President Joe Biden is making a lot of people very happy lately, with his recent announcement of a new infrastructure deal set to create millions of jobs and boost demand for materials, minerals, and metals. The mining industry will have no small role to play in this plan, the result of a deal struck between five Democrats and five Republicans.

“The Bipartisan Infrastructure Framework”

The bipartisan deal will lay out a plan for spending hundreds of billions of dollars on key infrastructure projects in the United States, including building roads, bridges, and highways in a massive coordinated effort to stimulate the American economy and create jobs in every sector of the economy. Of course, much of the job creation will be happening in the construction, planning, and other sectors directly related to the projects. Still, most ancillary sectors as well as many of the services needed to sustain these projects will benefit as well, particularly for those areas in which the projects will be running.

“We’ve struck a deal. A group of senators – five Democrats and five Republicans – has come together and forged an infrastructure agreement that will create millions of American jobs.”

The announcement boosted London copper prices last Friday, with a positive outlook for any and all metals that will be needed to supply this multi-year multi-billion dollar challenge. Better demand for metals in the coming years could translate into bigger profits for miners, and a supply push that could keep copper mining companies working hard to expand their mine portfolios and increase production rapidly.

More Price Gains for Copper

Three-month copper on the London Metal Exchange advanced to $9,459 per tonne, and the most-traded August copper contracts on the Shanghai Future Exchange closed down 0.5% to $10,644.73 per tonne. This continues to plot copper’s rise to the possible $15,000 target set by Goldman Sachs earlier this year, and builds on the price momentum seen over the past two months.

While copper has been one of the biggest gainers this year, suppliers and steelmaker’s stocks surged after the announcement as well. Caterpillar jumped an additional 2.6% on Friday after a 3.8% gain on Thursday, the biggest in three months for the company.

Huge Plans Driving Huge Demand

The U.S. will require massive amounts of steel for this ambitious plan, and steel stocks are already reflecting that positive outlook. Friday saw U.S. Steel Corp. climb over 3% and the largest steel producer in the U.S. Nucor Corp. jumped 2% with the news. The bill and the infrastructure plan is a tide that is set to lift all boats, from the top of the supply chain to the bottom. Mining companies in particular will have their hands full filling the rising demand from this plan, and the supply dearth the market is experiencing now could accelerate with the possible new dynamic.

“The Bipartisan Infrastructure Framework represents the largest federal investment in public transit history – including the largest passenger rail investment since the creation of Amtrak. I might be a little biased, but that’s a big deal.

While the coming copper supercycle is something miners are sure to be looking forward to, they will also be kept on their toes for some time working to fulfill all of the potential this rocket ride will provide.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

Pouring molten copper at a copper mill in Chile.

Copper’s continued rise seems to be without barriers right now, even after China ramped up efforts to cool the commodities surge that may be building fears of global inflation. Worries on the other side of the planet are also fueling concerns about the long-term supply outlook.

Chile’s proposed tightening of regulations in the country and higher taxes on royalties and other profits may not come to pass, but until a resolution is made by vote, miners and traders will continue to haggle over the direction of copper. For now, the bias has been a solid upward trend that is showing no signs of abating.

The world’s biggest copper-producing country (Chile) has just elected an assembly that had put the writing and signing of a new constitution mostly in control of the left-wing. With social and environmental concerns at the forefront of their political agenda, there isn’t much room for error as opponents of the new policies work to prevent them from being signed into law.

Compromise Will Be Necessary

In the end, some regulations could be coming down the pipeline, with miners facing more rigid rules around environmentally-friendly operations and mineral rights. That regulation would ultimately pave the way for one of the heaviest taxes on the mining industry in the world. Royalties and profits from mining activities in the country could be taxed at higher rates than ever before, possibly leading some miners to shift focus to other regions.

For some companies, risks are minimized. Canadian miner Teck Resources (NYSE:TECK) has a stability agreement in place with the country that will shield its massive Quebrada Blanca Phase 2 copper project from higher tx levels for 15 years, according to Chief Executive Don Lindsay. Many countries south of the equator have shifted tone on mining, with Peru’s socialist presidential candidate Pedro Castillo claiming he would raise taxes and royalties on Peru’s all-important mining sector and move to quickly renegotiate with large companies over their tax contracts. This is a big if, as he has not been elected, and opposition is strong.

Lobby groups, politicians, mining companies, and their workers will look to maintain operations as they are, with job creation and economic growth a key pillar for the countries in which the mining industry operates. As one of the most significant sectors for many of these countries, the jobs they rely on and the tax income generated are essential to the nations and the politicians who run them.

There’s No Stopping This Train, Even if it Slows

For now, China continues to maneuver to try to find ways to contain costs and keep prices low or at least stable. Citigroup analysts recently recommended buying the dips since Beijing could “easily run out of options” for tamping down price growth. Analyst Tracy Liao wrote in a note that, “We do not foresee such a U-turn any time soon given the strategic priority of these agendas.”

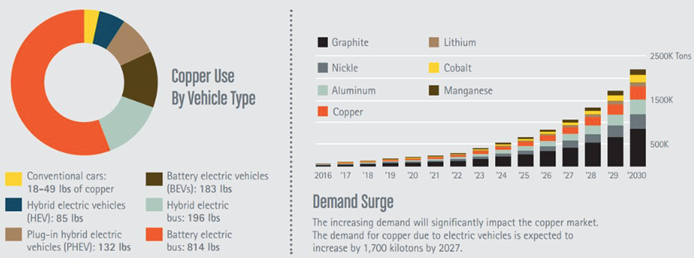

The coming decade is likely to see consistent growth for copper prices, regardless of intervention as the global economy pivots to an electrified format with EVs and batteries driving much of the transition.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

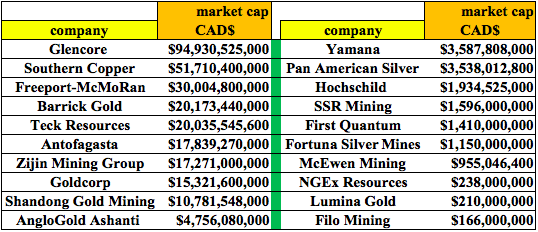

Glencore (GLEN:LN), one of the world’s largest producers and marketers of copper, produced 1.26 million tonnes and sold 3.4 million tonnes through its marketing business in 2020. Their copper production is so large that the company is also a major producer of cobalt, a byproduct of copper. Most of their cobalt product comes from the Democratic Republic of Congo.

The Start of an Upward Trend

While 2020 was a good year for Glencore (GLEN: LN), 2021 began to set the trend for production increases. On Thursday, the company reported 301,200 tonnes produced in the first quarter of 2021, 3% higher YoY from Q1 2020. While the reopening of production and the lifts of restrictions for miners contributed to this bump, productivity improvements also lent a hand to the increase.

“The group’s overall production was broadly in line with our expectations for the first quarter. Production in Q1 2021 reflects that many of our operations continue to maintain thorough Covid-safe working practices, as appropriate for each specific country and region. Full-year production guidance has been maintained for our key commodities,” according to CEO Ivan Glasenberg.

Big Influence

Glencore’s business is one of the most diversified, comprising more than 60 commodities. The company has operations at approximately 150 mining and metallurgical sites in more than 35 countries. Employing 135,000 employees and contractors, where Glencore goes, significant employment number improvement often follows, and the company holds so much sway in many commodities that it is often responsible for price changes as a direct result of supply and demand.

Copper’s in-demand status continues to increase, and Glencore’s production increase is just a piece of what will be necessary over the coming years to meet the massive demand coming. As one of the largest producers and marketers of copper in the world, Glencore (GLEN: LN) will need to take a lead position in the market and help balance the supply issues facing the industry right now.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

The Paris climate goals and the transition away from fossil fuels toward electrification are set to create an unprecedented surge in copper demand, according to Goldman Sachs’s new report on copper. The global investment bank is forecasting a long-term supply gap of 8.2 million tonnes of the metal by 2030, “twice the size of the gap that triggered the bull market in copper in the early 2000s.” This would be the “highest on record” and would set the tone for the 2020s making this period the strongest phase of volume growth in global copper demand in history.

Copper’s Importance

The world isn’t just moving away from fossil fuels, but it is actively working on reducing and reversing some of the warming effects of greenhouse gases. The impact of climate change costs the global economy hundreds of billions of dollars. Investing in clean technologies is the antidote. The investment in technologies like carbon capture and storage technology, renewable energy, and electrification of everything from cars to manufacturing means that copper will have a critical role to play in this new economy.

The centrality of the red metal makes it a critical component for strategic investments both from private businesses and governments. The countries willing to invest in the infrastructure and support for mining companies now will have profits coming in steadily over the next decade. Some have even called copper a national security issue due to its strategic value.

A Shortage That Threatens National Security

The high value, current under-investment, and lack of tier one mines makes it a potentially destabilizing force as many countries classify certain metals as strategic. For context, one only needs to look at history.

The wars of the past 50 years have been fought for several reasons, but one of the prime motivators for conflicts in the Middle East was oil. Winning the war meant rebuilding the infrastructure in the region and therefore gaining a foothold in the supply. This was highly valuable to foreign countries and the mining companies extracting these extremely strategic resources.

The countries with abundant copper deposits sitting within their borders may ultimately come to realize that the global demand and urgency of the commodity will drive its importance for the largest economies in the world. As the scramble continues and even accelerates as demand multiplies, those countries may find themselves standing between powerful corporate interests and the governments fighting to secure the supply required for their needs. A shortage of copper would mean a fierce fight for the material that is certain to play a significant role in the large and developed economies accelerating toward net-zero emissions right now. With most countries targeting 2050 for this goal, copper’s demand will likely grow fastest in the first half of the century and continue into the second. By the middle of the century, it will be necessary for a plethora of manufacturing, products, and energy supply and storage.

Each of these functions could easily fit under the national security blanket, pushing countries to nationalize supply or even move aggressively, as happened during the Iraq wars. The good news is that copper mining companies are exploring and developing those projects now and are setting themselves up to be right in the middle of this boom, taking advantage of a supercycle that will drive profits for decades.

Goldman Puts Things Into Perspective

Goldman’s prediction that the copper price would reach $6.80 per pound by 2025 is a significantly bigger statement, demonstrating that the investment bank believes that copper will not need to wait until 2050 to see new peaks in demand spiking regularly. According to their recent report, prices will also spike regularly, breaking highs and setting new records within as little as four years from now. This past February, copper hit a multi-year high, foreshadowing a sliver of what is to come.

Analysis

The authors of the report, Nicholas Snowdon, Daniel Sharp, and Jeffrey Curries estimate that demand from electrification “will grow nearly 600% to 5.4Mt (million tonnes) in our base case and 900% to 8.7Mt in the case of hyper adoption of green technologies” by 2030. In the conservative base case, copper miners would see a massive demand to be filled surge faster than current production and production plans can accommodate. In the case of “hyper adoption of green technologies,” the world is likely to see a problematic copper shortage that is certain to push the price higher and faster.

The authors continued: “Crucially, the copper market as it currently stands is not prepared for this demanding environment. The market is already tight as pandemic stimulus (particularly in China) has supported a resurgence in demand, set against stagnant supply conditions. Moreover, a decade of poor returns and ESG concerns have curtailed investment in future supply growth, bringing the market the closest it’s ever been to peak supply.”

Steep Trendlines

The report forecasts a copper price of US$15,000 per tonne by 2025, up from today’s price of around $9,000 per tonne today. To get a sense of the trend, the report included estimates of the average price by year:

2021: US$9,675/t

2022: US$11,875/t

2023: US$12,000/t

2024: US$14,000/t

The culmination in 2025 at $15,000 would mean huge profits for miners as well as a need for new greenfield project approvals.

Driving Prices

The demand driving the copper price stems from three main drivers of green copper (copper mined cleanly):

Electric vehicles (EVs)

Solar power

Wind power

Goldman estimates a 2021 sales volume of 5.1 million EVs in 2021, with that number rising to 31.51 million in 2030. Just to meet that demand, current copper production might need to double or triple. Including charging units (of which Goldman estimate 30 million will be installed by 2030), accessories, batteries, and other power storage needs, copper demand seems to be almost incalculable. Conservative estimates make it seem like production is far behind, and the top end of the range requires unprecedented investment in the industry for new projects.

How is it Going?

Right now, the copper market is not prepared for this demand. The massive copper deposits to be found in the Andean Copper Belt, being discovered and explored by miners like Solaris Resources, EcuaCorriente, and SolGold are set to become some of the most valuable projects in a high-value copper region.

Some analysts disagree with the borderline alarmist analysis in the report, with opinions often coming down on the side of caution where prices are concerned. According to TD Securities, “Commodity demand is being supported by a weakening dollar amid a consolidation in U.S. interest rates and fiery risk appetite. Demand continues to pick up, but as the world exits the pandemic and begins to ramp up production, “…metals supply risk is likely to subside from here, adding some pressure to industrial metals prices.”

It seems that for now, there is no perfect consensus as to where the copper market might end up. While demand is guaranteed to increase, the scale of supply risks and production worries are still speculative and do not add up to a definitive answer on where the balance lies. There will no doubt be an imbalance as demand outstrips supply for the next decade, but analysts are still split on how big that gap might be. In either of Goldman’s scenarios, the situation seems quite dire, with the price ending up in the stratosphere. TD Securities seems to temper that outlook somewhat, without disputing the key point here that copper prices are set to rise no matter what.

No matter which side of the spectrum you might fall, the next decade is sure to be a wild ride for everyone with a piece of this cake, and is guaranteed to bring a sugar high for decades to follow.

Open-pit copper mine, Peru.

Peru is one of the prime copper mining destinations for miners from every corner of the globe. Some of the largest deposits of the red metal are sitting in the ground in this mining-friendly country. For Anglo American, the Quellaveco Mine presents an opportunity to add another world-class cost-efficient mining operation to their diversified portfolio.

A Hotbed

Anglo American is part of a group of miners that contributed 58% of mining investment in Peru in January. While mining investment in Peru slumped because of the pandemic and remains below pre-pandemic levels, investment in infrastructure and planning has restarted in earnest now. The Quellaveco Mine is a significant focus of capital expenditure for the company, and it’s pretty easy to see why.

A Hot Commodity

According to Bloomberg, “Within a decade, the world may face a massive shortfall of what’s arguably the most critical metal for global economies: copper.

The copper industry needs to spend upwards of $100 billion to close what could be an annual supply deficit of 4.7 million metric tons by 2030 as the clean power and transport sectors take off, according to estimates from CRU Group. The potential shortfall could reach 10 million tons if no mines get built, according to commodities trader Trafigura Group. Closing such a gap would require building the equivalent of eight projects the size of BHP Group’s giant Escondida in Chile, the world’s largest copper mine.”

Copper miners are scrambling to keep up with demand, and for the time being, prices continue to climb due to the supply shortfall. In the coming years, companies will need to manage their projects to avoid overproduction and a glut of the valuable metal, but for now, there are plenty of opportunities to ramp up production and get more copper into the market.

This is great news for companies that are developing and investing in new projects right now,

Quellaveco Mine

The mine is one of the largest copper deposits in the world and is located in Peru’s most established copper-producing region. Due to the skilled workers and established infrastructure, the project is likely to be a big winner for the company when it begins.

Anglo American expects the mine to be ready for 2022, at which time the first copper production will begin. This project seems to be coming at just the right time to take advantage of a confluence of events and circumstances in the global economy and the process of electrification worldwide. For now, investors will be watching for any sign of the Quellaveco Mine proceeding according to plan, and Anglo American will need to deliver on many of their promises to deliver this project on time and on budget.

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a licensed professional for investment advice. The author is not an insider or shareholder of any of the companies mentioned above.

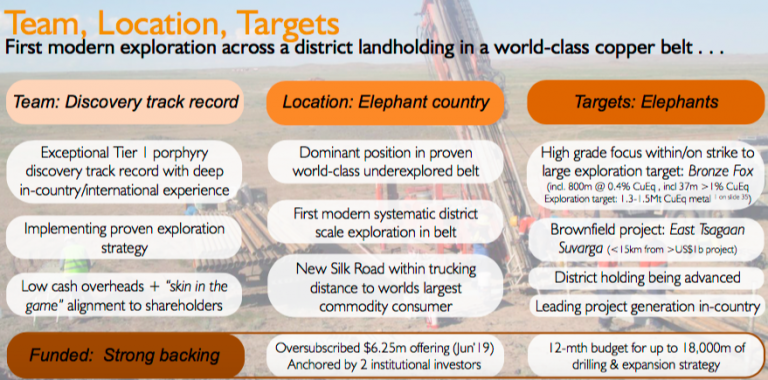

Kincora Copper [TSX-V: KCC] fell off investor’s radar screens due to an extended period of inactivity in 2018, but now the Company is cashed up, team in place, and ready for extensive drilling at 5 independent, large-scale porphyry targets with a 12-month funded budget for up to 18,000 m of drilling.

Kincora has been operating in Mongolia for > 8 years. In 2016, the Company secured unencumbered access to its promising Bronze Fox project and consolidated the dominant landholding in the Southern Gobi copper-gold belt, between and on strike with Rio Tinto’sOyu Tolgoi (“OT“) copper-gold mine, and the Tsagaan Suvarga porphyry project, via the merger with IBEX, a private vehicle indirectly controlled by Robert Friedland.

This attracted a world-class technical team, credited with multiple discoveries of Tier 1 copper deposits, looking to repeat such successes. Since then, the Company has been executing the first modern systematic exploration program across a district-scale landholding in a highly mineralized, but vastly under-explored copper-gold porphyry belt. Now, drilling is just days away.

These are exciting times for Kincora, the most exciting in the Company’s history. The Company is in a prime position in the copper sector where new discoveries are being well rewarded and successful juniors acquired at significant premiums. For example, just this week Australian-listed MOD Resources was taken out by a billion-dollar market cap Sandfire Resources.

A new cornerstone investor, HK-based New Prospect, now the 2nd largest shareholder with about 12% of the Company, is a natural resource specialist fund with an extensive global network. LIM Advisors remains the largest investor, one of the longest operating alternative investment managers in Asia, they invest across the capital structure in deep value & special situations.

Investors in small cap natural resource stocks know that the best time to be in a junior is right before a BIG discovery. That’s the time we could be at right now with Kincora. Management just raised $6.25M. Will there be a new discovery! More than one!! None!!! Yes, there could definitively be zero new discoveries…. This is a highly speculative situation, but backed by a team that has an excellent track record of large discoveries.

Even without blockbuster discoveries, the Company has planned a very detailed and well thought-out drill program that’s sure to cover a lot of bases and provide a pipeline of news flow over the next 12 months. Raising $6.25M in a very tough market at a $7M pre-money valuation was a BIG success in and of itself, demonstrating the strength of management, the projects / targets and the massive opportunity.

The de-risking capital raise is strong evidence of the belief by cornerstone investors & seasoned management that Mongolia is a great place to, potentially, make the newest globally significant copper discovery since 2014. To learn more, please continue reading this Interview of Sam Spring, President & CEO of Kincora Copper [TSX-V: KCC].

Can you talk about how we got to the point of a substantial drill program starting very soon?

After 2018 being a transitional year of setting the right corporate foundations for success, we are entering an exciting period where the drill bit will drive Kincora’s valuation once again. This month we will commence an aggressive, multiple rig, fully-funded drill program. The focus is discoveries on 5 large, independent copper porphyry targets on our 100%-owned Bronze Fox and East Tsagaan Suvarga (“East TS”) projects.

This will be the first drill program conducted by our industry-leading technical team, who have found multiple Tier 1 copper assets. For the last 3 years, we have undertaken the first modern, district-scale, exploration across this vastly mineralized, but significantly under-explored Southern Gobi copper-gold belt.

As readers may know, there are 2 large-scale porphyry projects in this region. Rio Tinto / Turquoise Hill Resources’Oyu Tolgoi open pit mine and underground development project, and a privately-held open pit development project called Tsagaan Suvarga. We believe there are more globally significant copper discoveries to be found.

Limited drilling supports our Bronze Fox project potentially hosting an independently defined, conceptual exploration target of 1.3 to 1.5 M tonnes (midpoint = 3.086 billion Cu Eq. pounds). That would be an in-situ value of $11 billion (1.32 CAD/USD, US$2.70/lb. Cu).

The first hole of the program will, for the first time, correctly test a very large zone (previously drilled in the wrong direction). However, prior drilling still managed to intersect 37 m at > 1% Cu Eq., within 864 m of 0.38% Cu Eq.

Our East TS project sits in the shadows of a billion-dollar open pit construction project at Tsagaan Suvarga (“TS”). Within this brownfield setting, we’re drilling 3 separate targets that are the closet analogues to the high-grade ore bodies at OT…. since OT! While just targets, readers should understand that what we’re exploring for is large and in a very favorable location and geological setting. OT’s ongoing underground expansion is the largest hard rock mining project in the world. It could become the 3rd largest copper mine on the planet, with a 100-year+ mine life.

Kincora was formed in 2011, but we are in the strongest position today that the Company has ever been in. Yet, our current market cap of $12M, (with $6M cash!) is a fraction of our peak valuation of nearly $50M. At that time, we had attracted a buyout offer for the Company and had signed 14 NDA’s with interested parties.

While naturally I’m biased, I think it would be hard to find many juniors with similar risk/return profiles and multiple near-term catalysts, backed by a world-class management, Board, Technical team, Advisors and key shareholders, trading at such a low valuation.

With the Company shortly ramping up drilling of our existing exploration portfolio, and focused on ongoing expansion opportunities, Kincora is the most active foreign-listed junior seeking to make the next Tier 1 discovery in Mongolia.

You just closed on a $6.25M capital raise in a very difficult market. Who were the key investors in this very important round?

~60% was taken up by 2 large natural resource funds and associated groups, who will represent > 40% of Kincora’s shares going forward. These groups, LIM Advisors & New Prospect Capital are both Hong Kong based funds and have a track record investing in Mongolia.

In total, there were > 30 investors in the deal, with strong Board / management participation and good support from high-quality sophisticated investors. As you can imagine, given current market conditions, a lot of work went into this raise. We truly appreciate the vote of confidence from those who invested.

How much of that $6.25M will go towards exploration? Please describe the upcoming drill program.

The vast majority will support Kincora undertaking the most aggressive exploration & discovery drill program anywhere in Mongolia this year. ~$5M will cover up to 18,000 m of drilling at Bronze Fox & East TS, plus project generation activities and advancing earlier-stage exploration targets.

Mongolia has unique geological potential to host globally significant discoveries, and that is what we are focusing on. This raising, with the accompanying warrant package, aligns our capital markets strategy with our exploration & expansion plans and gives us a good shot (but no certainty) at making new discoveries.

We are on record stating that these drill targets are, ‘as good as you get within a global setting for their respective stages’. The key driver in the next 12 months is proof of high-grade & our geological concepts, to confirm our models & interpretations with positive drill results.

In addition to your management team & Board, please describe recent due diligence done by independent advisors, consultants & analysts. Didn’t your largest shareholder also commission a study?

Our drill strategy is the culmination of almost 30 years’ copper exploration experience in this belt by senior members of our team, 5 years of exploration work and model refinements by ourselves and previous owners (including Ivanhoe Mines and IBEX) that provide us with strong conviction to focus on the selected 5 targets.

Kincora has been through 5 technical reviews since mid-2017, including from 1) a leading natural resource private equity group, 2) the EBRD, 3/4) LIM Advisors (twice) and 5) New Prospect Capital, all of which have resulted in capital being invested.

As you have picked up on Peter, our largest shareholder commissioned an independent technical review of our targets, work programs and strategy before becoming a cornerstone investor in our latest offering. This review suggested a, ‘discovery’ had already been made at Bronze Fox within the under-explored target zone to the west of a key regional fault in an area we are calling West West Kasulu. This is where the first drill hole will go. In the independent consultant’s opinion, this target area has been significantly upgraded by recent exploration activities.

While we are optimistic, and management participated in the recent raising, and have undertaken detailed systematic exploration, there’s nothing left to do but drill these targets. Please let me reiterate that Kincora is a high-risk, exploration play. Hence, there are high rewards for success.

A risk is that it might cost tens of millions to delineate an attractive NI 43-101 compliant resource. What is your team’s goal for the upcoming drill program, can you articulate what success might look like?

Absolutely. We appreciate the fact that porphyries are capital intensive, and that exploration is very risky. More meters of drilling provide us a better chance of confirming our geological concepts and riding the value creation curve for shareholders.

The best recent example of a large-scale copper porphyry discovery is that of SolGold at its Alpala project in Ecuador. The deposit at Alpala is deep, so drilling costs there are significantly more than in Mongolia. In March 2016, SolGold raised A$5.7 million at 2.3p/share, having drilled 13 promising holes and seeking to confirm its discovery. An equivalent drill program to what Kincora is now looking to complete at our 2 projects. They had fantastic results…. Over the course of 31 months, SolGold drilled a further 54 holes, attracted both Newcrest and BHP as strategic investors, and re-rated 20x for shareholders.

That’s what success at the target-testing phase of drilling can result in, even in difficult capital markets and a flat/decreasing copper price environment, which we believe is temporary.

At Bronze Fox, our drill campaign is designed to advance the strike potential away from the fault to the west, demonstrate the interpreted, significant increase in tonnage & grade potential, and confirm a new discovery. Prior higher-grade intersections include 3 of 4 holes drilled by Kincora that returned > 1% Cu and/or Cu Eq., incl. the best hole, F62, which hosted 13 m of 1.15% Cu / 1.41% Cu Eq., within 37 m at 0.83% Cu / 1.04% Cu Eq. and 864 m at 0.38% Cu Eq.

At our East TS, the geological concept we are seeking to confirm is that OT-style mineralization is present. Each of the 3 targets at East TS have large-scale potential, with individual coincident geophysical anomalies equivalent in size to ore bodies at OT and SolGold’s Alpala project.

While more conceptual and risky than the 2 targets at Bronze Fox, such a setting and scale of targets is unique – if located in more established copper districts around the world — it’s likely the area around TS & East TS would have already seen extensive drilling.

A rule of thumb for porphyry discoveries is that ~50,000 m of drilling generally provides visibility for ~5M tonnes Cu Eq. metal. Exercise of the warrants that were part of the recent offering would bring in an additional $15M (2.5x the recent raising), and enable another 100,000 meters of drilling.

There are many Copper bulls, yet the price at US$2.70/pound is half of what some bulls think is coming. Do you have a view on the Copper price?

A good question, we get asked that a lot. I will leave the forecasting to the experts, but we’re noticing that most investors see the writing on the wall. Like us, they believe the supply side will at some point (perhaps soon?) struggle to meet even average-trend demand growth, let alone any acceleration from increasing global electrification. This theme is being picked up by generalist investors as well, who have noticed what an unexpected supply shock has done to the iron ore price this year.

Regarding the industry players (mid-tiers & Majors), there has been a notable, but quiet, shift towards looking at new growth projects again over the last 18 months. BHP & Rio Tinto are even talking about organic exploration success stories, focusing on copper as a preferred commodity for expansion. That said, we are just starting to see more of the traditional miners expand into earlier stage projects to rebuild their pipelines.

Time will tell, but I certainly think that even at current copper prices, if we find what we’re looking for, there will be significant interest in Kincora. A tailwind from rising copper prices would of course be welcomed, but given the lack of exploration success industry-wide, globally, for many years now, the project pipeline is in great need of new, sizable discoveries. That is what we believe Mongolia and our targets offer investors.

Please talk about Mongolia, some readers probably won’t invest there. What do you tell investors, shareholders, prospective investors — about Mongolia country risk?

At the time I joined Kincora in 2012, Mongolia was the fastest growing economy in the world. This was driven by the first phase emergence of delivering previously untapped resources to international markets.

This emergence meant that at the time it was almost mandatory for coal & copper Majors to be seeking entry into the southern Gobi regions, with product trucked to the world’s largest consumer of both commodities. We are 5 Prime Ministers, 2 governments, a number of high profile disputes and reversals to unfavorable investment laws later, but the rocks and big picture potential remain unchanged.

In a landscape of few significant greenfield projects recently being commissioned, OT is proof of concept that Mongolia is a mature mining jurisdiction. OT is the largest development project in Mongolia’s history. It’s expected to account for up to a third of Mongolia’s GDP by the mid 2020s. It paves the way for companies like ours by lowering barriers to entry and we and others greatly benefit from newly built regional infrastructure.

When one looks at other copper jurisdictions, it’s becoming harder and more expensive to operate. Chile’s 2018 copper output was greater than the 2nd, 3rd & 4th largest country producers combined. The multi-billion-dollar cap-ex profile for Chile’s Codelco, just to keep production flat, shows the increasing challenges regarding water, community relations & high altitude, not to mention a declining copper grade!

Many other large copper supply regions are also difficult and/or increasingly difficult to operate in; look at recent developments in the DRC, China, Panama, Russia, Zambia, Indonesia, PNG, etc.

Given the team and operational track record we have at Kincora Copper [TSX-V: KCC] we are eyes wide open to the risk/reward scenario in Mongolia, which we find compelling, exploring for the next globally significant copper discovery.

Your readers should stay tuned for drill results, which should start arriving in 5-6 weeks’ time. We expect results to be ongoing for the rest of the year.

Thank you Sam, I think we covered a lot of ground. Bottom line, drill results will define Kincora Copper going forward, and a lot of smart money is betting on good drill results between now and year end.

Peter Epstein

Epstein Research

June 27, 2019

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Kincora Copper including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Kincora Copper are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owns shares in Kincora Copper, and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

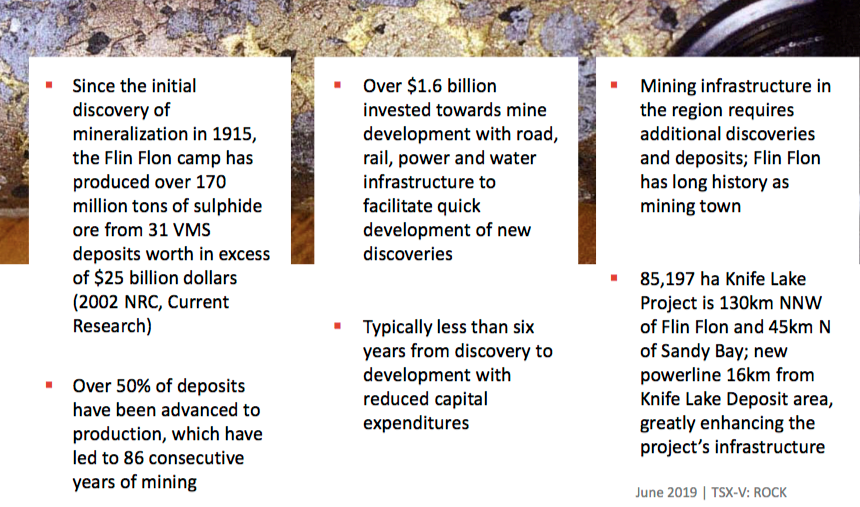

Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) is an exploration company focused on acquiring, exploring & developing mineral resource properties in Canada. Its focus is copper & base metals; more specifically — base, green energy & battery metals — of which copper is all three. Not just in any place, only top-tier mining jurisdictions such as Saskatchewan. And, only in mining districts that have had significant past exploration, development or production. And, only projects in close proximity to key infrastructure. Rockridge’s management team, Advisors & Board expertly and methodically eliminate many of the risk factors, early on, that can kill projects. This is a tremendous team for a company with a market cap of just C$5.6M / US$4.2M.

New CEO Bolsters Already Strong Team

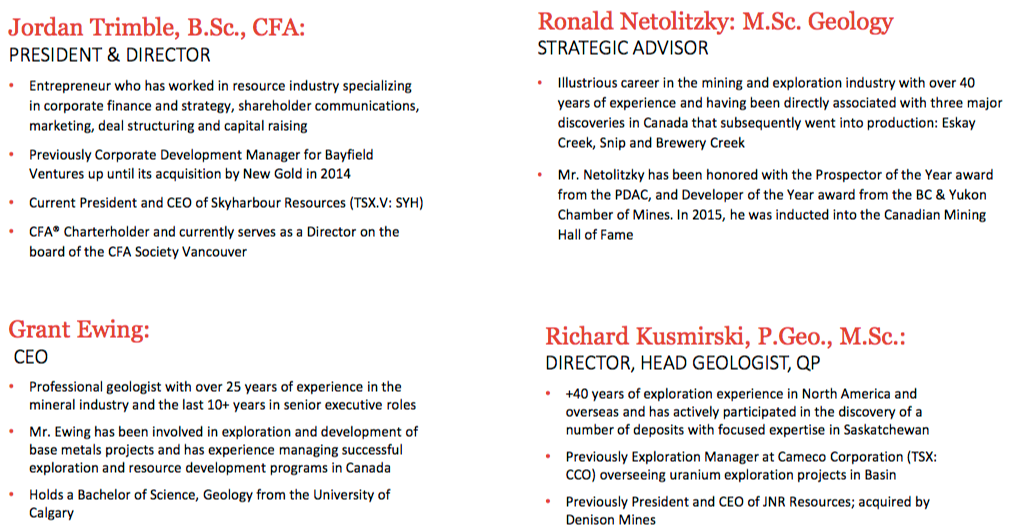

Late last month, Rockridge appointed Grant Ewing, P.Geo to be its new CEO. Jordan Trimble remains as President & a Director. Grant has more than 25 years’ experience in the Metals & Mining space. His expertise covers the mine development cycle, from early stage exploration through to production. I spoke with Grant last week and was impressed with his very extensive knowledge of base metals and his understanding of the district that hosts the Company’s Knife Lake project. Grant seems to be an ideal person to help advance the Project and make new discoveries. Please see more about CEO Grant Ewing, P.Geo here.

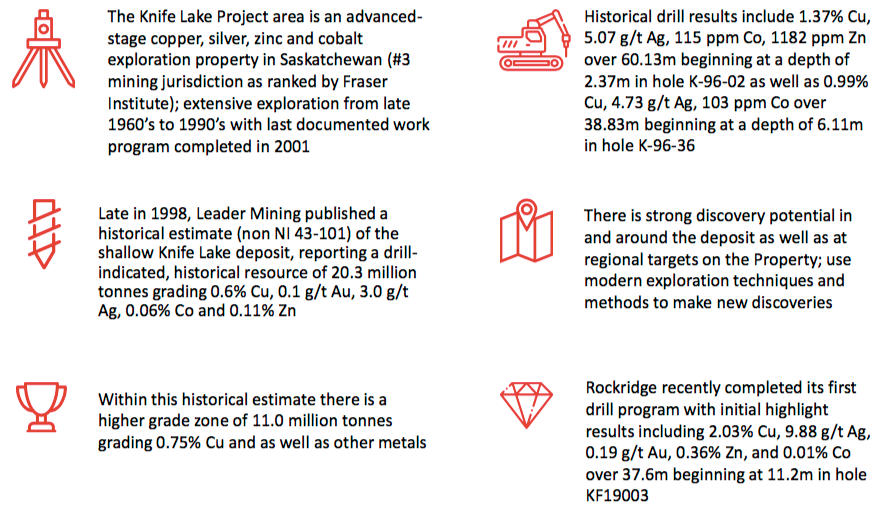

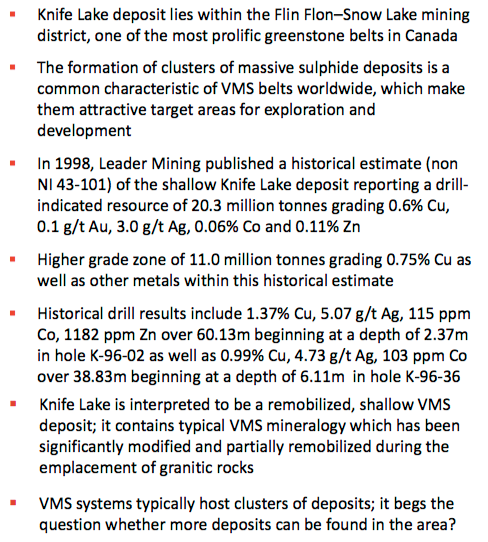

The Company’s flagship project, Knife Lake, is in Saskatchewan, Canada, (ranked 3rd best mining jurisdiction in the world) in the Fraser Institute Mining Company Survey. The Project hosts a near-surface, (high-grade copper) VMS copper-zinc-silver-gold-cobalt deposit, open along strike and at depth. Management believes that there’s strong discovery potential in and around the deposit area, and at additional targets on roughly 85,200 hectares of contiguous claims. As a reminder, Rockridge has an option agreement with Eagle Plains Resources to acquire a 100% Interest in the majority of the Knife Lake VMS deposit.

Flagship Project, Knife Lake, 12 Drill Hole Results Now in….

The Project is within the famous Flin Flon-Snow Lake mining district that contains a prolific VMS base metals belt. Management believes there’s tremendous exploration upside. The goal? High-grade discoveries in a mineralized belt that could host multiple deposits, as VMS–style zones often contain clusters of mineralized zones. Of course, the trick is finding them.

However, no modern exploration, drilling method or technology has been deployed at Knife Lake. It was discovered 50 years ago and last explored in the late 1990s. Airborne geophysics, regional mapping & geochemistry was done, but technologies have improved. Management believes that modern geophysics; high resolution, deep penetrating EM & drone mag surveys to cover large areas in detail, could make a big difference.

Earlier this year, Rockridge drilled 12 holes for a total of 1,053 meters. Importantly, this represents the first significant work on the property since 2001. Readers may recall from reading past articles & interviews on Epstein Research & Equity.Guru & Aheadoftheherd, and viewing videos of then CEO Trimble, that the Company’s primary goal is to explore districts that have been under-explored, never explored, or not recently explored. Management’s highly skilled & experienced technical team & advisors deploy the latest exploration technologies & methods. A lot has changed in 18 years; a simple example would be the use of lower-cost, high resolution drones to fly various surveys.

These 12 assays, added to the historical database, will generate a new NI 43-101 mineral resource estimate in late July or early August. This will be a major milestone that will hopefully draw the attention of prospective strategic partners. Subsequent to that de-risking event, Rockridge is funded for a Summer exploration program, that will likely stretch into Fall. The goal is to identify & refine targets at depth and regionally. Modern vectoring techniques will be deployed, using metal ratios & structural interpretation to identify “primary” VMS deposits.

Other modern methods include high-resolution geophysics, deep penetrating EM to identify conductors, and drone mag surveys to cover large areas in detail. Finally, ground work & sampling will be conducted, analyzing rock geochemistry to identify prospective VMS style hydrothermal systems. Importantly, very limited previous drilling was done below 100m, but of the deeper holes, several intersected mineralization at around 300m. Could they be mineralized lenses?

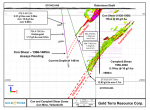

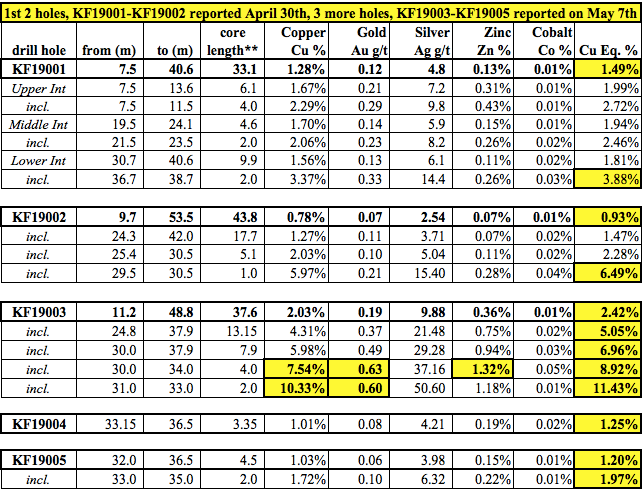

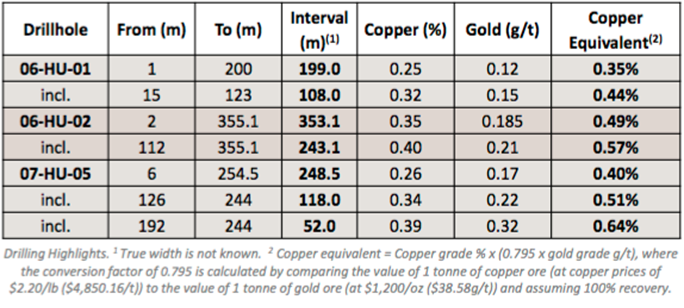

Last month Rockridge reported additional results from its Winter diamond drill program. The first 5 holes are shown in the chart above. Readers may recall that a key takeaway was that holes KF19001 & KF19002 largely confirmed historical grades, intercept widths & geological conditions. Hole KF19003, reported on May 7th, was a blockbuster, 37.6m of 2.42% Cu Eq., significantly better than the first 2 holes. KF19003 had a grade (Cu Eq.) x thickness (in meters) value of 91, compared to 41 & 49. Importantly, it confirmed high-grade mineralization up-dip of KF19002 in an area where no historical drilling is known to have been done. Therefore, this assay, and perhaps nearby assays to follow, could potentially increase the size & grade of the upcoming mineral resource estimate.

Best Intercept in Last 7 Holes: 15.2 m of 2.45% Cu Eq.

In a press release June 10th, holes KF19006 thru KF19012 did not contain any blockbusters, but 6 of 7 were nicely mineralized with Cu Eq. values ranging from 0.46% to 2.45%. The interval widths averaged nearly 8 meters. The best intercept was 15.15 m at 2.45% Cu Eq. in hole KF19006. This intercept is a good one, like those found in holes KF19001 & KF19002, reported in the April 30th. press release. Importantly, KF19006 tested the up-dip extension of the Knife Lake deposit in an area that had not been previously tested. Likewise, hole KF19007 tested the down-dip extension of the deposit near KF19006. KF19007 intersected a solid 2.95 m of 0.82% Cu Eq. grade. The latest property map provided from today’s press release is too large to fit comfortably within this article, please click on link here.

Rockridge’s CEO, Grant Ewingcommented:

“The Knife Lake property package is highly prospective for new discoveries using modern exploration techniques & methods given the lack of recent field work. The known deposit is thought to be a remobilized portion of a presumably larger primary VMS deposit, and there is excellent potential for deposit expansion at depth which we plan to test in future programs. Furthermore, there are several high quality targets to test on the expansive landholding, and there have yet to be satellite deposits discovered in the vicinity as VMS systems often host clusters or stacked deposits.”

Something I found interesting was the 2 portions of the 15.2 m intercept in KF19006 that assayed 7.25 m of 0.72 g/t Gold, (from 8.75 to 16.0 m), and 5.0 m of 0.93 g/t Gold, (from 11.0 to 16.0 m), both within 16.0 m of surface. Those 2 grades (true widths undetermined) are the highest Gold values reported to date. The 0.93 g/t showing is nearly 50% higher, and 1.0 m longer, (5.0 vs. 4.0 m) than the next highest grade Gold showing, in blockbuster hole KF19003. While intriguing, these values in isolation may not amount to much. Still, they’re worth keeping an eye on.

Rockridge’s President & Director, Jordan Trimblecommented:

“The results from this first-pass drill program have exceeded our expectations with almost all drill holes having intersected high-grade copper mineralization, and in doing so, we have successfully confirmed the tenor of mineralization reported by previous operators, while expanding known zones of mineralization. We are working towards issuing an NI 43-101 compliant resource estimate as well as planning a regional summer field program, both of which will provide steady news flow and catalysts over the near term. We will continue to execute on our value creation strategy of going into overlooked but prospective projects in prolific mining jurisdictions and using modern exploration methodologies to test new ideas and make new discoveries.”

The deposit remains open at depth. Additional discoveries are very possible as the property is nearly 85,200 hectares in size and vastly under-explored. The Winter drill program gives the Company’s technical team valuable information about geology, alteration & mineralization that will be applied to regional exploration targets. The Company is now working towards completing an NI 43-101 compliant resource estimate for Knife Lake with the results from this drill program. A summer exploration program is also being planned, details to follow.

Conclusion

As mentioned, Rockridge Resources (TSX-V: ROCK) / (Frankfurt: RR0) has a tremendous team — Management, Board & Advisors — for a company with a market cap of C$5.6M = US$4.2M. Readers should take just 5-10 minutes to review the Company’s new June Corporate Presentation. And, the latest press releases can be found here. The flagship Knife Lake project is large enough, at ~85,200 hectares, to keep the Company busy for years to come. Even if management were to farm out (get free-carried) a portion of the Property, there would still be tens of thousands of hectares remaining to explore in a top mining district in Canada.

Copper prices are down into the US$2.60’s/lb. from close to US$3/lb., but near-term fluctuations in the price are meaningless for anyone who believes that copper is needed for, 1) clean-green energy storage, 2) the global electrification of passenger & commercial vehicles, and 3) the surge of infrastructure building needed to accommodate a growing global middle-class population migrating to ever-larger cities. Not to mention the re-building of old and destroyed infrastructure like buildings, roads & bridges. Everything uses copper, everything will continue to use copper. The price of copper has to rise, or there won’t be enough copper, it’s that simple. Several experts believe that the copper price is headed to US$4-$5/lb. by 2020 or 2021. If so, a company like Rockridge Resources has a lot of leverage to that outcome.

Peter Epstein

Epstein Research (ER)

June 13, 2019

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] about Rockridge Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Rockridge Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock in Rockridge Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Glen McKay, Co-Founder Newfoundland Hard-Rok Inc.

It takes hard work and perseverance to succeed in the mining industry. Glen McKay, the chairman of the board of directors and founder of leading explosives manufacturer, Newfoundland Hard-Rok Inc, has both these qualities, starting his career as a deckhand in the fishing industry in Newfoundland and Labrador before leading businesses in a range of industries, including finance, construction and, yes, mining.

“Motivation and determination are essential attributes of any successful entrepreneur,” Glen McKay explained in a recent interview. “These are attributes that can be unlocked only from inside a person, not by external influences. A desire to learn and cultivating the ability to be insightful are necessary in assessing business opportunities.”

Newfoundland Hard-Rok Inc.

In 1985, McKay became the Dupont Explosives distributor in Newfoundland and Labrador and used the Newfoundland Hard-Rok division of his company MRO Supplies Ltd. to operate the explosives business. In 1987 Newfoundland Hard-Rok Inc. was incorporated as a separate entity by McKay, who then sold part of it to two employees of MRO Supplies Ltd., Carl Foss and Keith Phelan, who were then looking after the explosives division of the company. The drilling, blasting and explosives company has grown since then. In 1994 Newfoundland Hard-Rok Inc. built an ANFO manufacturing plant near Corner Brook, NL and acquired a fleet of hard rock drilling rigs. In May of 2009, Newfoundland Hard-Rok Inc. commissioned its newly constructed, state of the art Bulk Emulsion explosives manufacturing facility west of Corner Brook. It is now the premier supplier of explosives and drilling blasting services in the region.

Newfoundland Hard-Rok Inc. formed wholly owned subsidiary Dyno Nobel Labrador Inc. in 2004, and wholly owned subsidiary Dyno Nobel Baffin Island Inc. in 2013, with McKay serving as the Chair of the Board of Directors of Newfoundland Hard-Rok Inc. and managing the company’s finances and administration.

Dyno Nobel Labrador Inc. was awarded the contract from Vale (formerly Voisey’s Bay Nickel Company) in 2005 to design, build and operate a bulk emulsion (blasting agent) manufacturing plant supplying the needs of the open pit mine at Voisey’s Bay. Recently, Dyno Nobel Labrador Inc. was awarded an additional second contract for the underground delivery of loading equipment and related services at the mine. Vale’s mine site is in Northern Labrador along the coast near the community of Nain. The mine primarily produces nickel ore with some copper and cobalt and is accessible via air and sea only.

As Newfoundland and Labrador Premier Dwight Ball explains, a five-year construction project at Voisey’s Bay will extend the mine’s life by 15 years. Once operational, Ball estimates the underground mine will create an additional 1,700 jobs both at the mine and at the Long Harbour, NL, processing plant. The mining operation in northeastern Labrador opened in 2005 and currently employs about 500 people, Canadian Press reported.

Dyno Nobel Baffin Island Inc. is a wholly owned subsidiary of Newfoundland Hard-Rok Inc. and was formed in 2013 to service the Baffinland Iron Mines, Mary River Project. Dyno Nobel Baffin Island Inc. has been awarded a multi-year contract to supply explosives for the construction and mining phases. A state of the art modular emulsion manufacturing plant was constructed on site in 2014. The operations involve the manufacturing of bulk emulsion, loading, and firing the blast holes. The Mary River Mine is in the remote northern part of Baffin Island within the Arctic Circle. This remote cold location poses many challenges to shipping and logistics, equipment operation and working outdoors.

Cornerstone Capital Resources

But Dyno Nobel Labrador Inc was not Glen McKay’s first foray into the mining industry. In 1997, he co-founded Cornerstone Capital Resources Inc, a mineral exploration company best known for its Cascabel copper-gold project in Ecuador, which was acquired in 2011 during his tenure. While McKay was with Cornerstone, he served as president, chief executive officer and vice chair. He still owns shares in the company and keeps a close eye on its activities.

On July 13, 2018, Cornerstone released an update on the exploration program at its Cascabel copper-gold porphyry joint venture exploration project in northern Ecuador, in which the company has a 15% interest financed through to completion of a feasibility study. Cornerstone has several other projects in Ecuador and Chile.

“The Cascabel project increases in size with each round of drilling and an aggressive drilling campaign continues,” McKay posted onLinkedIn. “I think that they are probably 18-24 months away from a feasibility study, but I also expect that one of the majors will buy out the current owners (SolGold and Cornerstone) before then.”

SolGold owns the other 85% of Cascabel and is funding 100% of the exploration as the operator of the project. Cornerstone is spinning off its assets (except for its interest in Cascabel, shares of SolGold and the joint venture with the Ecuadorian state mining company) into a new company called Cornerstone Exploration, which will own several drill ready projects in Ecuador and Chile. Cornerstone will be re-named Cascabel Gold & Copper.

Apex Construction

That’s not the end of McKay’s entrepreneurial resume. In 1987, he provided the capital for Apex Construction Specialties Inc, which grew to become the largest supplier of commercial construction products in Newfoundland and Labrador. McKay remained as a shareholder and board member until the company was sold in 2017.

In his 40 years of business experience, McKay has learned a lot about people. In his own businesses, he looked for self motivated, bright, hard-workers who had the ability to be a part of a team. The simple but effective premise is that if you really value your people, they in turn will increase the value of your business.

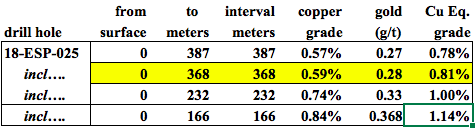

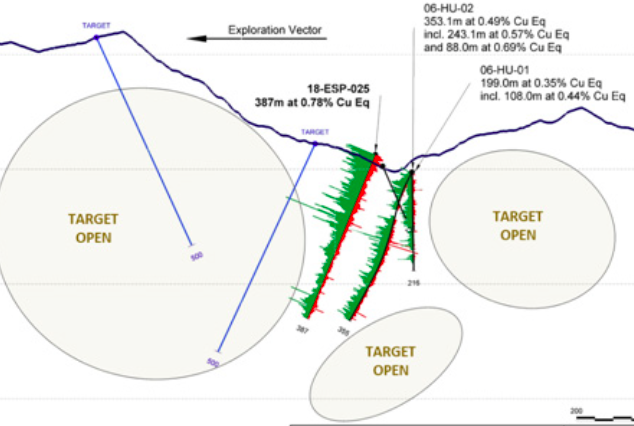

On April 20th, Centenera Mining [TSX-V: CT, OTCQB: CTMIF]reported a strong partial drill hole result at its Esperanza Copper-Gold porphyry project in San Juan Province, Argentina. Excitement over this assay was running high. Management believed that the core looked good, so they rushed the top 166 meters to the lab.

Sometimes when expectations are elevated, actual news can disappoint…. not in this case! The plan was to punch down to 500 m, but drilling difficulties ended the hole at 387 m. Importantly, Esperanza remains open at depth and in all directions.

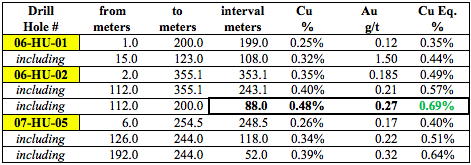

Mineralization was excellent through the top 166 m. On May 8th, Centenera put out the full drill hole assay, covering 387 m (from surface). Before jumping into the details, let me put into perspective historical work that Centenera has access to. Prior drilling returned the following highlights:

Mineralization outcrops at surface with a pyrite halo extending over a 1,400 m x 850 m area, drill holes generally intersected mineralization at surface, and the deposit is open in all directions. The majority of holes terminated in mineralization, the deposit is open at depth. Several holes demonstrated increasing grade with depth.

These are solid numbers, the best interval was 88 m, weighing in at 0.69% Copper (“Cu”) Equivalent (“Eq.”). The goal with this year’s drilling is to find more results like these through prudent step-out drilling. When exploring porphyry targets, one needs to find both wide intervals — 100+ meters, plus high-grade — say 0.60%-1.00% Cu Eq.

Having said that, the depth of a porphyry target matters a lot. All else equal, near-surface deposits can be viable at lower grades because pre-stripping (mining waste rock, or overburden, to reach an orebody) is expensive and time consuming. That’s why this first full assay from Centenera’s 2018 drill program is so exciting; a wide interval, plus strong grade,plus continuous mineralization from surface.

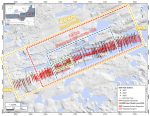

Drill hole 18-ESP-025 collared in mineralization that continued to the bottom of the hole at 387 m (hole abandoned due to drilling difficulties). Mineralization remains open at depth.

There is a number of porphyry exploration and development projects around the world with 0.30%-0.40% Cu Eq.orebodies. The lower the grade, the smaller the margin for error and the greater the need for abundant size. Centenera’s May 8th announcement places it well on its way to establishing economic grade, now it’s a matter of delineating a large-scale deposit. A surface expression of 1,400 x 850 meters is a good start.

East-west cross section showing complete results from 18-ESP-025 and a few previous drill holes. The exploration vector to higher grade Cu & Au is interpreted to be west, where 2 targets are highlighted. All drill holes are open at depth, and there’s significant untested ground to the west & east. Green = Cu grade / Red = Au grade.

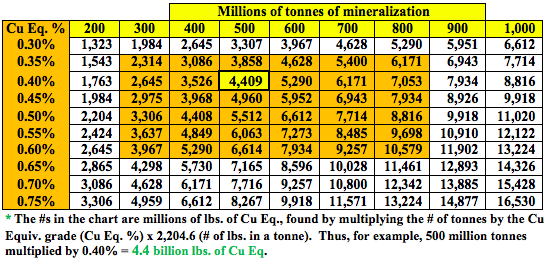

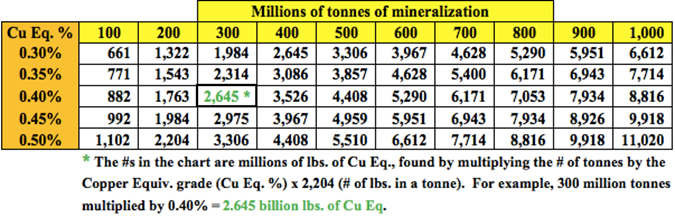

By large-scale I mean > 3 billion pounds Cu Eq. This year’s drilling will be testing for bulk tonnage potential. Readers please note, the Company might not be able to identify muti-billions of pounds in a maiden resource estimate, but perhaps management can do so over time.

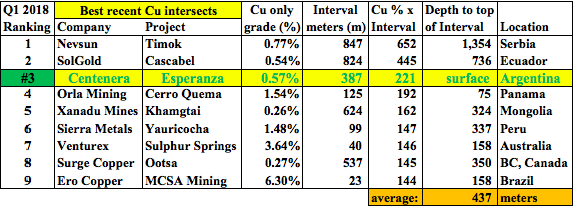

According to the Company, drill hole #: 18-ESP-025 would have ranked #3 among top global Cu intersections drilled in q1 2018. Drill intersections ranked by [the Cu portion only, multiplied by interval width (in meters)]. Despite a very promisingCu-Au project, and several other projects / properties in Argentina, Centenera’s market cap remains fairly low at justC$10.2 M / US$ 7.9 M. Shares are at C$0.14.

The above ranking is of projects where Cu is the primary metal and does not take into account other commodity credits. For example, Esperanza has meaningful gold credits that are not included. In addition to being at surface, (vs. an avg. depth to top of interval of 437 m) the Esperanza project is in a favorable mining province in Argentina, in fact the single best province — San Juan — (as measured by the latest annual Fraser Institute of Mining Survey).

A 0.40% Cu Eq.NI 43-101 compliant resource estimate would mark a robust outcome. Although there’s limited evidence of large scale to date, management’s goal is to find at least 500 million tonnes of mineralization (by no means a sure thing). 500 million tonnes at a grade of 0.40% would equate to nearly 4.5 billion Cu Eq. pounds. Management’s stated goal for its projects is to, “drill, add value and advance to JV or sale.”

I expanded the above chart from a prior article I wrote about Centenera Mining to include higher grades along the left side. This does not mean I believe that the overall mineralized grade will be up to 0.70%-0.75% Cu Eq., but in a constrained open-pit scenario (a subset of the entire deposit), perhapsa Cu Eq. of 0.45%+ could be achieved.

Near-term catalysts

Centenera has several catalysts worth watching for. First and foremost — another drill result in June. That hole was completed to a depth of approximately 450 m. Also, a possible update on its 100% owned Organullo epithermal gold project in Salta province. {2nd best province in Argentina–see brief overview of Organullo on left}

A study conducted in 2012 (using historical drill data) resulted inpotential tonnages & exploration target grades of gold.

** These potential exploration target quantities & grades are conceptual in nature, insufficient exploration & geological modelling has been done to define a mineral resource.

The conceptual (initial) target is between 600-960k ounces gold, grading between 0.92-0.94 g/t Au. Management acknowledges that Organullo will require a lot of drilling.

Another important catalyst is the upcoming closing of Centenera’sC$3 million capital raise. Once fresh capital has been banked, investors will stop worrying about that perceived overhang.

In the second half of 2018, there’s a decent chance cash burn will decrease as management finds partner(s) on one or both main projects. Partnerships typically involve giving up partial ownership in exchange for being free-carried(partner pays 100% of project costs) for a number of years [through key exploration (and possibly development) milestones].

It’s not hard to speculate on prospective partners. For instance, below a list of 20 companies that are Major or mid-tier Copper & Gold miners / project developers, with assets in Argentina and/or Chile, Peru, Ecuador. The top 9 players by market cap would not look at Centenera without evidence of the possibilityof finding > 10 billion pounds Cu Eq. The bottom 3 are small compared to the others, but could certainly come up with a relatively modest amount ofupfront funding required to get the Esperanza project into more robust, steady, active exploration.

I believe that Centenera Mining’s valuation at C$10.1 M / USD$ 7.8 M is too cheap given its portfolio of projects & properties in Argentina. Savvy natural resource stock investors point out that there are dozens of copper-focused porphyry targets in the hands of juniors that have > 1 billion pounds Cu Eq. That’s true, I’m tracking about 3 dozen.

However, there are red flags associated with many of the other prospects. For example, several projects are in higher-risk (than Argentina) or even dangerous jurisdictions in countries including the Philippines, Russia, Mongolia, Indonesia, the DRC & Namibia.Even Peru, the 2nd largest Cu producing country in the world, a jurisdiction with at least 5 major Cu projects held by juniors, is facing increasing challenges on the community relations front.

And, the largest Cu producing country by far, Chile, has prospective projects at elevations above ~4,000 meters that introduce a whole new set of risks, expenses & challenges. In part due to high altitude, Chile is much more sensitive to water issues. I’ve been told that Chile has become considerably more expensive to operate in than most other S. American countries.

Other potential red flags…. some projects have PEAs or PFSs with mediocre-to-poor economics; cap-ex figures twice or more the size of a project’s after-tax NPV. Or, IRRsbelow 15%, assumed Cu prices above US$3/lb., payback periods > 6 years, grades < 0.35%Cu Eq., strip ratios > 3:1.

Finally, infrastructure & project logistics– bulk mining operations require favorable access to transportation, roads, rail, port, power, water, a reliable work force and mining services / equipment providers.

Centenera Mining’s [TSX-V: CT, OTCQB: CTMIF] Esperanza project is probably in the middle of the pack on this score compared to the 3 dozen global juniors I’m tracking, but better than that among assets in S. America due to it being in San Juan province, having a very low strip ratio and being high grade. Esperanza is just 35 km from power lines and enjoys year-round road access. NOTE: {we still need to see further evidence of large-scale potential….}

Disclosures: The content of this article is for information purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein, about Centenera Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered, in any way whatsoever, implicit or explicit investment advice. Further, nothing contained herein is a recommendation or solicitation to buy, hold or sell any security. The content contained herein is not directed at any individual or group. Peter Epstein and Epstein Research [ER] are not responsible, under any circumstances whatsoever, for investment actions taken by the reader. Peter Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Peter Epstein and [ER] are not directly employed by any company, group, organization, party or person. The shares of Centenera Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares and stock options of Centenera Miningand the Company was a sponsor ofEpstein Research. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.

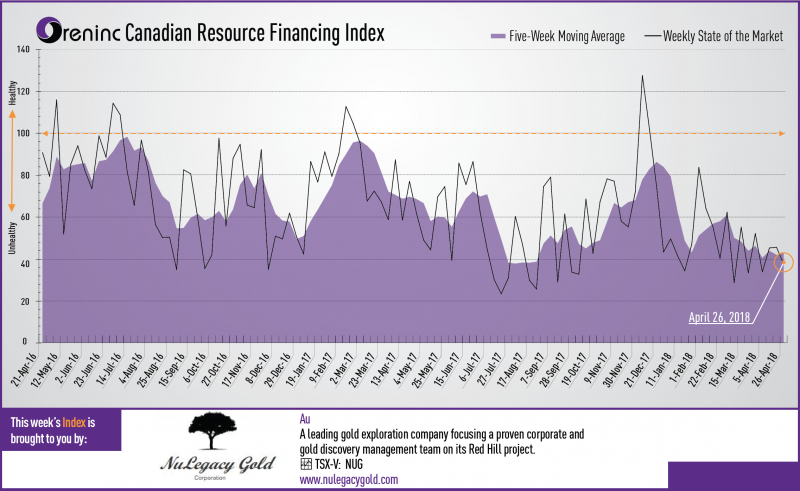

The Oreninc Index fell in the week ending April 27th, 2018 to 37.75 from an updated 45.59 a week ago as the number of deals fell despite some broker action returning.

A calmer and less volatile week all round with the presidents of North and South Korea meeting for the first time in decades, thawing tensions over the north’s nuclear ambitions, whilst in the US, president Donald Trump eased his position on sanctions against Russian aluminium producer Rusal. Maybe spring is in the air and the world is feeling more positive.

Another range-bound week for gold, this time ending in negative territory as the US dollar strengthened, although there are signs that gold stocks are starting to strengthen.

On to the money: total fund raises announced more than quadrupled to C$96.3 million, a four-week high, which included one brokered financing, a four-week low, and one bought deal financing, also a four-week low. The average offer size also more than quadrupled to C$4.8 million, a four-week high. However, the number of financings decreased to 20, a four-week low.

Gold closed down at US$1,324/oz from US$1,336/oz a week ago. Gold is now up 1.63% this year. Meanwhile, the US dollar index continued to strengthen and closed up at 91.54 from 90.31 a week ago. The van Eck managed GDXJ gave up ground and closed down at US$33.03 from US$33.49 last week. The index is down 3.22% so far in 2018. The US Global Go Gold ETF also fell to close down at US$12.99 from US$13.04 a week ago. It is down 0.12% so far in 2018. The HUI Arca Gold BUGS Index closed down at 182.04 from 184.18 last week. The SPDR GLD ETF saw a growth week as its inventory grew to 871.20 from 865.89 tonnes where it had been for nine-days straight.

In other commodities, silver’s recent growth spurt deflated and closed down at US$16.51/oz from US$17.11/oz a week ago. Copper also gave up a lot of ground as it closed down at US$3.06/lb from US$3.15/lb last week. Oil consolidated despite a slight loss on the week to close down at US$68.10 a barrel from US$68.40 a barrel a week ago.

The Dow Jones Industrial Average lost some ground and closed down at 24,311 from 24,462 last week. Canada’s S&P/TSX Composite Index put in a strong growth week as mining stocks showed growth to close at 15,668 from 15,484 the previous week. The S&P/TSX Venture Composite Index closed down at 783.76 from 804.96 last week.

Summary:

Number of financings decreased to 20, a three-week low.

One brokered financing was announced this week for C$15m a three-week low.

One bought-deal financing was announced this week for C$15m, a three-week low.

Total dollars nearly doubled to C$96.3m, a three-week high.

Average offer size grew to C$4.8m, a three-week high.

Financing Highlights

SilverCrest Metals (TSX-V: SIL) announced a C$15 million bought deal financing

Syndicate of underwriters led by PI Financial and Cormark Securities for 7.1 million shares @ C$2.10.

15% over-allotment Option.

Net proceeds will be used to continue exploration and drilling to deliver an updated resource estimate and maiden Preliminary Economic Assessment for the Las Chispas project in Sonora. Mexico.

Major Financing Openings:

Africa Energy (TSX-V: AFE) opened a C$57.98 million offering on a best efforts basis. The deal is expected to close on or about May 4, 2018.

Silvercrest Metals (TSX-V: SIL) opened a C$15 million offering underwritten by a syndicate led by PI Financial on a bought deal basis. The deal is expected to close on or about May 18, 2018.

Pacton Gold (TSX-V: PAC) opened a C$4 million offering on a best efforts basis. Each unit includes a warrant that expires in 36 months. The deal is expected to close on or about May 22, 2018.

Max Resource (TSX-V: MXR) opened a C$3.75 million offering on a best efforts basis. Each unit includes half a warrant that expires in 24 months.

Major Financing Closings:

Nemaska Lithium (TSX-V: NMX) closed a C$99.08 million offering on a best efforts basis.

Trilogy Metals (TSX-V: TMQ) closed a C$31.48 million offering underwritten by a syndicate led by Cantor Fitzgerald Canada on a bought deal basis.

Stina Resources (TSX-V: SQA) closed a C$12.5 million offering on a best efforts basis. Each unit included half a warrant that expires in 36 months.

Ashanti Gold (TSX-V: AGZ) closed a C$2.64 million offering on a best efforts basis.

Company News

Prospero Silver (TSX-V: PSL) provide an update on planned exploration work on its Mexican projects for 2018.

The key objective is to complete first-pass, proof-of-concept drill testing of three projects in the Altiplano belt of northern Mexico: Bermudez, Buenavista and Trias. Neither Trias or Bermudez have been drilled before.

About 6,000m of diamond drilling is planned.

A 4th hole for Pachuca SE project may be drilled once drilling is complete at the projects above.

Analysis

Having recently announced a fund raise, the work plan shows that Prospero will continue to drill test the targets it has identified via its geological hypothesis for discovering large, blind silver deposits. Whilst the news release did not explicitly state that its strategic partner Fortuna Silver (TSX:FVI) would co-fund this exploration program, that seems likely given the technical success of the 2017 exploration program and that Fortuna has yet to select a project to joint-venture under its strategic agreement with Prospero.

ORENINC MINING DEAL CLUB Access to high-quality, pre-vetted financing opportunities www.miningdealclub.com

MEET US AT THE INTERNATIONAL MINING INVESTMENT CONFERENCE MAY 15-16, 2018, VANCOUVER, CANADA Oreninc Presentation: Tuesday, May 15th, 1:00 – 1:20pm

I recently returned from a hectic trip to Toronto for an annual mining industry investment conference known as PDAC. I met with 28 companies and spoke to dozens of investors. I expected to talk a lot about Lithium & Cobalt— how the sell-off in those sectors could be close to over, how demand forecasts keep rising in the face of uncertain long-term supply, etc.

Although there were plenty of discussions on the, “battery metals,” I was surprised by the universal excitement over a metal that’s old school, but also indispensable to the future of electric vehicles & renewable energies…. A metal that needs no further introduction…. #Copper.

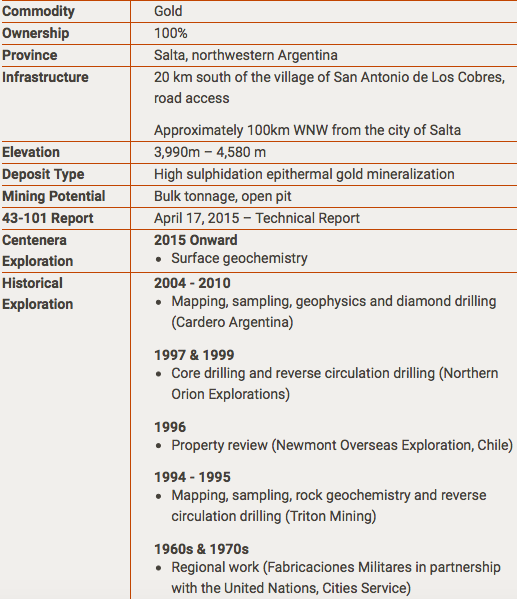

One of the best stories I heard at PDAC was an update from Keith Henderson M.Sc., CEO & Director of Centenera Mining Corp. [TSX-V: CT / OTC: CTMIF], an Argentina-focused company with attractive Copper (“Cu”) & Gold (“Au”) exploration projects. Upon a positive change in Argentina’s government in 2015, Centenera was quick to move more actively into the country.

Drilling is underway at the Company’s flagship project, and management believes that it’s going quite well. The first assay is expected around the end of March.

The crown jewel asset and primary focus of Centenera this year is the 100% controlled, near-surface Esperanza copper-gold project — (formerly known as the Huachi project) — an outcropping Cu–Au porphyry system with a blockbuster discovery that included a drill hole intersection of 353 meters grading 0.49% Cu Eq., (incl. 243 m at 0.57% Cu Eq. & 88 m at 0.69% Cu Eq.). Mineralization outlined at surface and found in shallow drilling is open in all directions and at depth. {see Corporate Presentation}

Assays from the discovery drill campaign included:

Esperanza is in San Juan province in northwestern Argentina, sitting at an elevation of between 2,800 and 3,250 meters. That’s relatively low compared to work being done in the high Andes. The project is 35 km from existing power lines. Proximity to key infrastructure is absolutely critical for mining bulk tonnage porphyry deposits.

Exploration can be performed year-round in San Juan, ranked in the 2017 Fraser Institute of Mining Survey as the #1 province in Argentina, and 3rd best mining jurisdiction in all of South America. Despite well-known players like Barrick (Veladero mine in San Juan)& Yamana Gold (Gualcamayo mine in San Juan) being active in the Province, the Esperanza project remains remarkably under-explored. Only 7 drill holes (2,011 m) have tested this extensive, outcropping copper-gold porphyry system.

After several weeks of delay due to unseasonal storms and flash flooding across multiple northern provinces, drilling is well underway at Esperanza. Interestingly, while repairing road access to site, new mineralization was exposed at surface in an area thought to be barren. Mineralization is now interpreted to extend significantly further to the southeast than previously known. Some of the best mineralization to date has been intersected in this area.

The Phase I drill program is investigating the potential for a bulk-tonnage copper-gold porphyry-style deposit. Management is currently drilling 4 step-out holes, ~2,000 m in total, of at least 100 m away from historical holes, aiming to reach deeper, (500 – 600 m), than prior efforts. Deeper drilling was called for because several assays from 2006-7 showed grade increasing at depth.

Some drill core from the first hole is about to be sent out for assay. I’m told that upon visual inspection, the technical team felt that the core looked really good, but readers will have to wait along with management until the end of March for lab results.

Upon success in Phase I, a Phase II program would include 4 additional step-outs of 100 – 150 m, plus 2 IP targets 500 m to the east, for a total of 6 holes.

Based on exploration to date, the significant grade, and thickness of reported intervals, management believes there could be hundred(s) of millions of metric tonnes of mineralization. The area of interest is already 1,400 m by 850 m. If strong grade and wide intervals continue to be found, the deposit could host billion(s) of Copper Equivalent (“Cu Eq.“) pounds. Make no mistake, it’s still early days, but there’s a real possibility for substantial scale to be unearthed here.

It’s worth reminding readers that McEwen Mining’s (NYSE: MUX) Los Azules project is also in San Juan province. McEwen’s website describes Los Azules as follows; 962 million tonnes containing 10.2 billion pounds Cu in the Indicated category, plus 2.666 billion tonnes containing 19.3 billion pounds Cu Inferred, with (Cu only) grades of 0.48% & 0.33%, respectively. That’s a combined 3.6 billion tonnes of mineralization, containing 29.6 billion pounds Indicated & Inferred Cu, at an average grade of 0.37%.