The Democratic Republic of Congo (DRC) has had its fair share of scandals and problems. For the mining industry operating in the country, child labour, corruption, bribery, occupational health and safety, and environment and public health impacts have often been neglected. The country has less regulations in place to protect miners and the people that work there, and enforcement is non-existent or lackadaisical at best.

Better Mining

One organization, Better Mining, is working to improve conditions in the mining industry on and around artisanal and small-scale mine (ASM) sites. By enabling companies to support the improvement of ASM sites and surrounding communities, Better Mining is actively solving the problems that plague the industry at every level and step of the mining process. As more media attention is directed to the industry within the Republic, labour conditions and compliance have come to the forefront and are now being addressed earnestly.

The organization has worked for a while now in the DRC, and being on the ground monitoring conditions and ensuring that the conditions set are being met is an important role to fill. As ASM sites have less management monitoring and regulation, independent organizations like Better Mining are key to ensuring that conditions are being met responsibly and completely.

China Moly Lends a Hand

Tech metals producer China Molybdenum and its Swiss-based trading arm IXM have now joined the Better Mining initiative, to help ASM sites become a responsibly-managed and viable source of battery minerals. Those minerals will include cobalt and tungsten, among others.

Cobalt, a key mineral that is a byproduct of copper or nickel, is used to make the lithium-ion batteries that power everything from batteries in laptops and smartphones to electric cars. This critical mineral is an important resource for the DRC, as the country generates about two-third of the world’s supply of cobalt.

As the world’ number 2 cobalt producer and largest tungsten producer, China Moly is uniquely positioned to increase the scale and effectiveness of Better Mining, and improve the assurance and impact program to benefit the communities that rely on ASM miners. Julie Liang, director of CMOC’s sustainability executive committee, noted “As a large industrial miner that maintains strict product control and custody procedures, ASM sits outside of our own cobalt supply chain but we recognize that ASM, and those communities reliant on it, should not be neglected.”

ASM

Artisanal miners traditionally sell ore to local cooperatives. This grassroots scale operational strategy allows almost anyone with the land and the workers to extract valuable minerals and get them to market. Those cooperatives sell to local traders, who then sell to international traders or larger operating mines with established transport links.

As the largest consumer of cobalt, China is the largest consumer of the mineral coming out of the DRC, and so has a significant stake in the country and its mining industry. The success of the country’s mining industry is integral to China’s success and ability to collect enough of the valuable tech mineral.

Risks

The risks of working artisanal miners are abundant, and Western mining companies have typically distanced themselves from supply coming out of these mines. Child labour continues to be rampant in central Africa, and so the source of the raw materials may be tainted by this unethical and illegal practice.

Solutions

To try to turn the situation around, pressure has been applied to get the mining industry in the region on track toward ethical and clean mining practices. In 2019, the London Metal Exchange (LME) introduced a responsible-sourcing standard that covers all metals traded on the exchange.

The LME forced producers to demonstrate compliance with the guidance drawn up by the Organization for Economic Cooperation and Development (OECD). This major step toward stronger and more effective regulation was an inflection point for the country as they were forced to confront a global community that ultimately put its foot down on the issue.

Tesla, Google, and Apple were even sued in 2018 by a human rights ground over alleged involvement in abusive mining practices in the DRC. The supply chain stretches so far that ultimately it is impossible to know in which conditions the cobalt is mined, and so the companies sourcing their materials have a difficult responsibility to track their suppliers and ensure that they are mining ethically and safely. Amnesty Internation has stated that children as yougn as seven have been found exploring for cobalt in the DRC, and claims to have evidence that some of the biggest brands in the world have sourced cobalt from supply chains tainted by child labour.

Overwatch

Better Mining has been working to not only watch and monitor companies in the region but police them when possible and report infractions to the appropriate authorities. The DRC is now taking concrete steps toward cleaning its cobalt sector, and Entreprise Generale du Cobalt (EGC), a large company (state-owned) released its own responsible sourcing standards.

With monopoly rights to the purchase and sale of the country’s hand-mined cobalt, this is a major step in the right direction as the company has significant sway in the DRC’s mining industry. Change is afoot for the cobalt mining industry in the Democratic Republic of Congo, setting the stage for the cobalt boom from the further electrification of the global economy.

This is big, really big. I can’t say that it’s a surprise that Glencore might want to partner with First Cobalt Corp. (TSX-V: FCC) / (QTCQX: FTSSF), but it would be by far the best possible outcome for management’s strategic review of its 100%-owned refinery in Ontario. Shareholders & prospective investors were understandably growing nervous about First Cobalt’s ability to deliver the restart funding with little or no additional equity issuance. Not because of management, because the battery metals sector is a complete disaster. Everyone knows that the Cobalt price is down a lot, did you know that Vanadium is down 73.5% in 6 months? This news alone, if this agreement is consummated, could mark a turning point for select Cobalt juniors. {See full press release here}

Glencore adds tremendous credibility to First Cobalt’s Refinery

In addition to the potential for significant revenue (C$100M+ at US$20/lb. Cobalt) and good, very good or great EBITDA margins (depending on the Cobalt price), this would open A LOT of doors for the company. They would instantly become the premier pure-play, North American Cobalt junior, not that there are many left to choose from. First Cobalt could solidify its leading position by acquiring other companies & assets. Might eCobalt Solutions (TSX: ECS) be first on the list !?! eCobalt might now prefer the embrace of First Cobalt over a takeover by Australian-listed Jervois Mining. I have no insight on this, I’m just reflecting on the recent acquisition of ECS shares.

At the risk of getting ahead of myself, this is a MOU not a signed, sealed & delivered deal, I continue with the benefits of an agreement between First Cobalt & Glencore. Glencore adds increased credibility to First Cobalt, the management team and the refinery. It would be a supreme vote of confidence. Outside of North America, First Cobalt might not be a very well-known name. That would change overnight, in fact it might be changing as I write this sentence…. First Cobalt would attract additional world-class executives. The company could pay a dividend! My quick math suggests that a 5% dividend yield would be possible from 50% of the cash flow on 2,000-2,500 tonnes of production at US$20/lb. Cobalt.

Glencore would greatly de-risk Refinery restart & attract attention to FCC.v

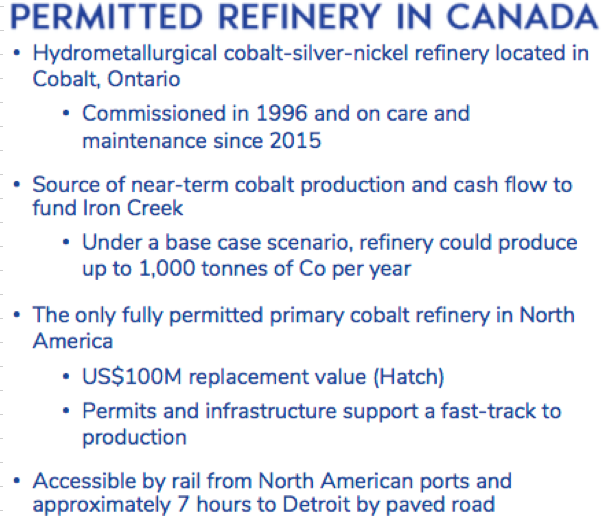

It’s amazing what Glencore would bring to the table that no one else possibly could. It appears from the press release that Glencore might provide a loan for up to US$30M, all of the capital needed, to restart the refinery. In addition, Glencore would provide technical assistance in bringing the refinery back into production, for instance they would, “collaborate on final flow sheet design.” Glencore would source up to 100% of the feedstock. The refinery is a hydro-metallurgical Cobalt facility in the Canadian Cobalt Camp of Ontario. It has the potential to produce either a Cobalt Sulfate for lithium-ion batteries, or Cobalt metal for the North American Aerospace industry and other industrial & military applications.

Taking this news a step further, if the restart were to be a success, guess who would be there to help (if feasible) ramp up operations from 2,000-2,500 to perhaps 4,000-5,000 tonnes/yr.? Glencore is to Cobalt what Albemarle and SQM are to Lithium. Yes, closing on this agreement would be really, really good for shareholders.

Assuming that Glencore is on board, the refinery would likely be up and running sooner than otherwise would be the case. And, once the world realized that a Cobalt Refinery was coming online in Canada in 2021, and that produced Cobalt would to be ethically sourced from mine to finished product, end-users would be very interested in speaking with First Cobalt. First on the list of visitors to see CEO Trent Mell would likely be execs from the automakers. The company has already signed NDAs with a number of them. Next to visit? Li-ion battery makers. Both automakers and battery companies need ethically sourced Cobalt for genuine moral considerations, for public relations and for security of supply.

As per the press release,

“With no cobalt sulfate production in North America today, the First Cobalt Refinery has the potential to become the first such producer for the American electric vehicle market. The Company has signed confidentiality agreements with several automotive companies interested in securing cobalt for the North American market.”

I have to remind myself that this is a MOU, not a done deal, but I think the chances of it getting done are pretty high. First Cobalt & Glencore have likely been talking about the refinery for months now, if not longer. And, although I’ve outlined the many benefits for First Cobalt shareholders, Glencore benefits as well. Over time, if the refinery could produce 5,000 tonnes of Cobalt products, and Glencore controls that off-take, that’s a meaningful amount, probably > 10% of the battery-grade Cobalt processed / refined & sold outside of Africa & China.

Speaking of China, recent news shows that geopolitical risks are alive and well with China hinting at restricting the free trade of rare earth metals from China to the U.S. It doesn’t matter who’s to blame, how the U.S. and China got here, all that matters are the potential consequences. Today it’s rare earth metals, will China threaten to stop exporting lithium & cobalt next? I doubt that China would sell to Canada or Mexico if there was an embargo against the U.S. for rare earth metals, lithium, cobalt, vanadium, graphite, etc.

But now I’ve veered off course, this isn’t about China… The news today is about Glencore signing a MOU with First Cobalt Corp. (TSX-V: FCC) / (OTCQX: FTSSF) to help design, re-engineer, refurbish & commission the company’s Cobalt refinery in Ontario. Glencore could deliver up 100% of the feedstock needed to produce 2,000-2,500 tonnes of finished Cobalt. And, Glencore is considering paying the entire US$30M cost (in the form of a loan to First Cobalt Corp.) to get it up and running again. This is the biggest news of the year for the Company. This is important news for the Cobalt sector. Let’s see if this marks a change in sentiment for Cobalt juniors.

May 24, 2019

Peter Epstein

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Cobalt Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Cobalt Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of First Cobalt Corp. and the Company was an advertiser on Epstein Research [ER].

Readers should consider me biased in favor of the Company and understand & agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

The market for natural resources remains subdued, but there are pockets of strength. In the Uranium sector, Energy Fuels, IsoEnergy & Appia Energy are up an average of ~150% from their respective 52-week lows. In Copper, Trilogy Metals & Pacific Booker are up an average of ~250%. Good things are happening, but not in Cobalt, at least not yet.

Could This Pure-Play, North American Cobalt Junior Shine Again?

However, when natural resource stocks gather steam, other sectors will join the party, and select Cobalt names will be invited. That doesn’t mean they all will, many companies are broken beyond repair. Last year there were over 100 Cobalt juniors listed in North America alone. Most are still-listed, but many can’t raise a penny to move projects forward. I believe there are fewer than 10 Cobalt names worth looking at.

One of 2017’s blue chip Cobalt juniors that I think has ample room for upside (again) this year is First Cobalt Corp. (TSX-V: FCC) / (OTCQX: FTSSF) / (ASX: FCC). The Company just raised C$1.6 M. Sell-side analysts peg the stock price in a range of C$0.70 to C$1.00. Yet, the current price is C$0.145. Without going into the analyst’s methodologies, (I have not seen the reports), I can see why they’re bullish. But before continuing, we need to discuss the pink elephant in the room – Cobalt prices – you may have noticed that they are down quite a bit.

But, What About the Cobalt Price?

That’s a big problem, but only for readers who believe that Cobalt will remain below US$15/lb. If one does not believe the price will rebound, then First Cobalt Corp. is not the stock for you. I’m not suggesting the price will soon soar, but a near doubling in the price to US$25/lb. in the next year could propel the best positioned companies higher, perhaps a lot higher. The price was > US$40/lb. < 12 months ago, and at US$25/lb. < 3 months ago.

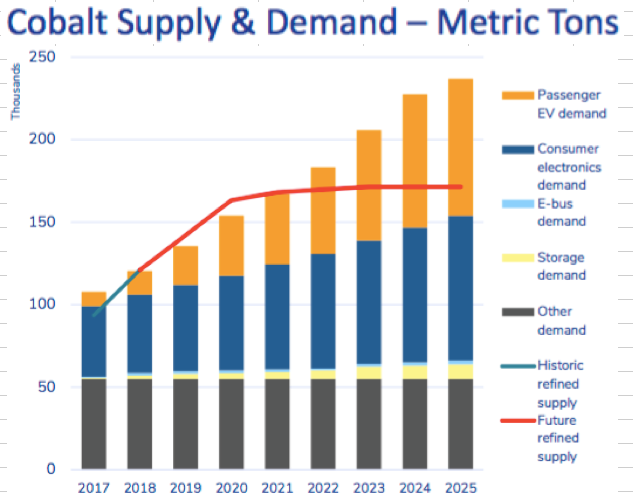

For those fearing that Cobalt is being engineered out of Electric Vehicle batteries due to high cost and/or security of supply concerns, they are only partially correct. I defer to industry experts Benchmark Mineral Intelligence. In February Simon Moores said, “As the energy storage revolution continues to pick up pace, Cobalt demand is set to rise 4 times by 2028.” That would be a 15% CAGR. The 8.1.1 chemistry is Nickel-Manganese-Cobalt in the ratio of 8:1:1.

Experts That I Trust See Strong Cobalt Demand Through 2028

Cobalt was designated a strategic mineral in the U.S. and in many other countries. I believe it will remain in strong demand, and that North American sources will be highly sought after. There’s growing discussion about the 2021 & 2022 EV model years being a global tipping point. Security of supply dictates that Cobalt needs to be locked up by end users well before then. The U.S. is not low on Cobalt supply…. it has NO domestic Cobalt supply!

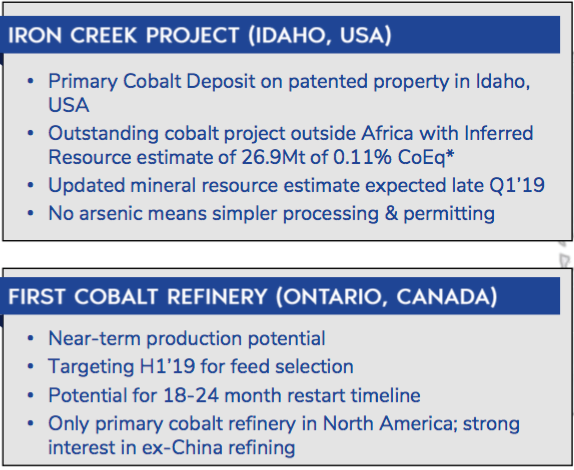

In addition to controlling ~45% of the past-producing Cobalt, Ontario, Cobalt-Silver camp, First Cobalt owns 100% of a fully-permitted, primary Cobalt Refinery. It can produce Cobalt Sulphate or Metallic Cobalt products and is the only one of its kind in North America. Management believes it could be up and running in 18-24 months.

Very Few Cobalt Juniors Have Hard Assets, like a Permitted Cobalt Refinery

Mining services firm Hatch estimated the Refinery’s replacement value at US$ 100M = C$ 133M. That figure does not include the time value of money, the 4-6 years it might take to get a new refinery designed, permitted, funded, constructed & commissioned. Compare that to the Company’s Enterprise Value [market cap + debt – cash] of ~C$43M. The estimated replacement value of the Refinery alone is 3 times First Cobalt’s entire Enterprise Value! There are few options outside of China to produce Cobalt Sulfate for the battery market, and management says there’s no other near-term refining prospect in North America.

How much revenue could the Refinery generate? At the Company’s base case of 1,000 tonnes/yr., at US$20/lb., that’s roughly US$44M = ~C$59M in revenue. Energy Fuels, an established uranium / vanadium producer, trades at 11.8x trailing 12-month revenue. SQM, a large lithium producer, trades at 4.8x. Bushveld Minerals, a vanadium player, trades at 6.2x, Katanga Mining, a Copper-Cobalt producer with operations in the DRC, trades at 6.4x. Those companies average ~7x trailing revenue. All have refineries or processing facilities. I’m not saying that First Cobalt will or should trade at 7x revenue. However, one can see the potential value of owned & operated hard assets.

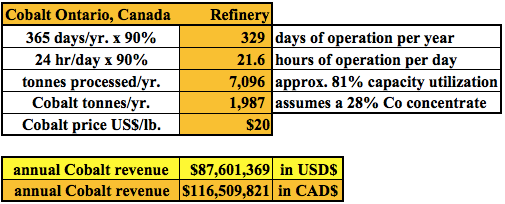

In the bare bones analysis above, I estimate what revenue the Refinery could generate operating 90% of the days in a year and 90% of the hours in a day. Combined, that’s 81% annual capacity utilization. I assume a 28% Cobalt concentrate feedstock, and a 90% recovery of Cobalt. At a price of US$20/lb., annualized gross revenue would be ~C$117M. At US$25/lb. it would be ~C$146M, and at US$30/lb. gross revenue would be ~C$175M. Although US$30/lb. Cobalt seems high today, it might not be in 2 years. As mentioned, the price was > US$40/lb. less than 12 months ago. However, to be clear, there’s no guarantee of a meaningful rebound in price.

I fear that investors are treating the estimated replacement value of the Refinery like they would the Net Present Value (“NPV“) of a mining project. That would be a mistake. The estimated value of a hard asset is more reliable than the NPV of a project, especially if the NPV comes from a PEA or PFS. Management says the Refinery can be monetized (cash flowing) in 18-24 months. By definition, a NPV is the present value of future cash flows stretching out decades.

First Cobalt’s Refinery Has Estimated Replacement Value of US$100M

First Cobalt is trading at ~0.33x the estimated replacement value of the Refinery alone. That means investors today get the Company’s flagship project in the U.S. for free, plus 50 past-producing mine sites in Cobalt, Ontario, with a large margin for error embedded in the estimated value of the Refinery.

There’s considerable risk for mining projects at PEA or PFS-stage. First Cobalt’s Refinery simply does not carry that kind of risk. Management needs to arrange funding to get it into production, that’s the primary risk. And, a higher Cobalt price would be nice. However, unlike for mining projects, the Company does not need to raise hundreds of millions of dollars. It needs ~US$25M (includes a 30% contingency). That funding should be achievable through a combination of debt, equity, streaming/royalty financing, and/or selling a portion of the asset.

U.S. Project Iron Creek has 45M lbs. Cobalt + 175M lbs. Copper, With Substantial Upside

Nearly 1,000 words in and I haven’t discussed First Cobalt’s flagship project, Iron Creek in Idaho (USA). There are very few primary Cobalt projects in the world. This one has a resource (26.9 M tonnes) that will be upsized by up to 50% (my guess only) this quarter. The existing resource contains an estimated 45M pounds Cobalt + 175M pounds Copper. Importantly, there’s no arsenic, which means simpler processing & permitting. The grade is low, so I asked CEO Trent Mell about that. His response,

“One can certainly point to some high-grade Cobalt drill results that have been released over the past couple of years, but these are typically vein-style deposits that struggle to hold together in resource modeling. In other words, grade is worthless without sufficient tonnage. By contrast, there are a number of Australian Nickel-Cobalt deposits that have the tonnage but lower grades than we have at Iron Creek.”

The rule of law, plus strong access to infrastructure, plus superior proximity to U.S. markets, make Iron Creek a desirable project compared to the dozens of projects & mines in Africa, a continent that accounts for up to 75% of global supply. Sourcing Cobalt from North America is becoming more important by the day. It will be interesting to see the size of the new resource and how much larger still the resource could become next year.

Iron Creek remains open in all directions. That suggests the possibility of a much larger resource. If the Company could double the size, that would greatly enhance the indicative economics of a PEA or PFS. In addition, CEO Trent Mell has mentioned the potential contribution from Copper. He said that up to one third of Iron Creek’s revenue could come from Copper. That would be a tremendous credit against the primary Cobalt production costs. I’m a big fan of Copper, the world cannot have an energy revolution (clean/green renewable energy sources), or the electrification of passenger & commercial transportation, or the building & rebuilding of critical infrastructure, without Copper.

Conclusion

I said that there are 10 or fewer Cobalt juniors worth looking at. First Cobalt (TSX-V: FCC) / (OTCQX: FTSSF) / (ASX: FCC) is high on the list. It has a lot of boxes checked, but at the same time, is still relatively early-stage. So, there’s high return potential, with commensurate high risk. As more boxes get checked, like the upcoming resource update at Iron Creek, ongoing metallurgical testing, lining up feedstock & funding sources for the Refinery…. this de-risking should get noticed by the market. That, and the estimated value of the Refinery being 3 times larger than the Company’s entire Enterprise Value, suggest today’s share price could be an attractive entry point.

{latest Press Releases}

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Cobalt Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Cobalt Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of First Cobalt Corp. and the Company was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

February 2018 saw 84 deals close in the Canadian financial markets for an aggregate C$367.0 million at an average of $4.5 million, down 15.2% over January 2018 when 105 deals closed for an aggregate C$432.8 million at an average of $4.32 million.

February saw 14 brokered deals close for an aggregate $250.0 million at an average of $17.9 million. This was up 54.3% from the nine brokered deals in January that closed for an aggregate $162.0 million at an average of $18.0 million.

Within the brokered deals, six bought deals closed in February for an aggregate of $136.7 million deal at an average $22.8 million, an increase of 29.1% over the five bought deals that closed in January for an aggregate of $105.9 million deal at an average $21.2 million.

95 deals opened in February

The top ten deals by size closed in February totaled $230.1 million with gold leading the field taking three spots of the top four spots and five of the top ten. Battery metals cobalt and lithium took three spots.

The top ten deals by size closed in January totalled $241.3 million with graphite, copper and tin leading the field. Gold took three spots of the top ten with cobalt also figuring.

February saw 56 gold deals close for $229.2 million at an average of $3.4 million, up 119.1% in total value terms from the $104.6 million raised in 44 gold deals in January at an average of $2.3 million. The top ten gold deals in February totalled $184.7 million, some 76.5% of the total.

Base metals accounted for $73.6 million of the funds raised in February, some 30.5% of the total, with the top ten deals accounting for $36.7 million with zinc and copper featuring heavily.

Battery metals accounted for $74.8 million of the funds raised in January, some 31.0% of the total and where the top ten battery raises brought in $73.6 million with three cobalt, five lithium one copper and one graphite raises.

#1 Torex Gold $61.7 million

Torex Gold Resources (TSX:TXG) closed a C$61.7 million offering underwritten by a syndicate led by BMO Capital Markets on a best efforts basis.

#2 Orla Mining $30.8 million

Orla Mining (TSXV: OLA) closed a C$30.8 million offering underwritten by a syndicate led by GMP Securities on a bought deal basis. Each unit included half a warrant that expires in 36 months.

#3 eCobalt Solutions $29.9 million

eCobalt Solutions (TSX: ECS) closed a C$29.9 million offering underwritten by a syndicate led by TD Securities on a bought deal basis. Each unit included half a warrant that expires in 18 months.

About Oreinc.com:

Oreninc.com is North America’s leading provider of relevant financing information in the junior commodities space. Since 2011, the company has been keeping track of financings in the junior mining as well as oil and gas space. Logging all relevant deal and company information into its proprietary database, called the Oreninc Deal Log, Oreninc quickly became the go-to website in the mining financing space for investors, analysts, fund managers and company executives alike.

The Oreninc Deal Log keeps track of over 1,400 companies, bringing transparency to an otherwise impenetrable jungle of information. The goal is to increase the visibility of transactions and to show financings activity in a digestible format. Through its daily logging activities, Oreninc is in a position to pinpoint momentum changes in the markets, identify which commodities are trending and which projects are currently receiving funding.

Website: www.oreninc.com

![]()

Power Americas Minerals (TSX-V: PAM) / (OTCQX: PWMRF) is well positioned among roughly 18 juniors exploring for Cobalt (“Co“) (and associated gold/silver) in the world-class, past-producing Silver-Cobalt Mining Camp in northeastern Ontario, Canada. Although reports vary, something on the order of 400-750 M ounces of Silver (“Ag”) and 40-50 M pounds of Co were produced in the district.

Power Americas has assembled a moderate-sized (vs. its peers) 3,330 hectare (~8,230 acre) land package, 100%-owned, on 15 un-patented mining claims.

Others have properties in and around the district, most notably First Cobalt Corp., (TSX-V: FCC) and Cobalt Power Corp. (TSX-V: CPO) who, like Power Americas, have substantially all of their assets in Ontario. First Cobalt is the bellwether Co name in the region, but it has a C$236 M market cap., ~24 times larger than Power Americas’ ~C$10 M market cap. Cobalt Power is a ~C$28 M company. NOTE: {First Cobalt has by far the largest Co footprint in Ontario, PLUS the only permitted cobalt extraction refinery in North America}.

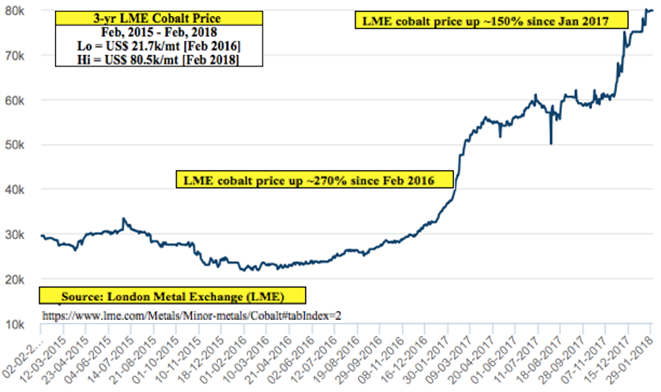

Importantly, none of the new players have advanced beyond early exploration stage. All of these stocks are highly speculative, and most companies probably would not exist were it not for the booming Co price– which has nearly quadrupled — (from US$21.7k/tonne in Feb 2016 to US$80.5k/tonne in Feb 2018) in the past 2 years.

Importantly, Power Americas has additional drill results to report this month and next. The Company is looking for multiple hits of 1 or more meters of greater than 1.00% Co mineralization, which would be better than most peers in the district have reported so far.

Perfect Storm for Cobalt Prices?

In the Co price chart above, notice the steepness of the curve over just the past several months. Cobalt has almost quadrupled (up ~270%) since February 2016 and is up ~150% since the beginning of last year. The move in Co prices is very similar to that of lithium prices, although lithium prices began moving 6-9 months earlier, and have not been moving up lately the way Co prices have.

Readers are likely aware that over 50% of global Co supply comes from the DRC, and that end users are very anxious to source Co elsewhere due to ongoing concerns about child labor law abuses. Making matters worse, the DRC (suddenly) raised its royalty rate on Co from 2% to 10%, and imposed a 50% “super-profits” tax — defined as income earned on sales of Co at prices > 25% above the price in a Company’s Feasibility Study.

This news comes at the same time that a number of major automakers like BMW, Tesla & Volkswagen are reportedly searching for long-term off-take agreements for cobalt & lithium. Of note, BMW is said to be close to a 10-yr agreement with an unnamed party. The DRC will remain the largest producer for years to come, but the playing field is wide open for supply from Canada and other more business-friendly countries.

Given the proverbial perfect storm for cobalt prices, the early-stage projects / properties in and around Cobalt Ontario could be among the better alternatives for Co supply next decade. Getting back to Power Americas, the management team is excited about the drill results they will be reporting shortly.

Jeffrey Cocks, President & CEO, stated,

“We believe we have assembled a sizable, 100%-owned land package [3,330 ha] that encompasses and surrounds several historical cobalt mines in the most active Cobalt Mining Camp in Canada. We’re highly encouraged by our initial 2017 Exploration Program’s results, and very excited to build off these results with our 2018 winter program that is currently underway.”

Neil Pettigrew, VP Exploration, explained an important factor that differentiates Power Americas from many nearby peers,

“Cobalt mineralization on the Kittson property occurs both in veins and fractures, this gives us a wider target zone. The mineralized zone also displays a fairly consistent strike and dip, these advantages give us a faster pathway toward defining what could be the first new NI 43-101 compliant cobalt resource in the camp.”

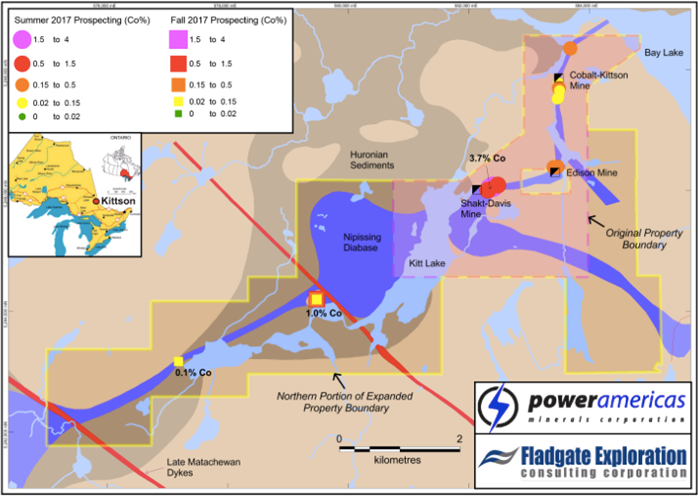

The Company’s Co contained mineralization is similar to that of the famous Silver-Cobalt Camp in Ontario, Canada, located ~15 km to the east. It contains the historic Shakt-Davis and Cobalt-Kittson mines, 4 mine shafts and numerous historic workings; the deepest extending down to 628 feet, and combined, > 2,500 feet of lateral development.

In late 2017, management acquired an additional 100% interest in 10 unpatented mining claims totaling ~2,240 hectares. Eight of the new claims are contiguous to the Kittson property and are interpreted to host the western extension of the Shakt-Davis and Edison mine structures. The other 2 are ~5 km south of the Kittson properties’ southern boundary.

Drilling is the Main Catalyst This Quarter

Management announced on January 23rd that it has commenced drilling on the 100% owned Kittson-Cobalt project. A total of 18 holes and 2,000 meters is underway as a follow up on the Fall 2017 ultra-light drill program. Sixteen holes are planned at the historic Shakt-Davis mine, and 2 on the northern extension of the historic Edison mine. Drill holes lengths of 75 to 250 m will test mineralization both near surface and below historic workings. Drill results will be released later this month and into March.

The fracture zone hosting the Shakt-Davis mine has returned grab samples up to 3.66% Co and 1.62% Co over 0.3 m in shallow drilling. The northern extension of the Edison mine hosts numerous historic trenches which have returned up to 0.49% Co in grab samples.

On January 16th, the Company announced results of their diamond drill program on the Kittson-Cobalt project. Seven shallow holes, totaling 161 meters were drilled beneath overburden-filled historic workings in the Shakt-Davis mine area. The program successfully intersected a fracture zone that hosts the Shakt-Davis mineralization over a strike length of 55 m, up to ~30 m deep. The zone is 5-13 m wide (drilled core length).

Commenting on these results, CEO Cocks said,

“These results represent the first drilling since the 1940’s at the Shakt-Davis mine and confirm the cobalt-rich nature of this extensive fracture zone. The zone which hosts the Shakt-Davis mine is related to those which also host the Kittson & Edison mines to the north and east, respectively, cumulatively representing over 3 km of strike length.“

Veins hosting the mineralization at Kittson differ from the typical Cobalt Silver Camp veins in that they are lower in Ag but richer in Co, and are associated with zones hosting meaningful amounts of Au. From assessment files in the Cobalt MNDM office,

“Assays and analyses indicated 1.5% Co and minor Ag over a width of 1.37 m, with select grab samples indicating up to 4.0% Co, and others with up to 2.72 oz/t gold. A further test of hand-picked ore indicated values of 0.87 oz/t Au, 7.92% Co & 7.72% Ni. Another sample returned 97 oz/ton Ag & 0.336% Co.” (Born and Hitch, 1990).

Conclusion

Power Americas Minerals (TSX-V: PAM) / (OTCQX: PWMRF) has as good a chance as any to find promising cobalt mineralization in Cobalt Ontario. A key takeaway from this article should be that Power Americas owns properties that have evidence of mineralization that is lower in silver but richer in cobalt, and is associated with zones hosting meaningful amounts of gold. And, the Company has a substantially lower market cap at C$ 10 M than many of its peers in the district.

Finally, near-term drill results, if they show some hits containing relatively large intervals of greater than 1.00% cobalt– could attract investor attention and drive the share price higher.

Disclosures: The content of this article is for informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research, [ER] including, but not limited to, commentary, opinions, views, assumptions, reported facts, estimates, calculations, etc. is to be considered implicit or explicit, investment advice. Further, nothing contained herein is a recommendation or solicitation to buy or sell any security. Mr. Epstein and [ER] are not responsible for investment actions taken by the reader. Mr. Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Mr. Epstein and [ER] are not directly employed by any company, group, organization, party or person. Shares of Power Americas Minerals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares and/or stock options in Power Americas Minerals and the Company was an advertiser on [ER]. By virtue of ownership of the Company’s shares and it being an advertiser on [ER], Peter Epstein is biased in his views on the Company. Readers understand and agree that they must conduct their own research, above and beyond reading this article. While the author believes he’s diligent in screening out companies that are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

![]()

‘In order to produce half a million cars a year…we would basically need to absorb the entire world’s lithium-ion production.’ – Elon Musk

“The skillsets that young people should learn about mining should apply to everything. We just need to do a better job of explaining to people in urban environments that the human activity of mining is absolutely fundamental to the way this planet is going to evolve. Completely and totally fundamental.” – Robert Friedland, Ivanhoe Capital

The future envisioned by industry leaders hinges heavily on the production of new materials to power and build the future. Leaders such as Elon Musk have been developing the blueprint for the future with electric cars, battery grids and renewable energy solutions. While, other leaders such as Robert Friedland are looking to supply the materials to build this future. Mr. Friedland makes the case and understands the story that is unrolling in real time. Mining is the critical component to meet the world’s demands for a sustainable future. The prerequisite for this future is mining and with every mineral discovery and development project, this future is coming closer.

Mr. Friedland is not the only miner that realizes the economy of tomorrow will require the development of new mining assets. Azincourt Energy Corp. (TSX-V: AAZ) is a Canadian junior exploration company that has been actively building their mining asset portfolio in anticipation of the future demand for minerals that will provide clean energy; from lithium to uranium to cobalt.

Azincourt Energy Chairman, Ian Stalker is an experienced mining executive that sees the writing on the wall when it comes to the materials and fuel that future technology will require. Mr. Stalker is a senior international mining executive with over 45 years of hands-on experience in resource development. Over his career Mr. Stalker has directed over twelve major mining projects, from exploration drilling to start-up, including gold, base metal, uranium and industrial minerals. He is currently CEO of LSC Lithium (TSX.V: LSC), and Chairman of Plateau Uranium (TSX.V: PLU), and is the former CEO of UraMin Inc., the London and Toronto listed public uranium company that was acquired by Areva for US$2.5 billion in August 2007. In a recent press release, Mr. Stalker outlined the current strategy for Azincourt.

“The lithium market is obviously very strong right now, and the near-term future for lithium demand remains extremely positive. Our decision to expand Azincourt’s focus to include lithium and other materials is something we feel strongly about. To get a foothold and exposure in this environment, at this time, is an important and strategic step for us.”

Azincourt recently acquired five lithiums projects in located in the Winnipeg River Pegmatite Field, Manitoba, Canada. Two of the projects, the Lithium One and Two projects, are adjacent to Quantum Minerals Corp.’s Cat Lake lithium project which includes a historical estimate from drilling in 1947 that defined 545,000 tonnes of 1.4 percent lithium oxide (Li2O). Drilling could prove up this ground.

Two other of the acquired lithium projects, the Lithman West and East projects are adjacent to the Tanco Mine lease property. These projects are part of the Winnipeg River pegmatite field which hosts numerous lithium-rich pegmatites or “hard-rock” lithium such as the Tanco pegmatite that has been mined at the Tanco mine since 1969 for spodumene, a major component for hosting lithium (Li), and other rare earth ores.

Azincourt has scheduled exploration work to begin in the spring of 2018, with a field program that includes detailed mapping of the known pegmatite outcroppings on the Lithium One and Lithium Two projects. This will be followed immediately by a comprehensive chip sampling program designed to generate targets for the drill programs anticipated at both properties during the summer of 2018.

Previous work in 2016 produced twelve samples between a range of 0.02 per cent to 3.04 per cent Li2O from the Eagle pegmatite, and up to 2.08 per cent Li2O. Select sampling will concentrate on the Eagle and FD5 pegmatites at Lithium Two, and on the Silverleaf pegmatite at Lithium One, which returned values as high as 4.33 per cent Li2O in the 2016 exploration program (see press release dated Feb. 1, 2018).

On Feb. 8, 2017, the company signed a non-binding letter of intent to acquire the BullRun erythrite project, a prospective cobalt property located six kilometres northwest of the town of Cobalt, Ont. (see press release date Feb. 8, 2018). Alex. Klenman, President and CEO of Azincourt Energy commented on the company’s strategy with this acquisition.

“We’ve been looking into adding a potential cobalt property as we grow our project portfolio, so we’re pleased to move to LOI on this. We are going to immediately begin a comprehensive due diligence process to gain as much understanding as we can on the potential of the project, and we hope to progress to the definitive stage in due course. In addition, we are actively reviewing other potential projects that will continue to strengthen the company in the growing clean energy space. We haven’t filled our want list yet, so we remain very active on the acquisition front.”

True to the company strategy, Azincourt announced a new project that is adjacent to the western edge of Plateau Uranium’s (TSX-V: PLU) Macusani Project in Peru. This project contains the high-grade Falchani discovery that includes consistent 3,000-3,500 ppm Li over 100m intercepts at depth, and U3O8 grades up to 500 ppm over 50m intercepts at surface. The plateau features areas of uranium-rich surface mineralization as well as lithium mineralization at depth.

Initial leach test results conducted by Plateau Uranium in December showed that 77-80% of contained lithium can be extracted from Falchani. Plateau’s Macusani Project is fast becoming one of the world’s largest undeveloped uranium-lithium districts. Although Macusani started life as a pure uranium story, exploration and metallurgical work has unearthed the lithium resource at depth.

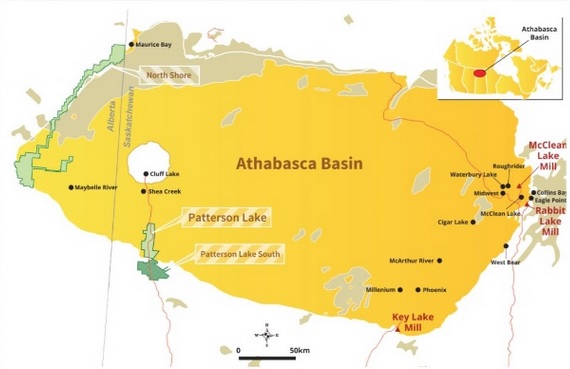

The company has been developing two projects in the Athabasca basin, in Northern Saskatchewan, home to the largest and highest grade deposits in the world, the Preston Project and the Patterson North Lake Property.

The Preston project comprises a large land position (approx. 121,249 hectares) strategically located to the south of NexGen Energy’s (TSX-V: NXE) Rook 1 project hosts the high grade Arrow deposit, as well as proximal to Fission Uranium’s (TSX: FCU) Patterson Lake South project host to the high grade Triple R deposit. The company has 15 drill target areas associated with eight prospective exploration corridors that have been successfully delineated through extensive geophysics.

The second project, The Patterson Lake North property “PLN” lies next to the northern edge of the Patterson Lake South property, owned by Fission Uranium Corp. (TSX-V: FCU) where uranium mineralization has discovered over 2.24 kilometres (east-west strike length) in four separate mineralized “zones.”

To date Azincourt has spent $3 million earning into PLN. Prior to Azincourt’s involvement, Fission spent approximately $4.7 million on exploration on PLN. There are three separate target areas that are drill-ready.

Azincourt Energy Corp. recently completed a private placement for gross proceeds of $1,655,000. In addition, the company has received an additional $1,215,009.48 in gross proceeds from the exercise of warrants over the past several weeks.

“We have more than enough funds to meet existing work requirements on our lithium and uranium projects for the next year or so, and further, the additional funding means we have upward flexibility in how we approach our work programs and portfolio expansion. Simply put, we can put more dollars into the ground, and into acquisitions,” said Mr. Klenman.

With ~69 million shares outstanding, cash in the bank, the company trading at 19 cents, the company has plenty of exploration news on the way, shares in Azincourt present a current opportunity.

While inventions and ideas grab the headlines, little attention is given to the fundamentals of building a clean energy future. Azincourt Energy Corp. (TSX-V: AAZ) has put together an impressive portfolio of mineral projects from lithium, uranium to cobalt; the minerals that will fuel the future. Azincourt Energy is in the early stages and with news on the way, investors should pay attention.

Clicker Here to Visit the Company’s Web Page: http://azincourtenergy.com/

*** The mineral reserve estimate cited above as part of the Lithium Two project is presented as a historical estimate which does not conform to current National Instrument 43-101 standards. A qualified person has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves. Although the historical estimates are believed to be based on reasonable assumptions, they were calculated prior to the implementation of National Instrument 43-101 standards. These historical estimates therefore do not meet current standards as defined under sections 1.2 and 1.3 of NI 43-101; consequently, the issuer is not treating the historical estimate as current mineral resources or mineral reserves.

***MiningFeeds.com was compensated for the creation and publication of this article. This does not constitute investment advice.

Cobalt is classified as a strategic metal by the United States Government and a critical metal by the European Union. Highly purified cobalt, a technology metal, has applications in the aerospace industry because it is very resistant to corrosion and damage, even at high temperature. It is also used in the manufacturing of rechargeable batteries and in medicine.

Although cobalt’s use is varied, only about 76,000 tons of refined cobalt was produced globally in 2010. With cobalt trading on the London Metals Exchange for$35,000 per tonne, this represents an estimated market value of US$2.7 billion. The main source of the element is as a by-product of copper and nickel mining. The copper belt that runs across the Democratic Republic of the Congo and the Republic of Zambia yields most of the cobalt mined worldwide. But one company is looking to break tradition.

Formation Metals is well on their way to becoming North America’s next cobalt producer having raised over $170 million in equity financing. Based on a NI 43-101 technical report released by the company in 2007, the Idaho cobalt project’s projected output will be equivalent to 3.3% of global cobalt supply which translates into 14.9% of North American’s annual demand. With political issues in the Congo which have, since 1998, chronically threatened to disrupt global cobalt supply, Cobalt’s recent status as a strategic metal and proximity to local markets in the U.S., some think Formation Metals is a good bet.

Jennings Capital analyst, Ken Chernin, issued a speculative buy recommendation on May 26th, 2011 with a 12 month target of $2.60, more than double today’s current price of $1.24. Chernin sites low costs of production, few impurities, the mine’s U.S. location and the company’s hydrometallurgical facility as reasons for his recommendation.

MiningFeeds.com recently connected with the President & CEO of Formation Metals, Mari-Ann Green, to find out more about cobalt and the company’s progress in Idaho.

Cobalt is a minor metal, one that many of our readers may not be familiar with, could you please provide some background on pricing and production?

Cobalt is a metal that many readers may not be familiar with, but they come across it every day in items from re-chargeable batteries to jet aircraft. It is also used in a number of green energy technologies including hybrid cars, fuel cell and wind turbine technologies, and as a catalysts in oil de-sulfurization and in Gas to Liquids technologies. Because of its use in jet turbine engines, cobalt is alloyed with steel to form high strength critical components of the moving parts of these engines. The U.S. government considers cobalt a strategic metal and yet they have no domestic source. We plan on providing the U.S. with a stable domestic source of this critical metal.

The price of cobalt has averaged around $22/lb over the past couple of decades, and high purity super-alloy grade material, 99.9% purity or better, the variety that Formation plans to produce, goes for about $20/lb today. Last year in February, the London Metal Exchange started trading “Grade B” material, which ranges in purity from 99.3% – 99.8%. This “low grade” cobalt trades at around $16.00 lb at the moment.

The copper belt in the Congo and Zambia yields most of the cobalt metal mined worldwide; however, your lead project is based in Idaho in the United States. Please tell us about the project.

That’s correct. Western Africa accounts for about 65% of the world’s production. Historically, the price of cobalt has risen sharply in response to political developments in the region that led to uncertainty of future supplies. Our project, on the other hand, is located in the heartland of the United States, who accounts for 58% of the world’s consumption of superalloy grade cobalt. We also own and operate a hydrometallurgical refining facility, which will be capable of producing the high purity cobalt metal right here in the U.S. – and we will be the only company in the country doing that.

What are the key differences between your deposit and those found in Africa?

There are a number of differences. Firstly, as was pointed out already, the project is located in the United States which is a big consumer of cobalt but does not have a domestic source of the metal. Secondly, it is the only primary cobalt deposit in the country. Just as importantly, we know from metallurgical test work that it will be capable of producing high purity cobalt suitable for critical applications in the superalloy sector. Lastly, being able to refine the metal ourselves offers the great advantage of producing value added end products that meet the high standards and specifications for domestic end users.

We hear about cobalt being a “conflict metal” but cobalt production in the Congo is produced in the Katanga province, hundreds of miles away from the conflict zones in the eastern part of the country. What is your take on this status?

Cobalt from the Congo is not defined as a conflict mineral, unlike coltan from the eastern provinces where niobium and tantalum are extracted. However, cobalt produced from the Congo often ends up being comingled with ore from other areas and refined out of the country. This produces end products with uncertain supply chains. End users, like large electronic companies, are being held to task more and more about where the raw materials used in their products originate from. Being able to clearly demonstrate a continuous supply chain of ethically sourced raw materials is becoming more and more important in today’s emerging socially responsible corporate world.

Formation Metals also has gold/silver projects and uranium projects, to what degree are you focused on developing your other projects and what are your long term plans in these other areas?

Yes, we have several satellite projects that we expect to do more work on as the cobalt project nears production. We have a number of gold projects in Idaho that have been on care and maintenance while we moved the cobalt project towards construction. Strong precious metal prices has resulted in renewed interest in these projects, which are likely to see more work done on them by ourselves, or through joint venture opportunities.

In the state of Tamaulipas in Mexico, we own a high grade silver-lead zinc project where grab samples have returned silver values near 2kg/ton. We recently announced we had acquired additional central ground on the project, and we expect to do more exploration work to define drill targets in the fall and winter of this year.

Lastly, we have two uranium projects in the Athabasca basin of Northern Saskatchewan joint ventured with Cameco and AREVA. One of the projects, the Virgin River project, where Cameco is acting as operator, has discovered the Centennial Deposit, a high grade uranium deposit that has been traced for over 650 metres. Cameco has indicated they are looking for a McArthur River style deposit, the largest and highest grade deposit on the planet, and to date they have spent over $26 million dollars developing the Centennial deposit. The project has returned results as high as 8.8% U3O8 over 34 metres – that’s 8.8% over 110 feet! They are currently drilling the project with a budget of $3 million for this year. We have a vested 2% interest in the project with the first right of offer to earn up to 10%. Time will tell how that project develops, but at this stage the future looks promising with continued excellent results coming from the project.

On July 26th Formation announced that mine site earthworks construction commenced on your Idaho Cobalt Project, what does the timeline look like going forward and when do you hope to be in production?

We actually completed Stage I construction last year with timber clearing and site preparation, and this Stage II of construction will see the development of the portal bench and the construction of the mine site structures. If all goes according to plan, it is expected to take about a year to construct, so conceivably, we could be in production by this time next year.

This interview is featured in the article 5 Critical Mineral Stocks to Watch – CLICK HERE – to read more.

If you would like to receive our free newsletter via email, simply enter your email address below & click subscribe.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fanCONNECT WITH US

Tweets

Tweet with hash tag #miningfeeds or @miningfeeds and your tweets will be displayed across this site.

MOST ACTIVE MINING STOCKS

Daily Gainers

|

CMB.V | +900.00% |

|

EDE.AX | +100.00% |

|

GXU.V | +62.50% |

|

CRD.V | +33.33% |

|

RJX-A.V | +33.33% |

|

CASA.V | +30.00% |

|

NAR.V | +29.17% |

|

GBZ.AX | +28.57% |

|

POS.AX | +25.00% |

|

PX.V | +20.00% |