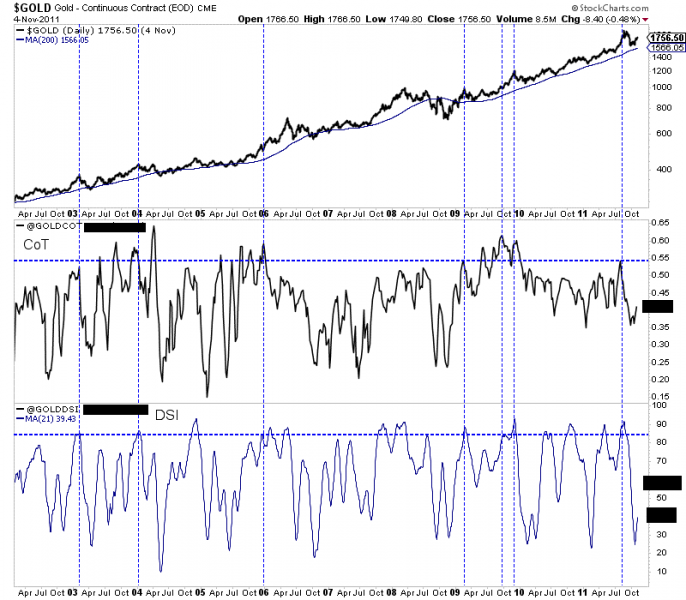

Gold’s net speculative position of 54% is very close to the peaks of 55% to 60% seen since 2000. It’s possible the commercial hedgers will start covering at some point like they did in 2006 and 2010 but for now we have to assume they won’t if $1550/oz holds as resistance.

In the next chart we plot Gold’s net speculative position (51%) and the 21-day average of the daily sentiment index (DSI) from 2002 to 2011 (84%).

During that strong 10-year period, those figures of 51% and 84% were reached seven times. Five of those seven times Gold corrected or consolidated for at least a few months.

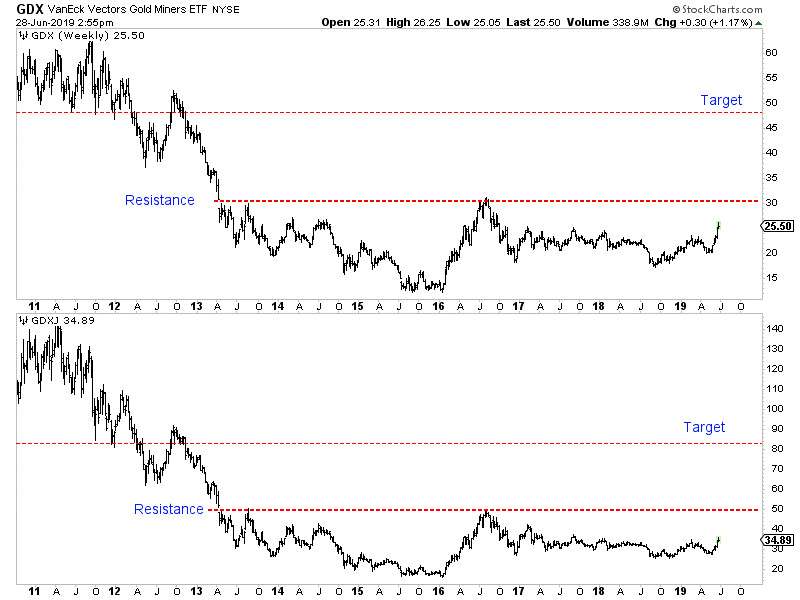

Turning to the gold stocks (and GDX specifically), we find a fairly overbought condition while the market approaches multi-year resistance at $31-$32.

The bullish percentage index (BPGDM) and a 20-day moving average of new highs in GDX are approaching the levels they peaked at in July 2016.

The trend in precious metals is strong and the fundamentals are bullish but there can obviously be corrections and consolidations within strong trends.

Sentiment indicators are becoming a concern and Gold and gold stocks (GDX) are approaching obvious resistance levels at $1550/oz and $31-$32.

This is not the time to be placing aggressive bets on Gold or the senior gold stocks. If there is a sector correction, those areas figure to be hit harder than Silver or junior mining stocks which are not as extended.

If you missed the recent run then it is best to be patient, buy value and wait for weakness in anything that is strong but too extended. New opportunities will emerge. To learn the stocks we own and intend to buy during the next correction that have 3x to 5x potential, consider learning more about our premium service.

By Jordan Roy-Byrne CMT, MFTA

August 14, 2019

The precious metals sector appears to have started a correction.

It was roaring higher until natural resistance kicked in and the U.S. Dollar grinded its way higher, towards its 2019 high. Factor in the Fed decision this week and it has created a natural “buy the rumor, sell the news” event.

We cannot know for certain what the Federal Reserve will do or even more importantly, how the market will react. But we can take note of key levels in these markets.

Gold has held above $1400/oz but has been unable to break past resistance at $1420-$1425/oz. A retest of $1385/oz is quite possible and so is a test of $1365/oz.

Silver has outperformed Gold since it broke above its 400-day moving average, which provided strong resistance dating back to the end of 2017.

Silver encountered resistance at $16.60-$16.70/oz and could test initial support at $16.20/oz. Below that is strong support at $15.95/oz.

Turning to the gold stocks, we find a clear setup between support and resistance.

GDX, the ETF for large gold producers has resistance at $28 but good support above $25.00, which was previous resistance for nearly three years. Look for initial support around $26.00.

GDXJ, the ETF for the “senior” junior companies, faces resistance at $40-$41. It has initial support around $37.50 with strong support at $36.00.

Regardless of what the Fed does or says, my expectation is precious metals will test these levels and ultimately hold them. The Fed and global central banks want to ease policy and this figures to be more than a one-off.

Precious metals became overbought and a correction is in order.

Investors who smartly positioned in recent months should continue to hold their winners. If the sector continues to correct then look to be a buyer at the aforementioned support levels.

Look to focus your capital on fresh opportunities and value plays that are not very overbought or extended. To learn the stocks we own and intend to buy on this weakness that have 3x to 5x potential, consider learning more about our premium service.

Jordan Roy-Byrne CMT, MFTA

July 30, 2019

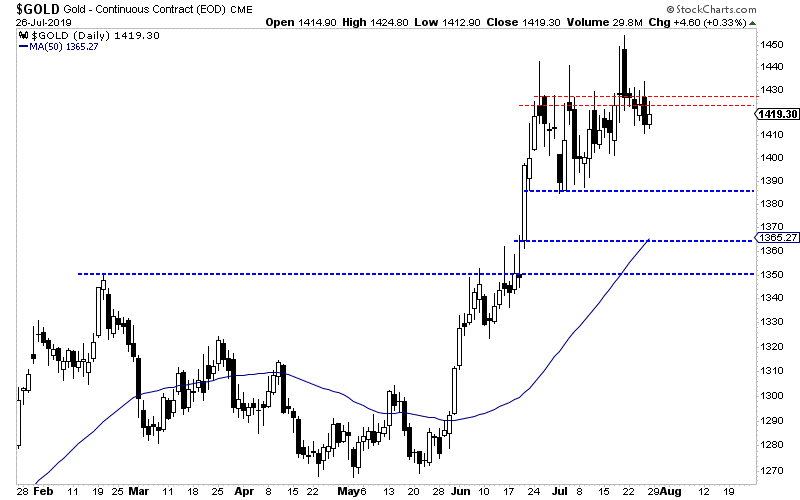

It was a huge week for the gold stocks. GDX gained nearly 7% while GDXJ surged over 10%.

Gold hit $1450/oz after Thursday before selling off Friday. Silver met the same fate on Friday but managed to close the week up over 6% and at a new 52-week high.

Let’s take a look at the current technicals.

Gold closed the week just below $1427/oz. If it remains above $1420-$1425, then it is likely to trend towards $1475/oz, which is the only resistance between $1425 and $1525.

If Gold trades back below $1420 then there is a risk it could test $1380 again.

Silver has taken out resistance at its 400-day moving average in convincing fashion but needs to surpass its February 2019 high. Its next major resistance target is the mid $18s.

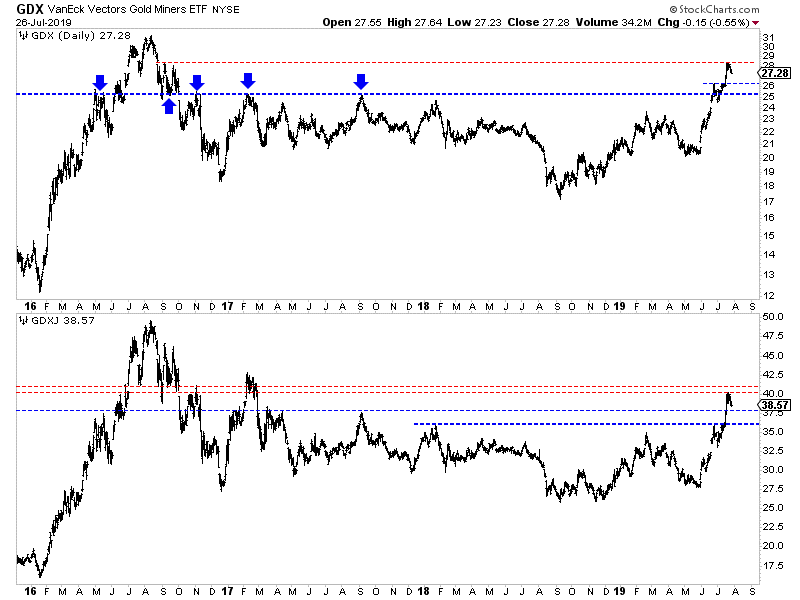

Turning to the stocks, we start with GDX which is closing in on its 2016 high. Should Gold trend towards $1475/oz then GDX would likely retest that 2016 high at $31.

Breadth remains strong and so too is GDX’ relative strength. GDX relative to the S&P made a 21-month high and relative to Gold made a 2-year high.

Both GDXJ (juniors) and the HUI (miners only) still have room to go before reaching their 2016 highs.

In fact, both are facing some immediate overhead resistance. For GDXJ which closed at $39.50, that resistance is at $40-$41. For HUI which closed at 211, that resistance is at 220.

The support levels are $36 for GDXJ and 195 for the HUI.

If Gold and Silver maintain current levels, then the immediate bias remains higher and GDX could soon test its 2016 high.

GDXJ and HUI have roughly 30% upside to their 2016 highs. Such a move probably requires a move in Gold to at least $1525/oz.

However, if Friday was the start of a correction then GDX could test $26 and GDXJ could test $36.

For investors in the juniors and seniors, continue to hold winners. If the sector corrects, then look to take advantage of that weakness. If metals and shares maintain these levels then focus your capital on fresh opportunities and value plays that are not overbought or extended. To learn the stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

By Jordan Roy-Byrne CMT, MFTA

July 23, 2019

Gold and gold stocks especially continue to shrug off bits and pieces of bad news.

No escalation in the trade war? The selloff lasted one day and the sector rebounded strongly the following day.

Strong headline jobs number? Again, the weakness was a buying opportunity.

This past week there was more.

The June CPI report came in hotter than expected, which could mitigate the degree the Fed eases in the future. Also, bond yields in the US have risen the entire week.

No dice.

Gold closed the week at $1412/oz while the gold stocks closed just inches from new highs on the daily charts.

Turning to the technicals of the gold stocks, we see both underlying and relative strength.

Nearly 95% of the large miners closed above the 200-day moving average. Meanwhile GDX relative to both the S&P 500 and Gold is above a rising 200-day moving average. The GDX to Gold ratio is at a 2-year high while the GDX to S&P 500 ratio is very close to a new 52-week high.

GDXJ is lagging GDX a bit but it is coming around.

90% of the ETF closed above the 200-day moving average. That is the highest reading in nearly three years.

GDXJ relative to the S&P and Gold has turned bullish and is holding above upward sloping 200-day moving averages.

The immediate upside targets for GDX and GDXJ are GDX $27.50 and GDXJ $37.50. The next level of targets would be GDX $30 and GDXJ $41.

Gold has endured some selling in the $1420-$1425/oz range but has remained bid around $1400/oz. A daily close above $1420/oz would remove much of the resistance from here to the low $1500s.

For investors in the juniors and seniors, continue to hold your winners and focus your capital on fresh opportunities and value plays that could move with the next leg higher. To learn which stocks we own and intend to buy that have 3x to 5x potential, consider learning more about our premium service.

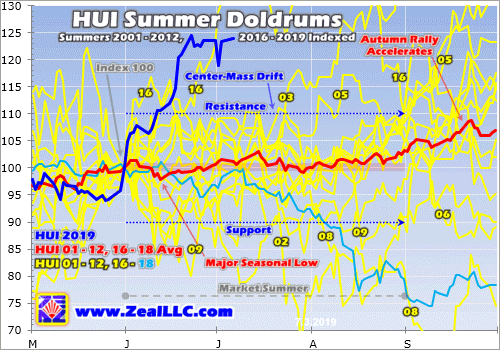

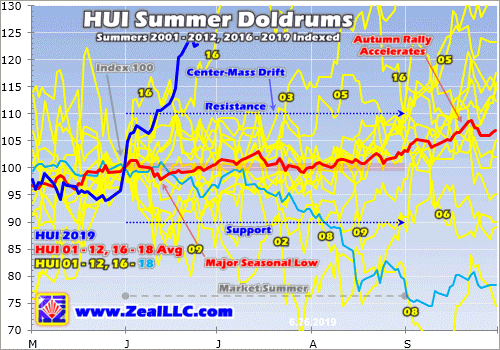

Gold’s incredible strength this summer is very unusual, as early summers are the weakest times of the year seasonally for gold, silver, and their miners’ stocks. With traders’ attention diverted to vacations and summer fun, interest in and demand for precious metals normally wane. So this entire sector tends to suffer a seasonal lull, along with the general markets. This June’s bull-market breakout is a momentous anomaly.

This doldrums term is very apt for gold’s usual summer predicament. It describes a zone in the world’s oceans surrounding the equator. There hot air is constantly rising, creating long-lived low-pressure areas. They are often calm, with little or no prevailing winds. History is full of accounts of sailing ships getting trapped in this zone for days or weeks, unable to make headway. The doldrums were murder on ships’ morale.

Crews had no idea when the winds would pick up again, while they continued burning through their limited stores of food and drink. Without moving air, the stifling heat and humidity were suffocating on these ships long before air conditioning. Misery and boredom were extreme, leading to fights breaking out and occasional mutinies. Being trapped in the doldrums was viewed with dread, it was a very trying experience.

Gold investors can somewhat relate. Like clockwork nearly every summer, gold starts drifting listlessly sideways. It often can’t make significant progress no matter what the trends looked like heading into June, July, and August. As the days and weeks slowly pass, sentiment deteriorates markedly. Patience is gradually exhausted, supplanted with deep frustration. Plenty of traders capitulate, abandoning ship.

Thus after decades of trading gold, silver, and their miners’ stocks, I’ve come to call this time of year the summer doldrums. Junes and Julies in particular are usually desolate sentiment wastelands for precious metals, totally devoid of recurring seasonal demand surges. Unlike much of the rest of the year, these summer months simply lack any major income-cycle or cultural drivers of outsized gold investment demand.

The vast majority of the world’s investors and speculators live in the northern hemisphere, so markets take a back seat to the great joys of summer. Traders take advantage of the long sunny days and kids being out of school to go on extended vacations, hang out with friends, and enjoy life. And when they aren’t paying much attention to the markets, naturally they aren’t allocating much new capital to gold.

Given gold’s dull summer action historically, it is never wise to expect too much from it this time of year. Summer rallies can happen, but they aren’t common. So expectations need to be tempered, especially in Junes and Julies. That early-1990s Gin Blossoms song “Hey Jealousy” comes to mind, declaring “If you don’t expect too much from me, you might not be let down.” The markets are ultimately an expectations game.

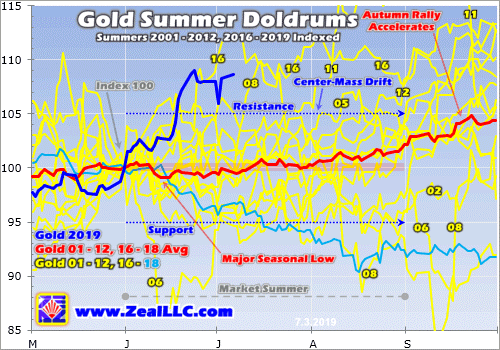

Quantifying gold’s summer seasonal tendencies during bull markets requires all relevant years’ price action to be recast in perfectly-comparable percentage terms. That is accomplished by individually indexing each calendar year’s gold price to its last close before market summers, which is May’s final trading day. That is set at 100, then all gold-price action each summer is recalculated off that common indexed baseline.

So gold trading at an indexed level of 105 simply means it has rallied 5% from May’s final close, while 95 shows it is down 5%. This methodology renders all bull-market-year gold summers in like terms. That’s necessary since gold’s price range has been so vast, from $257 in April 2001 to $1894 in August 2011. That span encompassed gold’s last secular bull, which enjoyed a colossal 638.2% gain over those 10.4 years!

Obviously 2001 to 2011 were certainly bull years. 2012 was technically one too, despite gold suffering a major correction following that powerful bull run. At worst that year, gold fell 18.8% from its 2011 peak. That was not quite enough to enter formal bear territory at a 20%+ drop. But 2013 to 2015 were definitely brutal bear years, which need to be excluded since gold behaves very differently in bull and bear markets.

In early 2013 the Fed’s wildly-unprecedented open-ended QE3 campaign ramped to full speed, radically distorting the markets. Stock markets levitated on the Fed’s implied backstopping, slaughtering demand for alternative investments led by gold. So in Q2’13 alone, gold plummeted 22.8% which proved its worst quarter in an astounding 93 years! Gold’s bear continued until the Fed started hiking rates again in late 2015.

The day after that first rate hike in 9.5 years in mid-December 2015, gold plunged to a major 6.1-year secular low. Then it surged out of that irrational rate-hike scare, formally crossing the +20% new-bull threshold in early March 2016. Ever since, gold has remained in this current bull. At worst in December 2016 after gold was crushed on the post-election Trumphoria stock-market surge, it had only corrected 17.3%.

So the bull-market years for gold in modern history ran from 2001 to 2012, skipped the intervening bear-market years of 2013 to 2015, then resumed in 2016 to 2019. Thus these are the years most relevant to understanding gold’s typical summer-doldrums performance, which is necessary for managing your own expectations this time of year. This spilled-spaghetti mess of a chart is fairly simple and easy to understand.

The yellow lines show gold’s individual-year summer price action indexed from each May’s final close for all years from 2001 to 2012 and 2016 to 2017. 2018’s is rendered in light blue. Together these establish gold’s summer trading range. All those past bull-market years’ individual indexes are averaged together in the red line, revealing gold’s central summer tendency. 2019’s indexed action is superimposed in dark blue.

While there are outlier years, gold generally drifts listlessly in the summer doldrums much like a sailing ship trapped near the equator. The center-mass drift trend is crystal-clear in this chart. The vast majority of the time in June, July, and August, gold simply meanders between +/-5% from May’s final close. This year that equated to a probable summer range between $1240 to $1370. Gold tends to stay well within trend.

Obviously this year has proven a huge exception to that normal summer rule, with gold rocketing higher to a major bull-market breakout! Gold blasted to its best early-summer performance ever seen in all modern bull-market years. Comparing this current summer’s dark-blue line to past years’ price action certainly drives home how unique, exceptional, and special gold’s breakout surge to major new secular highs has been.

Still, understanding gold’s typical behavior this time of year is important for traders. Sentiment isn’t only determined by outcome, but by the interplay between outcome and expectations. If gold rallies 5% but you expected 10% gains, you will be disappointed and grow discouraged and bearish. But if gold rallies that same 5% and you expected no gains, you’ll be excited and get optimistic and bullish. Expectations are key.

History has proven it is wise not to expect too much from gold in these lazy market summers, particularly Junes and Julies. Occasionally gold still manages to stage a summer rally, like this year’s monster. But most of the time gold doesn’t veer materially from its usual summer-drift trading range, where it is often adrift like a classic tall ship. With range breakouts either way uncommon, there’s often little to get excited about.

In this chart I labeled some of the outlying years where gold burst out of its usual summer-drift trend, both to the upside and downside. But these exciting summers are atypical, and can’t be expected very often. Most of the time gold grinds sideways on balance not far from its May close. Traders not armed with this critical knowledge often wax bearish during gold’s summer doldrums and exit in frustration, a real mistake.

Gold’s summer-doldrums lull marks the best time of the year seasonally to deploy capital, to buy low at a time when few others are willing. Gold enjoys powerful seasonal rallies that start in Augusts and run until the following Mays! These are fueled by outsized investment demand driven by a series of major income-cycle and cultural factors from around the world. Summer is when investors should be bullish, not bearish.

The red average indexed line above encompassing 2001 to 2012 and 2016 to 2018 reveals gold’s true underlying summer trend in bull-market years. Technically gold’s major seasonal low arrives relatively early in summers, mid-June. On average through all these modern bull-market years, gold slumped 0.9% between May’s close and that summer nadir. But seasonally that’s still on the early side to deploy capital.

Check out the yellow indexed lines in this chart. They tend to cluster closer to flatlined in mid-June than through all of July. The only reason gold’s seasonal low appears in mid-June mathematically is a single extreme-outlier year, 2006. The spring seasonal rally was epic that year, gold rocketed 33.4% higher to a dazzling new bull high of $720 in just 2.0 months between mid-March to mid-May! That was incredible.

Extreme euphoria had catapulted gold an astounding 38.9% above its 200-day moving average, radically overbought by any standard. That was way too far too fast to be sustainable, so after that gold had to pay the piper in a sharp mean-reversion overshoot. So over the next month or so into mid-June, gold’s overheated price plummeted 21.9%! That crazy outlier is the only reason gold’s major summer low isn’t later.

There were 15 bull-market years from 2001 to 2012 and 2016 to 2018. That is a big-enough sample to smooth out the trend, but not large enough to prevent extreme deviations from skewing it a bit. Gold sees a series of marginally-higher lows in late June, early July, and even late July. In this dataset they came in 0.0%, 0.3%, and 0.8% higher than mid-June’s initial low. And that last late-July one arrives over 6 weeks later.

So generally there’s no hurry to deploy capital right at that initial mid-June seasonal low. Gold tends to drift nearly flatlined over the next several weeks into early July, trying traders’ patience. Buying within a few trading days of the US Independence Day holiday seems to have the best odds of catching gold near its summer-doldrums lows. Investment capital inflows usually begin ramping back up after that as traders return.

On average in these modern bull-market years, gold slipped 0.4% in Junes before rallying 0.7% in Julies. After July’s initial lazy summer week, gold tends to gradually start clawing its way back higher again. But this is so subtle that Julies often still feel summer-doldrumsy. By the final trading day in July, gold is still only 0.3% higher than its May close kicking off summers. That’s too small to restore damaged sentiment.

Since gold exited May 2019 at $1305, an average 0.3% rally by July’s end would put it at $1309. That’s hardly enough to generate excitement after two psychologically-grating months of drifting. But the best times to deploy any investment capital are when no one else wants to so prices are low. Gold’s summer doldrums come to swift ends in Augusts, which saw hefty average gains of 1.9% in these bull-market years!

And that’s just the start of gold’s major autumn seasonal rally, which has averaged strong 5.7% gains between mid-Junes to late Septembers. That is driven by Asian gold demand coming back online, first post-harvest-surplus buying and later Indian-wedding-season buying. June is the worst of gold’s summer doldrums, and the first half of July is when to buy back in. It’s important to be fully deployed before August.

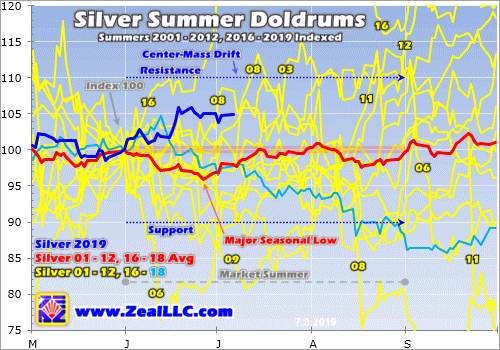

These gold summer doldrums driven by investors pulling back from the markets to enjoy their vacation season don’t exist in a vacuum. Gold’s fortunes drive the entire precious-metals complex, including both silver and the stocks of the gold and silver miners. These are effectively leveraged plays on gold, so the summer doldrums in them mirror and exaggerate gold’s own. Check out this same chart type applied to silver.

Since silver is much more volatile than gold, naturally its summer-doldrums-drift trading range is wider. The great majority of the time, silver meanders between +/-10% from its final May close. That came in at $14.56 this year, implying a summer-2019 silver trading range between $13.10 to $16.02. While silver suffered that extreme June-2006 selling anomaly too, its major seasonal low arrives a couple weeks after gold’s.

Given gold’s spectacular bull-market-breakout surge last month, silver’s summer performance this year has been utterly dismal. Normally silver amplifies gold upside by at least 2x. But silver has been bombed out and languishing for so long that investors and speculators still want nothing to do with it. Silver often acts as a gold sentiment gauge, and gold hasn’t been over $1400 long enough yet to shift psychology to bullish.

On average in these same gold-bull-market years of 2001 to 2012 and 2016 to 2018, silver dropped 4.1% between May’s close and late June. That is much deeper than gold’s 0.9% seasonal slump, which isn’t surprising given silver’s leverage to gold. Silver’s summer performances are also much lumpier than gold’s. Junes see average silver losses of 3.2%, but those are more than erased in strong rebounds in Julies.

Silver’s big 3.6% average rally in Julies amplifies gold’s gains by an impressive 5.1x! But unfortunately silver hasn’t been able to maintain that seasonal momentum, with Augusts averaging a modest decline of 0.7%. Overall from the end of May to the end of August, silver’s summer-doldrums performance tends to drift lower. Silver averaged a 0.4% full-summer loss, way behind gold’s 2.2% gain through June, July, and August.

That means silver sentiment this time of year is often worse than gold’s, which is already plenty bearish. The summer doldrums are more challenging for silver than gold. Being in the newsletter business for a couple decades now, I’ve heard from countless discouraged investors over the summers. While I haven’t tracked this, it sure feels like silver investors have been disproportionally represented in that feedback.

Since gold is silver’s primary driver, this white metal is stuck in the same dull drifting boat as gold in the market summers. Silver usually leverages whatever is happening in gold, both good and bad. But again the brunt of silver’s summer weakness is borne in Junes. Fully expecting this seasonal weakness and rolling with the punches helps prevent getting disheartened, which in turn can lead to irrationally selling low.

The gold miners’ stocks are also hostage to gold’s summer doldrums. This last chart applies this same methodology to the flagship HUI gold-stock index, which mostly closely mirrors that leading GDX VanEck Vectors Gold Miners ETF. The major gold stocks tend to amplify gold’s gains and losses by 2x to 3x, so it is not surprising that the HUI’s summer-doldrums-drift trading range is also twice as wide as gold’s own.

The gold miners’ stocks share silver’s center-mass summer drift running +/-10% from May’s close. This year the HUI entered the summer doldrums at 157.1, implying a June, July, and August trading range of 141.4 to 172.8. While gold stocks’ GDX ETF is too young to do long-term seasonal analysis on, in GDX terms this summer range translates to $19.43 to $23.75 this year. That’s based off a May 31st close of $21.59.

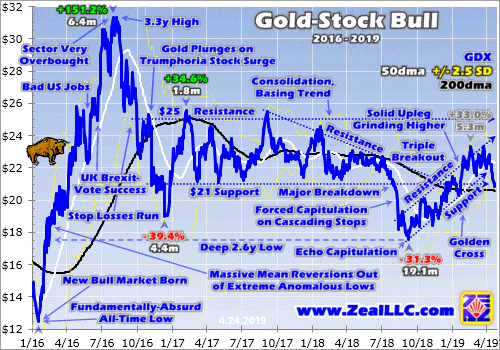

Thanks to gold’s dazzling bull-market breakout, gold stocks have defied these weak summer seasonals this year to soar to their own major decisive breakout! This high-potential contrarian sector has enjoyed its best early-summer performance ever witnessed in gold’s modern bull-market years. While I hope this incredible outperformance persists, the summer doldrums could still reassert themselves if gold retreats.

Like gold, the gold stocks’ major summer seasonal low arrives in mid-June. On average in these gold-bull-market years of 2001 to 2012 and 2016 to 2018, by then the HUI had slid 2.1% from its May close. Then gold stocks tended to more than fully rebound by the end of June, making for an average 0.6% gain that month. But there is no follow-through in July, where the gold stocks averaged a modest 0.5% loss.

Overall between the end of May and the end of July, which encompasses the dark heart of the summer doldrums, the HUI proved dead flat on average. Again two solid months of grinding sideways on balance is hard for traders to stomach, especially if they’re not aware of the summer-doldrums drift. The key to surviving it with minimum psychological angst is to fully expect it. Managing expectations in markets is essential!

But also like gold, the big payoff for weathering the gold-stock summer starts in August. With gold’s major autumn rally getting underway, the gold stocks as measured by the HUI amplify it with good average gains of 3.1% in Augusts! And that’s only the start of gold stocks’ parallel autumn rally with gold’s, which has averaged 9.3% gains from late Julies to late Septembers. Gold-stock upside resumes in late summers.

Like much in life, withstanding the precious-metals summer doldrums is less challenging if you know they’re coming. While outlying years happen, they aren’t common. So the only safe bet to make is expecting gold, silver, and the stocks of their miners to languish in Junes and Julies. Then when these drifts again come to pass, you won’t be surprised and won’t get too bearish. That will protect you from selling low.

The precious-metals sector radically bucked its seasonal-slump trend this year, surging to a record start. Gold began blasting higher on May’s final trading day, and that sharp rally carried into early June. New trade-war tariff threats were ramping up market fears, driving the US stock markets to selloff lows following late April’s all-time record highs. So traders remembered diversifying with gold and flocked back to it.

In mid-June gold’s gains accelerated after the Fed reversed its future-rate outlook from hiking back to cutting. That propelled gold to its first new bull-market highs in 3.0 years, with it surging to a 5.8-year secular high on that late-June breakout day. That momentum fed on itself and carried gold back over $1400 for the first time since early September 2013. Those awesome $1400+ levels have mostly held since.

The gold miners’ stocks naturally leveraged gold’s gains, enjoying their own epic early-summer action. The precious-metals sector is doing wildly better than last summer, when gold rolled over in mid-June on a sharp US dollar rally. Hyper-leveraged gold-futures speculators watch the dollar’s fortunes for trading cues. Hopefully gold’s huge early-summer gains can hold, and it consolidates sideways in coming weeks.

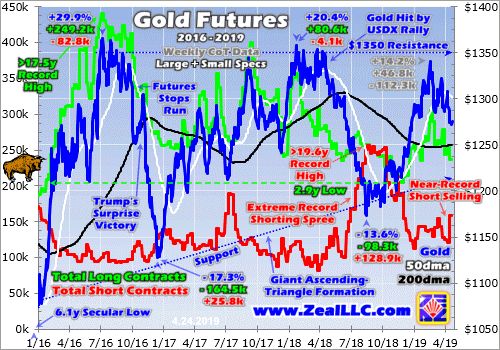

Gold’s massive and exceptional June rally was mostly fueled by speculators buying enormous quantities of gold futures. That has largely exhausted their available capital firepower, and left their collective bets on gold exceedingly bullish. These positions must be partially unwound with selling, which forces gold into a high consolidation at best and a sharp selloff at worst. So gold isn’t out of the summer-doldrums woods yet.

The inevitable coming gold-futures selling could be largely offset by investment buying. Investors are radically underinvested in gold after the second-largest and first-longest stock bull in US history, giving them big room to buy to reestablish normal portfolio allocations. Since they love chasing winners, gold’s powerful new-high psychology is starting to attract them back. Their return could dwarf gold-futures selling.

Given gold’s long-established lackluster summer-doldrums performance record, it is probably not prudent to chase this rally with gold-futures speculators effectively all-in longs and all-out shorts. But the metal and its miners’ stocks can be accumulated aggressively on any significant weakness. All portfolios need a 10% allocation in gold and gold stocks! Far-more upside is coming after recent overboughtness is worked off.

One of my core missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with superior fundamentals and upside potential. The trading books in both our popular weekly and monthly newsletters are currently full of these better gold and silver miners. Mostly added in recent months as gold stocks recovered from selloffs, their unrealized gains were already running as high as +105% this week!