The world’s two biggest gold miners both announced mega-mergers over the past 5 months or so. These huge deals briefly garnered some interest in the usually-forgotten gold-stock sector, and fleeting praise from Wall Street analysts. But gold-stock mega-mergers are bad news for gold-miner shareholders on all sides. They reveal the serious struggles of major gold miners, and really retard future upside in their stocks.

For decades the largest gold miners in the world have been Newmont Mining (NEM) and Barrick Gold (ABX). These behemoths have long dwarfed all their peers in operational scope. While the gold miners are in the process of reporting Q4’18 results now, their latest complete set remains Q3’18’s. As after every quarterly earnings season, I analyzed them in depth for the major gold miners of GDX back in mid-November.

The GDX VanEck Vectors Gold Miners ETF is the world’s leading and dominant gold-stock investment vehicle. In Q3 alone NEM and ABX mined a staggering 1286k and 1149k ounces of gold! To put this in perspective, the average of the next 8 largest gold miners rounding out the top 10 was just 508k ounces. Newmont and Barrick have long been in a league of their own, with commensurate market capitalizations.

In mid-November NEM and ABX were worth $17.1b and $14.9b, granting them massive 11.0% and 9.5% weightings within GDX. These two gold giants alone accounted for over 1/5th of GDX! That gives them outsized influence in not only that ETF, but in the entire gold-stock sector. GDX is the sector benchmark of choice for gold stocks these days, so the fortunes of NEM and ABX stocks really affect overall performance.

Gold-mining stocks are generally divided into three tiers based on their production. Anything over 1000k ounces annually is considered a major, which works out to 250k per quarter. NEM and ABX produced so much gold in Q3 they exceeded this threshold by a colossal 5.1x and 4.6x! They are really super-majors. Mid-tier gold miners produce between 300k to 1000k ounces every year, while juniors are under 300k.

Back on September 24th, 2018, Barrick Gold shocked the gold-stock world. It announced it was merging with Randgold (GOLD), which was really an all-stock acquisition of GOLD by ABX worth $6.5b. Barrick shareholders would own 2/3rds of the new combined company, while Randgold’s would own the rest. To avoid confusion, this essay uses the classic ABX and GOLD stock symbols to represent Barrick and Randgold.

ABX had been Barrick’s ticker for decades, but was just recently abandoned on January 2nd. With this mega-merger finished, the new company took over the excellent GOLD symbol going forward. That is a wise decision, as anyone who types “gold” into any brokerage account will see Barrick Gold. Years ago before Randgold got that coveted symbol, another major miner had it and really seemed to benefit from it.

In Q3 Randgold was the 10th-largest gold miner in the world producing 309k ounces. Added on top of Barrick’s 1149k, the new combined 1458k would take back the top-gold-miner crown from Newmont which produced 1286k that quarter. Apparently size matters a lot when you’re a gold-mining executive. But with both ABX and GOLD suffering chronic declining production, that mega-merger reeked of desperation.

Newmont’s leadership wasn’t happy with losing the pole position among global gold miners. So it soon got to work on looking for a mega-merger of its own. On January 14th, NEM announced it was acquiring major miner Goldcorp (GG) in an all-stock deal worth $10.0b! That looked like one-upmanship taking it to Barrick. NEM and GG shareholders would own about 2/3rds and 1/3rd of the new combined colossus.

Goldcorp was the world’s 7th-largest gold miner in Q3’18, producing 503k ounces of gold. Added on to Newmont’s 1286k, that creates a new monster running at an unprecedented 1789k-ounce quarterly rate! If bigger is better, these new combined super-major gold miners ought to be the best seen in history. But unfortunately in gold mining that isn’t true, and these new giants will likely fare worse than if they hadn’t merged.

In their merger announcements, the CEOs of all 4 of these major gold miners tried hard to sell their deals as wonderful news for shareholders. They argued that synergies and cost savings would make these new combined titans more effective at producing superior returns for their shareholders going forward. And as always with any large merger, Wall Street analysts universally applauded these mega-mergers as good.

Sadly the opposite is likely true, these deals are bad news for all the owners of Newmont and Barrick as well as former owners of Goldcorp and Randgold. These new giant super-majors are even bad news for the gold-mining sector as a whole. The odds are really high that their stocks will really underperform the smaller major, mid-tier, and junior gold miners in coming years. That will hurt this entire sector on multiple fronts.

Contrary to their CEOs’ marketing propaganda, none of these four major gold miners approached these deals from positions of strength. They’ve all been struggling with weakening production and rising costs. Gold mines are wasting assets that are constantly depleting, and it is increasingly challenging to find new gold to mine economically at the scale and pace the majors need. These mergers didn’t solve that core problem!

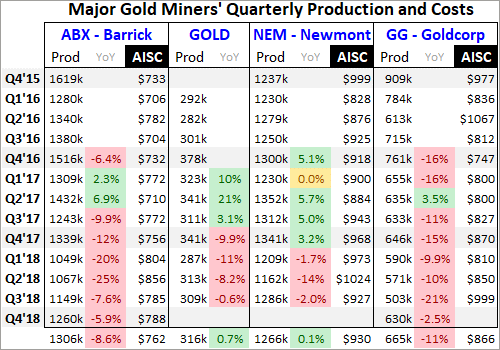

This table looks at the quarterly production, its year-over-year change, and all-in sustaining costs per ounce mined of Barrick, Randgold, Newmont, and Goldcorp during today’s secular gold bull. It started in late Q4’15 out of deep 6.1-year secular lows in gold. Barrick deleted Randgold’s old website, so there is no Q4’15 GOLD data. And as of Wednesday afternoon NEM and GG hadn’t yet reported full Q4’18 results.

Barrick and Newmont didn’t just effectively dilute their shareholders by 50% for some relatively-meager cost-saving synergies, but because they can’t grow their production internally. ABX’s gold mined each quarter has been falling sharply on balance for years! It has seen brutal YoY drops as high as 25.5%, which ought to be impossible for a world-class gold major. 7 of the last 9 quarters have seen big declines.

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses.

And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost for its first four quarters as a merged company, and then waning production will again be unmasked.

While the new giant Barrick will have more capital to develop new gold mines and expand existing ones, it seems unlikely that will be enough to turn this super-major around. Barrick and Randgold operated about 12 and 4 gold mines respectively pre-merger. So bringing another few online in coming years might not move the needle enough to outpace depletion. And it takes over a decade to permit and build new mines.

The entire gold-mining industry has been greatly starved of capital largely since 2013, with 2016 being a modest exception. Thus the big investments necessary to find new large-scale gold deposits and slowly advance them to mine builds have been severely lacking. So this whole industry’s pipeline of new gold to mine has been crippled, all but pinched shut. Declining miners merging does little to solve this problem.

Newmont has fared way better than Barrick in recent years, actually enjoying strong production growth on balance from Q4’16 to Q4’17. But this past year even mighty NEM has started to suffer from waning gold production. It averaged 5.9% YoY declines in the first three quarters of 2018. I suspect NEM is just a little behind ABX in rolling over into depletion outpacing mining growth. ABX’s merger forced NEM to act.

While Goldcorp was long celebrated as the world’s best major gold miner, it has been struggling for years with slowing production. Over the last 9 quarters GG only saw one modest production gain, with its gold mined dropping a colossal 11.0% YoY each quarter on average! So although GG produces about twice as much gold as Randgold, it might be a worse acquisition target due to its faster pace of shrinking production.

Like ABX and GOLD, it’s hard to imagine combining two more weakening majors NEM and GG will yield a way to stop and reverse their falling production. Again for their first four quarters together this new giant Newmont will appear to see big annual production growth. But once that post-merger comparison rolls past, the declining gold across all its mines will again be revealed. Mega-mergers can’t negate mine depletion.

Randgold didn’t even bother reporting industry-standard all-in sustaining costs, which is why they’re not included above. But its cash costs were often on the high side, so it’s likely the new combined company will drag overall mining costs higher. Barrick’s major-leading low AISCs aren’t likely to last with GOLD’s mines thrown in the mix, which means higher costs and lower overall profitability for Barrick going forward.

Newmont should benefit more from Goldcorp’s lower cost structure. NEM averaged $975 AISCs in the first three quarters of 2018, way higher than the $877 average in Q3’18 among the GDX gold miners. GG’s AISCs averaged $886 over that 9-month span, so the new combined Newmont should benefit from lower costs. But that may not last long, as weakening production eventually pushes per-ounce costs higher.

Gold-mining costs are largely fixed quarter after quarter, with actual mining requiring the same levels of infrastructure, equipment, and employees. So slowing production yields fewer ounces to spread mining’s big fixed costs across. If these new super-major gold behemoths can’t arrest their depleting production, their costs will inevitably rise in the future hurting profitability. Again these mega-mergers didn’t solve that problem.

So it looks like the managements of Barrick and Newmont just issued $6.5b and $10.0b of new stock so they could report big merger-driven production surges for a single year! Once those pre- and post-merger year-over-year comparisons pass, the vexing waning-production problems at all four of these predecessor gold miners will again become apparent. But that’s not even the biggest reason these mergers are bad news!

Even before these mergers as apparent in mid-November when I analyzed Q3’18 results, both Newmont and Barrick already had very-large market capitalizations of $17.1b and $14.9b. That again granted them massive 11.0% and 9.5% weightings in GDX. Like most stock indexes and ETFs, GDX’s components are weighted by market cap. Goldcorp and Randgold ranked 6th and 7th then in market cap and weightings.

Adding NEM and GG together as of mid-November would catapult their market cap and GDX weighting to $25.1b and 16.0%. Adding ABX and GOLD together yields a similar $22.3b market cap and 14.5% total GDX weighting. So these two super-majors alone could account for a crazy 30.5% of GDX’s weighting! That is almost scarily concentrated, although we don’t yet know how GDX’s managers will deal with this.

As of this week the new combined Barrick only has an 11.1% GDX weighting, while Newmont is at 8.2% since its mega-merger is not yet consummated. It will be interesting to see whether the new companies’ weightings going forward are kept in market-cap proportion or somehow limited. I hope it’s the latter, as many of the other gold miners in GDX have far-better growth prospects than these new super-majors.

ETF weightings aside, higher market caps create plenty of problems of their own. I’ve written essays in the past on picking great gold stocks, and surprisingly market capitalization is the single most important factor for future gains. The gold stocks with the largest market caps usually significantly underperform their smaller peers. These new super-majors are so darned big that they really compound this problem.

In mid-November when I analyzed the GDX miners’ Q3’18 results, the average market cap of its top 34 component stocks was $4.3b. Excluding NEM and ABX, that fell to $3.5b. It takes proportionally more capital inflows, investors buying shares, to push a larger stock higher than a smaller one. If the super-majors are worth $24b, it takes 6x as much buying of their stocks to drive the same gains as on a $4b company!

Imagine the different forces involved turning a supertanker versus a tugboat. The bigger any stock in the stock markets, the more inertia it has and thus the more capital is needed to overcome that and move the stock. And market-cap issues are not just a size thing in gold stocks. Smaller major, mid-tier, and junior gold miners have way fewer gold mines and much-lower production, which makes it far easier to grow output.

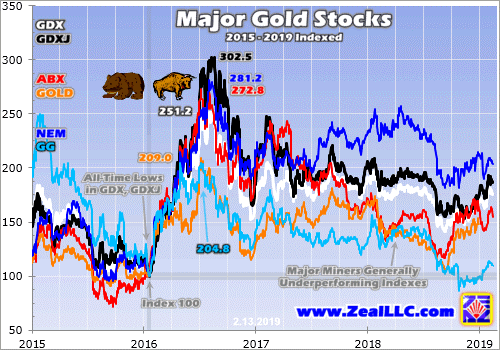

While Newmont is a temporary exception since it was bucking the major trend and growing production in 2017, Barrick, Randgold, and Goldcorp all really underperformed their sector in recent years. This chart looks at the indexed performance in ABX, GOLD, NEM, and GG stocks compared to the leading sector ETFs of GDX and the smaller GDXJ which largely tracks mid-tier gold miners under 1m ounces annually.

Both GDX and GDXJ fell to all-time lows back in mid-January 2016 when this gold-stock bull was born. So all 6 stocks are indexed to 100 as of that day, revealing their relative performance since. Despite their heavy weighting in GDX, the major gold miners generally lag their key sector benchmarks. ABX, GOLD, and GG have really struggled in recent years as their managers failed to stem big production declines.

This chart is pretty damning, showing why the managers of Barrick and Newmont are desperate to show rising production even if only for a year after their wildly-expensive mega-mergers. ABX and GOLD have both been really underperforming their peers, scaring investors away while putting serious pressure on managements to turn things around. NEM resisted that, but its production started to decline too in 2018.

And GG has been a basket case, actually managing to fall below its deep secular lows of early 2016 in recent months! That’s a sad fate for what was the world’s best major gold miner for many years. NEM buying this dog is likely to drag down NEM’s stock performance to some midpoint between what it has done and how GG has fared. For the most part the largest gold miners haven’t been good investments.

The much-larger market caps coming from combining struggling majors into super-majors is highly likely to exacerbate this underperformance trend. The new Newmont and Barrick are way bigger and far more ponderous, and will require a lot more share buying to move their stock prices materially higher. But why will most investors even bother to buy these titans when many smaller mid-tier gold miners are thriving?

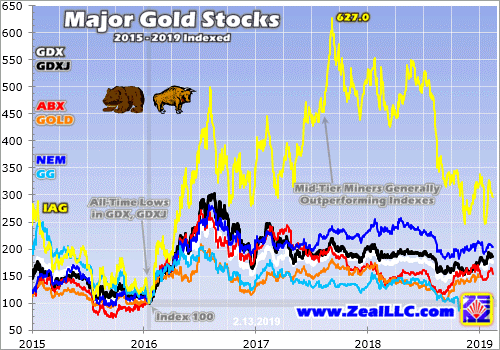

This next chart adds a single additional mid-tier gold miner to illustrate their outperformance. I chose IAMGOLD (IAG) for this example for a couple reasons. It produced 882k ounces in all of 2018, which makes it a larger mid-tier gold miner nearing that 1000k+ major threshold. And IAG is unremarkable fundamentally. It mined the same 882k ounces in 2017, so there was no production growth at all last year.

And its 2018 all-in sustaining costs are expected to come in on the high side near $1070 per ounce, which is worse than most of the majors. So there’s really nothing special about IAG operationally suggesting it should far outperform. If I wanted to cherry pick, there are other mid-tier miners that have trounced what IAG has done in recent years. Yet even IAG wildly outperformed the majors and sector ETFs during this gold bull.

If Newmont and Barrick were the only gold-mining stocks, they’d certainly be worth owning during a secular gold bull. But why own these massive supertanker-like gold miners when smaller major, mid-tier, and junior gold miners’ stocks are performing way better? The smaller miners not only have lower market caps easier to bid higher with much-smaller capital inflows, but plenty also have superior fundamentals.

They tend to have just a few or less gold mines, making it much easier to grow production by expanding existing mines or building new ones. Those expansion events act as major psychological catalysts to get investors interested in those stocks, fueling disproportionally-large buying to catapult them higher. There is really no reason to deploy capital in large majors when mid-tiers are easily running circles around them.

Even if like me you don’t own Newmont or Barrick and have no intention of investing in them, they could cause problems for the entire gold-stock sector. Their hefty GDX weightings mean their stocks have way-outsized influence in how that leading ETF fares. If these super-majors’ giant stocks lag, they are going to retard GDX’s upside which in turn will leave traders less optimistic and more skeptical on gold miners’ outlook.

So mega-market-cap gold miners could significantly slow the overall sentiment shift from bearish back to bullish which is necessary to attract in buying. If capital inflows diminish because of the perception this sector isn’t rallying enough, the bull-market uplegs will unfold slower and maybe end smaller. Even more problematic, the super-majors’ high weightings in GDX suck ETF capital away from more-deserving miners.

Most investors prefer sector ETFs over individual stocks, so lots of capital will flow into GDX as investors get interested in gold stocks again. GDX’s managers have to allocate any differential buying pressure into its underlying component companies in proportion to their weightings. The newly-merged Barrick and Newmont will likely command much-bigger weightings, starving smaller component miners of capital inflows.

But despite these mega-mergers being bad for everyone except the managers of those companies paying themselves huge compensation, all is not gloom and doom. If the new Newmont and Barrick continue to suffer waning production after their initial merger-boost year, investors will shift capital out of them into the other gold miners. That will gradually throttle their market caps and thus weightings in GDX, mitigating damage.

And if these super-majors taint the performance or expected upside in GDX enough, GDXJ may very well usurp it as the gold-stock sector benchmark of choice! While falsely billed as a Junior Gold Miners ETF, GDXJ has really become a mid-tier gold miners’ ETF. It has been increasingly outperforming GDX, and that trend could accelerate since GDXJ will hopefully never include the larger majors led by NEM and ABX.

With so many fundamentally-superior smaller gold miners to pick from, investors have no need to own the larger majors. Plenty of mid-tier miners are still growing their production organically, by expanding their existing mines or building new ones. Their upside as gold continues marching higher in its bull market is enormous, dwarfing what is possible in the giant majors struggling with waning production. Avoid the latter!

One of my important missions at Zeal is relentlessly studying the gold-stock world to uncover the stocks with the greatest upside potential. The trading books in both our weekly and monthly newsletters are currently full of these better gold and silver miners. Most of these trades are relatively new, added in recent months as gold stocks recovered from deep lows. So it’s not too late to get deployed ahead of big gains!

To multiply your wealth in stocks you have to do some homework and stay abreast, which our popular newsletters really help. They explain what’s going on in the markets, why, and how to trade them with specific stocks. Walking the contrarian walk is very profitable. As of Q4, we’ve recommended and realized 1076 newsletter stock trades since 2001. Their average annualized realized gain including all losers is +16.1%! That’s nearly double the long-term stock-market average. Subscribe today for just $12 per issue!

The bottom line is gold-stock mega-mergers are bad news for everyone in this sector. Combining major gold miners already struggling with slowing production doesn’t solve the problem, but only masks it for a single year. The resulting super-majors’ massive market capitalizations saddle their share prices with big inertia. They are going to require much-larger capital inflows to rally materially, really retarding their upside.

Their higher weightings within sector ETFs will lead to worse perceived sector performance, delaying the necessary sentiment shift from bearish back to bullish. And the super-majors will suck up more of the capital allocated to gold-stock ETFs, starving smaller and more-worthy gold miners of buying. Thankfully some of these problems can be avoided by shunning Newmont and Barrick, and sticking with great mid-tier miners.

Adam Hamilton, CPA

February 19, 2019

Copyright 2000 – 2019 Zeal LLC (www.ZealLLC.com)

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan

Comments are closed.