GoGold Resources (GGD.TO, C$0.71) is a company with assets in Mexico, both a producing and an exploration-stage project. Led by a management team that has over 27 years of experience in the country. The team developed 4 projects/companies that eventually got sold with at a good to hefty premium. Examples are: Gammon Gold ($1.5B merge with Alamos), Mexgold (sold for $375M), Nayarit ($80M, bought for $40M) and recently, the Santa Gertrudis project they sold to AEM for $96M (bought for $11M).

CEO Brad Langille is the second largest shareholder and holds 9.5% of outstanding shares. Biggest shareholder is Fred George, who was founding member of Gammon Gold. He led the development of the Ocampo project from exploration stage to one of the biggest silver and gold projects in Mexico, currently operated by Minera Frisco. Fred George owns about 14% of outstanding shares. Management combined owns over 30%.

Financial position is strong as they had C$9M in liquidity (cash + Metalla shares) at the end of the second quarter. After finishing the sale of the Santa Gertrudis project, they decided to pay off their remaining debt which leaves them debt-free.

Parral

After the sale of Santa Gertrudis, GoGold has two projects left. One of them is the young producing heap leaching mine of Parral, which is right next to the Mexican city of Chihuahua. This mine started its fifth year and is currently on a record streak: For the second consecutive quarter a beat in production and well on its way to reach 1.8Moz of silver equivalent. AISC is declining and currently sits at US$13.61/oz. Their realized silver price for the quarter was US$14.55, which gave them a 6.9% margin in Q2. As silver is a lot higher now than in Q2, we can assume a conservative realized price of US$17/oz for Q3. If AISC remains the same, their margin would rise to 24.9% or an increase of 261% quarter over quarter.

In June of this year, the company announced the build of a SART installation at their Parral mine. This will help lower costs of heap leaching and provide a saleable copper concentrate. This plant will see its first full operational quarter in Q1 of 2020. This should give a substantial decrease in AISC and add some revenue through the copper concentrate.

Their Parral mine will allow them to internally finance their exploration. Shareholders are protected from dilution through capital raises. In coming quarters, production will continue to rise towards 550-600Koz AgEq. Q2 saw 440Koz so we can expect further “records” in coming headlines. During my contact with management I received the following words:

“The cashflow we produce form Parral will fund our operations, G&A, and our exploration at Los Ricos and this is why we say we are a self-funding junior and do not need to raise money for the foreseeable future.”

Parral has a remaining mine life of 8 years and the proportion silver/gold in dollar value is about 55% silver and 45% gold. So despite of what you might read in their name, GoGold is mostly a silver producer.

Los Ricos

The Los Ricos project is my main reason to hold GoGold in my portfolio. The project has seen commercial production between 1908-1929. Production has been terminated at the start of the Great Depression. At the time of production, they kept track of the production data. Through this data we learn that the project was mined to a depth of 500m on different levels. Average values of 800g/t silver and 4g/t gold.

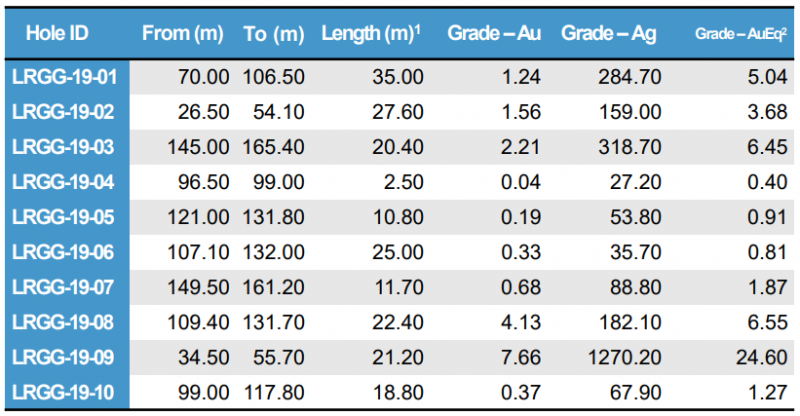

The project has about 65 historic drill results, which GoGold is trying to confirm with their own drill program. Up until today, they are succeeding well in this. Best hit: 21m of 7.66g/t gold and 1,270g/t silver (or 21m of 24.6g/t AuEq). Below I added the results of the first 10 drill holes by GoGold. Note that these are all 10 of them and not one has been left out mysteriously. By now the project has expanded to 37 drill results. I looked at all of these: Not one miss and on average thick mineralization with high values of gold and silver.

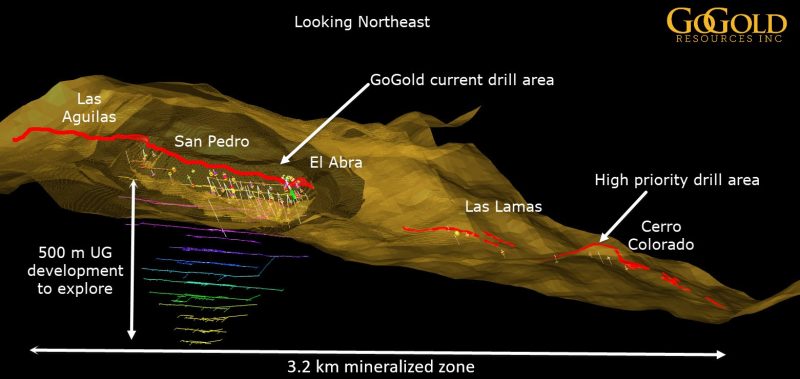

I recently felt an urgency to buy this company and this had nothing to do with silver taking off. In May, the company announced trenching results from a 3.2km strike. In this news release, GoGold told investors they would move a drill to the Cerro Colorado zone. This area has the ‘high priority drill area’ tag attached in the image below. Cerro Colorado is at the end of this strike and 1,500m away from the edge of the main zone.

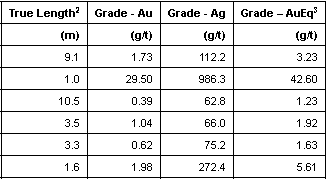

These first results of the Cerro Colorado zone seem to point to a big system. All 7 of these drill results show more high grade and thick gold and silver mineralization. As you can see in the image (above), there’s the ‘Las Lamas’ zone in between that 1,500m stepout. Below you find the results of the trenching GoGold did there. Management confirmed they would drill that target as well.

Since GoGold purchased the Los Ricos project, their share price has tripled. The silver price is largely a cause of this, but nonetheless an outperformance in the silver space. The Los Ricos project is a mere 6 months in their posession and the market is starting to notice. Should be, considering these drill results and potential. CEO Brad Langille recently noted that he’s been following this project for over 8 years and feels this is the most exciting project of his carreer. Talk is cheap of course, but seeing he upped his stake by 500,000 shares this year, is reason to take note.

The company is working on a maiden resource for Los Ricos, which they plan on delivering in the first quarter of 2020. Recently, they uploaded a VRIFY model on their website (link: https://gogoldresources.com/properties/los-ricos). CEO Langille wants to roll out this project on the Precious Metals Summit and Denver Gold Forum. Personally I believe this company will get some interest over the course of the next weeks. These presentations should be the start of this.

CEO Langille sees the Los Ricos project as an open pit mine with multi million ounces of high grade gold and silver. According to him this will be of similar, if not bigger size than the Ocampo mine which he helped build and eventually was valued at US$750M. Again, quotes like these are only to be given weight if supported by elevated insider ownership and preferably insider open market purchases. I see both here.

There’s only 1 analyst following this. HC Wainwright that has a current price target of C$0.80/share. Note that this is based on a realized silver price of US$15/oz, gold price of U$1,300 and doesn’t ascribe any value to the Los Ricos project.

Conclusion

- I upped my stake in this company after their Cerro Colorado drill results. I’m comfortable here because of the following reasons:

- Management with proven track record and a lot of their own money in the company

- A producing asset which is seeing rising production and margins

- No need for financing so no dilution

- Big players have to buy in the market, which was confirmed by management

- Los Ricos could be a world class deposit

- Lots of catalysts nearby:

exploration results - promotion of Los Ricos

- rising earnings at ParrJonas De Roose

September 18, 2019

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.