The gold miners’ stocks continue to rally on balance, after a major upside breakout extended their strong upleg. That’s driving mounting interest in this recently-forsaken sector. With the latest quarterly earnings season underway, traders will soon enjoy big fundamental updates from the gold miners. They are likely to report good Q2 results, with improving operational performances supporting further stock-price gains.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the US Securities and Exchange Commission by 40 calendar days after quarter-ends. The gold miners generally release their quarterly reports in the latter half of that window. So Q2’19’s will arrive between late July to mid-August.

After spending decades intensely studying and actively trading this contrarian sector, there’s no gold-stock data I look forward to more than the miners’ quarterly financial and operational reports. They offer a true and clear snapshot of what’s really going on, shattering the misconceptions bred by ever-shifting winds of sentiment. Nearly all fundamental analysis is based off the data gold miners provide in quarterlies.

So for many years I’ve delved deeply into gold miners’ quarterly results. They are the dominant source of information I use to winnow down the universe of gold stocks to the fundamentally-superior ones with the greatest upside potential. Every quarter after their latest earnings season ends, I research and write essays discussing the newest results from the major gold miners, mid-tier gold miners, and silver miners.

Q2’19’s full analyses are coming starting in mid-August once that 40-day post-quarter reporting deadline has passed. But before that I eagerly dive into individual companies’ results as they’re reported, since there’s so much to digest. Even earlier soon after a quarter ends, I start thinking about what gold miners’ latest quarterly results are likely to show collectively. Their aggregate trends can be somewhat predicted.

In high-level fundamental terms, gold mining is a simple business. These companies painstakingly wrest gold from the bowels of the Earth, then generally sell all they can produce at prevailing market prices. So their profits are effectively the difference between current gold levels and operating costs. The former is easy to calculate once a quarter ends, and the latter can be reasonably estimated for this sector as a whole.

Gold’s dramatic bull-market breakout a month ago and high consolidation since have greatly improved sector psychology. But gold’s big surge came late in Q2, minimizing its full-quarter impact. The early quarter was rough, with gold slumping to a new year-to-date low near $1271 in early May. The average gold prices in April, May, and June were $1286, $1284, and $1361. Gold was mostly sucking wind last quarter.

Thus Q2’19’s overall average gold price of $1309 was just a meager 0.4% better than Q1’s $1303. So the gold miners’ latest quarterly results aren’t going to get much help from gold’s young surge. That will really change in the current Q3 if gold can hold these high levels. With Q3 about 1/5th over, gold has averaged an awesome $1407 so far! So the higher-gold boost to gold-stock earnings is coming, but not in Q2.

Gold stocks really leverage higher gold prices because their mining costs are largely fixed. Quarter after quarter mining operations generally require the same levels of infrastructure, equipment, and employees. The vast majority of any gold mine’s future cost structure is actually determined during its planning phase, when engineers decide which ore to mine, how to excavate it, and how to process it to recover the gold.

Every quarter after results I analyze the all-in-sustaining costs reported by the world’s gold miners. These are the best measure of what it really costs to produce an ounce of gold. Over the past four quarters, the major gold miners of the leading GDX VanEck Vectors Gold Miners ETF reported average AISCs of $856, $877, $889, and $893. That in turn yields a trailing-four-quarter mean of $879 per ounce, a key cost metric.

With $1309 average gold in Q2’19 and AISCs likely near $879, that implies the large gold miners as an industry likely earned $430 per ounce last quarter. That’s actually a decent improvement considering the flat quarterly gold prices. Though gold averaged a similar $1303 in Q1, the GDX miners’ average AISCs that quarter came in a bit higher at $893. That implied $410 profits, which Q2 results should easily exceed.

$430 is up 4.9% quarter-on-quarter despite the relatively-flat average gold price! This is really impressive sequential profits growth relative to the broader stock markets, where earnings are stalling out. But if that is all we could hope for, I would’ve written on a different topic this week. The gold miners’ Q2’19 earnings are likely to well exceed expectations for an entirely-different reason, portending even-higher gold-stock prices.

Most traders assume gold miners produce their yellow metal at fairly-steady rates year-round. That sure makes sense given how capital-intensive gold mining is, how individual mines’ capacities and throughputs to process ore are fixed, and how expanding mines’ outputs takes years of construction. But surprisingly global gold mine production actually varies considerably quarter-to-quarter! This should really boost Q2 earnings.

The best global gold fundamental data is published by the World Gold Council, also on a quarterly basis. These Gold Demand Trends reports are essential reading for all gold-stock speculators and investors, as these miners are ultimately just leveraged plays on gold. The latest GDT covering Q1’19 was released in early May, with Q2’s due out in early August. One key number GDTs report is world gold mine production.

That happened to run 852.4 metric tons in Q1, nearly a third of which came from the major gold miners of GDX. Analyzing global gold mine production each quarter since 2010 reveals some fascinating quarter-to-quarter output trends. Over the last 37 quarters, calendar Q1s have seen gold mined average a sharp 7.2% QoQ plunge from the immediately-preceding calendar Q4s! Not a single Q1 saw sequential output growth.

From 2010 to 2019 Q1 gold mined fell 7.2%, 6.9%, 7.6%, 11.2%, 8.8%, 3.3%, 8.7%, 5.7%, and 5.6% from the respective Q4s. These drops and their uniformity across radically-different gold-price environments is stunning. For some reason the world’s gold mines suffer universal declines in their outputs early in calendar years. Why? This curious industrywide Q1 production slump results from an interplay of several factors.

Most gold miners run their accounting on calendar years. So early in new years they have new capital budgets to spend on maintaining and enhancing their existing operations. If they temporarily shut down their mills for repairs or minor upgrades, Q1s are usually when they do it. Weather plays a role too, as the majority of the world’s gold mines are in the northern hemisphere with the majority of the world’s land masses.

Winter creates operational challenges for gold mines, ranging from extreme cold to heavy snow or rains depending on their latitudes and elevations. So in addition to short planned shutdowns to work on infrastructure, adverse weather can impair operational efficiencies. But the main reason global gold-mine outputs plunge in Q1s is due to ore-grade-management decisions made by mine managers to maximize bonuses.

Gold deposits are not homogeneous, ore grades vary widely within them. So managers must choose which ore to mine, when to run it through their mills, and how to mix it with ores from other locations. The mills that crush the gold-bearing rock into small-enough chunks to recover the metal have fixed capacities in tonnage-per-day terms. So the less gold contained in the ore processed, the less gold the mines recover.

Mine managers often choose to dig through lower-grade ores, or run lower-grade ores through their mills, in Q1s. They save the higher-grade ores for later in calendar years. They often claim these decisions are related to early-year capital budgets being spent to improve outputs later in years. But there’s probably more to it, since this happens so universally across the world’s gold mines. Incentives have to play a role.

Gold-mine managers are often partially compensated based on how their stock prices are faring. This is usually a big factor in annual bonuses calculated near year-ends. These bonuses are the most-variable part of compensation, and can greatly boost income. After long years of study and talking with some of these guys, I’m convinced they choose to take any gold-output hits early in years to engineer strong finishes.

Q1 results are reported by mid-Mays, a long way out from year-ends. That’s the least-beneficial time in bonus terms for strong output to boost stock prices. Q2 results released by mid-Augusts and Q3 results published by mid-Novembers are far-more important. So mine managers feed their fixed-capacity mills better-grade ore mixes in Q2s and Q3s, after early-year maintenance is finished and summer weather is favorable.

Thus in calendar Q2s since 2010, global gold mine output according to the World Gold Council surged an average of 5.4% sequentially from Q1s! Over the past 9 years Q2s have seen huge QoQ global-output gains of 6.7%, 7.7%, 6.3%, 7.1%, 6.1%, 5.7%, 0.7%, 4.9%, and 3.4%. There has not been a single down Q2 in this span despite wildly-different gold-price environments. Such uniformity reveals deliberate planning.

Over roughly the past decade, world gold mine production has averaged -7.2% QoQ in Q1s, +5.4% in Q2s, another hefty +5.3% in Q3s, then just +0.5% in Q4s. That Q4 stalling is pretty telling too, as those Q4 results are typically released by mid-Marches which doesn’t affect annual bonuses when those quarters were underway. The gold miners contrive their best output reporting from late Julies to mid-Novembers!

So in these upcoming Q2’19 results, the gold miners are likely to report production about 5% higher than Q1’s! That big sequential output boost really increases overall corporate earnings. And it has another key benefit of reducing all-in sustaining costs. AISCs are calculated by spreading the costs of gold mining across all ounces produced. So the more gold mined, the lower the unit costs of producing it that quarter.

A year ago in Q2’18, the GDX gold miners’ average AISCs dropped a big 3.2% sequentially from the prior quarter’s to $856 per ounce. So it is certainly reasonable to expect Q2’19’s AISCs to retreat 3% or so from Q1’s $893, which yields $866 per ounce. Subtract that from Q2’19’s average gold price of $1309, and it yields likely earnings of $443 per ounce. That is 8.0% higher quarter-on-quarter from Q1’s results!

That’s conservative too. As detailed in my essay on the GDX gold miners’ Q1’19 results, that quarter’s average AISCs were skewed higher by a single anomalous outlier. That company expects costs to greatly retreat in Q2. Excluding it, the GDX gold miners averaged considerably-lower $874 AISCs in Q1. A 3% reduction to that on higher Q2 output leaves an excellent $848 AISC target, implying big $461 profits!

That represents a major 12.4% quarter-on-quarter surge, which should excite traders anytime. And with gold-stock sentiment already growing far more bullish thanks to gold’s bull-market breakout, there’s a good chance Q2 earnings’ positive psychological impact will be amplified. As long as gold hangs in there and doesn’t sell off, the gold miners’ stocks have real potential to rally considerably on good Q2 results.

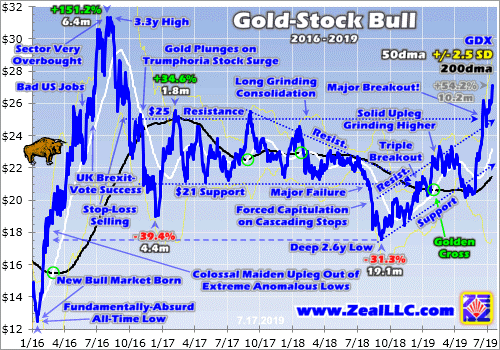

A couple charts offer some quick perspective. Gold’s breakout drove a major decisive upside breakout in gold stocks too as measured by their leading GDX benchmark. That dominant ETF is rendered in blue here, superimposed over its key technical lines. As of the Wednesday data cutoff for this essay, GDX had powered 54.2% higher in 10.2 months in its upleg to date. But gold-stock prices still remain relatively low.

Mid-week GDX hit $27.09 on close, its best levels in 2.8 years. But that remains well below gold stocks’ bull-to-date peak of $31.32 in early August 2016. The gold stocks ought to at least exceed those levels, which is another 15.6% higher from here. Good Q2 results interpreted through the lens of increasing sector bullishness should be enough to fuel a bull-market breakout. Gold argues for higher gold-stock levels.

Back in mid-2016 when GDX peaked at $31.32, gold merely hit $1365 at best. That was just after a quarter when the GDX gold miners’ AISCs averaged $886 per ounce. Gold was considerably higher this week, hitting $1425. And it has averaged $1408 for nearly a month since its bull-market breakout. So the higher prevailing gold prices this summer, and lower AISCs, should support much-higher gold-stock prices.

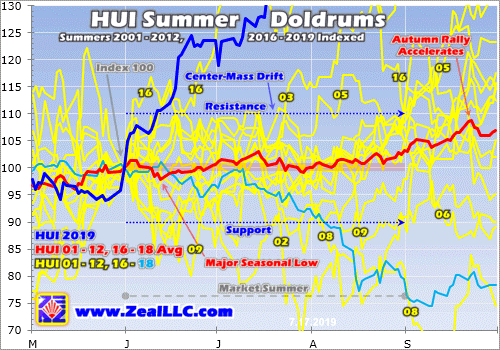

Showing just how strong gold stocks are and how unique today’s situation is, this last chart looks at gold stocks’ average performances in modern bull-market summers. I explained this indexed chart in depth in an essay on gold summer doldrums a couple weeks ago. The yellow lines show where the older HUI gold-stock index traded in past modern gold-bull-market summers, and the red line averages them together.

This year’s action is rendered in dark blue, revealing gold stocks’ best summer by far since 2016 after this gold bull’s massive maiden upleg! In the middle of this week the HUI rocketed 32.3% higher summer-to-date, literally off this seasonal chart I’ve gradually built up over the years. If there was ever a summer where gold stocks could punch out to new bull highs, this one is it. Their upside momentum is incredibly strong.

All this gold-stock bullishness aside, it is always wise to be wary when everyone else is getting excited. The potential for gold stocks to surge to new bull highs on good Q2 results is totally dependent on what gold does over the coming 6 weeks or so. While gold has shown awesome resilience in consolidating high and mostly holding $1400 over the past month, the gold selloff risk is high due to gold-futures positioning.

I wrote a whole essay last week explaining this in depth. In a nutshell, gold-futures speculators dominate short-term gold price action. Their current bets on gold are excessively-bullish, warning that their capital firepower to buy gold is nearing exhaustion. They are effectively all-in on long upside bets, and all-out on short downside bets. That leaves them vast room to sell hard on the right catalyst, pushing gold sharply lower.

There’s a chance new-high psychology can ignite enough investor gold buying to overpower and absorb any spec gold-futures selling. But realize gold-stock fortunes are still slaved to gold as always. Gold has to stay high to support new gold-stock highs. If gold materially falters and slumps into a healthy pullback or correction within an ongoing bull, the gold stocks will follow it lower regardless of how good Q2 results prove.

Buying high on strong upside momentum is always tempting, as that’s when traders feel the best about any sector. Bullishness and capital inflows soar as stocks power higher. But over time far-larger gains are won by instead buying low, adding positions when sectors are out of favor. The later you buy gold stocks in any upleg, the smaller their potential gains and the higher the odds a major selloff is looming.

To multiply your capital in the markets, you have to trade like a contrarian. That means buying low when few others are willing, so you can later sell high when few others can. In recent months well before gold’s breakout, we recommended buying many fundamentally-superior gold and silver miners in our popular weekly and monthly newsletters. Mid-week their unrealized gains ran as high as 123.9%, 123.5%, and 116.5%!

To profitably trade high-potential gold stocks, you need to stay informed about the broader market cycles that drive them. Our newsletters are a great way, easy to read and affordable. They draw on my vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today and take advantage of our 20%-off summer-doldrums sale! The biggest gains are won by traders diligently staying abreast so they can ride entire uplegs.

The bottom line is the gold miners’ just-starting Q2’19 earnings season should prove impressive. That’s no thanks to gold, as its awesome bull-market breakout came too late last quarter to push its average price significantly higher. But the gold miners are still likely to collectively report sharply-higher Q2 output, which is normal after Q1’s deep production slump. That will also naturally lead to proportionally-lower costs.

Growing production combined with lower costs at slightly-higher gold prices should yield big profits growth for the gold miners. Their Q2 results will be more closely watched and better received since psychology is shifting much more bullish in this sector. That should fuel big gold-stock buying as long as gold holds up. The yellow metal has proven resilient so far, but faces an ominous overhang of gold-futures selling pressure.

Adam Hamilton, CPA

July 22, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.