Gold and silver mining stocks face increased risks and uncertainty in 2018, not seen by investors and mining management teams for quite some time. Many of the top risks to gold stocks are related to geopolitical and financial, which will only compound the already high operational risks. Many of these top risks to gold stocks can be applied to silver stocks and any commodity stocks as well. What was most interesting, many of these risks are not seen as a concern to the management teams of Newmont Mining or Barrick Gold when going through their 10-Ks, versus the elevated risks the investment community sees in the macro landscape. Is the investment community concerned with many risks or is management thinking many of the risks won’t happen to them? These risks can heighten mining risk because of the elevated geopolitical and financial risks, potentially disrupting supply, and driving up gold prices even further without gold demand increasing.Are these the catalysts that will push up higher gold prices?

HISTORY REPEATS

Over a long-term enough time horizon, the sixteen biggest risk events repeat, but with a slight twist. The risks are the same, but the characters in the play are different. Capital controls, nationalization of assets, labor disputes, increased regulation on assets, and royalty changes. They all have occurred during different time periods, at some point or another. Most are tied to miners generating an incredible amount of profits, and individual countries wanting to get a bigger share of those revenues. It’s hard to move a mine, putting the mine at increased operational and political risk to earn more on those assets.

GEOPOLITICAL RISKS

Geopolitical Escalations Disrupting the Supply-chain

Government Election Uncertainty

Tariffs (on Mine Supplies)

Export Restrictions of Commodities

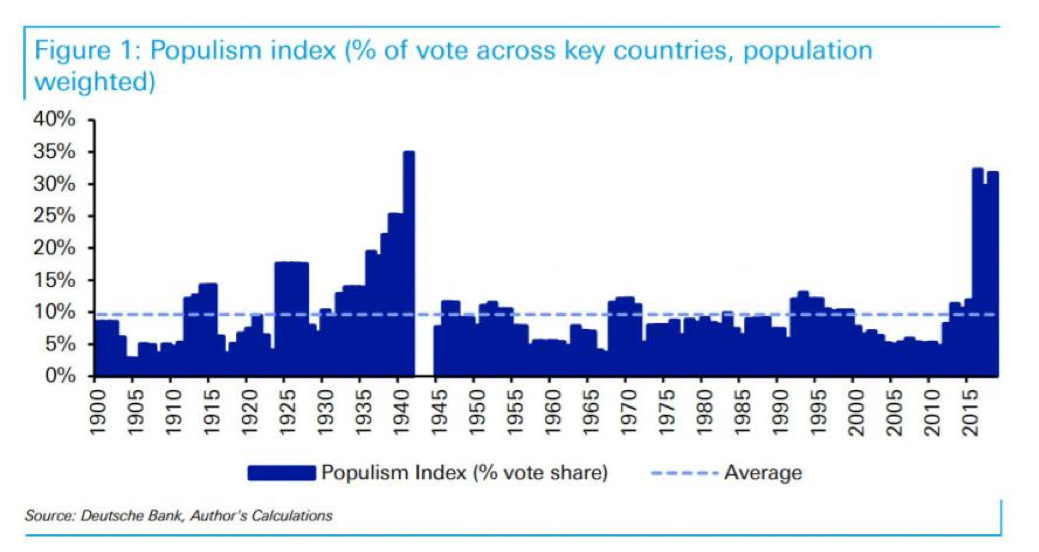

Supply disruptions from geopolitical are at heightened levels of risk not seen since the 1930’s and 1940’s, because of increased geopolitical risks. All of this political uncertainty increased demand for all private assets (not just gold).There is a shift from public assets to private assets.

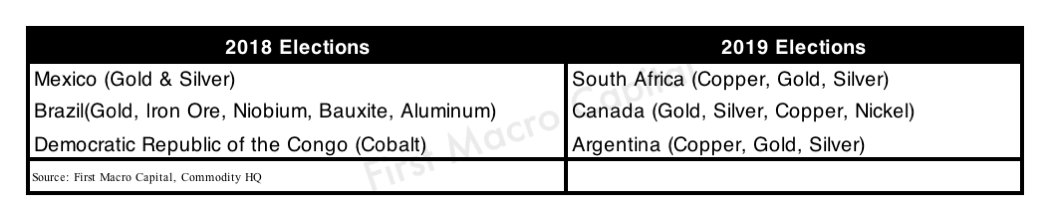

Geopolitical risks are always the hardest for management and investors to get a firm grip on. It requires so many “ifs or if that”, to really pinpoint which will do harm to the mine operations. The geopolitical risks can impact other items that impact funding of the operations like capital controls or the mine operations supplies. A simple solution for investors to mitigate geopolitical risk is to see if the miner has its operations across more than one country, to limit any country-specific risk. There are also several general elections in 2018 and 2019 in commodity-specific countries. Mexico is a significant gold and silver mining producer, and it is having elections in 2018. Brazil also has its general election in 2018, its second largest export commodity in dollar value is gold. Brazil also produces more than 90% of the worlds Niobium, third largest producer of iron ore, and sixth largest producer of aluminum [1]. Heightened political matters will only increase throughout 2018 and continue into 2019, adding to already heightened geopolitical issues.

FINANCIAL RISKS

Economic Slowdown

ETF margin requirements reducing liquidity in mining ETF impacting financing

Financial Taxation Changes by Governments

Bail-in Risk to cash balance

Rising Interest Rates

Cash held Government Bonds – Debt Jubilee

The world continues to work through the debt issues, that have not been resolved since 2008 financial crisis. The risks at banks continue to remain elevated, particularly the European banks. We expect there will be a debt jubilee in some form, with shorter duration government bonds being converted into longer-dated bonds. Companies that are holding shorter-term term government paper as “safe” allocation for their cash, will be caught off guard if their government paper is re-adjusted to a longer duration.Corporate bonds are a better alternative. For Canadian and Australian miners they also face the added bail-in risk of deposits. Federal governments have explicitly stated that they will consider bail-in options, issuing depositors a clear warning. However, “This will never happen to us” management teams always say. Well, they have before, and they will again. If governments are already warning you what they will do in the next crash, and you fail to heed their warning. The list of repeat offenders is quite long.

Even Goldman Sachs CEO, Lloyd Blankfein is warning about the sovereign crisis coming next.

“What is kind of a little bit off. A lot of the bank issues in the United States and around the world have been solved. But migrating the problem to the sovereign balance sheets. So the banks look pretty good,but the Fed has $4 trillion of debton its balance sheet. And it’s even more, we are not in a European audience. In Europe they would really know what they meant because all the European banking system is fixed but Europeans are all also buying up all the debt. The budget deficits haven’t contracted, they’ve widened. The banks buy the debt, then walk over to the European Central bank, finance it. Get new money, so they can buy the next round of debt.

So, you have countries with way bigger deficits, as a percentage of GDP than the U.S., that are borrowing money for ten years, at 3.0% or 2.5%. Really? And the banks look ok.

It is the sovereigns that look risky, like Greece. You wonder is the next crisis going to be a sovereign crisis? And if it is, it will just be a continuation. People will look back and say.. what we really did, we didn’t fix the outcome of the financial crisis. We left that open and as a result, its really been a thirty-year workout.”Lloyd Blankfein [Source: CNBC]

THIS COULD NEVER HAPPEN?

LATE IN THE CYCLE COMMODITY ISSUES

Labor price issues

Government Expropriation Risks

Royalty Regime increases on mining assets

Investors, who say that any of the above risks can never happen, fail to learn the lessons of history to see that, yes, these events have happened and they impacted miners at one point or another. They have impacted many miners over the past 30 years. My experience has taught me, that most investors only really look back far enough to the last crash as to what could happen. Every one of these late in the cycles issues (labor price pressures, government expropriation, royalty regime increases) have always all occurred during the last mining boom. We don’t see these late in the cycle commodity risks evident in gold and silver stocks at this time. Look at cobalt and the skyrocketing price increases. This resulted in governments stepping in and raising cobalt taxes. Investors and management should not be surprised that this occurred, but human beings rarely learn from the past lessons.

For the longer cycle-related events, the time period is much longer than the typical business cycle. By taking into account the business cycle and debt cycles in conjunction with the commodity cycle, you can see where the events will take place. One of my leading long-term bearish indicators in any industry is the regulation card because it has historically highlighted the top in the industry. The mining sector is not there yet.

RISK ALWAYS ON OPERATIONS

OPERATIONAL RISKS

Mine start-up

Cyber Espionage on Mines

Regulatory changes on permitting

The risk to miners will always have the operational risks, particularly when the mine is starting up. Even the best construction engineers and site managers do their best to mitigate the mine risks. The financial and geopolitical poses an added layer of risk that could disrupt the supply chain.

MANAGEMENT TEAMS WILL RESPOND ONLY AFTER

History has shown that management teams from all industries will respond only to a situation or negative event after it has happened. “It couldn’t happen to me” or “That happened 30 years ago”. For the investor, it is better to assume that management will respond only after the event has happened. I am always concerned when the majority of new MBA’s choose a hot and trending industry to build a career in because the top is almost always nearby. We don’t see MBA’s flocking to the gold sector at issue at this time, which continues to make an unloved and unwanted, but excellent for the long-term investor.

FAILURE TO LEARN FROM PAST CYCLES

As this new commodity cycle takes fold, new management teams have entered the mining sector. Old management teams have either sold out, been fired or decided to call it quits after a number of mining cycles. Gone are the lessons from past cycles putting out fires, dealing with governments, capital raising, and operating expertise. This is why it is important to seek those management teams that have succeeded in the past and are still around. It will only increase the odds of success.For the new management teams, they have to earn investor’s trust. If investing in them, watch about putting all your money in from the start, because they will slip. That is certain.

OPPORTUNITIES FOR INVESTORS

Risk events can present opportunities for investors on assets because when investors indiscriminately sell stocks, they sell out the good ones. By thinking through risk events now, it allows investors and management CEO’s to better capitalize on opportunities that can present themselves because your weaker and ill-prepared peers won’t. The risks can also reduce overall gold supply and even with the heightened demand due to geopolitical and financial risks. The gold and silver sectors remain under-owned in relation to other sectors. Technology remains over owned particularly given it is at the beginning of incoming regulation.

“By failing to prepare, you are preparing to fail.” ― Benjamin Franklin

TAKE AWAY FOR THE PORTFOLIO MANAGER & GOLD STOCK ANALYST

Warren Buffett said it best, in managing risk in the investments one makes:

“The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs.”

Better to focus on risk control

Country Diversification- Reduce risks in the portfolio by diversifying across multiple countries.

Financial Strength – Balance sheet counts at the end of the day. How management diversifies its cash will be critical reducing bank deposit risk and debt jubilee exposure.

Margin of Safety – The greater the difference between commodity price and the mine’s All-In-Sustaining-Cost (AISC) reduces the chances of going bust should commodity prices fall.

Investors can seek out less financially leveraged companies, and while ensuring the company is growth focused.

Seeking companies with high management ownership with a significant portion of their wealth in the company.

We have outlined the key geopolitical, financial, and operational risks that investors should be aware of and at least think through in their own portfolios and CEO’s in operating their businesses. 2018 is a period of elevated geopolitical and financial markets related risks to gold stocks. This elevated risk may be the catalysts that wake up the investment community and shift from public assets to private assets, benefiting commodities like gold and silver. While risk is always present when investing, there are risks that one can control, and there are risks that one cannot control.

“If you are not worried, you should be. If you are worried, probably less to be worried about” – Paul Farrugia

Paul Farrugia, BCom. Paul is the President & CEO of First Macro Capital. He helps his readers identify mining stocks to hold for the long-term. He provides a checklist to find winning gold and silver mining producer stocks, including battery metals.

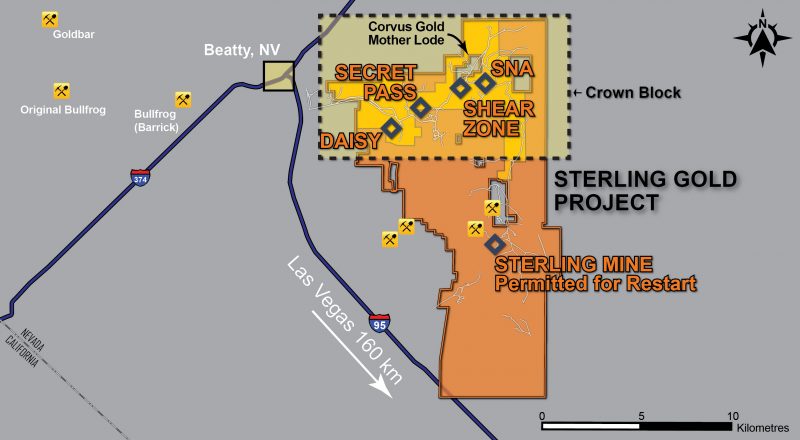

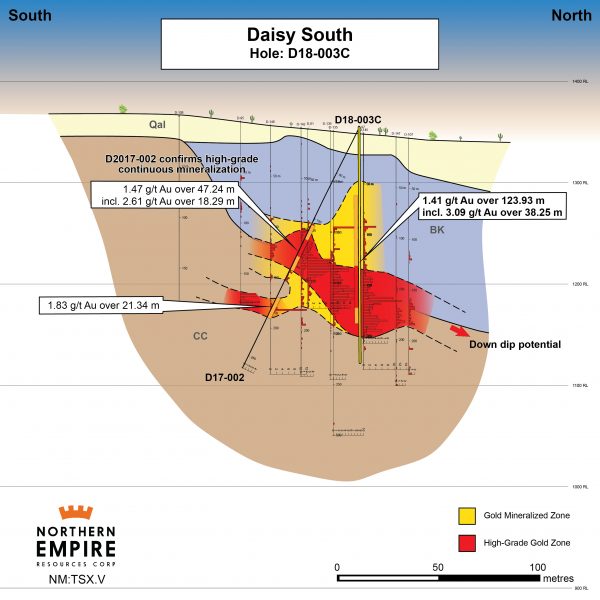

Northern Empire Resources Corp. (TSX-V: NM) released results from its Daisy Deposit as part of its 2018 15,000-metre drill program to expand resources at the Sterling Gold Project in Nevada. These results will go towards an updated resource due in the first half of 2019 and indicate the potential for an open pit, heap leach operation. The Daisy Deposit is located within the Crown Block of deposits in the north of the Company’s property.

Drill hole D18-003C was a vertical core hole that returned an intercept of 123.93 meters of 1.41 grams per tonne (g/t) gold (Au). The intercept included 38.25 meters of 3.09 g/t Au and oxides in the hole extended to a depth of 173 meters.

This is the third drill hole Northern Empire has reported from the Daisy Deposit. Results from last year included 47.24 meters of 1.47 g/t Au in hole D17-001 and 21.34 meters of 1.83 g/t Au in hole D17-002. All historical drilling at Daisy occurred before the introduction of NI 43-101 reporting standards, so confirmation drilling is required to expand the resource. Historical drilling was also all reverse circulation (RC), so core holes are vital for developing a comprehensive geological model.

In comparison to historical holes near D18-003C, yesterday’s result encountered mineralization closer to surface than expected. In concert with nearby mapping and sampling which returned surface grades of up to 15g/t, these results are demonstrative of the potential this system could be larger than previously thought.

Michael G. Allen, President and CEO, commented:

“D18-003C is the first of at least 10 exploratory, resource expansion, and infill holes that we plan to drill into the Daisy Deposit as part of our 15,000-meter program. The exceptional grade of these results is very encouraging. All of the mineralization from 67.88 to 173.22 meters down the hole was oxidized, as was the final 2.87 meters of mineralization. For the high-grade core of the deposit, where we cut 38.25 meters of 3.09 g/t gold, cyanide solubility assays averaged 90% of fire assay, indicating that the Daisy deposit may be amenable to open pit mining with heap leach recovery of gold.”

The broad intervals of relatively shallow, high-grade oxide mineralization present here are key if Daisy is to ever benefit from a low cost and efficient open pit, heap leach operation. The advantage of heap leach mining is that they generally have low all-in sustaining costs and provide rapid payback to the operator. The average grade of heap leach operations in Nevada is approximately 0.7g/t gold, which would make the inferred resource at Daisy of 174,000oz of gold at 2.12g/t triple that.

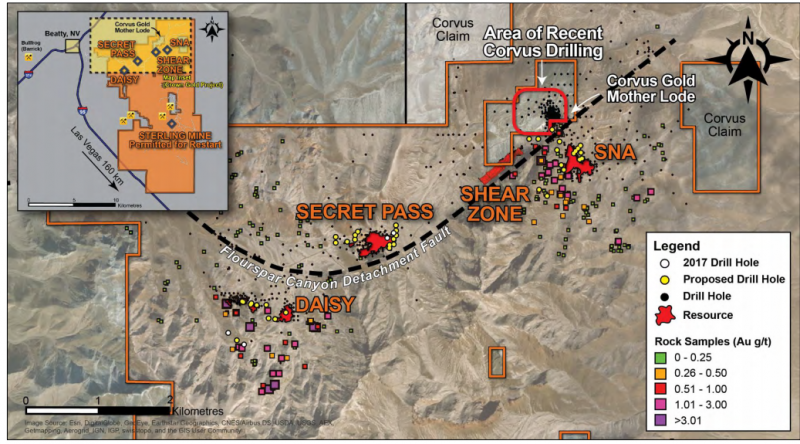

The Daisy Deposit is located in the Bare Mountain district known for its legacy of past production. The trend is along an east-west structure that hosts Barrick’s Bullfrog Mine on the westernmost extension and stretches to the east where Northern Empire’s SNA deposit and Corvus Gold’s (TSX: KOR) Mother Lode deposit. Mother Lode is located completely within Northern Empire’s claim package. Along this trend, more than four million ounces of gold have been extracted or identified in situ.

With several high-grade historical holes and showings, Northern Empire’s overall land package remains underexplored and numerous regional targets demand follow-up. For 2018, Northern Empire management put together a large exploration program with the intention to expand the resource through drilling. The company’s exploration is starting to demonstrate the potential at the Daisy Deposit.

The market has been responding positively to drill results. Since initial results released from the Daisy deposit on October, 04, 2017, shares in the company have moved from 77 cents per share to a year-high of $1.43, and at close of Feb. 23, 2018, $1.30. Upon release of the most recent results from Daisy, the stock rose 12 cents to $1.39 on 231,088 shares.

The company is also responding positively to these results with immediate plans to mobilize an additional drill rig to Daisy. Currently rigs are working on the SNA and Secret Pass deposits which are part of the Crown Block of deposits which includes the Daisy Deposit. In addition, field crews are mapping extensions of the known deposits and new drill targets.

This is just the beginning for Northern Empire in Nevada. Nevada is one of the largest gold producers in the world, renowned for open pit deposits which are amenable to heap leach mining. The early results from Daisy are indicating that the company is on the right track to adding high grade ounces to support the case for another open pit, heap leach mine in Nevada.

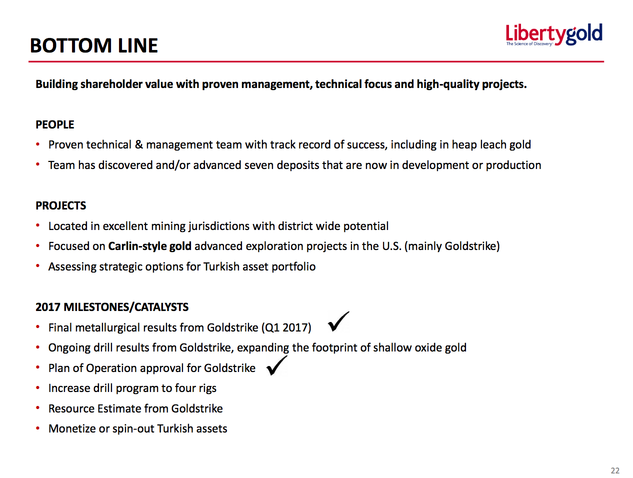

Spin-out of two (U$2.3 billion and U$190 million) gold start-up successes since 2011 has the talent and potential of the originals

Liberty Board at the historic Moosehead Pit at Goldstrike. From left: Rob Pease, Mark O’Dea, Don McInnes, Sean Tetzlaff, Cal Everett

The gold mining industry is massively depleting its reserves, not finding new deposits fast enough, and could be on the cusp of its most profitable turning point ever.

Gold mine supply will peak in 2019 and continue falling through at least 2025, according to BMO Capital Markets and Bloomberg.

Producers like Newmont (NYSE:NEM), Goldcorp (NYSE:GG), Barrick (NYSE:ABX) and Kinross (NYSE:KTO) are looking to the Western United States for their future pipeline. They have all made new investments there and are searching for more. Acquisitions are being focused in stable political and operating environments.

New gold finds have long been richly rewarded.

As an example, investors turned $200 million to $2.3 billion with Fronteer Gold, a Nevada explorer acquired by Newmont Mining (NYSE:NEM) in 2011. In 2016, Endeavour Mining purchased True Gold for U$190 million. Both discoveries were developed from the same group of scientists, led by Mark O’Dea.

Of the last 7 heap leach gold mines put into production in the world, 2 are from the O’Dea Oxygen group. They find deposits, drill them off, de-risk the discoveries and then sell or build them. Two other heap leach deposits from the same group are now being permitted to be built in Turkey by Alamos. That’s 4 projects out of a tiny universe where new discoveries are rare.

The dream team of gold scientists behind Fronteer and True Gold are doing it again.

This time, the industry is starving for new discoveries. A brutal six year bear market has prevented producing companies from investing in exploration. Meanwhile, everyday, gold miners deplete their ores. They are forced to dig deeper, and mine more difficult rock. Plus, project development timelines often take ten or twenty years.

As a result, there are now undeveloped gold resources with bigger valuations than similar projects already built — with construction costs already sunk.

“The older you get in this business, the lower-risk oriented you become in your investments,” commented Liberty Gold (TSX:LGD; OTC:LGDTF) CEO Cal Everett. Originally called Pilot Gold (TSX:PLG), the Fronteer spinout was rebranded Liberty Gold this year to reflect its Western US focus. Kicking rocks at Liberty is the same technical team who developed Fronteer and True Gold.

Liberty Team at Stamp Mill at Goldstrike

To name a couple of those key players:

Dr. Moira Smith is Liberty’s VP of Exploration and helped drive Fronteer’s Long Canyon discovery, which is now critical to Newmont’s growth. Smith has been involved in 7 significant gold mine discoveries in her career that are now in development or in production. “The lady’s absolutely brilliant,” Everett says.

Dr. Mark O’Dea is Liberty’s Chairman. He guided Fronteer to a $2.3 billion sale. More recently he established True Gold, a West African gold developer, that was bought out for U$190 million.

And Liberty now has fresh eyes to build towards a major discovery. It poached Cal Everett, Liberty’s President and CEO, following a recent Corporate acquisition.

Everett is a geologist from New Brunswick, Canada. His father was a military policeman. The younger Everett spent his early career in exploration working with large mining companies. He changed careers to the finance side and excelled as an investment advisor beginning in the early 1990s. Building his own proprietary resource models, and with an international network of geologists, Everett became one of the mining industry’s most influential discovery financiers, working with BMO Capital Markets, PI Financial and later, founding Axeman Resource Capital.

Everett was advising another explorer in 2014 that was competing with Liberty to acquire the past producing Goldstrike project in Utah.

When Liberty outbid, O’Dea offered Everett the top job a year later when the Company was looking for a management and direction change. For Everett, the team and projects were too good to pass up.

“They have an incredible screening process, having been all over the world. It’s no accident they do metallurgy early, avoid political risk, focus on large land positions and other vetting procedures up-front.” Everett says.

On Liberty’s assets, “Three major district-scalable projects, all that are drill confirmed and have given grade in the jurisdiction where everybody wants to be.”

“The secret to this business is when you have a big discovery in a district but still at an early stage, you never stop drilling. You drill until the market wakes up and pays attention.”

THE PROJECTS

The discovery formula is simple. Acquire past producing Carlin – style heap leach oxide gold mines in the Western US that closed 20 years ago in a U$350 gold market, re-interpret thousands of historical drill holes into a new target model and then drill out the discoveries in a higher priced gold market.

The Goldstrike asset in Utah is getting the most drilling this year with, with 3 drills operating almost year round, 50 holes in the lab on any given day and approximately 50 new holes drilled a month. Last week, a discovery was announced 6 km from the known resource area confirming the project is in a gold district by itself. Liberty is finding mineralization nearly everywhere the right rocks are outcropping at Goldstrike. There were 1519 historical holes and now 345 Liberty holes, with an 84% hit success rate over a 22 square kilometre drill confirmed target area. Fresh permits for 150 additional drill sites will help Liberty’s goal to define a million-ounce plus oxide gold resource in the near-term. Preliminary metallurgy has been released with 86% recovery of leachable gold in less than 10 days. This quick and high recovery will help establish Liberty as a low-cost gold producer.

The Kinsley property in Nevada was in production in the mid 1990s but shuttered due to low gold prices years ago. There, Liberty Gold made new high-grade gold discoveries below a past producing surface oxide gold mine and established an initial resource that remains totally open for expansion. The target is high grade at depth, not leachable gold at surface. Kinsley has excellent metallurgy and warrants aggressive follow-up drilling. Liberty is the operator of the project and holds a 79% interest. This year a short four hole drill test successfully found the extension of the high grade deposit to the east, 29.0 metres at 5.30 grams per tonne gold and 3.0 m at 3.68 grams per tonne gold, with a higher grade zone above it with 7.6 m at 6.84 grams per tonne gold and 4.6 m at 12.4 grams per tonne gold. There are many untested targets on the property.

The Black Pine project in Idaho was a significant mid-90s gold producer which Liberty acquired last year for US$800,000 cash, 300,000 shares and a 0.5% royalty. Everett says it’s a Goldstrike look-alike but 12 months behind in terms of advancement. Liberty is currently working on a Plan of Operations to gain approvals for a large exploration program at Black Pine. In the meantime, Liberty’s technical team has vast historical data to devour, including 1,866 historical drill holes. The Black Pine drill target area is drill confirmed over 12 square kilometers. Just gathering this information today for all three projects could cost in excess of Liberty’s current valuation of roughly $65 million (not including $14 million in cash at March 31, 2017).

Liberty Gold also owns an under-appreciated Turkish mineral portfolio. One of the interests, Halilaga, a copper-gold-moly deposit partnered with Teck Resources, was roughly valued at US$66 million in 2015 by Brent Cook, an influential mining analyst, but is a mere footnote in the Liberty Gold story today. Liberty also owns 60% of the TV Tower project, near Halilaga, with six gold and copper discoveries already.

The sale or joint venture of the Turkish assets could raise non-dilutive capital for Liberty to fund aggressive exploration at Goldstrike, Kinsley and Black Pine. Everett does not want to raise equity while Liberty’s stock trades near all time lows. He’s taking responsibility himself now to ramp up marketing. Liberty will have a presence at the major mining trade shows this Fall and is hosting a revolving door of technical presentations.

In the downturn, Liberty shares have fallen from over $3 in 2011 to less than 45 cents at press time. Macquarie mining analyst Mike Gray rates Liberty Gold an Outperform and Top Pick with an initial CAD $0.90 price target. That will prove to be a very conservative target if Liberty enjoys a sample of Fronteer’s success — an inevitability, according to its CEO.

In Everett’s words: “The mining companies know that if you have the district, and you keep drilling, you will find more gold. It’s as simple as that. We are advancing Goldstrike, targeting it to become a minimum 100,000 ounce gold producer. It just takes drilling and scientific back up to try and reach your goal.”

As gold producers struggle to find new mines, Liberty is literally at the ground floor of growth — advancing its three key projects. With many paths to unlock value and the industry’s brightest geologists at the helm, Liberty is one of the few companies positioned to profit from gold’s production growth problem.

Other Western USA gold plays worth mentioning:

Gold Standard Ventures (TSXV:GSV, NYSE:GSV). Moved quickly in the bear market to consolidate a large and strategic land position in Nevada’s Carlin Trend where it is making new discoveries. Gold Standard has attracted strategic investment from OceanaGold and Goldcorp. With a $500 million valuation, it is the most advanced junior in Nevada.

Newcastle Gold (TSX:NCA, OTC:CTMQF). Newcastle boasts an impressive management team led by Detour Gold founder Gerald Panneton and financial backers including mining magnates Richard Warke and Frank Giustra. Developing the multimillion ounce Castle Mountain project in California. Several drill rigs turning to grow and upgrade resources on the production fast track. Valuation today approaching $175 million.

Fiore Gold (TSXV:F, OTC:FIORF). Another Giustra-backed gold vehicle, with Pan, an operating gold mine in Nevada, Gold Rock, a nearby development project, and Golden Eagle, an exploration play in Washington State. Fiore Gold is the pending business combination of Fiore Exploration and GRP Metals, the recapitalized Midway Gold. It is expected to trade in Fall 2017 with a roughly $100 million market capitalization. Investors will be watching to see if Fiore can successfully ramp up the Pan mine and take advantage of other growth opportunities in Nevada.

Barrick Gold (NYSE:ABX). Major producer Barrick is leaning heavily on its Nevada assets to help lower production costs, and recently acquired the Robertson property from Coral Gold Resources in the Cortez District. Barrick is on track to reduce its debt to $5 billion by the end of 2018 and appears to be on track after a sold quarter.

Goldcorp (NYSE:G). It’s no secret Americas-focused gold producer Goldcorp is making bets on small exploration companies to fund its future growth, and hasn’t been shy about the Western United States, where it recently acquired a gold mine in Nevada, and backed a junior there, Gold Standard Ventures. Goldcorp has been one of the worst performing gold stocks of late but refocusing on the Western United States is a step in the right direction.

Newmont Mining (NYSE:NEM). Nevada is the workhorse of Newmont Mining, one of the world’s largest producers. Operations include 11 surface mines, eight underground mines and 13 processing facilities. Annual production from Nevada alone exceeded 1.6 million ounces in 2016, obviously requiring new discoveries or M&A to be sustained.

Kinross Gold (TSX:K, NYSE:KGC). Kinross is on track to meet its annual production guidance of 2.5-2.7 million ounces of gold and costs of $660-$720/ounce and AISC is expected at $925-$1,025/ounce. Production is expected to double at Bald Mountain in Nevada, however the Buckhorn mine in Washington State has recently run out of ore.

Disclaimer: All statements in this report, other than statements of historical fact should be considered forward-looking statements. These statements relate to future events or future performance. Forward-looking statements are often, but not always identified by the use of words such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “targeting”, “intend”, “could”, “might”, “should”, “believe” and similar expressions. Much of this report is comprised of statements of projection. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. Risks and uncertainties respecting mineral exploration companies are generally disclosed in the annual financial or other filing documents of those and similar companies as filed with the relevant securities commissions, and should be reviewed by any reader of this newsletter.

Tommy Humphreys is an online financial newsletter writer. He is focused on researching and marketing resource and other public companies. Nothing in this article should be construed as a solicitation to buy or sell any securities mentioned anywhere in this newsletter. This article is intended for informational and entertainment purposes only!

Be advised, Tommy Humphreys is not a registered broker-dealer or financial advisor. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer.

Never, ever, make an investment based solely on what you read in an online newsletter, including Tommy Humphreys’ online newsletter, especially if the investment involves a small, thinly-traded company that isn’t well known.

Tommy Humphreys’ past performance is not indicative of future results and should not be used as a reason to purchase any stocks mentioned in his newsletters or on this website.

In many cases Tommy Humphreys owns shares in the companies he features, and that is the case with respect to Liberty Gold. For those reasons, please be aware that Tommy Humphreys can be considered extremely biased in regards to the companies he writes about and features in his newsletters, including Liberty Gold. Because Tommy Humphreys owns shares of Liberty Gold, there is an inherent conflict of interest involved that may influence his perspective on Liberty Gold. This is why you should conduct extensive due diligence as well as seek the advice of your financial advisor and a registered broker-dealer before investing in any securities. Tommy Humphreys may purchase more shares of Liberty Gold for the purpose of selling them for his own profit and will buy or sell at any time without notice to anyone, including readers of this newsletter.

Tommy Humphreys shall not be liable for any damages, losses, or costs of any kind or type arising out of or in any way connected with the use of this newsletter. You should independently investigate and fully understand all risks before investing. When investing in speculative stocks, it is possible to lose your entire investment.

Any decision to purchase or sell as a result of the opinions expressed in this report will be the full responsibility of the person authorizing such transaction, and should only be made after such person has consulted a registered financial advisor and conducted thorough due diligence. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that they are accurate or complete. Our views and opinions in this newsletter are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies mentioned in this newsletter (specifically Liberty Gold) will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect.

Tommy Humphreys does not undertake any obligation to publicly update or revise any statements made in this newsletter.

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan