December 3, 2018

The junior gold miners’ stocks have spent recent months mostly languishing near major multi-year lows. That spawned a sentiment wasteland riddled by bearishness and bereft of bids. But these companies’ battered stock prices aren’t fundamentally righteous, as proven yet again by their latest earnings season. Faring far better in a challenging third quarter than stock prices imply, they need to mean revert way higher.

Four times a year publicly-traded companies release treasure troves of valuable information in the form of quarterly reports. Companies trading in the States are required to file 10-Qs with the U.S. Securities and Exchange Commission by 40 calendar days after quarter-ends. Canadian companies have similar requirements at 45 days. In other countries with half-year reporting, many companies still partially report quarterly.

The definitive list of elite “junior” gold stocks to analyze comes from the world’s most-popular junior-gold-stock investment vehicle. Mid-month the GDXJ VanEck Vectors Junior Gold Miners ETF reported $4.1b in net assets. Among all gold-stock ETFs, that was second only to GDX’s $9.0b. That is GDXJ’s big-brother ETF that includes larger major gold miners. GDXJ’s popularity testifies to the great allure of juniors.

Unfortunately this fame created serious problems for GDXJ a couple years ago, resulting in a stealthy major mission change. This ETF is quite literally the victim of its own success. GDXJ grew so large in the first half of 2016 as gold stocks soared in a massive upleg that it risked running afoul of Canadian securities laws. And most of the world’s smaller gold miners and explorers trade on Canadian stock exchanges.

Since Canada is the centre of the junior-gold universe, any ETF seeking to own this sector will have to be heavily invested there. But once any investor including an ETF buys up a 20%+ stake in any Canadian stock, it is legally deemed to be a takeover offer that must be extended to all shareholders! As capital flooded into GDXJ in 2016 to gain junior-gold exposure, its ownership in smaller components soared near 20%.

Obviously hundreds of thousands of investors buying shares in an ETF have no intention of taking over gold-mining companies, no matter how big their collective stakes. That’s a totally-different scenario than a single corporate investor buying 20%+. GDXJ’s managers should’ve lobbied Canadian regulators and lawmakers to exempt ETFs from that 20% takeover rule. But instead they chose an inferior, easier fix.

Since GDXJ’s issuer controls the junior-gold-stock index underlying its ETF, it simply chose to unilaterally redefine what junior gold miners are. It rejiggered its index to fill GDXJ’s ranks with larger mid-tier gold miners, while greatly demoting true smaller junior gold miners in terms of their ETF weightings. This controversial move defying long decades of convention was done quietly behind the scenes to avoid backlash.

There’s no formal definition of a junior gold miner, which gives cover to GDXJ’s managers pushing the limits. Major gold miners are generally those that produce over 1m ounces of gold annually. For decades juniors were considered to be sub-200k-ounce producers. So 300k ounces per year is a very-generous threshold. Anything between 300k to 1m ounces annually is in the mid-tier realm, where GDXJ now traffics.

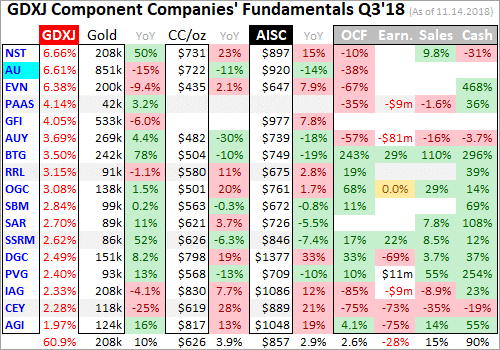

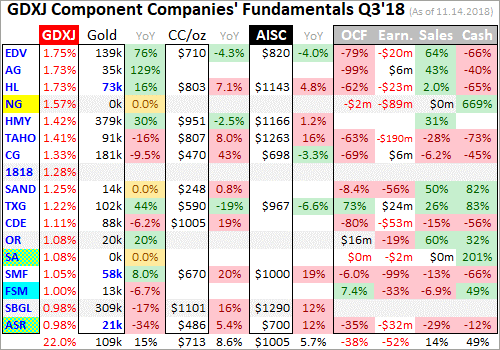

That high 300k-ounce-per-year junior cutoff translates into 75k ounces per quarter. Following the end of the gold miners’ Q3’18 earnings season in mid-November, I dug into the top 34 GDXJ components’ results. That’s simply an arbitrary number that fits neatly into the tables below. Although GDXJ included a staggering 70 component stocks mid-month, the top 34 accounted for a commanding 82.9% of its total weighting.

Out of these top 34 GDXJ companies, only 3 primary gold miners met that sub-75k-ounce-per-quarter qualification to be a junior gold miner! Their quarterly production is rendered in blue below, and they collectively accounted for just 3.8% of this ETF’s total weighting. GDXJ is inarguably now a pure mid-tier gold-miner ETF, not a junior one. But its holdings include the world’s best gold miners with huge upside potential.

I’ve been doing these deep quarterly dives into GDXJ’s top components for years now. In Q3 2018, fully 31 of the top 34 GDXJ components were also GDX components! These are separate and distinct ETFs, a “Gold Miners ETF” and a “Junior Gold Miners ETF”. So they shouldn’t have to own many of the same companies. In the tables below I highlighted the symbols of rare GDXJ components not also in GDX in yellow.

These 31 GDX components accounted for 79.2% of GDXJ’s total weighting, not just its top 34. They also represented 31.7% of GDX’s total weighting. Thus nearly 4/5ths of this “Junior Gold Miners ETF” is made up by nearly 1/3rd of the major “Gold Miners ETF”! These GDXJ components also in GDX are clustered from the 11th- to 30th-highest weightings in that latter larger ETF. GDXJ is mostly smaller GDX stocks.

In a welcome change from GDXJ’s vast component turmoil of recent years, only 4 of its top 34 stocks are new since Q3 2017. Their symbols are highlighted in light blue below. Thus the top GDXJ components’ collective results are finally getting comparable again in year-over-year terms. Analyzing ETFs is much easier if their larger components aren’t constantly in flux. Hopefully changes going forward are relatively minor.

Despite all this, GDXJ remains the leading “junior-gold” benchmark. So every quarter I wade through tons of data from its top components’ latest results, and dump it into a big spreadsheet for analysis. The highlights make it into these tables. Most of these top 34 GDXJ gold miners trade in the US and Canada, where comprehensive quarterly reporting is required by regulators. But others trade in Australia and the UK.

In these countries and most of the rest of the world, regulators only mandate that companies report their results in half-year increments. Most do still issue quarterly production reports, but don’t release financial statements. There are wide variations in reporting styles, data presented, and release timing. So blank fields in these tables mean a company hadn’t reported that particular data for Q3 2018 as of mid-November.

The first couple columns of these tables show each GDXJ component’s symbol and weighting within this ETF as of mid-November. While just over half of these stocks trade on US exchanges, the other symbols are listings from companies’ primary foreign stock exchanges. That’s followed by each gold miner’s Q3’18 production in ounces, which is mostly in pure-gold terms excluding byproduct metals often found in gold ore.

Those are usually silver and base metals like copper, which are valuable. They are sold to offset some of the considerable costs of gold mining, lowering per-ounce costs and thus raising overall profitability. In cases where companies didn’t separate out gold and lumped all production into gold-equivalent ounces, those GEOs are included instead. Then production’s absolute year-over-year change from Q3’17 is shown.

Next comes gold miners’ most-important fundamental data for investors, cash costs and all-in sustaining costs per ounce mined. The latter directly drives profitability which ultimately determines stock prices. These key costs are also followed by YoY changes. Last but not least the annual changes are shown in operating cash flows generated, hard GAAP earnings, sales, and cash on hand with a couple exceptions.

Percentage changes aren’t relevant or meaningful if data shifted from positive to negative or vice versa, or if derived from two negative numbers. So in those cases I included raw underlying data rather than weird or misleading percentage changes. This whole dataset together offers a fantastic high-level read on how the mid-tier gold miners as an industry are faring fundamentally. They actually did relatively well in Q3.

While this new mid-tier GDXJ is generally excellent, some decisions by its managers are utterly baffling. Out of all the world’s gold miners they could’ve added over this past year, they inexplicably decided on the giant largely-African AngloGold Ashanti. It produced an enormous 851k ounces of gold last quarter, the largest in GDXJ by far. It and the rest of the South African majors definitely don’t belong in GDXJ!

Remember that major-gold-miner threshold has long been 1m+ ounces per year. AU’s production is annualizing to well over 3x that, making this company the world’s 3rd-largest gold miner last quarter. Why on earth would managers running a “Junior Gold Miners ETF” even consider AngloGold Ashanti? It is as far from junior-dom as gold miners get. The same is true with the rest of the troubled South African gold miners.

AU, Gold Fields, Harmony Gold, and Sibanye-Stillwater mined 851k, 533k, 379k, and 309k ounces in Q3’18, all are majors. Yet they accounted for 13.1% of GDXJ’s total weighting. They are riddled with all kinds of problems too, from shrinking production to high costs to increasing stealth expropriations from South Africa’s openly-Marxist anti-white-investor government. Their inclusion heavily skews and taints GDXJ.

These South African majors’ Q3 production of 2.1m ounces was a whopping 41% of the GDXJ top 34’s total! And it still fell 7.0% YoY due to South Africa’s tragic death spiral. Excluding them and the amazing Kirkland Lake Gold which has grown so fast it was moved exclusively into GDX over this past year, the rest of the GDXJ top 34 grew production 3.4% YoY in Q3. The South African majors’ cost impact is even worse.

Mining in that country is very expensive thanks to very-old very-deep mines and endless new government interference via stifling regulations. In Q3 the South African majors’ cash and all-in sustaining costs came in really high averaging $925 and $1088 per ounce. The rest of GDXJ’s top 34 averaged $629 and $877, a massive 32.0% and 19.4% lower! The South African majors are really retarding GDXJ’s performance.

As struggling majors far larger than mid-tiers and juniors, they need to get kicked out of GDXJ posthaste. They can be left in GDX where they belong. AU effectively took KL’s place, which makes no sense at all fundamentally. Kirkland Lake produced 180k ounces of gold in Q3 at $351 cash costs and $645 AISCs. So unlike AU, KL remains solidly in the mid-tier realm and has been performing incredibly well operationally.

While GDXJ’s managers really dropped the ball including those South African majors, they deserve big praise for upping the weighting of the outstanding Australian miners. They are Northern Star Resources, Evolution Mining, Regis Resources, St Barbara, and Saracen Mineral. Their collective weighting in GDXJ grew to 21.7% at the end of Q3’s earnings season, nearly 2/3rds higher from their 13.3% a year earlier.

Unlike AU’s dumbfounding inclusion, the Australians’ rise is well-deserved. Their production surged 8.9% YoY to 686k ounces, or 23% of the GDXJ top 34’s total excluding those South African majors. And the Australian miners are masters at developing great gold deposits and controlling costs, as their cash costs and AISCs in Q3 averaged just $586 and $724! It’s fantastic GDXJ offers American investors this Aussie exposure.

GDXJ’s component list and weightings are a work in progress, and are gradually getting better. For years I’ve pointed out things like the South African majors that weren’t right, and GDXJ’s managers eventually seem to come around and change things for the better. Greatly helping that process is investors buying the better individual stocks like KL and shunning laggards like AU, readjusting their relative market capitalizations.

GDXJ and GDX are essentially market-cap weighted, with larger companies rightfully commanding larger weightings. These leading gold-stock ETFs’ managers can override this by deciding which gold miners to include in each ETF. So they can easily purge GDXJ of the deteriorating South African majors and add real mid-tier gold miners. But the true core problem is having so many of the same stocks in GDX and GDXJ.

Such massive overlap between these two ETFs is a huge lost opportunity for VanEck. It owns and manages GDX, GDXJ, and even the MVIS indexing company that decides exactly which gold stocks are included in each. With one company in total control, there’s no need for any overlap in the underlying companies of what should be two very-different gold-stock ETFs. Inclusion ought to be mutually-exclusive.

VanEck could greatly increase the utility of its gold-stock ETFs and thus their ultimate success by starting with one big combined list of the world’s better gold miners. Then it could take the top 20 or 25 in terms of annual gold production and assign them to GDX. Based on Q3’18 production, that would run down near 139k or 93k ounces per quarter. Then the next-largest 40 or 50 gold miners could be assigned to GDXJ.

Getting smaller gold miners back into GDXJ would be a huge boon for the junior-gold-mining industry. Most investors naturally assume this “Junior Gold Miners ETF” owns junior gold miners, which is where they are trying to allocate their capital. But since most of GDXJ’s funds are instead diverted into much-larger mid-tiers and even some majors, the juniors are effectively being starved of capital intended for them.

That’s one of the big reasons smaller gold miners’ stock prices are so darned low. They aren’t getting enough capital inflows from gold-stock-ETF investing. So their share prices aren’t bid higher. They rely on issuing shares to finance their exploration projects and mine builds. But when their stock prices are down in the dumps, that is heavily dilutive. So GDXJ is strangling the very industry its investors want to own!

Back to these mid-tier gold miners’ Q3’18 results, production is the best place to start since that is the lifeblood of the entire gold-mining industry. These top 34 GDXJ gold miners that had specifically reported Q3 production as of mid-November produced 5063k ounces. That surged by a massive 18.8% YoY, implying these miners are thriving. But that is heavily distorted by that huge 851k-ounce boost from AU’s addition.

Without the world’s 3rd-largest gold miner, the rest of the GDXJ top 34 saw their production slip 1.2% YoY to 4212k ounces. That reflected the peak-gold challenges the gold-mining industry is facing, as I discussed a couple weeks ago while reviewing the GDX majors’ Q3’18 results. The GDXJ top 34 are still outperforming the GDX top 34, which saw their gold production retreat 2.9% YoY in Q3 bucking historical trends.

Sequentially quarter-on-quarter from Q2’18 the GDXJ top 34’s production surged a dramatic 13.3%! And AU was already one of GDXJ’s top components then. That partially came from new mines ramping up at the world’s best mid-tier gold miners. It is far easier for them to grow production off lower bases than it is for the majors off high bases. That’s a key reason why the mid-tiers’ upside potential trounces that of the majors.

For all GDXJ’s faults, it does still offer investors exposure to much-smaller gold miners. The average quarterly production of all the top 34 GDXJ miners reporting it in Q3 was 163.3k ounces. That is 43% smaller than the 288.8k averaged by the top 34 GDX miners last quarter. And again AU’s crazy inclusion really skews this. Ex-AU, the GDXJ average falls to 140.4k. Without all the South African majors, it is 110.8k.

These annualize to 562k and 443k, both solidly in the mid-tier realm. Analyzing GDXJ’s production and costs requires breaking out those heavily-distorting South African majors that have no place in a mid-tier gold-miner ETF. Again their production fell 7.0% YoY in Q3, while the rest of the GDXJ top 34’s ex-KL grew 3.4%! Production and costs tend to be proportionally inversely related because of how mining works.

Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. The tonnage throughputs of the mills that process the gold-bearing ore are also fixed. So gold produced varies with ore grades each quarter. The more gold that is recovered, the more ounces to spread gold mining’s big fixed costs across. That lowers per-ounce costs.

There are two major ways to measure gold-mining costs, classic cash costs per ounce and the superior all-in sustaining costs per ounce. Both are useful metrics. Cash costs are the acid test of gold-miner survivability in lower-gold-price environments, revealing the worst-case gold levels necessary to keep the mines running. All-in sustaining costs show where gold needs to trade to maintain current mining tempos indefinitely.

Cash costs naturally encompass all cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. In Q3’18, the overall cash costs of the GDXJ top 34 surged 8.4% higher YoY to $663 per ounce. That was still largely in line with the past four quarters’ $612, $618, $692, and $631 averaging $638.

But that sharp jump was mostly the result of the South African majors’ deepening troubles. Again their average cash costs last quarter were a whopping $925! Without them, the rest of the GDXJ top 34 averaged $629 per ounce which was only up 2.8% YoY and below the rolling-four-quarter mean. So the mid-tier gold miners of GDXJ are holding the line on cash costs, a sign their operations are fundamentally sound.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it really costs to maintain gold mines as ongoing concerns. AISCs include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current gold-production levels.

These additional expenses include exploration for new gold to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administration expenses necessary to oversee gold mines. All-in sustaining costs are the most-important gold-mining cost metric by far for investors, revealing gold miners’ true operating profitability.

The GDXJ top 34 reported average AISCs of $911 in Q3, up 3.8% YoY. But like cash costs, this was roughly in line with the $877, $855, $923, and $886 seen in the past four quarters. But again that was skewed quite a bit higher by those wrongly-included South African majors, which reported $1088 average AISCs in Q3. The rest of the top 34 averaged $877, which is actually better than the $885 four-quarter average.

So the South African majors are really tainting GDXJ’s collective operational performance, with lower production and higher costs dragging down this entire ETF. Those giant struggling gold producers are an albatross around the neck of the many great mid-tier gold miners in GDXJ! If you are a GDXJ investor, contact VanEck and urge them to boot the South African majors out of GDXJ to help it thrive going forward.

Gold-mining earnings are simply the difference between prevailing gold prices and all-in sustaining costs. And both sides of this equation moved the wrong way in Q3, squeezing the mid-tier gold miners’ profits. Q3’18’s average gold price of $1211 was 5.3% lower than Q3’17’s. And with overall GDXJ top 34 AISCs 3.8% higher at $911, that really cut into margins. These gold miners were collectively earning $300 per ounce.

That implied solid 25% profit margins absolutely, which aren’t bad. But they still plunged 25.4% YoY from Q3’17’s $402 per ounce, which amplified gold’s decline by 4.8x. But gold-mining profits leverage to gold is exactly why the gold stocks make such compelling investments. Gold stocks were weak in Q3 because gold was pounded to a deep 19.3-month low in mid-August on extreme all-time-record gold-futures short selling.

Left for dead and neglected, the gold miners’ stocks are the last cheap sector in these lofty bubble-valued stock markets. Their fundamental upside as gold mean reverts higher on speculators’ gold-futures buying and new investment demand as stock markets roll over is enormous. This is easy to understand with a simple example. In the last four quarters including Q3’18, the top 34 GDXJ gold miners’ AISCs averaged $894.

During gold’s last major upleg in essentially the first half of 2016, it powered about 30% higher driven by surging investment demand after stock markets suffered back-to-back corrections. That was even small by historical gold-bull-upleg standards. If we merely get another 30% gold advance from its recent mid-August low of $1174, we’re looking at $1525 gold. That would work wonders for gold-mining profits and stock prices.

At $1525 gold and $894 AISCs, the mid-tier gold miners would be earning $631 per ounce. That’s 110% higher than Q3’18’s $300! If gold-mining profits double, gold-stock prices will soar. Indeed during that last 30% gold bull in the first half of 2016, GDXJ rocketed 203% higher! So the gold-stock outlook is wildly bullish with gold itself due to power higher as the stock markets roll over on the Fed’s record tightening.

The rest of the top 34 GDXJ gold miners’ fundamentals were mixed last quarter. Cash flows generated from operations totaled $1.3b in Q3, down 21.2% YoY. That’s reasonable given average gold’s 5.3% YoY retreat and their leverage to it. Cash on hand remained high at $5.4b, down just 5.3% YoY. So these mid-tier gold miners have plenty of capital to build and buy new mines to continue growing their production.

Revenues only slipped 0.4% YoY to $4.1b, which means the softer gold prices were largely offset by higher production. But GAAP profits looked like a disaster, with the GDXJ top 34’s plummeting to a $379m loss in Q3’18 from being $212m in the black in Q3’17! That was far worse than the lower gold prices warranted, but thankfully it was mostly the result of big non-cash charges flushed through income statements.

Tahoe Resources reported a massive $170m impairment charge on its suspended Escobal silver mine that is being held hostage by the corrupt Guatemalan government. Yamana Gold wrote off $89m after selling a mine in Argentina. Explorer NOVAGOLD reported an $81m loss from discontinued operations on the sale of one of its projects. These three unusual items alone wiped out $340m of profits from GDXJ’s ranks.

Without them, the top 34 GDXJ gold miners’ earnings would’ve fallen to -$39m from +$212m. That isn’t great, but it doesn’t reveal any serious issues a rising gold price won’t quickly solve. Interestingly if KL was still included instead of AU, that would’ve added another $56m in Q3’18 profits. The mid-tiers’ overall earnings should dramatically leverage and outpace gold in coming quarters as it inexorably mean reverts higher.

While GDXJ should certainly no longer be advertised as a “Junior Gold Miners ETF”, it offers exposure to some of the best mid-tier gold miners on the planet. It’s really growing on me, I like this new GDXJ way better than GDX. That being said, GDXJ is still burdened by overdiversification and way too many gold miners that shouldn’t be in there. They are either too large, are saddled with inferior fundamentals, or both.

So the best way to play the gold miners’ coming massive mean-reversion bull is in individual stocks with superior fundamentals. Their gains will ultimately trounce the major ETFs like GDXJ and GDX. There’s no doubt carefully-handpicked portfolios of elite gold and silver miners will generate much-greater wealth creation. GDXJ’s component list is a great starting point, but pruning it way down offers far-bigger upside.

The key to riding any gold-stock bull to multiplying your fortune is staying informed, both about broader markets and individual stocks. That’s long been our specialty at Zeal. My decades of experience both intensely studying the markets and actively trading them as a contrarian is priceless and impossible to replicate. I share my vast experience, knowledge, wisdom, and ongoing research through our popular newsletters.

Published weekly and monthly, they explain what’s going on in the markets, why, and how to trade them with specific stocks. They are a great way to stay abreast, easy to read and affordable. Walking the contrarian walk is very profitable. As of Q3, we’ve recommended and realized 1045 newsletter stock trades since 2001. Their average annualized realized gains including all losers is +17.7%! That’s double the long-term stock-market average. Subscribe today and take advantage of our 20%-off holidays sale!

The bottom line is the mid-tier gold miners reported solid fundamentals despite a challenging third quarter for gold prices. Excluding the South African majors, they were able to grow their production nicely while holding the line on costs. That portends dramatic operating-cash-flow and earnings growth in the coming quarters as gold mean reverts higher on big investment buying. The mid-tier gold miners’ stocks will soar on that.

Gold stocks are not only unloved and dirt-cheap today, but they are a rare sector that rallies strongly with gold as general stock markets weaken. While virtually no one was interested in these leveraged plays on gold upside in recent months, that will change fast as these lofty stock markets roll over. And the mid-tier gold miners’ recent Q3 earnings season proved they remain ready to fundamentally amplify gold’s gains.

Adam Hamilton, CPA

Copyright 2000 – 2018 Zeal LLC (www.ZealLLC.com)

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.