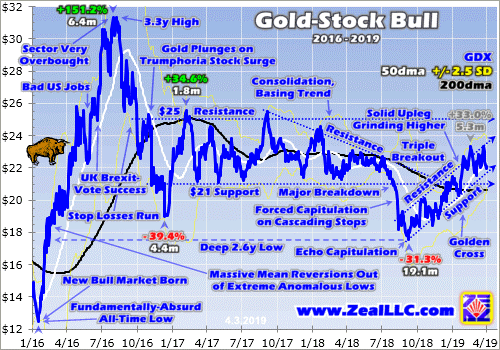

Gold reversed hard last week after blasting higher for a month, leaving traders wondering why and what that portends. The answers are found in gold’s dominant short-term driver, speculators’ collective trading in gold futures. Their positioning has grown excessively bullish, they are essentially all-in betting on more gold upside. That spawned a massive and ominous gold-futures-selling overhang, which needs to be normalized.

Since gold-futures trading is so esoteric, most investors and speculators ignore it. That’s a big mistake, as gold’s near-term price action is overwhelmingly driven by what speculators are doing in gold futures. Their buying and selling heavily impacts gold, and those moves are amplified in both silver and the stocks of precious-metals miners. Trading anything in this realm without watching gold futures is like flying blind.

The reason gold, silver, and their miners’ stocks soared between early August to early September was heavy spec gold-futures buying. That exhausted these traders’ sizable-but-still-limited capital firepower, which is why gold’s powerful upleg stalled out last week. Then gold began falling as specs started to unwind some of their excessively-bullish bets. Gold’s recent action is largely a tale of spec futures trading.

Despite being relatively small compared to the broader gold market, gold futures exert disproportional outsized impacts on gold prices. Unfortunately the gold-futures tail usually wags the gold dog, mostly due to a couple key factors. Gold-futures trading allows extreme leverage far beyond anything seen in normal markets, and the resulting gold-futures price is gold’s global reference one that heavily influences sentiment.

Investors normally buy gold outright, so $1 of capital allocated exerts $1 of price pressure which makes for no leverage at 1.0x. Since 1974, the legal maximum allowed in the US stock markets has been 2.0x. So an investor using maximum margin could buy the world’s leading gold exchange-traded fund, the GLD SPDR Gold Shares, at 2.0x. That would effectively double the price impact of $1 of capital deployed to $2.

But gold futures are in an extreme league of their own for leverage. Each COMEX gold-futures contract controls 100 troy ounces of gold, which is worth $150,000 at $1500 gold. Yet this week the maintenance margin required to hold each contract is only $4,500. That’s all the cash traders are required to have in their accounts, enabling crazy maximum leverage as high as 33.3x! $1 of capital can exert $33 of price pressure.

Gold-futures speculators punch way above their weights in moving gold prices because the price impact of their trading is amplified by up to 33.3x! That juiced gold-futures capital radically outguns investors over short periods of time. Traders can choose to use less leverage, and many do. But even at 10x or 20x, significant spec gold-futures activity drowns out everything else. This has big negative side effects.

At 33.3x, traders can’t afford to be wrong for long or risk catastrophic losses. A mere 3.0% gold move against their bets would obliterate 100% of their capital deployed! That forces these guys into extreme myopia. Their gold outlook isn’t measured in weeks and months, but in hours and days. All they can care about bearing such ridiculous risks is piling on and riding gold’s immediate momentum. Nothing else matters.

The extreme leverage inherent in gold futures also enables gold-price-manipulation attempts. Relatively-small amounts of capital can be blitzed into gold futures at full amplification in very-short timeframes to artificially move gold prices. Often these huge buy and sell orders are rapidly placed then cancelled before they can be executed, which is known as spoofing. This fraud is finally leading to criminal convictions.

Gold prices would be far-less volatile, and vastly more reflective of underlying global supply and demand, without that 30x+ gold-futures capital bullying them around. Gold futures’ impact is multiplied even more since that COMEX gold-futures price is the world reference one. That is what investors and speculators watch around the globe, heavily influencing their own gold sentiment and outlooks which affects their trading.

So what speculators are doing in gold futures changes how investors perceive gold in real-time. They love chasing performance, tending to add gold positions on strength while selling on weakness. Thus heavy gold-futures selling amplified through extreme leverage hammering the gold price lower curtails investment buying and spawns selling. The psychological impact of that reference gold-futures price is sweeping!

There’s no doubt gold would be far better off without hyper-leveraged futures trading, which ought to be banned. These speculators should be bound by the same 2x that has served stock markets well for nearly a half-century. The crazy risks and perverse incentives of running 10x, 20x, 30x+ leverage are really contrary to the core mission of futures markets, which is enabling actual physical users to hedge prices.

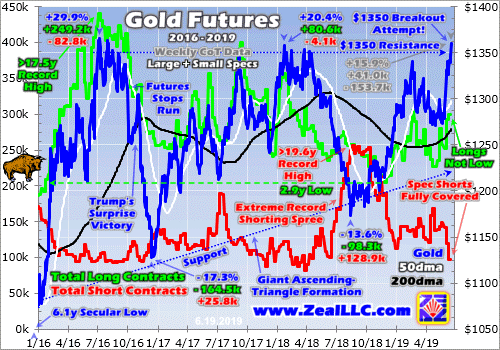

But we must trade the markets we have, not the ones we want. And gold futures’ current wildly-outsized price impact on gold makes watching speculators’ trading activity essential for gaming gold’s near-term price action. Every week the collective spec trading in gold futures is summarized in the CFTC’s famous Commitments of Traders reports. They are current to Tuesdays closes, but not published until late Fridays.

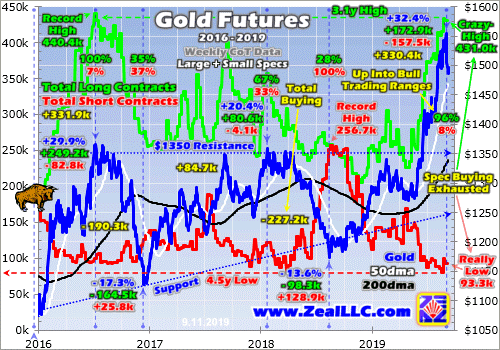

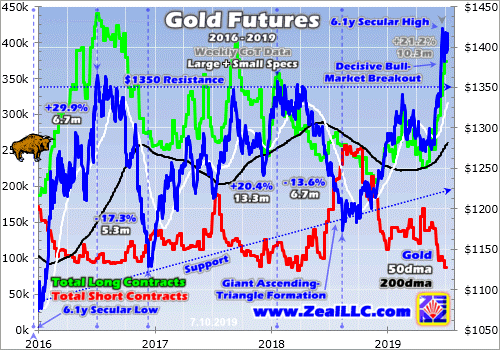

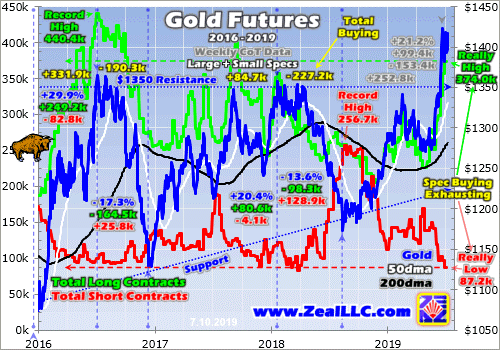

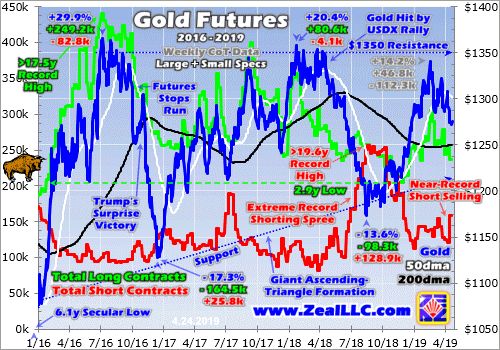

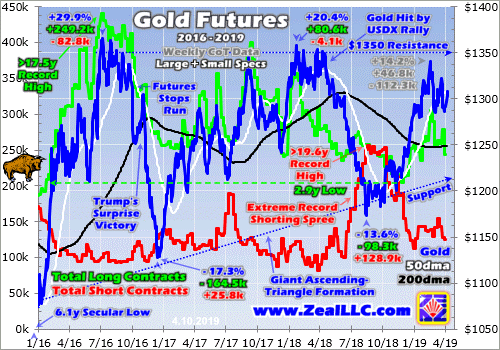

This chart superimposes the current gold bull over speculators’ total long and short positions in gold-futures contracts. The green long line shows their total upside bets each CoT week, while the red short one tracks their downside ones. Gold powers higher when these leveraged traders are buying, and falls when they are selling. Gold, silver, and their miners’ stocks can’t be successfully traded without following this.

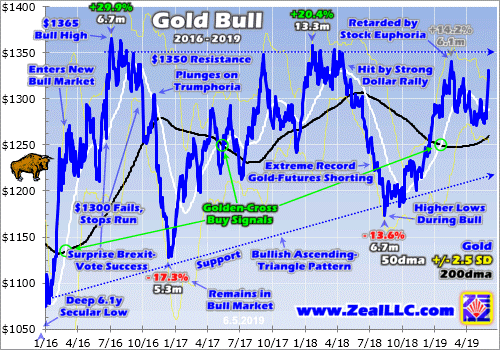

This secular gold bull was born in mid-December 2015, and its maiden upleg was powerful and exciting. Gold soared 29.9% in just 6.7 months, a sea change after languishing in the prior bear market for years! Heavy spec gold-futures buying was the key driver of that mighty move. During that relatively-short span, speculators bought 249.2k gold-futures long contracts while buying to cover another 82.8k short ones.

That added up to a huge 331.9k contracts of total buying in largely the first half of 2016! That is the equivalent of 1032.3 metric tons of gold, or almost 2/3rds of the world’s total mined gold supply that half-year. The other primary driver of gold is investment demand, which was dominated by GLD in that upleg. But GLD’s holdings merely grew 352.6t in that same upleg span, just over a third of gold-futures buying.

The vertical blue lines divide this gold bull into its major uplegs and corrections. Note that uplegs require the green spec-gold-futures-longs line to rise and their red shorts line to fall. Gold can’t consistently rally when these guys aren’t buying. And when they are selling as evidenced by falling longs and rising shorts, gold heads lower in corrections. Speculators’ leveraged gold-futures trading dominates gold’s price action!

Fast-forward to today, where gold has powered 32.4% higher over 12.6 months in its biggest upleg of this bull so far. This move was largely driven by massive spec gold-futures long buying and short covering. This upleg was born last August when these traders were exceedingly bearish on gold. Their longs were relatively low, and their shorts had soared to an all-time-record high of 256.7k contracts. That was super-bullish!

I explained this at the time, writing an essay on specs’ record gold-futures shorts just over a year ago as gold traded under $1200. I concluded then “…gold and silver soon soared on short-covering buying following all past episodes of excessive and record short selling. There’s nothing more bullish for gold and silver than extreme shorts! … Record futures shorts are the best gold and silver buy signals available.”

Because of the extreme risks inherent in gold futures, the group of traders willing to bear these is always fairly small. The capital they collectively command is finite and relatively minor by market standards. So though their price-moving firepower is greatly amplified by radical leverage, their buying and selling soon exhausts itself. Once specs have bought or sold all the gold futures they are able to, gold is going to reverse.

All-time records in spec longs or shorts are easy to identify as extremes not likely to be sustainable for long. Spec longs hit their record high of 440.4k contracts in early July 2016, as this gold bull’s powerful maiden upleg peaked. Spec shorts crested at that 256.7k contracts in late August 2018, which is what birthed today’s strong upleg. But how can we decide what is relatively high or relatively low outside of records?

We want to aggressively buy gold and gold stocks when speculators’ gold-futures positioning grows too bearish, when their longs are low and shorts high. And we need to prepare to sell the resulting winning trades when their collective bets get excessively bullish, evidenced by high longs and low shorts. I’ve tried various approaches to analyzing this over the years, and finally developed a simple one that works.

Every week I game the near-term outlook in gold, silver, and their miners’ stocks by looking at how spec gold-futures longs and shorts are trading relative to their own bull-market-to-date trading ranges. These are expressed as percentages. When gold bottomed in mid-August 2018, total spec longs were 28% up into that range while total spec shorts were at 100% of their own. There was way more room to buy than sell.

The most-bullish-possible gold-futures positioning is specs being all-out, represented by 0% longs and 100% shorts. That means about all they can do is buy, both by adding new longs and buying to cover and close existing shorts. The lower spec longs and higher spec shorts, the more bullish gold’s near-term outlook and the bigger the coming gains as these traders buy to normalize their excessively-bearish positions.

Indeed gold’s latest upleg was driven by massive spec long buying and short covering over the past year or so. During that entire 12.6-month span ending last week where gold climbed 32.4%, total spec longs soared 172.9k contracts while total spec shorts collapsed 157.5k. That adds up to 330.4k contracts of gold-futures buying, the equivalent of 1027.7t. That’s nearly identical to the 331.9k bought in this bull’s first upleg!

Today’s upleg’s latest interim gold high of $1554 came last Wednesday September 4th. The latest weekly CoT report available before this essay was published was current to the previous day’s close. At that point before gold reversed hard and started falling, total spec longs were running 96.3% up into their gold-bull-market trading range since mid-December 2015. Total spec shorts were just 7.6% up into their own range.

The most-bearish-possible gold-futures positioning is specs being all-in, which happens at 100% longs and 0% shorts. Their capital firepower is exhausted, they are tapped out and just can’t materially add to their excessively-bullish bets any more. At that point all they can do is sell, beginning to normalize their lopsided positioning. And gold-futures selling quickly cascades due to the extreme leverage in these trades.

Last Tuesday as gold exuberance mounted, total spec longs ran 431.0k contracts. That was the third-highest on record, after the prior CoT week’s 433.0k and early July 2016’s 440.4k! There wasn’t much room for material new buying with longs so excessive. No matter how excited traders get after a strong gold run, the ranks of gold-futures speculators won’t swell much since the risks they bear are so extreme.

Gold not only faced virtually no more spec long buying last week, but little potential short-covering buying. The total spec shorts of 93.3k contracts weren’t much above their lowest levels seen in this gold bull just a couple CoT weeks earlier. Spec shorts never go to zero, there’s always a floor no matter how big and fast gold rallies. In this bull that has run around 90k or so. This upleg’s huge short covering was out of steam.

When gold-futures speculators’ potential buying exhausts itself, gold has to stall and top out. There’s just no more high-octane leveraged fuel to keep driving it higher. And at that point with specs essentially all-in longs and all-out shorts, it’s only a matter of time until some catalyst sparks selling. Early last Thursday it happened to be news the US-China trade talks are back on and better-than-expected US private-sector jobs.

Neither headline would’ve moved gold much had spec gold-futures positioning not been so extreme. But the only thing these traders could do was sell, and that soon snowballed. Again at 33.3x leverage, gold only has to move 3.0% against speculators’ bets to wipe out 100% of their capital risked. So they have to sell fast or risk ruin. And the more they sell the quicker gold falls, triggering still more selling by other traders.

Now that this gold-futures selling is underway, the extreme gold-futures-selling overhang that led into it has to be largely wiped out. That is likely to take at least a couple months coming from such near-record extremes. That portends a major correction in gold as specs dump their excessive longs and ramp up their barely-existent shorts. This gold bull’s own precedent is certainly ugly, as we saw after its maiden upleg.

In early July 2016 after gold soared 29.9% in 6.7 months, total spec longs and shorts were running 100% and 7% up into their bull trading ranges. By the time the necessary gold-futures selling to rebalance those positions ran its course, gold plunged 17.3% over the next 5.3 months! Just last week specs’ total longs and shorts stretched a similar 96% and 8% up into their bull-market trading ranges, which is menacing.

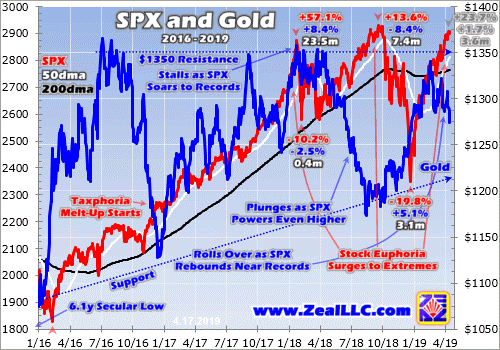

While gold is in for a major correction, thankfully it isn’t likely to challenge that H2’16 extreme. That was really exacerbated by an exceptional one-off anomaly. Trump’s surprise election win goosed the stock markets on hopes for big tax cuts soon, leading to extraordinary gold selling. Before Trump won, gold had decisively bottomed down just 8.3% before rallying again for weeks. That’s about what’s probable this time.

Speculators’ gold-futures positioning is so important to follow that I always discuss it in our weekly and monthly newsletters for subscribers. Since they graciously fund our business, they get this critical data and analysis well before I consider writing essays on it. I warned about all this in our new September newsletter published early on August 31st. That was before gold cracked on the inevitable gold-futures selling.

My conclusion then was “Gold is overextended, due for a healthy bull-market correction over the near-term. Its technicals are way too overbought, and its sentiment way too greedy. Too many buyers have flooded in too quickly, exhausting gold’s near-term upside potential. My best guess is a 6%-to-12% gold selloff, which the major gold stocks will leverage like usual by 2x to 3x.” That works out to 12% to 36%.

Gold-futures-selling overhangs can’t be taken lightly, as extreme spec positioning never lasts for long. The resulting gold corrections are very healthy for bulls, restoring balance to sentiment and technicals. But there’s no need to get trapped in them and see big prior-upleg gains in gold stocks just evaporate. When gold stocks are very overbought like last week, stop losses should be tightened to protect gains.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In the first half of 2019 well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. We’ve recently realized big gains including 109.7%, 105.8%, and 103.0%!

To profitably trade great gold stocks, you need to stay informed about speculators’ positioning in gold futures which drives gold. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off sale! Get onboard now so you can mirror our coming trades for gold’s next upleg after this correction.

The bottom line is gold stalled and reversed hard because speculators’ leveraged gold-futures bets had grown too excessively bullish. Their longs were way up just under all-time-record highs, and their shorts were way down just over bull-market lows. These gold-dominating traders were effectively all-in longs and all-out shorts, leaving them little room to keep buying but vast room to sell on the right catalyst hitting.

Such gold-futures-selling overhangs resulting from specs waxing too bullish need to be normalized before gold bulls can resume. That only happens through heavy selling, both jettisoning exaggerated longs and ramping up meager shorts. This forces gold into major corrections, which are both necessary and healthy between major bull-market uplegs. They lead to the best buying opportunities seen within ongoing bulls.

Adam Hamilton, CPA

September 16, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

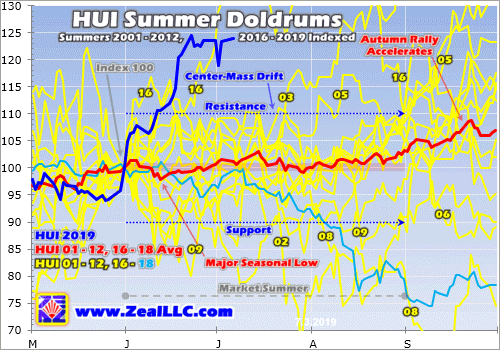

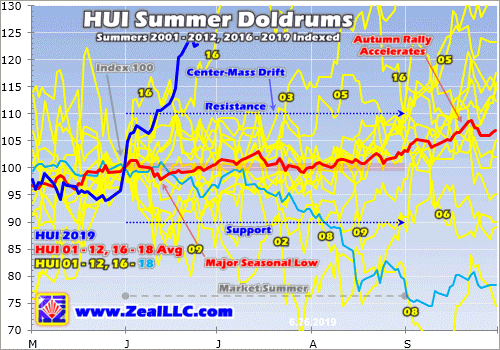

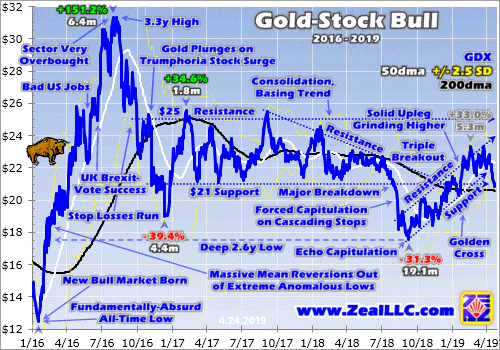

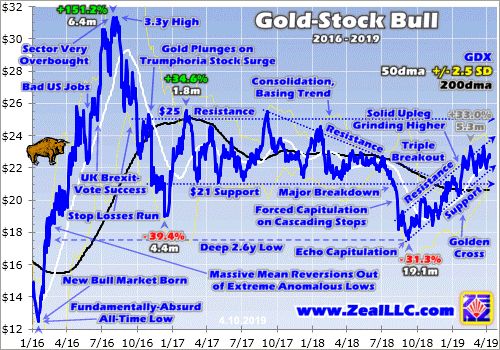

The gold miners’ stocks have grown very overbought after soaring dramatically higher in recent months. Blasting really far really fast has left this sector really stretched technically and sentimentally. Excessive gains and greed always soon lead to major corrective selloffs, which are necessary to restore balance. All bull markets, even the most powerful, flow and ebb. Big uplegs are inevitably followed by corrections.

With gold and gold stocks plunging hard Thursday morning, the timing of this research thread is certainly lucky. My weekly-web-essay workflow is well-defined, this happens to be the 877th I’ve written. I have to decide on each week’s topic by early Wednesdays, to do the research and build necessary spreadsheets and charts that day.

Even before this latest bout of selling erupted, the serious downside risks facing overbought gold stocks were readily apparent. According to virtually every technical indicator out there, this sector was looking ever-more extreme in recent weeks. The longer and farther gold stocks surged, the greater the odds for a selloff. I warned about this Saturday morning in the conclusion to our latest monthly newsletter for subscribers.

Before the selling hit I wrote, “Gold is overextended, due for a healthy bull-market correction over the near-term. Its technicals are way too overbought, and its sentiment way too greedy. Too many buyers have flooded in too quickly, exhausting gold’s near-term upside potential. My best guess is a 6%-to-12% gold selloff, which the major gold stocks will leverage like usual by 2x to 3x.” That works out to 12% to 36%!

Stock prices can’t soar higher without material interruptions indefinitely. Even strong uplegs eventually burn themselves out, attracting in all interested buyers over the near-term. They rush to buy to ride the upside momentum, basking in the warm greed. But once their capital firepower is exhausted, price gains stall and peak. That leaves nothing but sellers, and their resulting downside momentum feeds on itself.

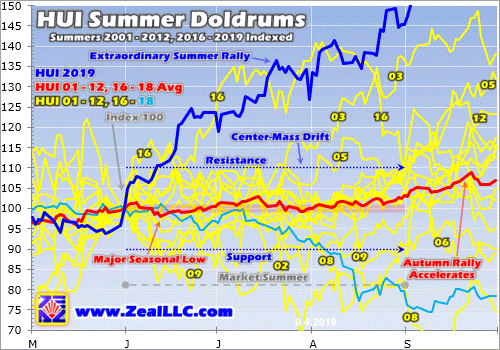

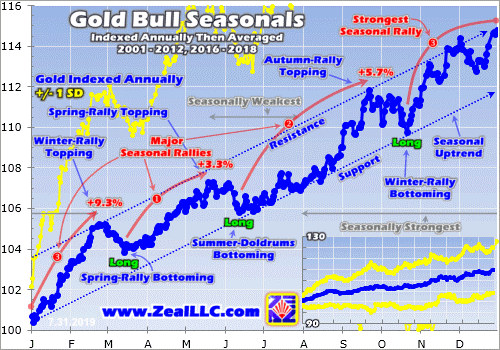

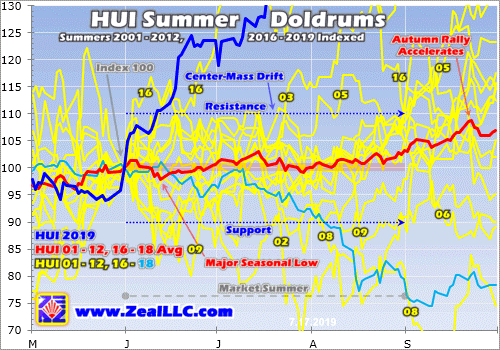

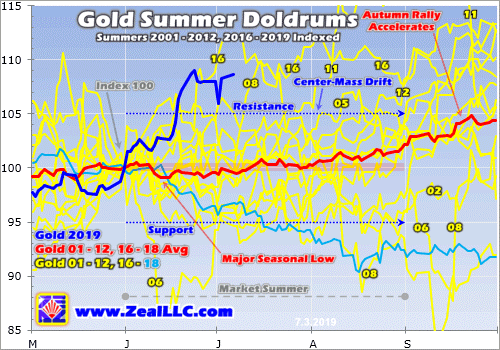

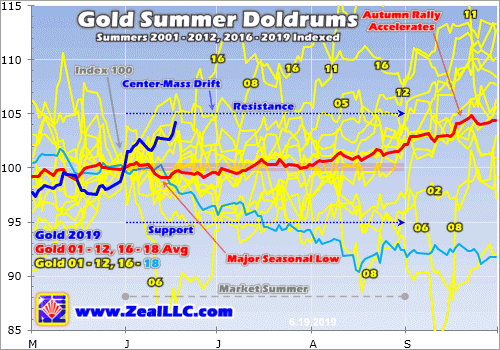

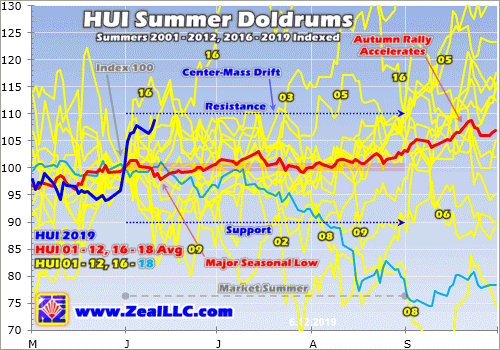

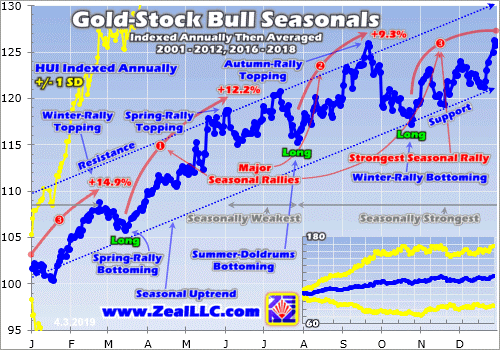

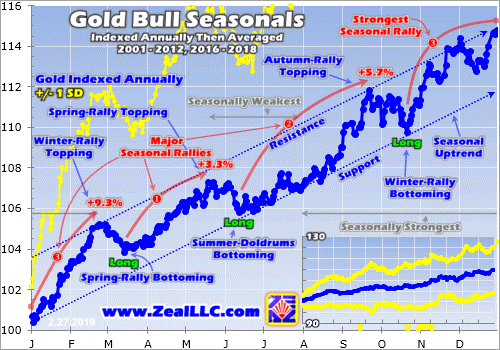

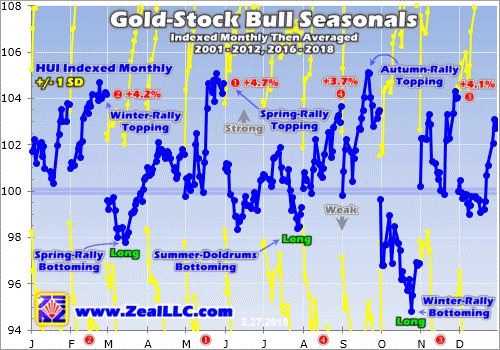

The massive gains gold miners’ stocks enjoyed in recent months have truly been extraordinary, stoking widespread greed. This first chart is a seasonal one, rendering this sector’s price action in like indexed terms during every summer in modern bull-market years. Normally gold and gold stocks face seasonal drifts to slumps in market summers, the dreaded summer doldrums. This summer’s monster rally defied that.

Traders use two major benchmarks to measure gold-stock prices, the popular GDX VanEck Vectors Gold Miners ETF and the venerable HUI NYSE Arca Gold BUGS Index. Both of these track the major gold miners’ stocks. While GDX has gradually usurped the HUI in prominence, it remains too young for long-term studies. GDX was born in May 2006, roughly halfway through the last secular gold and gold-stock bull.

So the HUI has to be used to distill all gold-stock summer action from 2001 to 2012 and 2016 to 2019, the modern gold-bull-market years excluding intervening bear years. Every summer is individually indexed to its final May close, which is set at 100. Then its June, July, and August price action is recast from that common baseline. All these individual-summer indexes averaged together show the summer-doldrums drift.

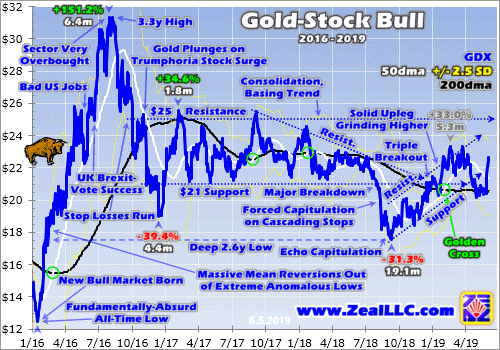

The center-mass trend of this spilled-spaghetti chart is a sideways grind, within 10% either direction of the final May close. This summer’s breakout gold-stock rally is rendered in dark blue, and it proved an utter monster. By the end of August, the HUI had skyrocketed 45.3% higher during the three calendar months of the market summer! The seasonal average in modern gold-bull-market years before 2019 was a 3.2% gain.

The gold miners just soared to their best summer performance in recent decades! The only comparable year was 2016, making its example important for gaming today’s overboughtness. The gold stocks spent the last few months racing higher neck-and-neck with the summer of 2016, trading the lead back and forth multiple times. It wasn’t until the last couple weeks that 2019 injected the nitrous and screamed past.

By the end of July 2016, the HUI had soared 36.3% summer-to-date compared to 2019’s considerably-smaller 26.9% gains in that same span. But by the end of August 2016, those had collapsed back down to +10.1% over that entire summer. This summer’s strong finish after a powerful multi-month rally is truly in a league of its own. Only 2003 rivaled it with 36.9% summer gains, but those started well later mid-summer.

Overboughtness is a relative thing, it can’t be defined absolutely since prevailing price levels gradually change over time. But the biggest summer gold-stock rally in modern history certainly raises concerns of running too far too fast. Gold stocks soaring by about half in several months is a huge move even by their wild standards! This mighty gold-stock surge looks even more extreme considered in longer-term context.

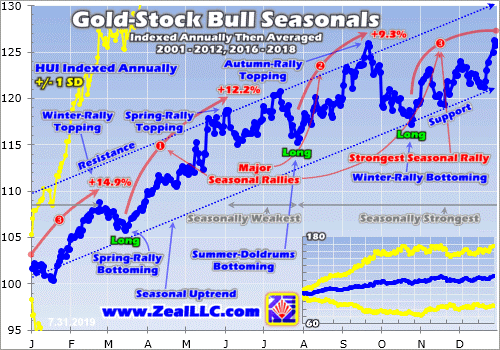

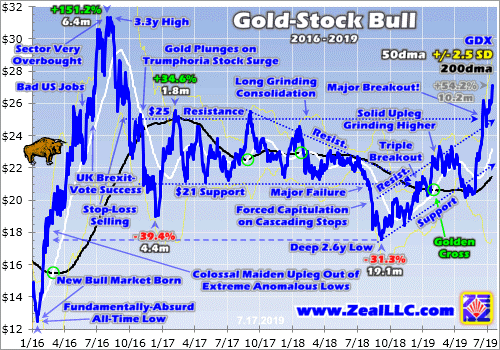

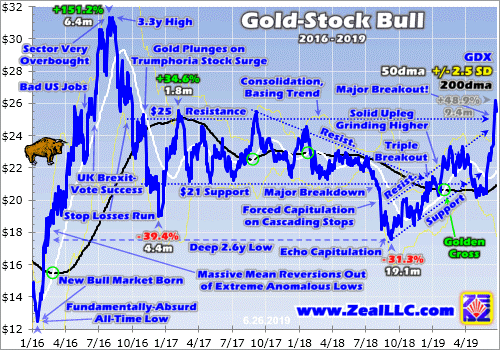

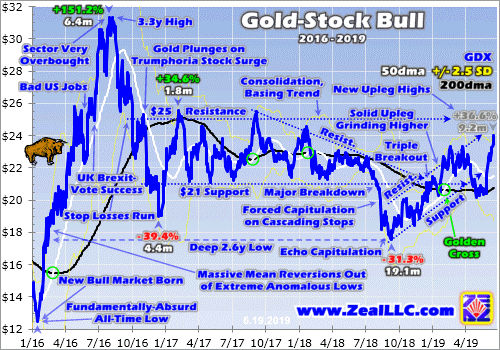

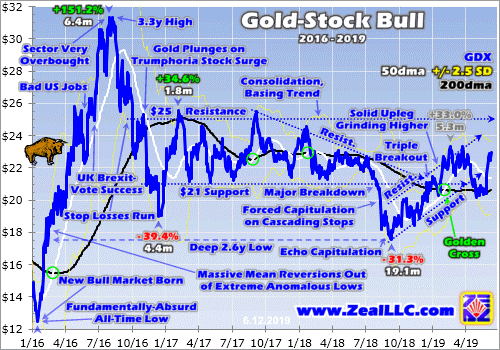

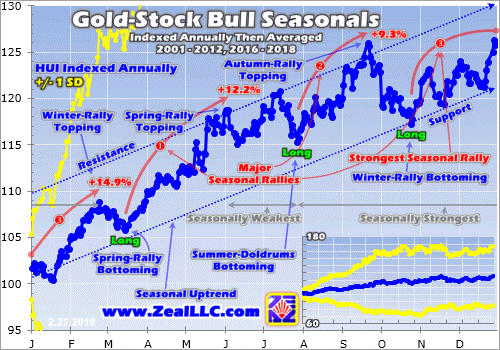

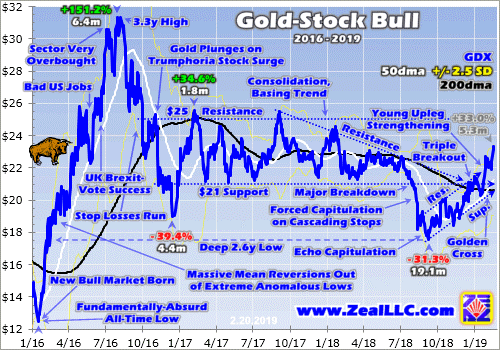

This next chart encompasses the current gold-stock bull since early 2016, which was driven by gold’s own parallel secular bull. Professional institutional investors have often gamed this bull with that leading and dominant GDX ETF, so it is used here rather than the older HUI. While the gold miners’ stocks achieved much technically this summer, there’s no doubt they soared to super-overextended levels which is ominous.

As of this past Wednesday’s close, the data cutoff for this essay, GDX had powered up 76.2% in 11.8 months. Interestingly that’s right in line with the last secular gold-stock bull’s average upleg gain. From November 2000 to September 2011, the HUI skyrocketed 1664.4% higher over 10.8 years! Those gains accrued in 12 separate uplegs. Excluding an anomalous post-stock-panic-recovery one, they averaged 80.7% gains.

It’s hard to believe now, but back in early May GDX languished at $20.17 and you could hardly give away gold stocks! Traders didn’t want anything to do with them when they were universally despised and easy to buy incredibly low. I was pounding the table on buying the dirt-cheap gold stocks last spring, when this sector still had massive near-term upside potential. Near-record gold-futures shorting portended a major upleg.

Near the end of April in an essay on gold futures, I explained why. “Speculators’ big bearish shift in gold-futures positioning will have to be normalized, resulting in big buying that will push gold higher. That upside momentum could really grow… The biggest gains as gold mean reverts back higher will come in the stocks of its miners. They’ve proven resilient as gold swooned, and are poised to surge again.”

The out-of-favor gold stocks ground along near demoralizing lows for most of May, giving traders plenty of opportunities to buy relatively low before they ran again. We took advantage of that then to aggressively load up on fundamentally-superior gold miners and silver miners in our subscription newsletters. Trump of all things proved the catalyst to awaken gold and thus its miners’ stocks. That happened at the end of May.

Gold and gold stocks started surging after Trump threatened Mexico with tariffs, in an attempt to force it to stem the flood of illegal immigration into the U.S. Tying trade tariffs to other issues stunned traders, which unleashed safe-haven buying in gold. That helped the gold stocks rally strongly though much of June, with bullish momentum. But they really didn’t start soaring until late that month on a momentous gold milestone.

While gold technically remained in a bull market, it hadn’t made a new bull-market high since right after this bull’s maiden upleg way back in early July 2016. After 2.9 years with zero new highs, traders had long since lost interest in this sector. But in late June after the Fed shifted its future-rate-hike outlook from hiking to cutting, gold finally staged a decisive bull-market breakout. That changed everything psychologically.

The best gold levels seen in 5.8 years lit a fire under gold stocks, which kept rallying sharply in July when they are usually forgotten. They were getting overbought by mid-July, so momentum flagged heading into month-end. They were starting to roll over into what would’ve likely been a pullback until Trump surprised again, hiking tariffs on China as August dawned. That ignited gold stocks’ latest surge earlier last month.

That too soon started to fade since the gold stocks were so overbought. Smart traders who’ve dedicated many years to studying and understanding market cycles realized a corrective selloff was increasingly likely after such a big and fast surge. But yet again in late August Trump surprised with still another hike on Chinese tariffs! That sparked and fueled another gold and gold-stock rally that persisted into this week.

The result of these three catalyzing Trump-tariff-hike announcements in recent months is the near-vertical gold-stock surge seen in these charts. GDX blasted to its best levels in 3.1 years. That’s not necessarily high absolutely, but it is certainly high relatively. When prices surge really far really fast on major buying as sentiment turns greedy, overboughtness always results. Such blistering rallies inevitably lead to selloffs.

While traders chasing the herd to buy in high later in uplegs practically panic when major selloffs hit, they are actually very healthy. They are essential and necessary to rebalance sentiment, eradicating the out-of-control greed after excessive gains. They force prices lower until technicals grow oversold as popular psychology waxes bearish. That leaves gold stocks relatively low again, a great opportunity to buy back in.

These inexorable upleg-correction cycles are what enable shrewd traders to multiply their wealth in bull markets. The goal is to buy relatively low after the corrections, then sell relatively high after the uplegs. This can only be achieved by doing what’s unpopular, fighting the crowd to do the opposite. When other traders are scared and selling is when to buy low, then when they are excited and buying is when to sell high.

The challenge is defining relatively low and relatively high, seeing oversold and overbought conditions in real-time when they can be capitalized upon. While there are many technical indicators, one of the best is among the simplest. It just looks at prevailing price levels relative to their 200-day moving averages. I call this Relatively Trading, and started developing this system over 15 years ago. It has proven really profitable.

There’s no gold-stock level that can be considered high absolutely across different years and toppings. In early August 2016, GDX peaked at $31.32. From there it would plummet 39.4% over the next 4.4 months in a colossal selloff! That was considered a correction instead of a bear market since gold-stock bull-and-bear cycles are defined by gold’s own. But GDX peaked at $66.63 in September 2011 with gold’s last bull.

Is GDX high at $31, which it again challenged this week, or does it have to get to $67 to be high? Gold stocks’ absolute price levels are irrelevant, as what is exceptionally high or low gradually changes over time. So some kind of reference point is needed to identify overboughtness and oversoldness right as they happen, but that too needs to slowly evolve. I’ve found gold stocks’ 200dma acts as an ideal metric for this.

200dmas aren’t static, they gradually adjust to different prevailing gold-stock price levels. At the same time, they have enough inertia to lag extreme short-term price moves. Calendar months average about 21 trading days, so a 200dma digests the past 9.5 months of price action. Exceptional gold-stock moves stretch current prices far away from their trailing 200dmas. That distance is easily quantifiable to trade upon.

Relativity Trading simply divides daily price closes by their 200dmas and charts the resulting multiples over time. With a sufficiently-long span, especially in trending markets, horizontal trading ranges of these multiples form. After much study and trial and error, I settled with the last 5 calendar years to define Relativity trading bands. Seeing where 200dma multiples trade comparatively offers good buy and sell signals.

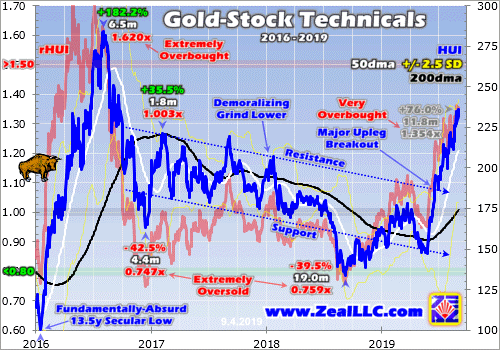

Again GDX is much newer than the HUI with a far-shorter price history. And all my years of work applying Relativity to trading gold stocks has used the HUI as their benchmark index. So I’m going to shift back to the HUI for this final chart on gold-stock overboughtness. The Relative HUI indicator, or rHUI, currently has a trading range of 0.80x to 1.50x. This is rendered in this chart with the green and red shaded zones.

Visually a Relativity chart effectively flattens a 200dma, straightening it to 1.00x. Then a price’s multiple to that 200dma oscillates around it over time, in perfectly-comparable percentage terms regardless of the prevailing price levels. No matter where gold stocks are trading, when the rHUI hits 0.80x or 1.50x the actual HUI is trading at 80% or 150% of its current 200-day moving average. Here is this gold-stock bull’s chart.

Thanks to the gold stocks’ blistering rally this summer, the rHUI shot up as high as 1.362x last week. On Wednesday as this upleg’s latest high was hit, the rHUI still ran 1.354x. In other words, the major gold stocks as a sector are stretched 35% to 36% above their 200dma! That is very overbought, and doesn’t happen very often. Gold-stock uplegs usually only deviate from their 200dmas so greatly when they go terminal.

Bull-market uplegs usually start gradually, with not many traders interested in buying relatively low after major corrections. But as uplegs gather steam and gains mount, traders get excited about the upside momentum and want to buy in. The higher prices climb, the more greed grows and the greater the allure of chasing the herd. Thus upleg gains tend to be back-loaded, the majority accruing quickly as uplegs mature.

So really-overbought readings generally only happen late in uplegs. Actual gold-stock topping levels in rHUI terms still vary greatly though. Back in this bull market’s mighty maiden upleg peaking in summer 2016, the rHUI soared as high as 1.70x before drifting back to 1.62x when gold stocks actually crested in early August. But anytime the major gold stocks stretch 25%+ above their 200dmas, traders need to be wary.

Since there’s so much variability in upleg toppings, I generally haven’t sold trading positions outright. My strategy is usually to ratchet up trailing stop losses as prices get more overbought. That effectively locks in more of our upleg gains, while preserving upside potential if the upleg persists even longer. Although stop losses have their own challenges as they can be whipsawed into tripping early, they help manage risk.

I also consider gold-stock overboughtness in rHUI-multiple terms against the backdrop of how speculators are currently positioned in gold futures. Gold stocks are effectively leveraged plays on gold, and the gold-futures traders dominate gold’s short-term price action. I last explained this in depth in a mid-July essay. For our purposes today, realize gold’s own selloffs driving gold stocks’ are almost always governed by futures.

In the latest weekly data, speculators held their second-highest levels of gold-futures long contracts on record! That left their total longs running 97% up into their gold-bull-market trading range since mid-December 2015, which was topped by July 2016’s all-time-record high. When specs are effectively all-in gold-futures longs, all they can do is sell. Excessive long positions precede major corrections in gold.

After that only time spec longs were slightly higher in mid-2016, gold plunged 17.3% over the next 5.3 months which hammered the gold stocks 39.4% lower per GDX! And on the short side of gold futures, in the latest weekly read specs’ total contracts were running just 11% up into their own gold-bull-market trading range. That means they also have little room to buy gold futures to cover shorts, but lots of room to sell.

The most-bearish-possible near-term outlook for gold happens when total spec longs and shorts swing to 100% and 0% up into their bull-market trading ranges. The latest 97% and 11% as of last Tuesday’s close is getting pretty darned close! Since gold stocks will tank with gold regardless of how overbought they get, their downside risks are high. A major correction is far more likely than additional material rallying.

Rather amusingly, warning of overboughtness and impending selloffs after powerful uplegs always gets people riled up. After these 877 weekly essays, I know my e-mail inbox will be full of people telling me what a fool I am Monday morning. How could gold stocks not soar to the moon? This time is different because… The irony is traders should welcome corrective selloffs as they create new buy-low opportunities.

I opened with the first third of my conclusion from our brand-new monthly newsletter, and here’s the rest. “That will rebalance sentiment, paving the way for far-bigger future gains. There’s no sense redeploying capital high before that inevitable selloff arrives. Don’t let that short-term bearishness cloud the big picture. Gold’s powerful surge higher in the last several months changes everything going forward.”

“It confirms gold is indeed in a secular bull market! That was ignored and disputed for years since gold failed to break out to new bull highs. Gold’s decisive breakout and rallying since ballooned interest in it. So future gold and gold-stock uplegs are going to attract way more capital from way more traders around the world, growing them to much-larger sizes.” This latest upleg was fun, but bigger and better are coming.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In the first half of 2019 well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. We’ve recently realized big gains including 109.7%, 105.8%, and 103.0%!

To profitably trade high-potential gold stocks, you need to stay informed about the broader market cycles that drive gold. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off sale! Get onboard now so you can mirror our coming trades for the next upleg as they are deployed in real-time.

The bottom line is gold stocks are very overbought. The powerful counter-seasonal rally in recent months catapulted gold-stock benchmarks far beyond their 200-day moving averages. Such stretched technicals coupled with very-bullish popular sentiment are a warning this recent upleg is maturing. It is likely to roll over into a healthy correction soon to restore balance, driven by gold-futures selling from spec extremes.

All bull markets flow and ebb, with big uplegs followed by major corrections. Fighting the latter is utterly pointless. Ride the bull-market waves rather than drowning in them. Buy relatively low near the troughs, then sell relatively high near the crests. That means buying when everyone else is scared, before selling when everyone else is greedy. After enjoying a great and very-profitable upleg, we can cash out for the next one.

Adam Hamilton, CPA

September 9, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

The battered silver miners’ stocks surged in recent months, staging a strong rebound rally. That overdue turnaround was fueled by silver mean reverting higher on improving sentiment after gold’s decisive bull-market breakout. But silver miners still had a challenging Q2, as most of silver’s gains came after last quarter ended. They continued diversifying into gold to help weather silver’s endlessly-languishing low prices.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

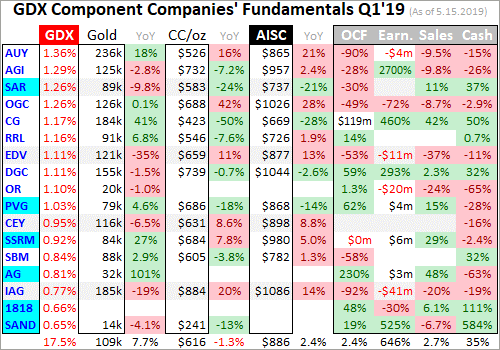

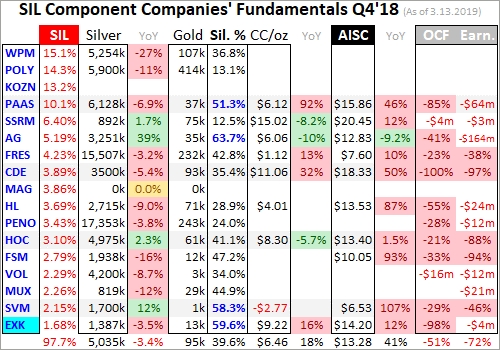

The definitive list of major silver-mining stocks to analyze comes from the world’s most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. Launched way back in April 2010, it has maintained a big first-mover advantage. SIL’s net assets ran $476m in mid-August near the end of Q2’s earnings season, 5.3x greater than its next-biggest competitor’s. SIL is the leading silver-stock benchmark.

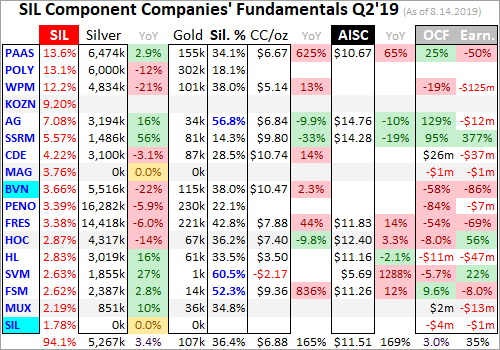

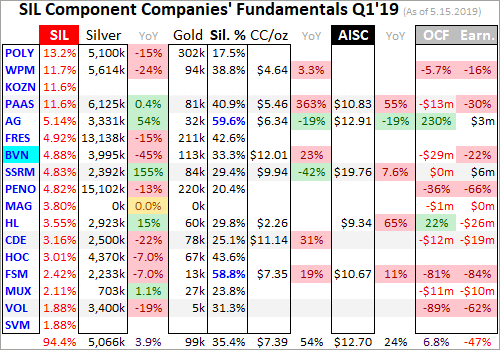

In mid-August SIL included 23 component stocks, which are weighted somewhat proportionally to their market capitalizations. This list contains the world’s largest silver miners, including the biggest primary ones. Every quarter I dive into the latest operating and financial results from SIL’s top 17 companies. That’s simply an arbitrary number that fits neatly into the table below, but still a commanding sample.

As of mid-August these major silver miners accounted for fully 94.1% of SIL’s total weighting. In Q2’19 they collectively mined 73.7m ounces of silver. The latest comprehensive data available for global silver supply and demand came from the Silver Institute in April 2019. That covered 2018, when world silver mine production totaled 855.7m ounces. That equates to a run rate around 213.9m ounces per quarter.

Assuming that mining pace persisted in Q2’19, SIL’s top 17 silver miners were responsible for over 34% of world production. That’s fairly high considering just 26% of 2018’s global silver output was produced at primary silver mines! 38% came from lead/zinc mines, 23% from copper, and 12% from gold. Nearly 3/4ths of all silver produced worldwide is just a byproduct. Primary silver mines and miners are quite rare.

Scarce silver-heavy deposits are required to support primary silver mines, where over half their revenue comes from silver. They are increasingly difficult to discover and ever-more expensive to develop. And silver’s challenging economics of recent years argue against miners even pursuing it. So even traditional major silver miners have shifted their investment focus into actively diversifying into far-more-profitable gold.

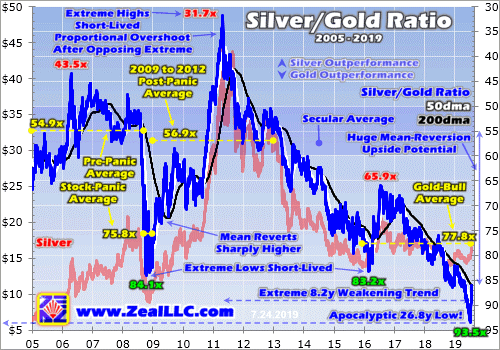

Silver price levels are best measured relative to prevailing gold prices, which overwhelmingly drive silver price action. In early July the Silver/Gold Ratio continued collapsing to its worst levels witnessed in 26.8 years, since October 1992! Those secular extremes of the worst silver price levels in over a quarter century sure added to the misery racking this once-proud sector. That compounded miners’ challenges in Q2.

The largest silver miners dominating SIL’s ranks are scattered around the world. 11 of the top 17 mainly trade in U.S. stock markets, 3 in the United Kingdom, and 1 each in South Korea, Mexico, and Canada. SIL’s geopolitical diversity is good for investors, but makes it difficult to analyze and compare the biggest silver miners’ results. Financial-reporting requirements vary considerably from country to country.

In the U.K., companies report in half-year increments instead of quarterly. Some silver miners still publish quarterly updates, but their data is limited. In cases where half-year data is all that was made available, I split it in half for a Q2 approximation. Canada has quarterly reporting, but the deadlines are looser than in the States. Some Canadian miners really drag their feet, publishing their quarterlies close to legal limits.

The big silver companies in South Korea and Mexico present other problems. Their reporting is naturally done in their own languages, which I can’t decipher. Some release limited information in English, but even those translations can be difficult to interpret due to differing accounting standards and focuses. It is definitely challenging bringing all the quarterly data together for these diverse SIL-top-17 silver miners.

But analyzing them in the aggregate is essential to understand how they are faring. So each quarter I wade through all available operational and financial reports and dump the data into a big spreadsheet for analysis. Some highlights make it into this table. Blank fields mean a company hadn’t reported that data by mid-August, as Q2’s earnings season wound down. Some of SIL’s components report in gold-centric terms.

The first couple columns of this table show each SIL component’s symbol and weighting within this ETF as of mid-August. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each miner’s Q2’19 silver production in ounces, along with its absolute year-over-year change. Next comes this same quarter’s gold production.

Nearly all the major silver miners in SIL also produce significant-to-large amounts of gold! That’s truly a double-edged sword. While gold really stabilizes and boosts silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. So the next column reveals how pure these elite silver miners are, approximating their percentages of Q2’19 revenues actually derived from silver. This is calculated one of two ways.

The large majority of these SIL silver miners reported total Q2 revenues. Quarterly silver production multiplied by silver’s average price in Q2 can be divided by these sales to yield an accurate relative-purity gauge. When Q2 sales weren’t reported, I estimated them by adding silver sales to gold sales based on their production and average quarterly prices. But that’s less optimal, as it ignores any base-metals byproducts.

Next comes the major silver miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated and hard GAAP earnings, with a couple exceptions necessary.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. Companies with symbols highlighted in light-blue have newly climbed into the elite ranks of SIL’s top 17 over this past year. This entire dataset together is quite valuable.

It offers a fantastic high-level read on how the major silver miners are faring fundamentally as an industry and individually. The super-low silver prices for most of Q2 really weighed on operating cash flows and earnings last quarter. But the major silver miners’ years-old and still-ongoing diversification into gold helped them weather the brutal low-silver-price storm. They still need silver to power far higher to thrive again.

The silver miners had the cards stacked against them last quarter, so their Q2 results weren’t going to look good. In addition to slumping towards early July’s incredible 26.8-year secular low relative to gold, silver languished for most of Q2. By late May it had fallen 5.0% quarter-to-date, far worse than gold’s own 1.0% QTD loss. While it did rally 6.6% into quarter-end from that nadir, that lagged gold’s 10.2% rebound.

Overall in Q2’19, silver merely eked out a pathetic 1.3% gain despite gold’s blistering 9.1% rally. And silver prices averaged a miserable $14.88 last quarter, plunging 9.9% year-over-year from Q2’18’s levels! Silver was about as deeply out of favor as it can get, which naturally killed any interest at all in the silver-mining stocks. At worst in late May, SIL had dropped 12.2% year-to-date on silver’s own 7.2% YTD loss.

So there weren’t going to be any silver-stock fireworks coming out of such a dismal quarter. Considering that nigh-apocalyptic silver backdrop, the major silver miners fared reasonably well in Q2. They kept on plugging away despite the choking pall of despair. The chronically-weak silver prices continued to justify the years-old shift into gold by traditional silver miners, which was again evident in the top SIL miners’ outputs.

That 73.7m ounces of silver these SIL-top-17 miners produced last quarter fell 1.8% YoY from Q2’18’s levels. Over the 13 quarters since Q2’16 when I started this deep-quarterly-results research thread, the SIL-top-17 peak was 78.6m ounces in Q4’17. Silver production is waning even among traditional major silver miners, its economics have been too constrained. They are increasingly shifting into gold instead.

The collective gold production from these elite silver majors ran 1.5m ounces in Q2’19, shooting up 13.4% YoY! They’ve been increasingly diversifying into gold in recent years as silver languished, since the yellow metal has had way-superior economics. The bombed-out silver prices have heavily impaired silver mines’ generation of operating cash flows and profits. So the silver miners have been forced to adapt.

Silver mining is as capital-intensive as gold mining, requiring similar large expenses to plan, permit, and construct new mines, mills, and expansions. It needs similar fleets of heavy excavators and haul trucks to dig and move the silver-bearing ore. Similar levels of employees are necessary to run silver mines. But at recent years’ average precious-metals prices, silver mines generate far lower returns than gold mines.

So even longtime traditional silver miners have reallocated much of their capital investments into growing gold outputs at silver’s expense. According to the Silver Institute’s latest World Silver Survey, 2018 was the third year in a row of waning global silver mine production. The mined-silver-supply shrinkage is even accelerating, running 0.0% in 2016, 1.8% in 2017, and 2.4% in 2018! Peak silver could really be upon us.

SIL’s top 3 component stocks commanding fully 38.9% of its total weighting sure exemplify the yellowing of the major silver miners. Pan American Silver currently crowns this leading silver-stock ETF, and has a proud heritage of mining its namesake metal. Last quarter its silver output only grew 2.9% YoY, yet its gold production skyrocketed 190.1% higher to 155k ounces! Thus its silver purity collapsed to merely 34.1%.

PAAS acquired troubled silver miner Tahoe Resources back in mid-November. Tahoe had owned what was once the world’s largest primary silver mine, Escobal in Guatemala. It had produced 5.7m ounces in Q1’17 before that country’s government unjustly shut it down after a frivolous lawsuit on a trivial bureaucratic misstep by the regulator. PAAS hopes to work through the red tape to win approval to restart Escobal.

But the real prize in that fire-sale buyout was Tahoe’s gold production from other mines. That deal closed in late February, so that new gold wasn’t fully reflected until PAAS’s latest Q2 results. Now this former silver giant is forecasting midpoint production of 575.0k ounces of gold and 25.8m ounces of silver in 2019. That is actually deep into mid-tier-gold territory and a far cry from 2018’s output of 178.9k and 24.8m!

SIL’s second-largest component in mid-August as this latest earnings season ended was the Russian-founded but UK-listed Polymetal. Its silver production fell 11.8% YoY in Q2, yet its gold output soared 30.2% to 302k ounces. That actually makes this company a major gold miner, exceeding 1m ounces annually! So not surprisingly only 18.1% of its Q2 revenues were derived from silver, among the lowest of SIL.

SIL’s third-largest component is Wheaton Precious Metals. It used to be a pure silver-streaming play known as Silver Wheaton. Silver streamers make big upfront payments to miners to pre-purchase some of their future silver production at far-below-market unit prices. This is beneficial to miners because they use the large initial capital infusions to help finance mine builds, which banks often charge usurious rates for.

Back in May 2017 Wheaton changed its name and symbol to reflect its increasing diversification into gold streaming. In Q2’19 WPM’s silver output collapsed 20.6% YoY, but its gold surged 17.9% higher! That pushed its silver-purity percentage in sales terms to just 38.0%, way below the 50%+ threshold defining primary silver miners. This gold-heavy ratio is forecast to persist, with WPM allocating more capital to gold.

Pan American will probably soon follow in Wheaton’s footsteps and change its name and symbol to reflect its new gold-dominated future. As miserable as silver has fared in recent years, I’m starting to wonder if the word “silver” in a miner’s name has become a liability with investors. The major primary silver miners are a dying breed, as it’s exceedingly difficult to generate sufficient cash flows and profits mining silver alone.

Major silver miners are becoming so scarce that SIL’s fourth-largest component is Korea Zinc. Actually a base-metals smelter, this company has nothing to do with silver mining. It ought to be kicked out of SIL posthaste, as its presence and big 1/11th weighting really retards this ETF’s performance. Korea Zinc smelted about 64.0m ounces of silver in 2018, which approximates roughly 17% of its full-year revenue.

Global X was really scraping the bottom of the barrel to include a company like Korea Zinc in SIL. I’m sure there’s not a single SIL investor who wants base-metals-smelting exposure in what is advertised as a “Silver Miners ETF”. The weighting and capital allocated to Korea Zinc should be reallocated and spread proportionally across the other SIL stocks. The ranks of major silver miners are becoming more rarefied.

In Q2’19 the SIL-top-17 silver miners averaged just 36.4% of their quarterly revenues from that metal! That was on the lower side of the recent years’ range. Only 3 of SIL’s top-17 component stocks were still primary silver miners last quarter, First Majestic Silver, Silvercorp Metals, and Fortuna Silver Mines. SIL is effectively another gold miners’ ETF, where its holdings derive nearly 2/3rds of their revenues from gold!

With SIL-top-17 silver production sliding 1.8% YoY in Q2’19, the per-ounce mining costs should’ve risen proportionally. Silver-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. So the lower production, the fewer ounces to spread mining’s big fixed costs across. But the major silver miners’ Q2’19 costs surged disproportionally.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q2’19 these SIL-top-17 silver miners reported cash costs averaging $6.88 per ounce, which soared 73.9% YoY! While sounding catastrophic, that remains well under Q2’s average silver price.

That means the silver miners faced no existential threat last quarter despite its terrible silver prices. The reason cash costs soared is because Hecla Mining and Silvercorp Metals both reported negative cash costs in Q2’18 due to big byproduct credits. Excluding them, the comparable cash costs a year ago ran $6.49 which is much closer to last quarter’s levels. The silver miners are doing well holding the line on costs.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain silver mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

The SIL-top-17 silver miners reporting AISCs in Q2’19 averaged $11.51 per ounce, which was only up 5.3% YoY. That was really impressive considering their waning silver production, and the challenges of producing this metal at such low prices. That was well under late May’s silver low of $14.34, as well as mid-November’s 2.8-year secular low of $13.99. The silver miners are nicely navigating silver’s vexing slump.

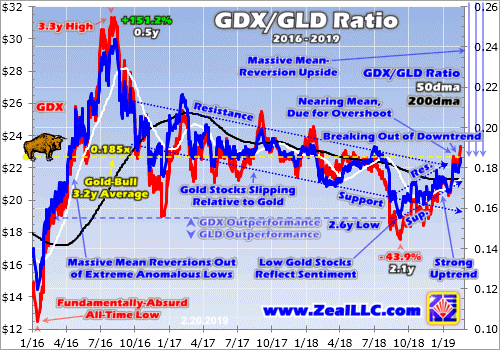

At Q2’19’s average silver price of $14.88 and average SIL-top-17 AISCs of $11.51, these miners were earning $3.37 per ounce. That’s not bad for a sector that investors mostly left for dead, convinced it must be doomed. Being so wildly undervalued relative to gold, silver has the potential to surge much higher in this resurgent gold bull. Historically the Silver/Gold Ratio has averaged around 55x, which has big implications.

At early July’s apocalyptic 26.8-year low relative to gold, the SGR plunged all the way to 93.5x! In other words, it took 93.5 ounces of silver to equal the value of a single ounce of gold. But silver was awoken from its zombified stupor soon after, thanks to gold’s decisive bull-market breakout to major new secular highs. So by mid-August as Q2’s earnings season wrapped up, silver had clawed back up to an 88.5x SGR.

By August 15 silver had regained $17.22 at best, which was merely an 18.4-month high. That was still a joke compared to gold though, which at $1524 had soared to its own 6.3-year secular high! In order to mean revert back up to historical norms compared to gold, silver has a long way to go. At $1524 gold, a 55x SGR implies a silver price of $27.71. That’s another 61% higher from silver’s still-weak mid-August levels.

Industry-wide all-in sustaining costs don’t change much regardless of prevailing silver prices. That is because they are largely determined during mine-planning stages, when engineers and geologists decide which ores to mine, how to dig to them, and how to process them to extract the silver. So higher silver prices yield explosive profits growth, which is what makes the volatile silver-mining stocks so alluring to traders.

A silver mean reversion to 1/55th the price of gold at its mid-August prices would catapult silver-mining profits 381% higher at Q2’s AISCs! Capital would deluge into this forsaken sector if these miners were earning $16.20 per ounce on $27.71 silver. And mean reversions out of extreme lows never stop at the historical averages, but their strong upside momentum carries them to proportional upside overshoots.

So the potential silver-miner earnings growth and thus stock-price gains when silver normalizes relative to gold are colossal. But lest that seem like a pie-in-the-sky pipe dream, consider just the first half of Q3’19 already in the books when Q2’s earnings season concluded. As of August 15th, silver had already risen to a $16.10 QTD average. That was 8.2% higher than Q2’s miserable $14.88, and very bullish for the miners.

Assuming Q3’s AISCs stay in line with Q2’s which is highly likely, silver-mining profits could be exploding 36.2% higher QoQ in this current quarter! That of course supports much higher silver-stock prices. All silver and its miners’ stocks need to thrive is for traders to be convinced gold is likely to keep climbing on balance. That necessary shift in overall precious-metals sentiment back to bullish is finally underway.

The caveat is the degree to which silver miners’ earnings amplify this metal’s upside is dependent on how much of their sales are still derived from silver as it reverts north. If the SIL top 17 are still getting 36% of their sales from silver, their stocks should surge with silver. But the more they diversify into gold, the more dependent they will be on gold-price moves. Those aren’t as big as silver’s since gold is a far-larger market.

Back to Q2’19 results, the SIL-top-17 silver miners’ hard accounting metrics mostly weakened. And that makes sense with average silver prices falling 9.9% YoY and these elite silver miners producing 1.8% less. They did manage to achieve a 2.4% gain in total revenues to $3.6b last quarter. That was solely thanks to their collective gold output growing 13.4% YoY. Without that gold, Q2 would’ve looked terrible.

Operating-cash-flow generation was weak, plunging 43.8% YoY to $555m across the SIL top 17. That makes it harder for these miners to invest in future production growth. Their total cash treasuries reported at the end of Q2 also fell 33.9% to $2.4b. Silver needs to rally considerably and stay higher for at least a few quarters before the silver miners can spin off strong cashflows again. Hopefully that’s now underway.

These major silver miners’ hard GAAP earnings in Q2’19 proved really weak, reflecting the miserable prevailing silver prices. Together they reported a collective net loss of $134m, compared to a $463m group profit in Q2’18. Out of the 13 of these SIL-top-17 miners that reported last quarter’s earnings, 8 were losses. Leading the way was the streaming giant Wheaton Precious Metals, which lost $125m alone.

WPM wrote down $166m on a streaming agreement it had overpaid for, a massive non-cash charge that helped torpedo the silver miners’ profits. But I didn’t see any other major writedowns, which was on the impressive side given last quarter’s super-low silver prices. Thankfully traders don’t buy silver stocks for how they’re faring today, but for how they are likely to do as silver mean reverts higher. It’s all about potential.

Silver’s last major upleg erupted in essentially the first half of 2016, when silver soared 50.2% higher on a parallel 29.9% gold upleg. SIL blasted 247.8% higher in just 6.9 months, a heck of a gain for major silver stocks. But the purer primary silver miners did far better. The purest major silver miner First Majestic’s stock was a moonshot, skyrocketing a staggering 633.9% higher in that same short span! SIL’s gains are muted.

The key takeaway here is avoid SIL. The world’s leading “Silver Miners ETF” is increasingly burdened with primary gold miners with waning silver exposure. And having over 1/11th of your capital allocated to silver miners squandered in Korea Zinc is sheer madness! If you want to leverage silver’s long-overdue mean reversion higher relative to gold, it’s far better to deploy in smaller purer primary silver miners alone.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In the first half of 2019 well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. We’ve recently realized big gains including 109.7%, 105.8%, and 103.0%!

To profitably trade high-potential silver stocks, you need to stay informed about the broader market cycles that drive gold. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast so they can ride entire uplegs.

The bottom line is the major silver miners had a challenging Q2. Silver languished the entire quarter, on its way to horrific quarter-century-plus lows relative to gold. Silver didn’t start perking up until mid-July, after gold’s decisive bull-market breakout had lasted long enough to convince traders gold’s upside was real and sustainable. So silver miners’ operating cash flows and earnings were way down last quarter.

That will really change in Q3 as long as silver doesn’t plummet into quarter-end. It’s incredible how fast silver miners’ fundamentals improve with higher silver prices. And silver’s upside potential is enormous, as it has a vast way to go to normalize relative to prevailing gold prices. The more that precious-metals sentiment improves, the more capital will flow into the tiny silver sector catapulting miners’ stocks far higher.

Adam Hamilton, CPA

September 3, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

The mid-tier gold miners’ stocks have soared in recent months on gold’s decisive bull-market breakout. They are this sector’s sweet spot for stock-price upside potential, with room for strong production growth which investors love. That’s an attractive contrast to the stagnating major gold miners. The mid-tiers’ recently-reported Q2’19 results reveal whether their fundamentals justify their strong surge this summer.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

The global nature of the gold-mining industry complicates efforts to gather this important data. Many mid-tier gold miners trade in Australia, Canada, South Africa, the United Kingdom, and other countries with quite-different reporting requirements. These include half-year reporting rather than quarterly, long 90-day filing deadlines after year-ends, and very-dissimilar presentations of operating and financial results.

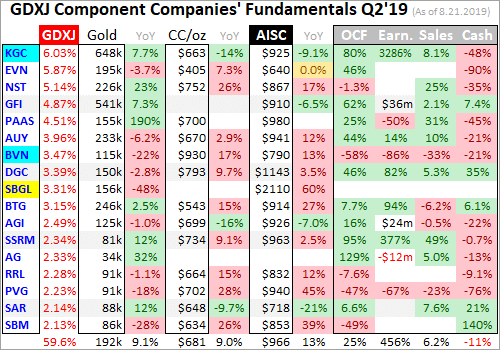

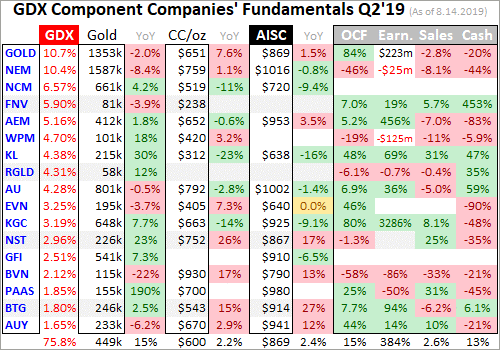

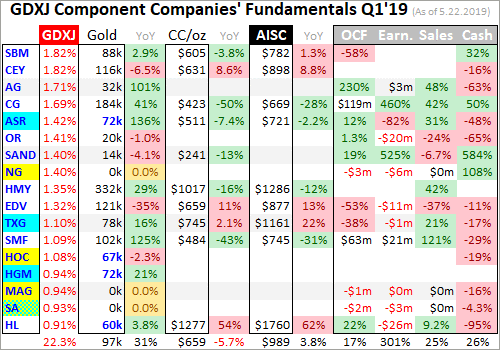

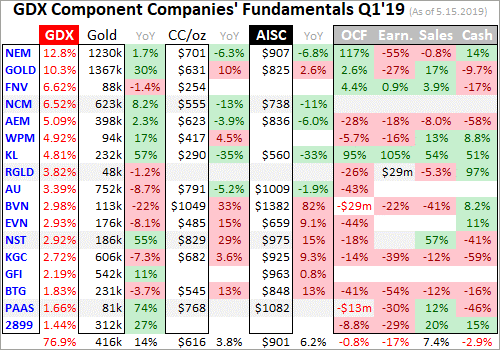

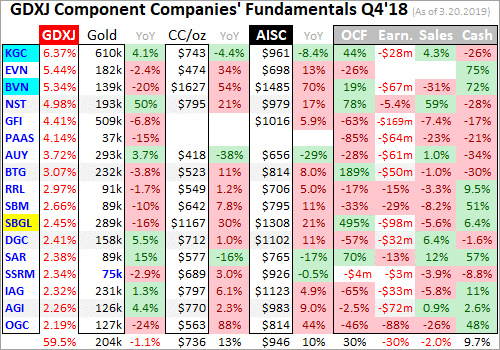

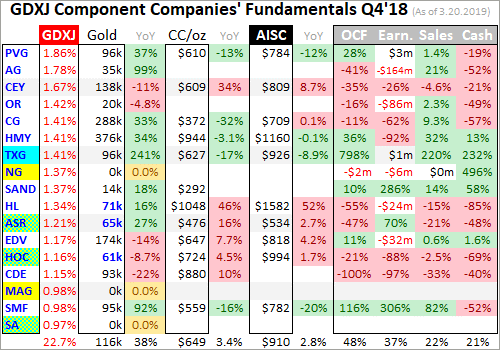

The definitive list of mid-tier gold miners to analyze comes from the GDXJ VanEck Vectors Junior Gold Miners ETF. Despite its misleading name, GDXJ is totally dominated by mid-tier gold miners and not juniors. GDXJ is the world’s second-largest gold-stock ETF, with $4.5b of net assets this week. That is only behind its big-brother GDX VanEck Vectors Gold Miners ETF that includes the major gold miners.

Major gold miners are those that produce over 1m ounces of gold annually. The mid-tier gold miners are smaller, producing between 300k to 1m ounces each year. Below 300k is the junior realm. Translated into quarterly terms, majors mine 250k+ ounces, mid-tiers 75k to 250k, and juniors less than 75k. GDXJ was originally launched as a real junior-gold-stock ETF as its name implies, but it was forced to change its mission.

Gold stocks soared in price and popularity in the first half of 2016, ignited by a new bull market in gold. The metal itself awoke from deep secular lows and surged 29.9% higher in just 6.7 months. GDXJ and GDX skyrocketed 202.5% and 151.2% higher in roughly that same span, greatly leveraging gold’s gains! As capital flooded into GDXJ to own junior miners, this ETF risked running afoul of Canadian securities laws.

Canada is the center of the junior-gold universe, where most juniors trade. Once any investor including an ETF buys up a 20%+ stake in a Canadian stock, it is legally deemed a takeover offer. This may have been relevant to a single corporate buyer amassing 20%+, but GDXJ’s legions of investors certainly weren’t trying to take over small gold miners. GDXJ diversified away from juniors to comply with that archaic rule.

Smaller juniors by market capitalization were abandoned entirely, cutting them off from the sizable flows of ETF capital. Larger juniors were kept, but with their weightings within GDXJ greatly demoted. Most of its ranks were filled with mid-tier gold miners, as well as a handful of smaller majors. That was frustrating, but ultimately beneficial. Mid-tier gold miners are in the sweet spot for stock-price-appreciation potential!

For years major gold miners have struggled with declining production, they can’t find or buy enough new gold to offset their depletion. And the stock-price inertia from their large market capitalizations is hard to overcome. The mid-tiers can and are boosting their gold output, which fuels growth in operating cash flows and profitability. With much-lower market caps, capital inflows drive their stock prices higher much faster.

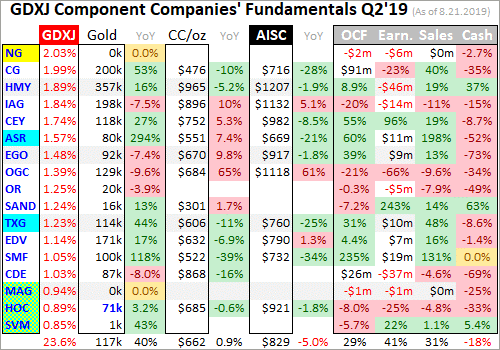

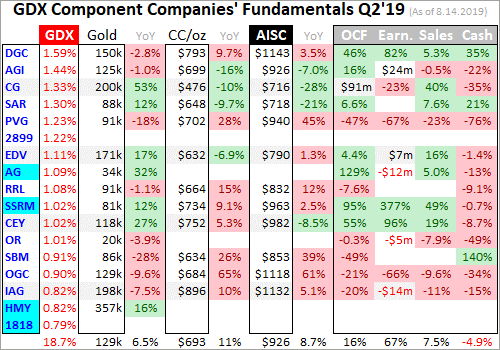

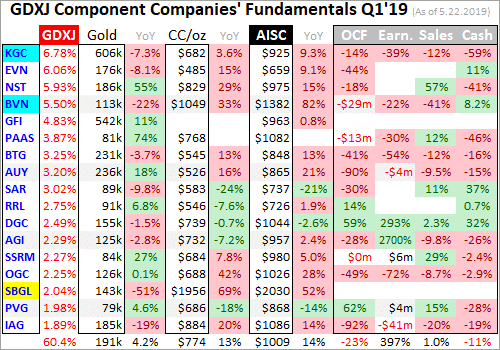

Every quarter I dive into the latest results from the top 34 GDXJ components. That’s simply an arbitrary number that fits neatly into the tables below, but a commanding sample. These companies represented 83.2% of GDXJ’s total weighting this week, even though it contained a whopping 70 stocks! 3 of the top 34 were majors mining 250k+ ounces, 24 mid-tiers at 75k to 250k, 5 “juniors” under 75k, and 2 explorers with zero.

These majors accounted for 12.8% of GDXJ’s total weighting, and really have no place in a “Junior Gold Miners ETF” when they could instead be exclusively in GDX. These mid-tiers weighed in at 60.9% of GDXJ. The “juniors” among the top 34 represented just 6.6% of GDXJ’s total. But only 1 of them at a mere 0.9% of GDXJ is a true junior, meaning it derives over half its revenues from actually mining gold.

The rest include 2 primary silver miners, a gold-royalty company, and a gold streamer. GDXJ is actually a full-on mid-tier gold miners ETF, with modest major and tiny junior exposure. Traders need to realize it is not a junior-gold investment vehicle as advertised. GDXJ also has major overlap with GDX. Fully 29 of these top 34 GDXJ gold miners are included in GDX too, with 23 of them also among GDX’s top 34 stocks.

The GDXJ top 34 accounting for 83.2% of its total weighting also represent 39.8% of GDX’s own total weighting! The GDXJ top 34 mostly clustered between the 10th- to 40th-highest weightings in GDX. Thus nearly 5/6ths of GDXJ is made up by almost 4/10ths of GDX. But GDXJ is far superior, excluding the large gold majors struggling with production growth. GDXJ gives much-higher weightings to better mid-tier miners.

The average Q2’19 gold production among GDXJ’s top 34 was 157k ounces, a bit over half as big as the GDX top 34’s 299k average. Despite these two ETFs’ extensive common holdings, GDXJ is increasingly outperforming GDX. GDXJ holds many of the world’s best mid-tier gold miners with big upside potential as gold’s own bull continues powering higher. Thus it is important to analyze GDXJ miners’ latest results.

So after each quarterly earnings season I wade through all available operational and financial reports and dump key data into a big spreadsheet for analysis. Some highlights make it into these tables. Any blank fields mean a company hadn’t reported that data as of this Wednesday. The first couple columns show each GDXJ component’s symbol and weighting within this ETF as of this week. Not all are U.S. symbols.

19 of the GDXJ top 34 primarily trade in the U.S., 5 in Australia, 8 in Canada, and 2 in the U.K. So some symbols are listings from companies’ main foreign stock exchanges. That’s followed by each gold miner’s Q2’19 production in ounces, which is mostly in pure-gold terms excluding byproducts often found in gold ore like silver and base metals. Then production’s absolute year-over-year change from Q2’18 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drive profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, revenues, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. In cases where foreign GDXJ components only released half-year data, I used that and split it in half where appropriate. That offers a decent approximation of Q2 results.

Symbols highlighted in light blue newly climbed into the ranks of GDXJ’s top 34 over this past year. And symbols highlighted in yellow show the rare GDXJ-top-34 components that aren’t also in GDX. If both conditions are true, blue-yellow checkerboarding is used. Production bold-faced in blue shows any rare junior gold miners in GDXJ’s higher ranks, under 75k ounces quarterly with over half of sales from gold.

This whole valuable dataset compared with past quarters offers a fantastic high-level read on how mid-tier gold miners are faring fundamentally as an industry. This last quarter was interesting, as gold’s awesome breakout surge to major new secular highs didn’t get underway until just before quarter-end. So the mid-tier gold miners had to contend with flat gold prices, with Q2’19’s average of $1309 merely 0.2% higher YoY.

The shuffling in the ranks of GDXJ’s top 34 components continued over this past year, with major gold miner Kinross Gold added. It, Gold Fields, and Harmony Gold really should be shifted exclusively into GDX since their production is way into major-dom. Gold miners of that scale just defeat the purpose of a “Junior Gold Miners ETF”, retarding its upside potential and eroding traders’ confidence in its managers’ competence.

Most of the other new additions are good though, including mid-tiers Buenaventura, Alacer Gold, and Torex Gold. While Hochschild Mining was technically a junior last quarter, it will likely soon grow into a mid-tier mining 75k+ ounces of gold quarterly. But there’s one GDXJ component that reported such an extreme quarter that it skews most of the year-over-year comparisons. That is South Africa’s Sibanye-Stillwater.

SBGL is actually a primary platinum-group-metals miner, which drove nearly two-thirds of its implied revenue based on average metals prices in Q2! Its shrinking South African gold operations are a total mess, just emerging from a 5-month-long strike organized by a violent Marxist union. That crippled its gold mines, and left at least 9 people dead! Sibanye-Stillwater also has to fight South Africa’s absurdly-corrupt government.

Even though that hellish strike ended in mid-April, very early in Q2, SBGL’s gold production plummeted a catastrophic 47.9% YoY last quarter! That catapulted its all-in sustaining costs to a ridiculous $2110 per ounce, up an extreme 60.5% YoY from already-high levels. This shocking anomaly needs to be excluded in GDXJ comparisons. I wouldn’t invest in this company if it was the last miner on earth, it is a nightmare.

Production has always been the lifeblood of the gold-mining industry. Gold miners have no control over prevailing gold prices, their product sells for whatever the markets offer. Thus growing production is the only manageable way to boost revenues, leading to amplified gains in operating cash flows and profits. Higher production generates more capital to invest in expanding existing mines and building or buying new ones.

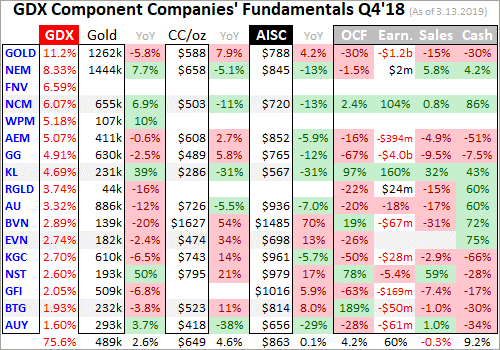

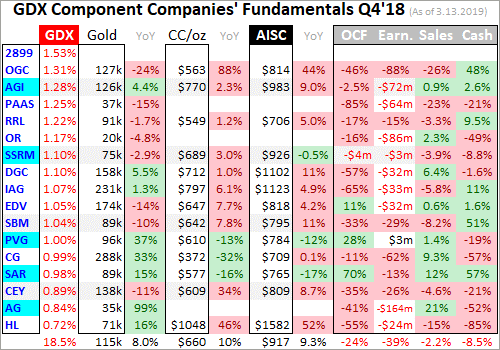

Thus gold-stock investors have long prized production growth above everything else, as it is inexorably linked to company growth and thus stock-price-appreciation potential. In Q2’19 these GDXJ-top-34 gold miners collectively produced 5.0m ounces of gold. That was actually down 1.2% YoY, which is worse than the 0.7% shrinkage the top 34 GDX majors reported last quarter after being adjusted for mega-mergers.

But excluding SBGL’s mayhem, the rest of the GDXJ top 34 actually managed to grow their total output by an impressive 1.7% YoY to 4.9m ounces! That not only trounced the majors, but narrowly bested the world’s aggregate production growth in Q2. According to gold’s leading fundamental authority, the World Gold Council, total world output grew 1.6% YoY last quarter to 28.4m ounces. The mid-tiers are thriving.

The GDXJ mid-tiers were able to enjoy strong production growth because this ETF isn’t burdened with many struggling major gold miners that dominate GDX. Again GDXJ’s components start at the 10th-highest weighting in GDX. The 9 above it averaged colossal Q2 production of 585k ounces, which is 3.7x bigger than the GDXJ top 34’s average! Gold mining’s inherent geological limitations make it very difficult to scale.

The more gold miners produce, the harder it is to even keep up with relentless depletion let alone grow their output consistently. Large economically-viable gold deposits are getting increasingly difficult to find and ever-more-expensive to develop, with low-hanging fruit long since exploited. But with much-smaller production bases, mine expansions and new mine builds generate big output growth for mid-tier golds.

The majors don’t only face that large-base growth problem with their production scales, but also with their stocks’ market capitalizations. The GDXJ top 34 companies averaged $2.5b in the middle of this week, compared to $6.9b in the GDX top 34 when I analyzed their Q2 results last week. With the mid-tiers generally around a third as big as the majors, their stock prices have much less inertia restraining them.

With gold returning to favor since late June’s awesome decisive bull-market breakout, the mid-tier-filled GDXJ is already outperforming the major-dominated GDX. Since its year-to-date low in late May, GDXJ surged as much as 52.1% higher by early August! That was considerably better than GDX’s 46.2% rally in the same timeframe. The longer gold-bull uplegs persist, the bigger the mid-tier outperformance grows.

The mid-tier gold miners continue to prove all-important production growth is achievable off smaller bases. With a handful of mines or less to operate, mid-tiers can focus on expanding them or building a new mine to boost their output beyond depletion. But the majors are increasingly failing to do this from the super-high production bases they operate at. As long as majors are struggling, it is prudent to avoid them.

Also interesting on the mid-tier production front was silver. Last quarter the GDXJ-top-34 miners’ silver output blasted 42.8% higher YoY to 28.2m ounces! Some of these companies indeed saw exploding silver production, led by Yamana Gold’s rocketing up 65.8% YoY to 2.2m ounces and SSR Mining’s soaring a similar 55.8% YoY to 1.5m ounces. But new GDXJ-top-34 components drove most of the silver growth.

Buenaventura and Hochschild Mining produced 5.5m and 4.3m ounces of silver last quarter, and they weren’t in GDXJ’s top 34 in Q2’18. Excluding them, the rest of these mid-tier gold miners actually saw their total silver output slump 5.1% YoY. I’ll discuss the serious challenges silver mining faces in next week’s essay, which will wade through the results of the top silver miners of the leading silver miners’ ETF.

In gold mining, production and costs are generally inversely related. Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring about the same levels of infrastructure, equipment, and employees. So the higher production, the more ounces to spread mining’s big fixed costs across. Thus Q2’19’s solid production growth among the GDXJ top 34 ex-SBGL should’ve yielded proportionally-lower costs.

There are two major ways to measure gold-mining costs, classic cash costs per ounce and the superior all-in sustaining costs per ounce. Both are useful metrics. Cash costs are the acid test of gold-miner survivability in lower-gold-price environments, revealing the worst-case gold levels necessary to keep the mines running. All-in sustaining costs show where gold needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q2’19 these top-34-GDXJ-component gold miners that reported cash costs averaged $672 per ounce. That actually rose a sharp 6.6% YoY, and was worse than the GDX-top-34 majors’ $641 mean.

Sibanye-Stillwater didn’t report Q2 cash costs, so that wasn’t a factor. But a couple of other anomalous situations dragged up this average. Buenaventura has been struggling with weaker production, resulting in extreme $930 cash costs last quarter. And Harmony Gold, a South African miner facing that country’s miserable operating environment, had even-worse $965 cash costs in Q2’19! Those are crazy-high.