The silver miners’ stocks have been pummeled in recent months, plunging near major secular lows in late May. Sentiment in this tiny sector is miserable, reflecting silver prices continuing to languish relative to gold. This has forced traditional silver miners to increasingly diversify into gold, which has far-superior economics. The major silver miners’ ongoing shift from silver is apparent in their recently-released Q1’19 results.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Required by the U.S. Securities and Exchange Commission, these 10-Qs and 10-Ks contain the best fundamental data available to traders. They dispel all the sentiment distortions inevitably surrounding prevailing stock-price levels, revealing corporations’ underlying hard fundamental realities.

The definitive list of major silver-mining stocks to analyze comes from the world’s most-popular silver-stock investment vehicle, the SIL Global X Silver Miners ETF. Launched way back in April 2010, it has maintained a big first-mover advantage. SIL’s net assets were running $294m in mid-May near the end of Q1’s earnings season, 5.6x greater than its next-biggest competitor’s. SIL is the leading silver-stock benchmark.

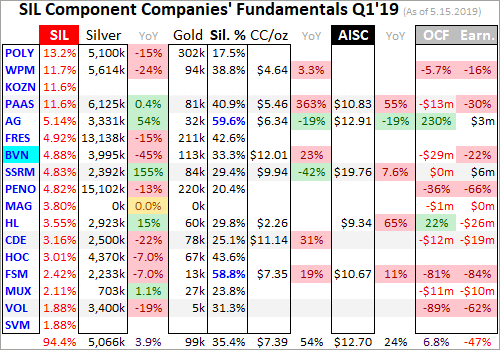

In mid-May SIL included 24 component stocks, which are weighted somewhat proportionally to their market capitalizations. This list includes the world’s largest silver miners, including the biggest primary ones. Every quarter I dive into the latest operating and financial results from SIL’s top 17 companies. That’s simply an arbitrary number that fits neatly into the table below, but still a commanding sample.

As of mid-May these major silver miners accounted for fully 94.4% of SIL’s total weighting. In Q1’19 they collectively mined 70.9m ounces of silver. The latest comprehensive data available for global silver supply and demand came from the Silver Institute in April 2019. That covered 2018, when world silver mine production totaled 855.7m ounces. That equates to a run rate around 213.9m ounces per quarter.

Assuming that mining pace persisted in Q1’19, SIL’s top 17 silver miners were responsible for about 33% of world production. That’s relatively high considering just 26% of 2018’s global silver output was produced at primary silver mines! 38% came from lead/zinc mines, 23% from copper, and 12% from gold. Nearly 3/4ths of all silver produced worldwide is just a byproduct. Primary silver mines and miners are fairly rare.

Scarce silver-heavy deposits are required to support primary silver mines, where over half their revenue comes from silver. They are increasingly difficult to discover and ever-more expensive to develop. And silver’s challenging economics of recent years argue against miners even pursuing it. So even traditional major silver miners have shifted their investment focus into actively diversifying into far-more-profitable gold.

Silver price levels are best measured relative to prevailing gold prices, which overwhelmingly drive silver price action. In late May the Silver/Gold Ratio continued collapsing to its worst levels witnessed in 26.1 years, since April 1993! These secular extremes of the worst silver price levels in over a quarter century are multiplying the endless misery racking this once-proud sector. This silver environment is utterly wretched.

The largest silver miners dominating SIL’s ranks are scattered around the world. 10 of the top 17 mainly trade in U.S. stock markets, 3 in the United Kingdom, and 1 each in South Korea, Mexico, Peru, and Canada. SIL’s geopolitical diversity is good for investors, but makes it difficult to analyze and compare the biggest silver miners’ results. Financial-reporting requirements vary considerably from country to country.

In the U.K. companies report in half-year increments instead of quarterly. Some silver miners still publish quarterly updates, but their data is limited. In cases where half-year data is all that was made available, I split it in half for a Q1 approximation. Canada has quarterly reporting, but the deadlines are looser than in the States. Some Canadian miners really drag their feet, publishing their quarterlies close to legal limits.

The big silver companies in South Korea, Mexico, and Peru present other problems. Their reporting is naturally done in their own languages, which I can’t decipher. Some release limited information in English, but even those translations can be difficult to interpret due to differing accounting standards and focuses. It’s definitely challenging bringing all the quarterly data together for the diverse SIL-top-17 silver miners.

But analyzing them in the aggregate is essential to understand how they are faring. So each quarter I wade through all available operational and financial reports and dump the data into a big spreadsheet for analysis. Some highlights make it into this table. Blank fields mean a company hadn’t reported that data by mid-May, as Q1’s earnings season wound down. Some of SIL’s components report in gold-centric terms.

The first couple columns of this table show each SIL component’s symbol and weighting within this ETF as of mid-May. While most of these stocks trade on US exchanges, some symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each miner’s Q1’19 silver production in ounces, along with its absolute year-over-year change. Next comes this same quarter’s gold production.

Nearly all the major silver miners in SIL also produce significant-to-large amounts of gold! That’s truly a double-edged sword. While gold really stabilizes and boosts silver miners’ cash flows, it also retards their stocks’ sensitivity to silver itself. So the next column reveals how pure these elite silver miners are, approximating their percentages of Q1’19 revenues actually derived from silver. This is calculated one of two ways.

The large majority of these top SIL silver miners reported total Q1 revenues. Quarterly silver production multiplied by silver’s average price in Q1 can be divided by these sales to yield an accurate relative-purity gauge. When Q1 sales weren’t reported, I estimated them by adding silver sales to gold sales based on their production and average quarterly prices. But that’s less optimal, as it ignores any base-metals byproducts.

Next comes the major silver miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated and hard GAAP earnings, with a couple exceptions necessary.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. Companies with symbols highlighted in light-blue have newly climbed into the elite ranks of SIL’s top 17 over this past year. This entire dataset together is quite valuable.

It offers a fantastic high-level read on how the major silver miners are faring fundamentally as an industry and individually. The crazy-low silver prices really weighed on operating cash flows and earnings in Q1, and the silver miners’ years-old shift into gold continued. These companies are having no problem just surviving this silver-sentiment wasteland, but they probably won’t be thriving again before silver recovers.

SIL’s poor performance certainly reflects the challenges of profitably mining silver with its price so darned cheap. Year-to-date in late May, SIL had already lost 12.2%. Silver itself was down 7.2% YTD at worst, starting to threaten mid-November 2018’s 2.8-year secular low of $13.99. And that just extended last year’s losing trend, where SIL plunged 23.3% amplifying silver’s own 8.6% loss by 2.7x. This sector looks ugly.

Silver’s weakest prices relative to gold in over a quarter century have continued to devastate silver-mining sentiment. Investors understandably want nothing to do with the forsaken silver miners, so their stock prices languish near major lows. Even their own managements seem really bearish, increasingly betting their companies’ futures on gold rather than silver. Silver’s Q1 price action further supports this decision.

During Q1’19 silver ground another 2.3% lower despite a 0.8% gold rally, bucking its primary driver. Q1’s average silver price of $15.54 fell 7.1% YoY from Q1’18’s average. That was way worse than gold’s mere 1.9% YoY average-price decline. The silver-mining industry is laboring under a pall of despair. Although production decisions aren’t made quarter by quarter, the chronically-weak silver prices are choking off output.

Production is the lifeblood of silver miners, and it continued to slide. The SIL top 17 that had reported their Q1 results by mid-May again mined 70.9m ounces of silver. That was down 3.1% YoY from Q1’18’s silver production, excluding Silvercorp Metals. SVM’s fiscal years end after Q1s, and it doesn’t report its longer more-comprehensive annual results until well after Q1’s normal quarterly earnings season wraps up.

It’s not just these major silver miners producing less of the white metal, the entire industry is according to the Silver Institute’s latest World Silver Survey. 2018 was the third year in a row of waning global silver mine production. This shrinkage is accelerating too as silver continues to languish, running 0.0% in 2016, 1.8% in 2017, and 2.4% in 2018! Peak silver may have been seen with this metal so unrewarding to mine.

The traditional major silver miners aren’t taking silver’s vexing fading lying down. They’ve spent recent years increasingly diversifying into gold, which has way-superior economics with silver prices so bombed out. The SIL top 17’s total gold production surged 10.9% YoY to 1387k ounces in Q1! This producing-less-silver-and-more-gold trend will continue to grow as long as silver prices waste away in the gutter.

Silver mining is as capital-intensive as gold mining, requiring similar large expenses to plan, permit, and construct new mines, mills, and expansions. It needs similar fleets of heavy excavators and haul trucks to dig and move the silver-bearing ore. Similar levels of employees are necessary to run silver mines. But silver generates much-lower cash flows than gold due its lower price. Silver miners have been forced to adapt.

This is readily evident in the top SIL miners’ production in Q1’19. SIL’s largest component in mid-May as this latest earnings season ended was the Russian-founded but UK-listed Polymetal. Its silver production fell 15.0% YoY in Q1, but its gold output surged 41.1%! Just 17.5% of its Q1 revenues came from silver, making it overwhelmingly a primary gold miner. Its newest mine ramping up is another sizable gold one.

SIL’s second-largest component is Wheaton Precious Metals. It used to be a pure silver-streaming play known as Silver Wheaton. Silver streamers make big upfront payments to miners to pre-purchase some of their future silver production at far-below-market unit prices. This is beneficial to miners because they use the large initial capital infusions to help finance mine builds, which banks often charge usurious rates for.

Back in May 2017 Wheaton changed its name and symbol to reflect its increasing diversification into gold streaming. In Q1’19 WPM’s silver output collapsed 24.4% YoY, but its gold surged 17.4% higher! That pushed its silver-purity percentage in sales terms to just 38.8%, way below the 50%+ threshold defining primary silver miners. WPM’s 5-year guidance issued in February forecasts this gold-heavy ratio persisting.

Major silver miners are becoming so scarce that SIL’s third-largest component is Korea Zinc. Actually a base-metals smelter, this company has nothing to do with silver mining. It ought to be kicked out of SIL post-haste, as its presence and big 1/9th weighting really retards this ETF’s performance. Korea Zinc smelted about 64.0m ounces of silver in 2018, which approximates roughly 17% of its full-year revenue.

Global X was really scraping the bottom of the barrel to include a company like Korea Zinc in SIL. I’m sure there’s not a single SIL investor who wants base-metals-smelting exposure in what is advertised as a “Silver Miners ETF”. The weighting and capital allocated to Korea Zinc can be reallocated and spread proportionally across the other SIL stocks. The ranks of major silver miners are becoming more rarefied.

SIL’s fourth-largest component in mid-May is Pan American Silver, which has a proud heritage mining its namesake metal. In Q1’19 its silver production was flat with a negligible 0.4% YoY increase, yet its gold output soared 74.2%! Thus PAAS’s silver purity slumped to 40.9%, the lowest by far seen in the years I’ve been doing this quarterly research. And it’s going to get much more gold-centric in coming quarters.

PAAS acquired troubled silver miner Tahoe Resources back in mid-November. Tahoe had owned what was once the world’s largest silver mine, Escobal in Guatemala. It had produced 5.7m ounces in Q1’17 before that country’s government unjustly shut it down after a frivolous lawsuit on a trivial bureaucratic misstep by the regulator. PAAS hopes to work through the red tape to win approval for Escobal to restart.

But the real prize in that fire-sale buyout was Tahoe’s gold production from other mines. That deal closed in late February, so that new gold wasn’t fully reflected in PAAS’s Q1 results. Now this former silver giant is forecasting midpoint production of 27.1m ounces of silver and 595.0k ounces of gold in 2019! That is way into mid-tier-gold territory and a far cry from 2018’s output of 24.8m and 178.9k. PAAS has turned yellow.

Pan American will probably soon follow in Wheaton’s footsteps and change its name and symbol to reflect its new gold-dominated future. As miserable as silver has been faring, I’m starting to wonder if the word “silver” in a miner’s name is becoming a liability with investors. The major primary silver miners are going extinct, forced to adapt by diversifying out of silver and into gold as the former languishes deeply out of favor.

In Q1’19 the SIL-top-17 miners averaged only 35.4% of their revenues derived from silver. That’s also the lowest seen since I started this thread of research with Q2’16 results. Only two of these miners remained primary silver ones, and their silver-purity percentages over 50% are highlighted in blue. They are First Majestic Silver and Fortuna Silver Mines, which together accounted for just 7.6% of SIL’s total weighting.

With SIL-top-17 silver production sliding 3.1% YoY in Q1’19, the per-ounce mining costs should’ve risen proportionally. Silver-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. So the lower production, the fewer ounces to spread mining’s big fixed costs across. SIL’s major silver miners indeed reported higher costs last quarter.

There are two major ways to measure silver-mining costs, classic cash costs per ounce and the superior all-in sustaining costs. Both are useful metrics. Cash costs are the acid test of silver-miner survivability in lower-silver-price environments, revealing the worst-case silver levels necessary to keep the mines running. All-in sustaining costs show where silver needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of silver, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q1’19 these SIL-top-17 silver miners reported cash costs averaging $7.39 per ounce. While that surged 23.6% YoY, it still remains far below prevailing prices. Silver miners face no existential threat.

The major silver miners’ average cash costs vary considerably quarter-to-quarter, partially depending on whether or not Silvercorp Metals happens to have edged into the top 17. This Canadian company mining in China has negative cash costs due to massive byproduct credits from lead and zinc. So over the past couple years, SIL-top-17 average cash costs have swung wildly ranging all the way from $3.95 to $6.75.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain silver mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current silver-production levels.

These additional expenses include exploration for new silver to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee silver mines. All-in sustaining costs are the most-important silver-mining cost metric by far for investors, revealing silver miners’ true operating profitability.

The SIL-top-17 silver miners reporting AISCs in Q1’19 averaged $12.70 per ounce, 7.2% higher YoY. That remained considerably below last quarter’s average silver price of $15.54, as well as late May’s ugly silver low of $14.34. So the silver-mining industry as a whole is still profitable even with silver drifting near quarter-century-plus lows relative to gold. And those AISCs are skewed higher by SSR Mining’s outlying read.

Another traditional silver miner that changed its name, this company used to be known as Silver Standard Resources. SSRM has shifted into gold too, gradually winding down its old Pirquitas silver mine resulting in abnormally-high AISCs of $19.76 per ounce. Excluding these, the SIL-top-17 average in Q1 falls to $10.94 which is a much-more-comfortable profits cushion between production costs and low silver prices.

Interestingly SSRM has been ramping up a new mine close to its old Pirquitas mill, and is starting to run that ore through. That makes SSR Mining one of the rare silver miners that’s going to see growing output this year. It is forecasting a midpoint of 4.9m ounces of silver production in 2019, a 74% jump from last year’s levels! Higher production should lead to lower AISCs going forward, pulling the average back down.

As hopeless as silver has looked in recent months, it won’t stay down forever. Sooner or later gold will catch a major bid, probably on surging investment demand as these dangerous stock markets roll over. Capital will start migrating back into silver like usual once gold rallies long enough and high enough to convince traders its uptrend is sustainable. Since the silver market is so small, that portends much-higher prices.

At Q1’19’s average silver price of $15.54 and average SIL-top-17 AISCs of $12.70, these miners were earning $2.84 per ounce. That’s not bad for a sector that investors have left for dead, convinced it must be doomed. Being so wildly undervalued relative to gold, silver has the potential to surge much higher in the next gold upleg. The average Silver/Gold Ratio since Q1’16 right after today’s gold bull was born was 77.1x.

At $1400 and $1500 gold which are modest upleg gains, silver mean reverting to recent years’ average SGR levels would yield silver targets of $18.16 and $19.46. That’s conservative, ignoring the high odds for a mean-reversion overshoot, and only 16.9% and 25.2% above Q1’s average price. Yet with flat AISCs that would boost the SIL top 17’s profits by 92.3% and 138.0%! Their upside leverage to silver is amazing.

The caveat is the degree to which silver miners’ earnings amplify this metal’s upside is dependent on how much of their sales are still derived from silver when it turns north. If the SIL top 17 are still getting 35% of their sales from silver, their stocks should surge with silver. But the more they diversify into gold, the more dependent they will be on gold-price moves. Those aren’t as big as silver’s since gold is a far-larger market.

On the accounting front the top 17 SIL silver miners’ Q1’19 results highlighted the challenges of super-low silver prices. These companies collectively sold $3.0b worth of metals in Q1, which actually clocked in at an impressive 10.8% YoY increase. That was totally the result of these companies mining 10.9% more gold in Q1. Though it dilutes their silver-price exposure, shifting into gold really strengthens them financially.

But operating-cash-flow generation looked much worse, collapsing 55.1% YoY to $237m across the SIL top 17 that reported them for Q1. There was no single-company disaster, but Q1’s average silver prices being 7.1% lower YoY eroded OCFs universally. That led to these miners’ collective treasuries shrinking 22.9% YoY to $2.3b. That’s plenty to operate on, but not that much to fund many mine builds or expansions.

Hard GAAP profits reported by the SIL top 17 silver miners were very weak too in Q1’19, plunging 54.9% YoY to $123m. But there were no major writedowns from these low silver prices impairing the value of silver mines and deposits. Investors don’t buy silver stocks for how they are doing today, but for what they are likely to do as silver mean reverts higher. Silver-mining earnings surge dramatically as silver recovers.

Silver’s last major upleg erupted in essentially the first half of 2016, when silver soared 50.2% higher on a parallel 29.9% gold upleg. SIL blasted 247.8% higher in just 6.9 months, a heck of a gain for major silver stocks. But the purer primary silver miners did far better. The purest major silver miner First Majestic’s stock was a moonshot, skyrocketing a staggering 633.9% higher in that same short span! SIL’s gains are muted.

The key takeaway here is avoid SIL. The world’s leading “Silver Miners ETF” is increasingly burdened with primary gold miners with waning silver exposure. And having over 1/9th of your capital allocated to silver miners squandered in Korea Zinc is sheer madness! If you want to leverage silver’s long-overdue next mean reversion higher relative to gold, it’s far better to deploy in smaller purer primary silver miners alone.

One of my core missions at Zeal is relentlessly studying the silver-stock world to uncover the stocks with superior fundamentals and upside potential. The trading books in both our popular weekly and monthly newsletters are currently full of these better gold and silver miners. Mostly added in recent months as these stocks recovered from deep lows, their prices remain relatively low with big upside potential as gold rallies!

If you want to multiply your capital in the markets, you have to stay informed. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. As of Q1 we’ve recommended and realized 1089 newsletter stock trades since 2001, averaging annualized realized gains of +15.8%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is the major silver miners are still struggling. With silver continuing to languish at quarter-century-plus lows relative to gold, the economics of extracting it remain challenging. That led to slowing silver production and higher costs in Q1. The traditional major silver miners continued their years-long trend of increasingly diversifying into gold. Their percentage of sales derived from silver is still shrinking.

There aren’t enough major primary silver miners left to flesh out their own ETF, which is probably why SIL is dominated by gold miners. While it will rally with silver amplifying its gains, SIL’s upside potential is just dwarfed by the remaining purer silver stocks. Investors will be far-better rewarded buying them instead of settling for a watered-down silver-miners ETF. Their stocks will really surge as silver mean reverts much higher.

Adam Hamilton, CPA

June 4, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.