The junior resource sector is a people business. In my view, making money consistently in a sector which is fraught with risk and failure, without a doubt, is inextricably linked to the quality of the people who are running the companies with which I am investing.

This statement, and statements like it, are very likely the most common answers you will hear from many pundits throughout the industry. While this should now be common knowledge, however, I still hear from investors who invest and lose money with “butchers, bakers and candlestick makers.”

So, why does this still happen? I’m not totally sure. Maybe it’s the potential for a quick buck or simply investors caught up in a narrative. Whatever the answer may be, I’m sure it will continue in the future, and that’s too bad. While it makes a select few rich, overall, the promotion of mediocrity is really bad for the sector.

In saying this, today I have for you a conversation with one of the sector’s ‘greats;’ a man and a group in which it’s worth investing.

This person is Dr. Mark O’Dea, Chairman and Founder of Oxygen Capital.

Oxygen Capital has a great track record of success within the sector, as they have provided a ton of value for their shareholders through the sale of many of their projects, such as Fronteer Gold, Aurora Energy and True Gold.

In our conversation, I asked O’Dea about the secret behind Oxygen Capital’s success, lessons he’s learned while working in the sector, his view of jurisdictional risk and more. There’s a lot to glean from O’Dea’s answers – Enjoy!

Brian: In my opinion, one of the biggest issues facing most people is their lack of self-awareness. Whether it be in their investments or their personal lives, many people either have no idea or are prone to lying to themselves about where they are strong and where they are weak and, thus, typically fall short of their goals and aspirations. Oxygen Capital and its managing partners definitely don’t have this issue, as their track record for success within the resource sector is among the best I have seen. What has and continues to make Oxygen Capital successful within the resource sector?

Mark: When you start working on a project, you know reasonably soon, whether it has the potential to be an economic deposit or not, and if it doesn’t, there’s really no point in faking it. It’s a waste of time, it destroys the trust of shareholders, and it builds the wrong type of working culture. So, you’re much better off focusing your efforts on finding the right project. We have lived by the philosophy of “good projects and good places” for 20 years now and it has worked out really, really well.

Over that period, I’ve been CEO and/or Executive Chairman of a number of public companies that have been acquired, because they were underpinned by projects that were either operating mines, or advanced projects that could ultimately become mines.

For example, Fronteer Gold, among other things, had the high grade Long Canyon deposit that ultimately became a mine built by Newmont, after they acquired Fronteer in 2011. It is now one of their lowest cost mines in the USA. Aurora Energy defined and advanced one of the largest uranium deposits in Canada back in 2009, and it was ultimately acquired by Paladin in 2011. Its Michelin deposit needs higher Uranium prices, but it’s got all the attributes of a long life mine. And most recently, at True Gold, we built an open-pit, heap leach gold mine in West Africa, and shortly after we poured our first gold bar in 2016, we were acquired by Endeavour Mining. So, all of our big successes have been underpinned by high quality projects that were either mines or had the potential to become mines.

Today, we’ve got four companies at Oxygen – Pure Gold, Liberty Gold, Sun Metals and Discovery Metals. We’ve created, in my view, one of the best exploration and development pipelines in the business. And all of our companies continue to be underpinned by good projects, in good places. At Pure Gold, we have the large Madsen Gold Deposit in Red Lake Ontario, which is currently the highest grade gold development project in Canada today. We just finished a bankable feasibility study that’s underpinned by a two million ounce indicated resource, at almost nine grams per ton, with another half million ounces of inferred gold. It’s going through the final permitting process and ultimately the goal is to become the next Canadian producer.

Liberty is rapidly advancing three big open pit gold projects in the Great Basin of the United States. They’re excellent projects in a Tier 1 jurisdiction. We recently put out a PEA on Gold Strike and it shows that it’s got the makings of an excellent low cost mine. It’s very appealing. And we’re about to start drilling Black Pine, which is another big Carlin-style gold system that has exciting size potential.

Finally, Sun Metals, we just made a highly disruptive discovery in BC, which was frankly, one of the best high grade copper-gold intercepts in Canada in 2018. We’re about to get back in there this summer and continue drilling to build continuity and size. We are all very excited. So, all of our businesses are underpinned by real projects and that’s been the key to our success.

Brian: Over the course of my life, I have learned that a large portion of what it takes to be successful is not being afraid of failure. The caveat being that it doesn’t pay to be irrationally courageous, either. Firstly, do you agree? Secondly, can you give an example, in terms of your personal resource sector career, of how you used this philosophy to overcome adversity and be successful?

Mark: I would agree with both points, this business is like a treasure hunt, and you know you’re going to make a lot of wrong turns, and hit a lot of dead ends along the way. But when you persevere and ultimately get to the prize, the reward can be spectacular for everyone, and it’s worth it.

We look at dozens and dozens of projects every year, and the key is to know, A, what makes a good project, and those are things like grade, size, strip ratio, metallurgy, all those kinds of things. The second is knowing when to keep going and when to stop.

In my opinion, it is perfectly fine and, in fact, preferable to cut your losses and move on, if your project isn’t shaping up into something meaningful. So, maybe the metallurgy is fatal, or the strip ratio is too high, or the grade is too low, or maybe you just got the geology all wrong. Whatever the reason, failure is part of this business and winning teams in my opinion need to be able to try and fail and quickly move on to a better project. That’s what investors expect of you.

Brian: For me, jurisdictional risk is an interesting subject because everyone has their own criteria for what constitutes risk. For most, jurisdictional risk is most closely tied to the politics of the country in question, or the politics of a neighbouring country.

Over the course of your career, you have worked in and run mining companies in a variety of different countries around the world. These countries range from premier jurisdictions, like Canada and the United States, to some of the more difficult places, like Burkina Faso and Turkey. How have these experiences shaped the way you view jurisdictional risk?

Mark: In my view, risk comes in many forms and I put risk in two categories. One is subterranean risk. Everything below the ground, and the other is above ground risk. And so, 50 years ago in our sector, all the risk associated with mining was subterranean and related to the deposit itself. Did it have the grade and the size or not? And today, all those subterranean risks are still there, to the exact same extent, but layered on top of it all are the above ground risks. Which are, in many ways, far more challenging, because they’re difficult to manage and they can take a lot of time.

I’m talking about things like regulatory, permitting, social, and geo political risk, and mining is under increased scrutiny today. Regardless of the jurisdiction you’re in these days, each jurisdiction has its challenges, whether it’s from local communities or an environmental group.

From day one, your project needs to be positioned in a way that benefits the local community, regardless of where you are. And that means employment, a better way of life and environmental protection, and if you get these three correct right out of the gate, then you are at least increasing your chances of success down the road.

Brian: At the moment, bearish sentiment within the resource sector appears to be very prevalent. As a consequence, many of the junior companies that I have spoken to are finding it very hard to raise cash to further develop their projects. Oxygen Capital companies have a great reputation when it comes to their ability to raise cash. First, how is it that Oxygen companies are able to raise cash in difficult markets and, second, in your opinion, why is the junior resource sector on a whole, seemingly, having a hard time attracting investment capital?

Mark: Since 2013, we’ve been in a bear market; gold spiked at US$1890 /oz in 2012, and then we’ve been bumping along in the US$1200s to US$1300 range for about six years now. And, during this period, there have been some pretty massive structural changes, with traditional funding having exited the space and dried up. ETF flows have stolen liquidity, and passive money is taken over from active money. During this period, we’ve been able to stick to our knitting and we’ve been focused on buying, exploring and advancing great projects in great places, and building our pipeline. Our businesses have been able to grow in this bear market because we’ve been able to attract some of the best investors and name brand backers in the sector, and I’m extremely thankful for their support in backing our companies. Since 2012, we’ve raised about $500 million dollars in 30 finances. And that includes the CapEx to build the Karma open-pit mine in Burkina Faso.

The biggest challenge to raising new capital today is the decimation of actively managed resource funds. These funds kept the ecosystem going for decades and most of that capital has now migrated into passively managed ETFs, which don’t participate in financings. It has also shifted into other speculative industries, which hasn’t helped. But I do fundamentally believe, that the relevance and approval of the sector is going to have a renaissance as the demand for green technologies puts a bigger and bigger focus on the need for metals in our modern lives.

Brian: Having attended many resource sector focused investment conferences over the years, it’s clear, to me at least, that the majority of investors in the sector are in their, so-to-speak, ‘golden years.’ The younger generations, mainly the millennials, on mass, are virtually absent, with their attention seemingly more focused on cannabis and crypto. The question that comes to my mind is, why? Is it a matter of relatability? In your opinion, why has the resource sector failed to attract the millennial generation’s investment dollars, thus far?

Mark: I think that is an important question, but I’m not sure we’re getting the answer right. The broader market has been booming, other sectors have been on fire and generating great returns, in sectors that are more topical and, frankly, cooler. In contrast, you look at the mining space and the equities have been going down for eight years, so there hasn’t been an opportunity for them to make any money. So, they’ve been staying away and that’s one answer.

The other answer, I think there’s a cognitive dissonance between understanding the role of mining in propelling a greener, more sustainable society. That vision requires metals. And, ultimately, I think a connection needs to be made by people, who are embracing electric vehicles, wind turbines, solar panels, and recognize that they all require metals. Lots of metal, which can be extracted without destroying the environment.

As an example, Tesla just published an article today saying there’s not going to be enough metal to supply the electric vehicle demand that’s anticipated. And that’s all copper, cobalt, nickel, etc. What end consumers and investors need to realize is that, mining and environmentalism are all part of the same continuum. We’re all on the same team. And people can feel good about extracting metals from the ground, to build a sustainable greener future, while still protecting the environment. It all needs to be able to coexist as part of the same ecosystem.

Brian: Within Oxygen, you tend to focus on de-risked projects as part of your ethos. A great example of an advanced de-risked project would be the Madsen Red Lake Gold Mine, which is owned by Pure Gold, in Red Lake, Ontario. Red Lake is a prolific district. What are your reasons for focusing on gold right now and what do you see as a future for Red Lake?

Mark: Almost all of our success as a group comes from projects that have been worked on in the past and we have effectively “rediscovered” them. We can include the Michelin Project that Aurora had, Goldstrike and Black Pine at Liberty Gold, Karma at True Gold, Long Canyon at Fronteer Gold and Madsen at Pure Gold. These were all past producing mines or previous exploration projects that were forgotten and put away for various reasons including low metal prices or changes to corporate direction.

Madsen is a perfect example to highlight. This was a past producing mine for 38 years, it produced 2.5 million ounces of gold and effectively lay dormant for 20 years, owned by the predecessor company Claude Resources, who worked on it intermittently, but never advanced it to the stage of developing a new geological understanding and getting it back into production.

Pure Gold picked it up in 2014, and consolidated the property for a net cost of $8.7 million dollars and the team has focused on re-interpreting, compiling, integrating, every bit of data they could for two years on this project. We came up with a new geological model and the Company is now sitting on the highest grade development gold project in Canada, with a million ounces of reserves, drilled off at six-and-half meter centers, and sitting within a 2.1 million ounce indicated resource with another half million ounces of inferred resource. It’s an extraordinary accomplishment and these are all new ounces. This is not a remnant project that we’re going to go in and salvage. These are brand new ounces sitting outside of historical development. So, that’s a pretty important fact to include in there.

Madsen, even though it’s evolved from a historical legacy project, it is actually a big part of the future of Red Lake. It’s a sunrise asset today. We’re about to move through the final permitting process and into production with a high grade gold reserve of one million ounces, with the potential to provide decades of production in Red Lake. Meanwhile, the Red Lake mine complex itself is a sunset asset and it’s starting to wane. So, I think Madsen is going to be a very, very important component of the whole consolidated Red Lake package.

Brian: In my opinion, distinguishing if management teams are owners or if they are solely employees is integral to understanding the motivation the team has to succeed. Not only is it integral to understand how much of the company insiders own, but at what price.

How important do you think it is that management own shares in their own companies?

Mark: I think it’s vital, I think it’s one of the most important things that a shareholder should look at, when they invest in a company. How much skin in the game does the management have? There’s a massive difference between being an employee and being an owner. Being an owner of your company, through owning a significant portion of shares, is a really strong testament to your dedication and your focus on making it a successful venture. For example, at Pure Gold, we recently had five year options that were about to expire last month and everybody in the group, all the board and senior management, exercised those options and held the stock, adding three million shares of insider ownership to the books.

One of the things I have learned over the years is that when you have a project that you truly believe in, own as much of it as possible. I’m one of the largest shareholders in each of the oxygen companies, and have been regularly adding to my position at Pure Gold and Liberty Gold.

Brian: Mark, it has been a pleasure. Thank you very much for sharing your thoughts on the resource sector and, most importantly, educating us on the Oxygen Capital group of companies. Before we end, do you have any final thoughts or advice for resource sector investors in 2019 and beyond?

Mark: I will leave you with a quote from Miles Davis, who knew what he was talking about when it came to jazz when he said, “Time is not the main thing. It’s the only thing.” He wasn’t talking about mining, obviously, he was talking about music. But I think it is equally applicable to the mining sectors.

In this business or any cyclical business, if you get the timing right, the results can be spectacular, beautiful. And to me, it feels very much like the timing is right for the resource stocks to resurface and breakout from this bear market in the very near term.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do NOT own shares in any of the companies discussed in the interview. I have NO business relationship with Oxygen Capital or any of its associated companies.

Northern Empire – The Sterling Gold Project Site Visit

On April 6th, I had the opportunity to visit Northern Empire’s Sterling Gold Project, located north-west of Las Vegas, Nevada. My visit was great and really gave me a good perspective of the Sterling Gold Project’s scale and its potential for further resource expansion.

In particular, the Crown Block stood out as having great exploration potential, as not only is this area a focus for Northern Empire, but also has drawn a lot of attention from Corvus Gold, whose Mother Lode Open Pit is completely surrounded by Northern Empire.

In all, I left the site visit very optimistic that Northern Empire’s 2018 drill program should shed a lot of light onto the Sterling Gold Project’s potential and am eagerly awaiting news flow!

Las Vegas

After landing in Vegas, I hopped in an Uber to get to my hotel. As this was my first visit to the area, I was mesmerized by the bright lights, massive celebrity advertisements and sheer size of the Las Vegas Strip.

View from the bridge connecting the Bellagio and Ballys

Las Vegas truly is the center of the universe when it comes to marketing, because the corporations that reside here clearly understand human behaviour and how to manipulate it. Everything about the strip is designed to put a smile on your face while simultaneously extracting the maximum amount of money from your wallet.

Along the strip, a Starbuck’s tall Americano is $5.50 USD, a tall can (493ml) of domestic beer $10.00 USD, and a ‘big gulp’ slushy with rum or tequila will run you $30 USD. These prices remind me of those typically reserved for sporting events or concerts, which may be a good comparison for the confines of the Vegas Strip.

A view of New York New York from my hotel parking lot

While my comments here may seem negative to some, they aren’t meant to be. I have a high regard for the marketing expertise that has created this ‘wonderland.’

View of the Bellagio

Bottom-line, even if you aren’t a gambler, Las Vegas is a place that everyone should visit at some point in their lives. It truly is unique in terms of what it has to offer.

Sterling Gold Project

The day of the site visit started early, as we met in the lobby of the hotel at about 6:30 am. I, however, hadn’t adjusted to the 3 hour time change and was up some time before. One thing about starting your day at 4 am in Vegas is that you aren’t alone. That said, I’m sure most of the people I encountered at that time of the morning had yet to go to bed!

From our hotel, it was about a 2 hour drive up the I95 to the Sterling Gold Project. Given the size of our group, we split up into 3 vehicles. In the SUV with me was Executive Chairman, Doug Hurst, and The National Investor newsletter Editor/Publisher, Chris Temple. Both men are very experienced in the mining and investment worlds and shared several, great anecdotal stories about their experiences and lessons they’ve learned from the sector.

Drones and Area 51

Roughly half way to our destination, we drove past a U.S. Air Force base which, famously or infamously, is the site of at least a portion of the U.S. drone fleet.

A drone flying in the Sterling Gold Project Vicinity

One of the most intriguing, yet mysterious, sites along the way was Area 51. Of course, you can’t actually see Area 51, but many of the businesses along the highway have names inspired by this mysterious U.S. Air Force base. I’m by no means an expert on the lore surrounding Area 51, but after spending the day at the Sterling Gold Project, you very quickly become aware of a U.S. military presence.

2 (small) Helicopters in the distance

Walker Lane Trend

The Walker Lane Trend extends north-west from Las Vegas to Reno, running parallel to the Nevada and California state borders. While not as famous as the Carlin or Battle Mountain-Eureka Trends in the northern portion of the state, the Walker Lane Trend has a very rich gold mining history.

It’s estimated that 50 million ounces of gold have been discovered within the Walker Lane Trend, with the Comstock Lode Mine located near Reno being, arguably, the most famous. Additionally, the Round Mountain and Bullfrog Mines are other examples of gold producing mines within the trend.

Interestingly, Barrick’s past producing 2.3 million ounce Bullfrog Open Pit Gold Mine can be seen from Northern Empire’s Crown Block. I was able to snap a photo, while standing at the top of the Secret Pass Open Pit – see below.

View from the Secret Pass Open Pit – Barrick’s Bullfrog Mine

Satellite Image of the Crown Block

As you can see in the satellite image above, the Bullfrog Detachment Fault and the Fluorspar Canyon Detachment Fault run in a similar east-west fashion, and lay host to the past producing open pit mines. Also, the Faults divide the tertiary volcanic rocks in the north and the sedimentary rocks in the south.

Sterling Mine

The site visit began at Northern Empire’s permitted Sterling Mine, which is in the southern region of the property. After completing our site safety orientation and collecting our PPE, we hit the road, making our first stop at the heap leach pads.

Sterling’s Main Entrance Road, Looking away from the Sterling Mine

Sterling’s Main Entrance Road, Looking at the Sterling Mine

Currently, there’s one active leach pad; at the time of our visit, it was being turned over by the bulldozer featured in the photo below. The ore is mixed on the pad to help oxygenate the pile and break up any fluid channels that formed over the last cycle. Ultimately, this leads to higher recoveries in the processing plant. These are simple smart things that the Company does to improve efficiency show the respect that they treat shareholder capital. Also to note, the existing facilities and processing plant appear to be in great shape, which is a real plus when it comes time to begin production.

Active Leach Pad

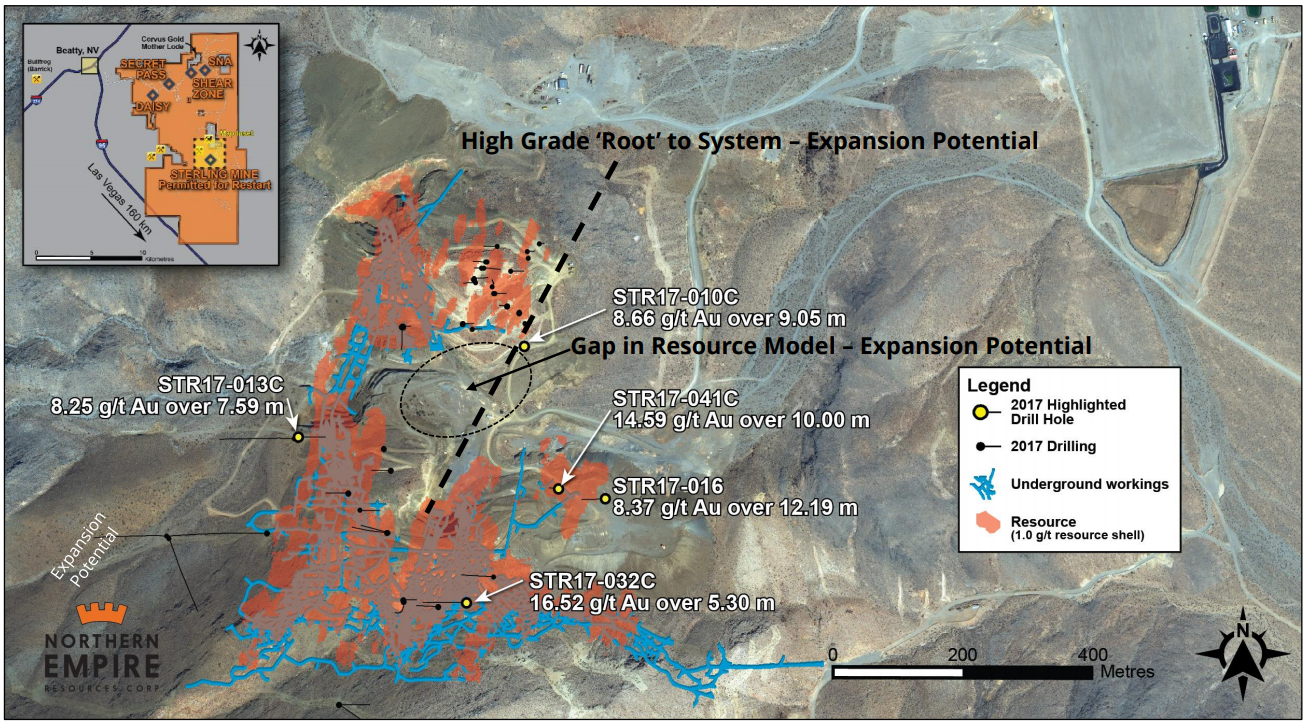

We then moved into the Sterling Mine open pit area, more specifically up onto the Water Tank Hill, which gives a great vantage point for viewing all three open pits.

Northern Empire CEO, Mike Allen, on Top of Water Tank Hill

While standing on Water Tank Hill, CEO, Mike Allen, took the opportunity to explain how they will attempt to expand the Sterling Mine resource. As explained in my introductory article, the company will follow up on recent high-grade drill holes that sit on the pit shell edge, as seen in the satellite photo below.

Sterling Gold Project Mineralization – Core Shack

Next, we headed back to the main offices for lunch and a look at the core shack. As with all Carlin-Style gold, the core doesn’t possess any eye-catching visible flakes or nuggets, but instead it is the orange oxidized material (the more broken up the better) which should catch your eye, as it is gold bearing. The samples, however, were still very interesting as the fluorite and calcite mineralization found on the property can be seen in the core samples. In the photo below, for instance, the purple mineral is fluorite.

Core Sample with Purple Mineral Fluorite

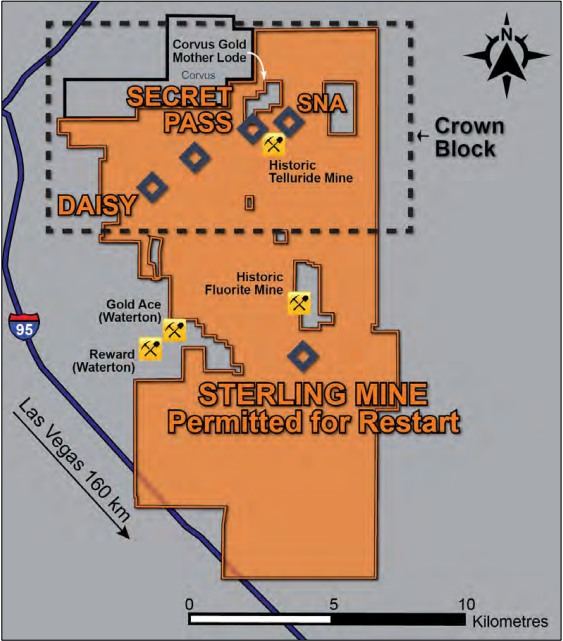

In fact, the Sterling property boundaries not only surround Corvus Gold’s Mother Lode Project, but also historic fluorite and mercury mines, which can be seen in the property map below. Interestingly, it was mentioned during the visit that the fluorite mine was hampered by gold contamination, what a wonderful issue to have!

Sterling Gold Project

Sterling Mine Site Manager Chuck Stevens , who worked previously in the Sterling underground mine, showed me a few excellent calcite samples in his office and, additionally, pointed out the massive calcite sample sitting outside the geologist’s office trailer. Also, Executive Chairman, Doug Hurst, pointed out a couple of cinder cones which lie just east of the property; another example of the geological diversity of the property and its surrounding area. The immediate area around Northern Empire’s Sterling Project features fluorite, decorative rock, precious metals and marble mines demonstrating both the endowment of the area, the impact of mining on the local economy, and the ability to permit both large and small mines effectively.

NOTE: A Cinder Cone is formed by volcanic eruptions of mafic / intermediate lavas, which collect to build a cone around a volcanic vent. On the east side of I95, on your way up to the Sterling Gold Project from Las Vegas, a cinder cone is currently being mined for decorative stone used in landscaping.

The Crown Block

Yours truly with the Secret Pass Open Pit in the background

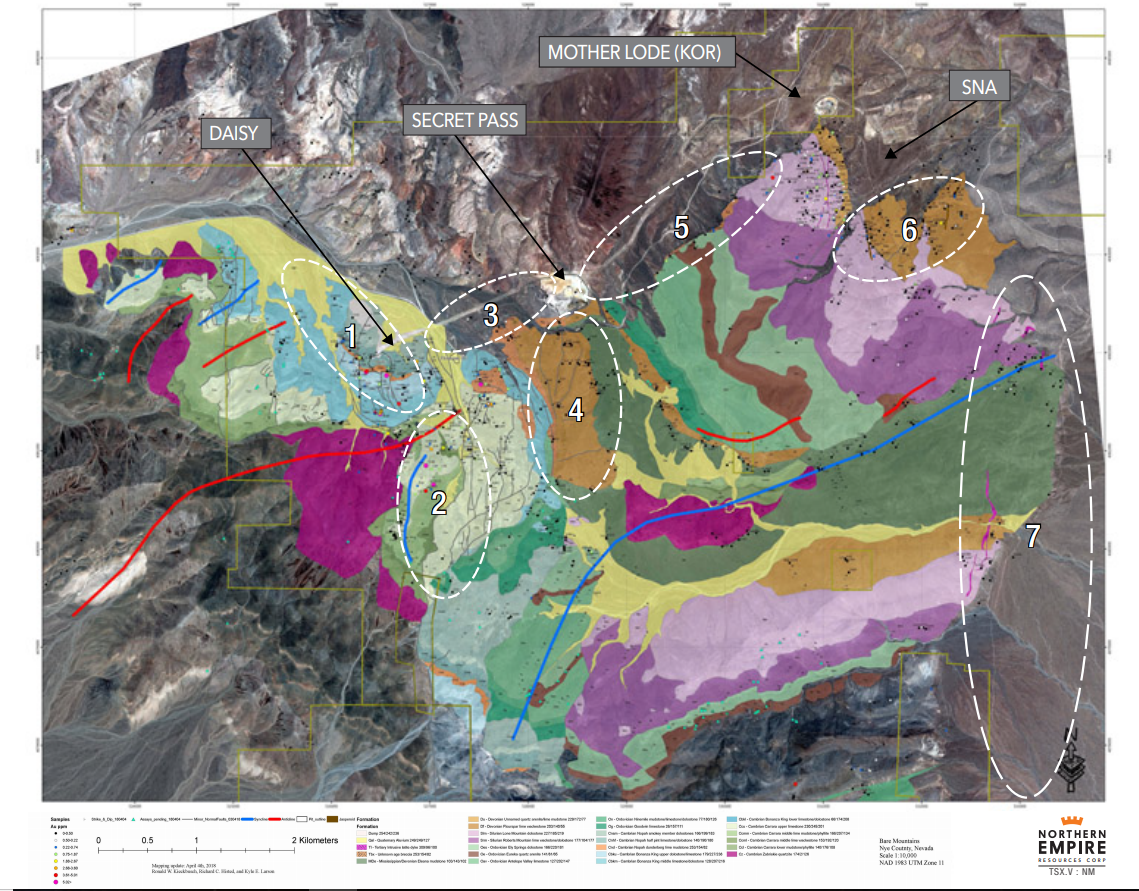

Heading back out onto the I95, we then headed north toward the town of Beatty, to the Crown Block. As you will remember from my introductory article, the Crown Block is made up of 4 main targets: Daisy, Secret Pass, Shear Zone and SNA, all of which are located along the Fluorspar Canyon Detachment Fault.

Our first two stops were at Daisy and Secret Pass deposits, where Senior Geologist, Ron Kieckbusch, and Exploration Manager, Rich Histed, discussed the geology of the area, the work they completed in 2017, and where they were headed in 2018.

Geology of Crown Block

South of the fluorspar detachment fault, mapping has defined an asymmetric fold-thrust belt in the sediment package, with a northwest vergence and northeast plunge likely of Mississippian age (327-290 Ma).

It’s my understanding that the folding of the sediment package generated perpendicular faults, which were later made larger during a caldera collapse. For those who aren’t familiar, a caldera is a large volcanic crater, which can be formed by either an explosive volcanic eruption or the collapse of surface rock into an empty magma chamber. The now larger faults become easier conduits for fluid flow, thus explaining the mineralizing event.

Geological Mapping and Geochemical Sampling

Currently, 30% of the 141 square-kilometer property package has been geologically mapped and geochemically sampled, with the Crown Block being the primary focus. Mapping and sampling is a very efficient and cheap way of acquiring drill targets. In total, 580 rock chip samples have been taken, returning grades within a range of undetectable to a high of 13.85 g/t gold, and 34 samples returned greater than a 1.0 g/t gold.

As stated, the mapping and sampling within the Crown Block has identified new exploration targets, which were noted in the April 25th news release and can be found in the image above.

Road Zone – located north of the Daisy Deposit and features several up-dip surface samples of greater than 1.0 g/t gold, which indicates potential for shallow mineralization.

Gold Ace Fault – located south and up-dip of the Daisy Deposit and features a large undrilled area of high-grade surface samples, including a high of 13.85 g/t gold.

Crowell Extension – located east of the Daisy Deposit and features reported gold grades of up to 7.0 g/t from the historic Crowell fluorite mine. The Crowell Extension target has a strike length of roughly 800 meters.

Radio Tower – Anomalous surface geochemistry to the south of the Secret Pass pit indicate a possible target at depth.

Secret Pass East – As the name suggests, this target lays on the under-explored eastern portion of the large Secret Pass Deposit. Surface sampling has returned up to 5.0 g/t gold and represents a potential strike length of roughly 1200 meters.

Ronko Jasperoids – Located south of the SNA, undrilled Jasperoids returned sample values of up to 2.0 g/t at surface. Jasperoids are excellent host rocks for mineralization and represent a strike length of roughly 500 meters.

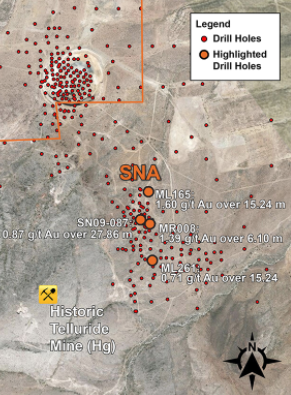

Range Front Fault Zone – Range front fault systems have, historically, laid host to many of the largest Carlin-Style gold deposits in Nevada. The range front fault, which runs along the eastern portion of the land package, is sizeable and untested, which has the potential to host a large deposit. Historic sampling returned values upwards of 5.0 g/t gold at surface on secondary structures. It should be noted that range front structures host 3 deposits on the eastern side of the Bare Mountain Range; Motherlode, SNA and the 144 Zone.

In my opinion, there is a TON of potential here, as Northern Empire begins to expand and fill the gaps between these historic deposits. As seen in the image above, it looks like one big shallow gold system, with good grade. In the gold mining world, it doesn’t get much better!

With the identification of these high prospective targets, Northern Empire is expanding their current drill program to 18,000 meters and have already begun the permitting process for a larger 50,000 meter program, which will focus on expanding the Crown Block resource and testing these new regional targets.

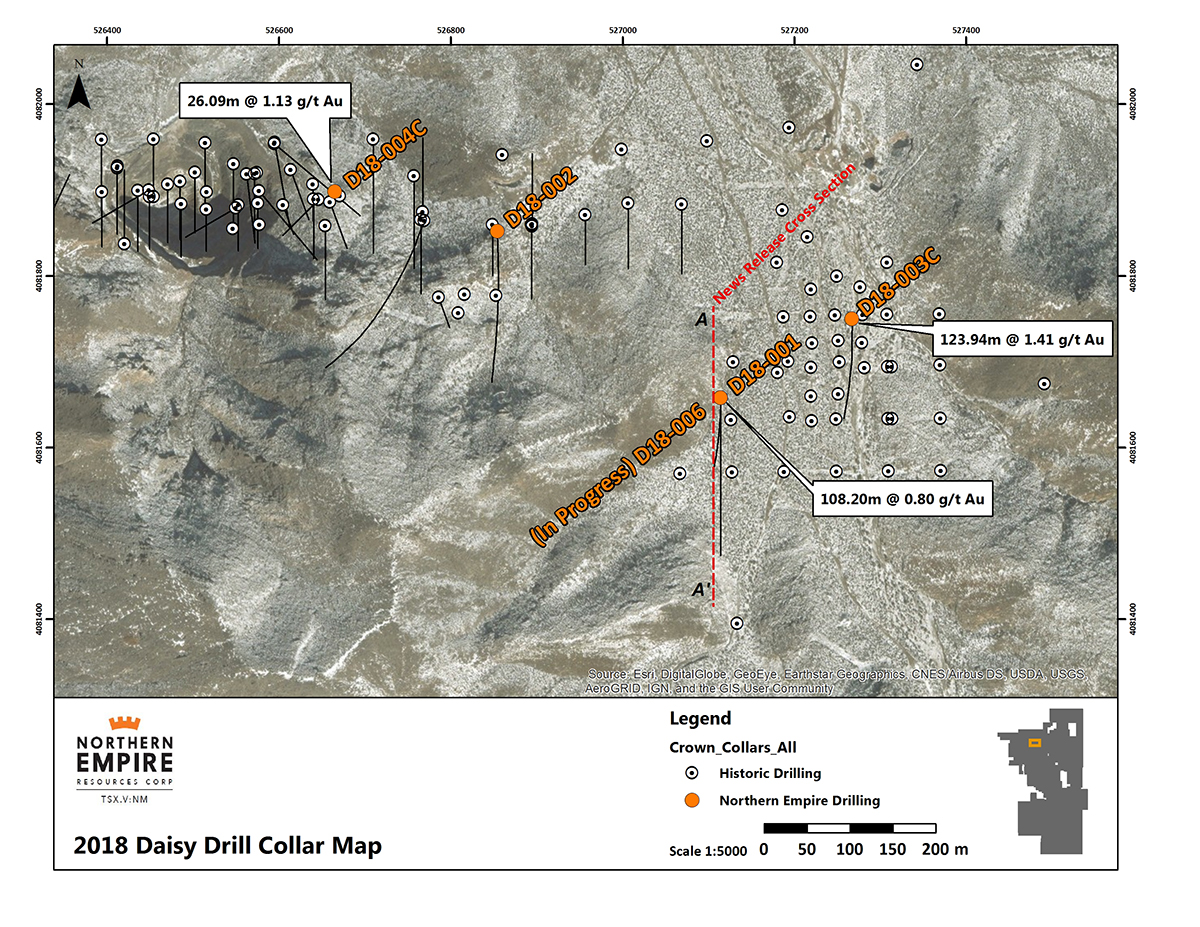

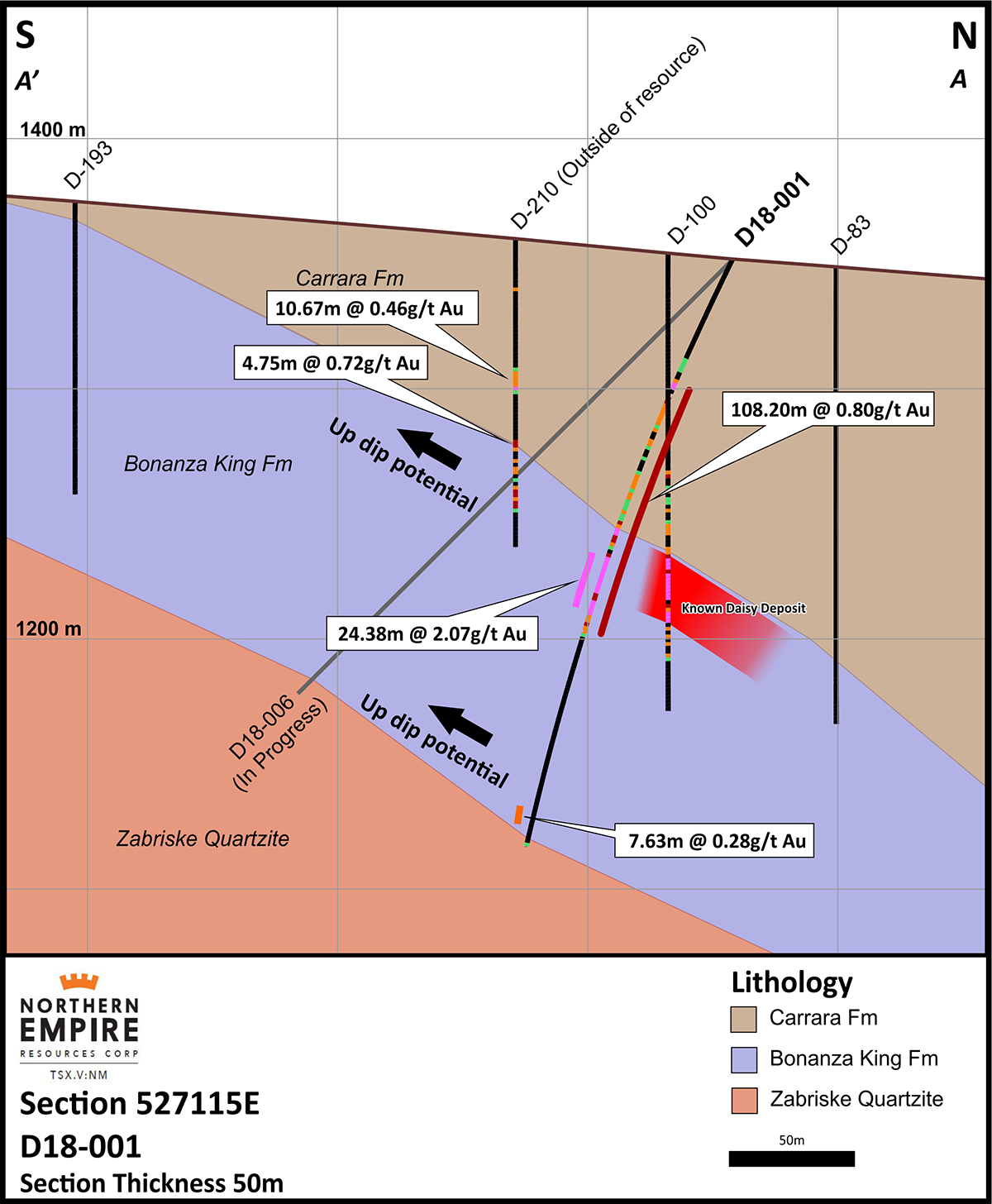

Exploration Drill Results – Daisy and Secret Pass

Step-out drill results from the Daisy and Secret Pass, released May 2nd, not only returned good grades and widths, but confirm that both deposits are open for expansion. The results are highlighted by,

The highlighted D18-001 step-out hole encountered mineralization 53.35 meters down the hole, which was shallower than expected. Additionally, mineralization was encountered at the base of the Cararra formation, which suggests that there is a possibility for further mineralization to be discovered lower in the stratigraphic sequence. In all, the drill results confirm that the Daisy Deposit remains open up-dip for further expansion. Please see the news release for complete details.

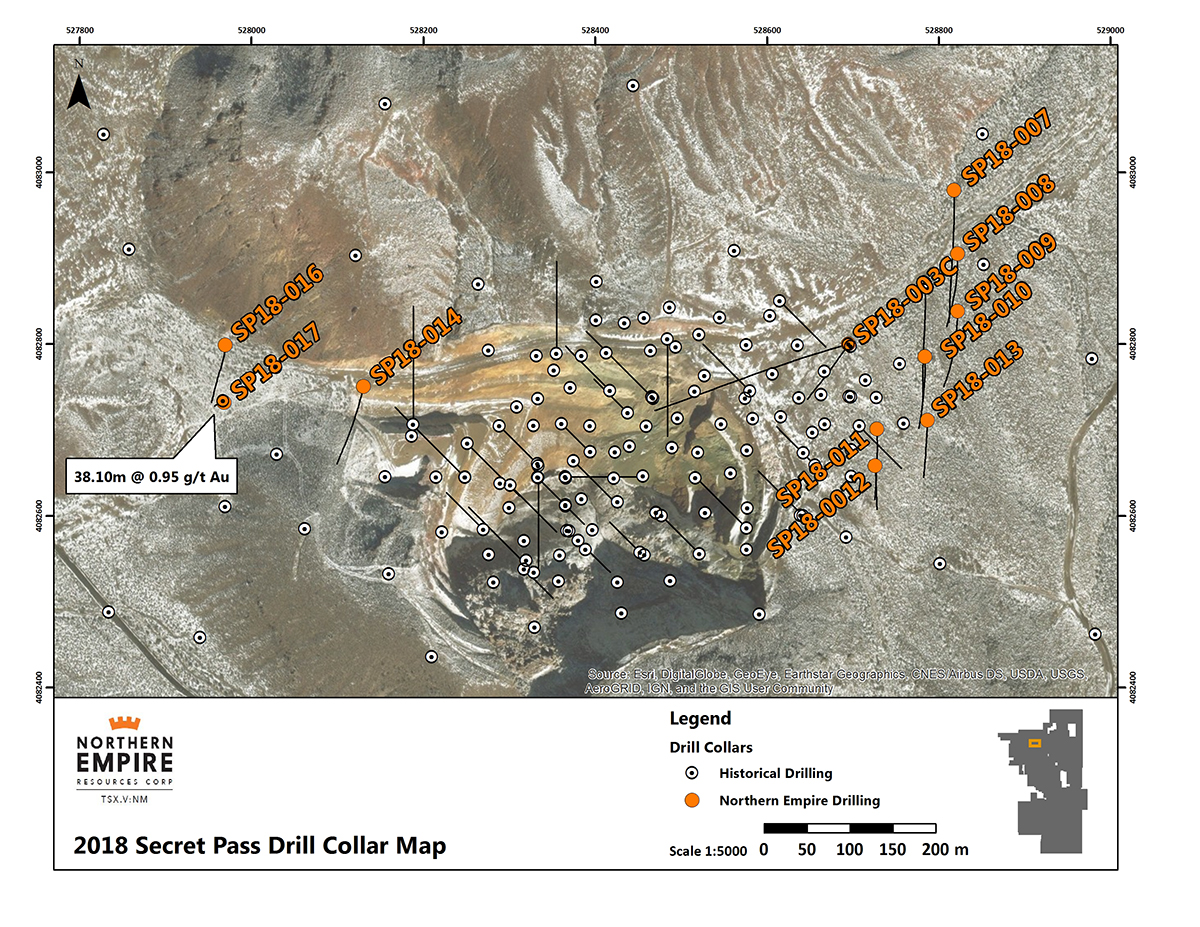

Secret Pass Drilling

The highlighted SP18-017 drill hole stepped out 200m west from the known Secret Pass Deposit and 196.9 meters deep encountered mineralization grading 0.95 g/t gold over 38.1 meters. To note, this hole was terminated before losing mineralization. Northern Empire states within the news release that they intend on re-drilling the hole to better understand the full extent of what has been discovered. This step-out is a great result as it confirms that the Secret Pass Deposit mineralization is open to the west.

Corvus Gold

The last stop of the day was at the SNA Deposit, in the north-east corner of the property. As we approached the SNA Deposit, we first drove past Corvus Gold’s Mother Lode Open Pit, which is completely encompassed by Northern Empire’s Crown Block.

Corvus Gold’s Mother Lode Open Pit

For those who are not familiar, the Mother Lode Deposit has been a major focus for Corvus over the last year, with 10,000m of drilling in 2017 and another 13,000m of drilling planned for the first half of 2018. For those that may not be familiar, Corvus has a MCAP around $300 million, which is largely based on the drilling success at Mother Lode. I find this interesting as a Northern Empire shareholder, because I’m intrigued by the amount of drilling that’s occurring around the existing open pit and, specifically, how that mineralization may extend out toward, or connecting to, the SNA Deposit.

Examining the satellite image below, you can see the concentration of Corvus drill holes not only in the vicinity of the open pit but, more importantly, along the claim boundary.

This is a fairly obvious observation, one that didn’t get past Northern Empire management; while viewing the SNA Deposit during our visit, drilling was taking place along the Corvus claim boundary. In news released April 17th, Northern Empire confirmed that the Mother Lode mineralization does extend south towards the SNA deposit and have drilled significant gold grades from structures which cut favourable host rock for Carlin-type gold mineralization beneath the historic Telluride Mercury Mine.

Northern Empire Drilling beside Mother Lode Open Pit

Concluding Remarks

As I’ve said in the past, site visits are an excellent way for you to bring your due diligence to the next level, and nothing beats seeing the property and interacting with the people in person. My visit to the Sterling Gold Project was no different, as it gave me a better view of the upside potential of the property and the type of people managing the company.

Just to recap, here’s a list of what I see as the strengths for Northern Empire:

Good management team with extensive experience exploring and developing gold projects in Nevada.

The Fraser Institute ranks Nevada 3rd in the world for Mining Investment Attractiveness.

Northern Empire is in possession of all the necessary production permits to restart the Sterling Mine.

The Sterling Mine potential production scenario should be low-cost, as the Carlin Style gold mineralization will be mined from an open pit and is amenable to heap-leaching.

Exploration Potential – The Crown Block, especially, holds a lot of resource expansion potential as it appears all of the existing deposits have the potential to be larger; potentially, one large, shallow and good grade gold system.

18,000 meter drill program underway and a larger 50,000 meter drill program on the horizon as it is currently being permitted!

Existing inferred global resource of 985,000 ounces of gold at 1.29 g/t.

CASH – $16 million!!

I believe there’s a lot of upside potential for Northern Empire if they’re able to execute their plan of expanding the resource at both the Sterling Mine and the Crown Block. I look forward to good news flow over the coming months as this story really begins to come together on the back of their 18,000m drill program.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I do own shares in Northern Empire Resources. All Northern Empire Resources’ analytics were taken from their website and press release. Northern Empire Resources is a Sponsor of Junior Stock Review.

Whether it be financial, political or social, there’s the potential for any decision we make to be fueled by emotion. In particular, when participating in a high risk, high reward area of the market, like the junior resource sector, it can be lethal to your odds of success.

In my experience, those who can use arithmetic as their primary “truth” are the best at eliminating bias and reducing the amount of emotion contained in an investment. Today, I have for you an interview with a man who uses arithmetic to construct, what I believe, is the most compelling argument for gold that I have ever heard.

This man is Trey Reik, a Senior Portfolio Manager with Sprott USA. Reik is a commentator on gold markets and monetary policy, including policies and actions of global central banks, global conditions for money and credit, and factors affecting supply/demand conditions for gold bullion.

I first heard Reik speak at the 2015 Sprott Natural Resources Symposium in Vancouver, British Columbia. From then on, I’ve always paid attention when I’ve heard or seen the name, ‘Trey Reik;’ there’s a lot you can learn from him, especially when it comes to his commentary on gold.

Without further ado, a conversation with Trey Reik.

Enjoy!

Brian: In my view, we live in a society of paradigms or bias that lock us into thought patterns that keep many of us blind to other alternatives – alternatives that may be more efficient or beneficial.

In reference to financial markets and in particular gold, in your opinion, how does one keep an open mind and see through paradigms and their own inherent bias?

Trey Reik: I think that a lot of what’s been going on, at least in markets since the turn of the millennium, so the 2000s, is that we’ve hit a period in which central banking has become probably the most important variable on the investment landscape, and I would add much more important than it should be. This has really cast a prism or a rose-coloured glasses view of what’s really going on in the world. It has, I think, relieved people and investors from reality, to a great degree.

Let me just back up a teeny bit, and talk about it from the perspective of gold. Number one, I’ve given probably 1,000 presentations about gold over the 15 years in which I have been covering it, and I’ve never once convinced anybody to buy gold. I don’t expect to change people’s views today any more than I did yesterday or last month. Number two, gold’s a funny topic because almost everybody has an opinion, generally unburdened by a real strong command of any relevant underlying fundamentals or facts. Third, gold has more investment queues than any other asset with which I’ve been involved over my career.

Some people think it’s an inflation hedge, some people think it’s a deflation hedge. Some people think gold is a risk-on trade, other people would look at it as a risk-off investment. When we have stress in the financial system, some people would view gold as a safe harbour. Other people would still favour the US dollar, although far fewer than would have made that determination say, in 2008. Given the negative reflexive relationship between the dollar and the US gold price, you could actually have a situation where stress in the financial system has a reflexively negative impact on gold.

Now, I went through all of that because my gold thesis is a little different than most. I don’t really think gold has much to do with CPI-type inflation. The way I would pose this is that if the price of hedonically adjusted hot dogs in Houston goes up, why would you buy gold? I don’t really see a strong connection there. Another way to look at inflation is if the prices of goods and services go up for healthy reasons, like a strengthening economy, I’m not really sure the price of gold should go up any faster than say, thumbtacks. If the inflation is of the monetary sort or variety, then I think gold should logically do a lot better.

Now, over the last 17 years, gold is up in 14 of those 17 years and has amassed a compound annual return since year end 2000 through year end 2017 of just about 9.5%. Actually, 9.65%. Over the same 17 years, the compound annual return of the S&P 500, including reinvestment of dividends was 6.32%. Gold has significantly outperformed the S&P with reinvestment of dividends for 17 years and is up in 14 of the 17. Now, if gold is up in 14 of the 17 years, it proves my point that it’s not related to some of these knee-jerk reactions that get ascribed in the press all the time to gold investors. In other words, we’ve had periods of inflation and periods of deflation over that timeframe. We’ve had round trips in equities and commodities. We’ve had yields on both the short end and the long end, largely falling over the timeframe, but we even had periods like June of ’04 to June of ’06 where the Fed raised rates at 17 consecutive FOMC meetings and quintupled the Fed funds rates from one-percent to five-and-a-quarter-percent, and gold went up during that timeframe by as much as 86%.

My point is, for gold to do as well as it has for so long, posting the best performance of any global asset, there’s obviously something more going on. I think what that is, is that at the margin, we have about $280 trillion now in global financial assets, and each year, in my opinion, my thought experiment, if you will, is that a very small portion of that global wealth seeks a home in hard assets, things that can’t be debased or defaulted upon, things that can’t be printed. That’s why fine art, in my opinion, has done so well over a period that has not exactly been exhibiting breakneck growth, but nonetheless, the art market’s been on fire. Things like Honus Wagner baseball cards, fine Bordeaux wines, all that kind of stuff has done really, really well.

Gold has benefited, I think from that migration. Each year, we have a different rate of migration from the financial asset pile to things like gold, and in certain years, that migration may have even reversed, like 2013, for example. The whole gold thesis is about that rate of migration going from say 1/10th of 1% to say, 1/2 of 1% ’cause 1/2 of 1% of $290 trillion is $1.45 trillion. The available gold stock is about $2.8 trillion. $1.5 trillion isn’t going to get into $2.8 trillion without a serious price dislocation.

When you talk about paradigms or things being misleading or that type of thing, although that’s a leading, almost political kind of question, I think the biggest misdirection, I think, of markets is the degree to which certainly over the past three years especially, but over the last 17 years, how big a part of financial asset valuations has become central bank policy.

Now, to back this up to two weeks ago, I think most of the market still believes that this disturbance that we had is–just as when we had the crisis of 2007, ’08, and ’09—the first words out of people’s mouths are always, “It’s contained.” Just as we thought in 2007 that the disturbance was limited to subprime mortgages, we are currently, I think, a large percentage of folks would say that the current disturbance is limited to a very small group of perhaps leverage, but certainly a short bet on the VIX. I look at it very differently. I would suggest that after nine years of ZIRP and QE, but 17 years of egregious central policy and interventions really starting with Mr. Greenspan, the entire financial system has been imbued with this short-volatility way of looking at the world. I’m sure given your situation, that you’ve read Chris Cole’s stuff from Artemis, but he’s the Michael Burry of this trade. You remember Burry was the guy that figured out the subprime-short trade for Scion Capital in the movie The Big Short. Coles is, I think, the Michael Barry of this trade. If you’ve read his stuff, he estimates that there’s about $2 trillion-worth of short-volatility exposures.

He’s got it all broken out in the stuff that he’s written. If you have about $2 trillion of exposures left, we haven’t even really started to scratch the surface of re-pricing things back to reality. I would say that in an environment of 0% interest rates and QE, we’ve lost the ability to assess the demand for anything.

People who laugh or criticize gold, like Warren Buffett–here’s a guy, he’s got more financial assets, paper assets than any other human being on the planet, or I guess Jeff Bezos might be up there with him now.Warren Buffett, who has more to lose from gold doing well than any other person on the planet, and ask him what he thinks about gold? But yet we do. When we do, he says, “Well, if you take all the gold in the world and you fit it on a tennis court, you got this big lump of gold and then in the other, box B, you could have five General Motors or GEs, and all the farmland in America, and you’d still have a trillion dollars leftover. Who wouldn’t pick box B?” The answer is anybody who thinks box A, which is all the gold in the world, is going to go up faster than box B.

We have a system where people think they have these franchises and these moats and all the stuff that Buffett writes about, and impenetrable franchises, but in fact, the denominator of all of these things, the unit of account, even if you’re talking about cash flow, is dollars. The one thing that is not stable as a unit of account is dollars, so no one really has any idea what the value of any of these franchises are.

If we normalized rates, and we took say, Fed funds to, well what’s normal anymore? We took them from 1% to 5.25% as recently as 2006, but if we took them to 4-5%, and we took the 10-year Treasury yield to eight percent, would the financial systems still be intact? I think the answer is no.

Until we can normalize rates, we don’t know what the list of Buffett’s companies–the Nebraska Furniture Mart and Wells Fargo and he just sold his IBMno one knows what the demand for anything is at these companies with this much monetary debasement.

Brian: Since 2008, I have personally suffered from being too pessimistic on paper currencies, mainly the U.S. dollar and risk in the broader market. Depending on perspective, this view both made me and cost me money.

Now, 10 years later, I have taken time to reflect on my investment choices and believe that bias or the so called “gold bug” in me prevented me from having a clearer picture of what was actually happening in the world.

However, I still believe that there is a price to pay for the massive amounts of money printing and low interest rates we have seen over the last 10 years. To me it is a “when” not “if” question.

My question for you is, has the “when” already occurred in the gold market? Meaning, realistically, should investors view the current gold price around $1300 USD/oz as the payback for the QE and low interest rates, or is the “when” still to come?

Trey Reik: I do believe there is no empirical equation that could generate a gold price that really means anything. The gold price is the reciprocal of your comfort with the financial system, the dollar, and central-bank stewardship. If you’re of the opinion as an investor that those three are fine, gold really serves no purpose. If you are like me, of the opinion that all three of those are deeply in doubt, meaning the value of the US dollar, debt levels, central bank stewardship, etc., then gold is a mandatory investment.

It doesn’t really matter if the price is $1,200 or $2,300, if those three issues are still a problem, you need to have gold in your portfolio. That’s what I was saying earlier; I have three litmus tests for when gold is a mandatory portfolio investment. I was sharing the first with you, which is whether you could normalize rates and then you have to decide what normalizing means. Let’s even call it 3% on Fed funds. I don’t think we can get there without a financial calamity or 6-8% on the 10-year Treasury. If you could normalize rates without big impact, gold’s role may have diminished.

The second litmus test would be if we take the ratio of debt-to-GDP, for the last 100 years the ratio of debt-to-GDP in this country has averaged 140-170%, except for two events. The depression and the Alan Greenspan/Bernanke/Yellen era. In the first example, we had GDP fall 50%, the debt remained constant, so the ratio got up to like 260%. FDR had to devalue the dollar and confiscate gold in the US and make it illegal, for what turned out to be 41 years. In the current environment, which is a numerator event, we’re just piling all this debt on top of relatively stable GDP. If we don’t get that debt-to-GDP ratio back to say, 200% from its current level of about 370%, goldwill remain a mandatory investment.

The reason is, that in order to get that ratio back into balance, the only two options are default or debasement. Each time the markets try to choose default, the Fed steps with QE1, QE2, QE3, Operation Twist, etc., and they will again. We’re either going to have 20 trillion or so of credit in the United States go away, or the other way to look at this is household net worth.

In March of 2009, household net worth, which is the Fed’s measure from Z1; basically it’s stocks, bonds, real estate, minus debt. Household net worth in March of 2009 was $54.79 trillion, GDP was $14.09 trillion. Today, household net worth is $96.94 trillion and GDP is $19.5 trillion. GDP has gone up $5.4 trillion from $14.09 trillion to $19.5 trillion, and household net worth over the same time period has gone up $42 trillion from $54 trillion to $96.94 trillion.

This means that over the past—let’s see, March of ’09, and now we’re in March of ’18, so the past nine years, household net worth has grown 7.77 times, or call it eight times faster than GDP growth. Now, the one thing I know for certain is you can’t grow wealth eight times faster than output forever. Once again, is gold necessary? Have we had the ‘when’ yet? Absolutely not. In the household net worth type of multiple to GDP, if you look at the 40’s, the 50’s, the 60’s, the 70’s, everything really through the 80’s, we used to have about a 3.5 times multiple to GDP and savings, is what household net worth should be.

Probably 30, 35, 40 trillion dollars worth of household net worth has to go away to get the system back in balance. This is like litmus test number two. We either need $20 trillion in credit, or $30-35 trillion in the combination of real estate, stocks, and bonds, (minus debt) to go away to bring the system back in balance. Until that happens, I think gold is a mandatory portfolio component because, once again, the only two options are default or debasement.

Then the third litmus test would be if we could get back to some sort of normalized GDP growth, and once again, we’re debating these days what “normal” is. Trends, capability, normal, say 3%, used to be 3.5%. We used to accomplish 3.5% growth with a savings rate, very importantly, in the 8-10% area. That would be healthy growth. It wouldn’t require the non-financial credit expansion that is now necessary to keep the debt pyramid from toppling, which is on the order of $2 trillion a year. Again, to review the three litmus tests would be normalizing rates without crashing the financial system, rationalizing the excess paper claims in the economy, whether it’s debt or the household net worth, and the third would be normalize GDP supported by savings as opposed to non-financial credit creation.

Unless you have basically all of those, or even two out of three, gold is still a mandatory portfolio investment, in my opinion. Which is, by the way, why even though it never gets any accolades, it is the best performing asset and is up in 14 of the past 17 years. That’s going to continue until we get the system in better balance between claims on future output and the future output itself.

Brian: Is there an event or series of events that would have to occur for you to change your mind about the long-term fundamentals of gold?

Trey Reik: One of the reasons that I’m as confident as I am is I’ve spent more time thinking about the underlying fundamentals than most human beings. There’s a lot of people that invest in gold for lots of different reasons, as we already discussed, but I’m not in that group. I’m investing in gold for a very specific tenant, which has to do with monetary variables and the claim on future output. There’s just too much paper claim out there. Until those imbalances are solved, one way or another, and I’m suggesting the only two solutions are default or debasement, there isn’t any other solution.

Well, the third solution would be we grow into it, but in order to grow into it, even if we had GDP at 10% for each of the next eight quarters, it would take GDP from $19.5 trillion to maybe $22 or $23 trillion, and that can’t support $66 trillion of debt any more than $19.5 trillion. Further, if the variables that I just gave you in the last 17 years hold anywhere remotely true, when we get GDP up to $22 or $24 trillion, the debt won’t have remained constant. It would probably be up seven times faster than the GDP growth. You can’t grow out of it, you’ve got to have default or debasement. These imbalances are so profound that I’m not swayed to change my mind at all, even by periods like September 2011 to December 2015, when the high tick for gold was 1911 down to 1050 because these imbalances are still there.

Over the past 17 years, by the way, people always ask when’s gold gonna do its thing? Or why isn’t it doing better?… My response is always, It’s the best performing asset on the planet for 17 friggin’ years. I’ll be fine if gold keeps performing just like this, you know what I mean?

Brian: Yes, absolutely.

Trey Reik: Now, you mentioned the currency thing. I believe all fiat currencies have become an extension of the US dollar. Currency people have to pick one of the seven or five, or however many you want to say there are. That’s a shell game, and that’s all fine. It has gone on much longer than I would have thought possible. It is amazing that 2008 was 10 years ago, and here we are, but things are starting to change.

People talk a lot about the dollar and this is just an interesting thing, if you take the 10 worst market days in each year and you look at those 10 worst market days, you’d have 50 if you looked at five years. From 2008 to 2012, the 50 days when the DOW dropped at least 100 points, the dollar tended to rally on those days. During those days, dollar index rallied 80% of the time and an average 0.6% on these bad days.

Now, if you look at the next five years, from ’13 to ’17, and we look at the 10 worst days for the DOW, the dollar fell on those 50 days an average of .3 and it only rose 26% of the time. What I’m saying here is we are and, by the way, what happened on those 2,000 point days, I think fiat currencies are starting to fail. That’s a bench-clearing statement, but I think it’s true. We are in the early stages of a potential currency collapse, and so we may be getting “there.”

Brian: In your opinion, is the investment thesis for only gold the same as the thesis for only gold mining companies?

Trey Reik: The thesis is the same, but the deployment or the execution is obviously tricky. Gold is the best performing asset on the planet, as I mentioned, since 2000. Gold equities have had three big runs. The three big runs in gold equities were November 2000 to December 2003, , May 2005 to March 2008 and then November 2008 to September 2011.

Now, ironically, each one of the three was within a month or two of exactly three years. I believe that gold equities provide unparalelled alpha when the faith in US financial assets is being recalibrated. We never want to say stocks could go down, so I’ve come up with that phrase.

If we look at November 17th, 2000, through December 2, ’03, the GDX was up 342%, the S&P was down 22%. The next three year period, the GDX was up 185% and the S&P was up 10%. Then, in the third, it was 309% versus 39.70%. Now, if we compound the advance of the GDX in those three periods, which by the way, is nine years out of the past 16 years, it’s a little over 55% of the time you get a compound performance of 5,081.61%. The coincident performance of the S&P, to the day, was 20.39%, which means that gold equities outperformed the S&P by a factor of 249-to-one in nine of the past 16.5 years.

Now, the problem is the corrections between those advances measured negative 36%, negative 76%, and then after the last advance, negative 86%. If you compound those declines, you get basically 98%. That’s why gold equities in December of 2015 were trading below where they were at the end of the first of those three advances, where they were in December of 2003. The GDM in December of 2003 was at 799 and we got down below, I can’t remember the number, but it was much lower than by the end of ’15. Are they motivated by the same investment thesis? Loosely, but the key with gold equities is, as I think you learned after 2016, neither gold nor gold equities are a permanent investment. They serve different roles.

With what we call the jaws-of- life of the inverse correlation between the S&Ps, since October of 2012 through to today, never having been wider. The last time it was this inversely correlated, gold stocks was like 1996 to 2000, and we all know what was happening then. When people get dumb about US financial assets, gold stocks have a tendency to get left for dead. Then, when the inevitable correction comes, and there were two since 2000. The first was 50.5%, second was 57%. As I’ve proved in the prior example, gold stocks have a tendency to provide among the best alpha available in any asset class.

While I think it’s been necessary to have a good bullion allocation consistently in the last several years, I think that now would be an example of the time period where it’s also incumbent to have a representation in the equities themselves. It’s because of the alpha provided if we have one of these recalibrations of faith in US financial assets, and secondly, simply because of the inverse correlation, which has opened to such an egregious degree between the S&P and gold equities.

Brian: It has been a pleasure Trey, thank you very much for taking the time to answer my questions!

Concluding Remarks

The world’s politicians and a good portion of the mainstream media would have you believe that the actions carried out by the world’s central banks, mainly QE and low interest rates, saved us from the depths of what could have been a much worse situation in 2008. In my opinion, this couldn’t be further from the truth. While, it has taken longer than I have expected, there will be a price to pay for this poor monetary policy and, unfortunately, for those who are blissfully unaware, they will be rudely awakened, one day, when the market re-adjusts.

In my discussion with Reik, he cited three Litmus tests which can be used to gauge whether gold is currently a mandatory investment within your portfolio. Ask yourself:

First, is it possible to normalize interest rates?

Second, can the debt to GDP ratio be reduced back to historical norms?

Third, is it possible to get back to normalized GDP growth?

If you can honestly answer even one of these questions with a ‘yes,’ first, I’m surprised and, second, maybe gold isn’t a good investment choice for you. In my mind, Reik presents a compelling thesis for the investment in gold and gold equities, making it a “when” not “if” investment choice for your portfolio.

For those interested in purchasing the physical metal, yet would prefer the convenience of purchasing it through the stock market, I highly suggest checking out the Sprott Physical Gold Trust, which is traded on the NYSE under the ticker PHYS, or the Sprott Physical Gold and Silver Trust on the TSX under the ticker CEF.

The Sprott Trusts offer a few advantages. First, they differ from bullion funds, in that all of the bullion owned by the trusts is held in the trusts’ allocated accounts in physical form. Second, all of the Trusts’ bullion is stored at the Royal Canadian Mint, a Federal Crown Corporation of the Government of Canada. Thirdly, for U.S. non-corporate investors who hold units for more than one year and make a timely Qualified Election Form submission, gains realized on the sale of the Trust’s units are currently taxed at the long-term capital gains rate versus the maximum applied to most precious metals ETFs and physical gold coins.

Additionally, I highly suggest following Reik’s market commentary by subscribing to Sprott’s Thoughts, one of the best sources of financial commentary in the resource sector. Also, I highly suggest attending the Sprott Natural Resource Symposium in July, where you will be able to see and listen to Reik in person, along with a fantastic group of speakers which includes Rick Rule, Doug Casey, and James Grant, to just name a few. I hope to see you there!

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company(s) and sector that is best suited for your personal investment criteria. Junior Stock Review does not guarantee the accuracy of any of the analytics used in this report.

If you’re looking to take your due diligence process to the next level, you have to incorporate a site visit into your repertoire. All the analysis in the world can’t replace the effectiveness of seeing a project and meeting the people in person.

Not only can you confirm what the management team is telling you, but you can meet the people who are on the front lines, mining underground, driving loaders, collecting soil samples or simply answering the phone in the office. All of this can tell you a lot about the health of a company and how it treats its employees, which is paramount to the company’s success, in my opinion.

In October, I had the opportunity to visit Anaconda Mining’s Point Rousse Project, and was not surprised to see that Anaconda’s leadership makes it a priority to empower their workforce. For this, they’re paid back through a motivated workforce.

I returned from my visit to Newfoundland and Labrador very satisfied that Anaconda’s operational team has the right ingredients for success; they look set to put the Stog’er Tight Deposit into production, produce a maiden resource estimate for the Argyle Zone, and explore and develop the Goldboro Project toward production.

2018 looks to be a monumental year of growth for Anaconda, one that I look forward to as a shareholder!

Anaconda Mining – Site Visit October 2017

On the morning of October 22nd, I flew out of Toronto’s Pearson International Airport on my way to Deer Lake, located in western Newfoundland and Labrador. While I was here, I had the opportunity to visit Anaconda Mining’s Point Rousee Project, located on the Baie Verte Peninsula in north western Newfoundland and Labrador.

Gros Morne National Park – Western Brook Trail

The western portion of the island of Newfoundland, while sparsly populated, possesses, in my opinion, some of Canada’s most spectacular scenery and destinations. I landed in Deer Lake, an interesting town because it’s home to western Newfoundland and Labrador’s major airport, and compared to many of the other areas in this part of the island, it’s also well developed on a commerical level.

Most importantly, however, it’s the largest centre next to Gros Morne National Park, and acts as a jumping point for people looking to explore this UNESCO world heritage site.

On the last day of my trip, I spent the day hiking a few of the trails in Gros Morne and was amazed by the scenery – this is a place you will want to add to your bucket list, you won’t be disappointed!

Baie Verte, Newfoundland and Labrador

Baie Verte – HWY 410 thru the main part of town

Baie Verte – A view from Bistro on the Bay

Baie Verte is a small town located on the coast of the Baie Verte Peninsula. Baie Verte’s history as a town is rooted in the pulp and paper industry, but owes its major growth to the asbestos mine which was founded in 1955 by George McNaughton and Norman Peters.

Asbestos Open Pit Mine – 1963 to 1995

The open pit asbestos mining operation, which is located a short drive north of Baie Verte, employed 500 people at its peak. The mine was operated by a number of companies throughout its history, including Advocate Mines Ltd., Baie Verte Mines Inc., and Teranova. The mine was closed permanently in 1995.

While there are other employers in this region of Newfoundland, I definitely got the feeling from speaking to a few of the residents that, outside of being employed by government, mining was the most desirable industry in which to work.

The mining operations that are closest to Baie Verte are Anaconda Mining’s Point Rousse Project and Rambler Metals and Mining’s Ming Mine and Nugget Pond Mill. The two companies, in total, employ roughly 400 people in the surrounding area.

Depending on your speed, it’s roughly a 2 hour drive from the Deer Lake airport to Baie Verte. I spent two days in Baie Verte, staying at the Dorset Inn, which is right in the heart of town. From here, Anaconda’s Point Rousse Project is about a 30 minute drive on the 418, which leads to the town of Ming’s Bight.

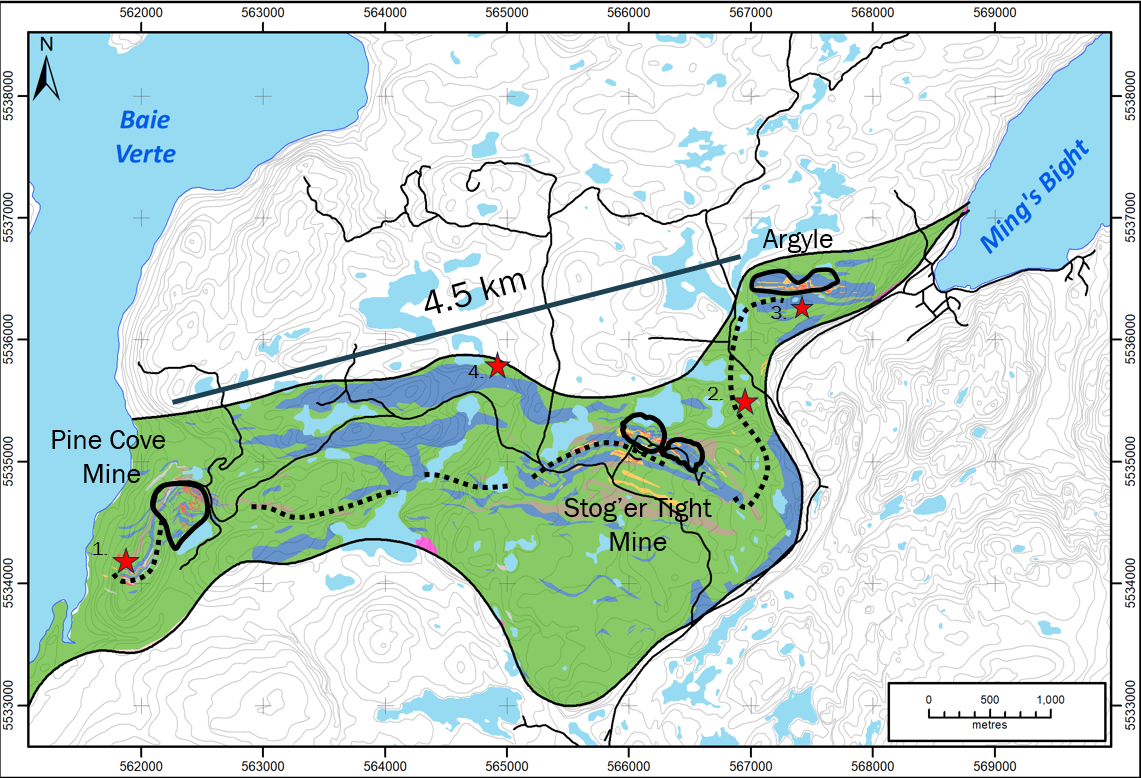

The Point Rousse Project

The Point Rousse Project is a collection of Anaconda’s Newfoundland assets, which include the Pine Cove Mine and Mill, the Stog’er Tight Deposit, the Aggregates Project and over 5,800 ha of prospective property.

The Point Rousse Project is located down a very well kept gravel road, about 5 km off the 418. The road makes its way through the forest, up and down hills, until reaching the site’s main offices to your left, and tailings pond to your right. Elevation-wise, the main offices, mill and tailings pond are set roughly 75 to 100 ft above the top of the Pine Cove open pit, and probably another 75 to 100 ft above the sea level at the Port Facility.

During my visit, I was accompanied by the Mine and Mill Superintendent, Tony Chislett. Chislett has been with Anaconda for 10 years, working in a few different roles before becoming Superintendent. In my experience, the best operation managers typically work their way up to the position after having extensive experience in the various jobs that they are going to manage. This not only gives them the much needed knowledge of the process, but also the respect of the workers.

Chislett and his team will be put to the test in the coming months with the conversion of the Pine Cove open pit mine to a long term tailings facility and the start up of the Stog’er Tight Mine, which should occur in early 2018. Not only this, but on the horizon there is the possible processing of the Goldboro ore, which will be an extra wrinkle for the team to deal with, as the Goldboro ore is different from what is mined along the Scrape Trend.

Pine Cove Mine and Mill Superintendent, Tony Chislett

As we drove around the property, Chislett gave me a break down of the operation, and how they have incorporated cutting-edge technology and their personnel’s input to improve the process. For instance, GPS targeting for blasting and on the company’s heavy equipment allows for precision mining and the ability to maximize efficiency with the flow of ore to and from the open pit to the mill. With the movement to Stog’er Tight getting closer, these technologies, I believe, will aid Anaconda in avoiding some of the pitfalls that could accompany the mining operation’s move.

Pine Cove Open Pit Mine– Dump Truck Driving Up the Ramp

Pine Cove Open Pit Mine – Mining of Gold Ore from the Bottom of the Pit

Stog’er Tight Deposit – Located in Close Proximity to the Pine Cove Mill

Scrape Trend

While the Stog’er Tight Deposit looks to become Anaconda’s next producing asset, there are many more prospective targets located in what is called the Scrape Trend.

Source: Anaconda Mining

In the image above, you can see the exploration targets listed from 1 to 4. Starting on the left-hand side of the image with #1, is Anaroc, which is located in close proximity to the Pine Cove open pit mine. Next, #4 is Corkscrew Road, followed by the #2 Connector and, finally, #3 the most explored of the targets, the Argyle Zone.

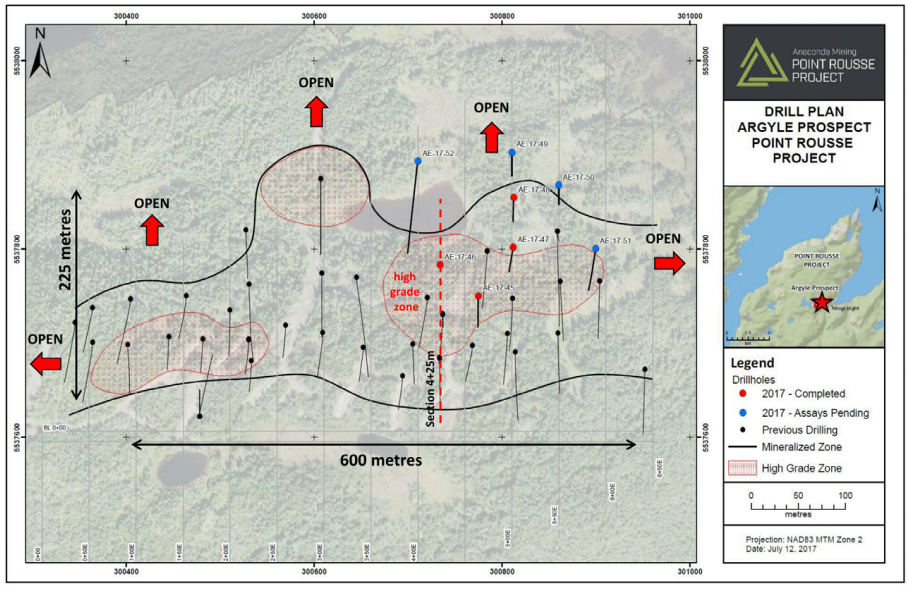

Argyle Zone

Fifty-two holes have been drilled at the Argyle Zone, totalling 4,860 meters. The strike length is over 600m and 225m down dip. To date, here are some of the drill highlights at the Argyle Zone: 6.09 g/t over 8.9m (AE-16-11), 9.31 g/t over 6.0m (AE-16-39) and 3.63 g/t over 12.0m (AE-17-46).

In a recent news release, Anaconda announced a flotation recovery of 97.3% and a leach recovery of 94.5% for a combined recovery of 91.9% of a 25 kg sample of blended core samples from Argyle, with an average grade of 2.69 g/ton gold.

Additionally, Anaconda’s geologists have identified other targets to the south and along strike using geophysical data.

Source: Anaconda Mining

PUSH: A maiden resource estimation for the Argyle Zone is expected to be announced in December 2017. Additionally, Anaconda’s team is working on an environmental assessment application, conducting metallurgical and ARD testing and government consultations.

Aggregates Project

Deep Sea Port which Facilitates the Aggregate Shipments

While not a focus for Anaconda, the cash and the removal of waste rock that the Aggregates Project provides is a huge plus for the company. The Aggregates Project and the proposed use of some of the larger waste rock as armour stone is a testament to the innovation that Anaconda’s leadership has instilled in their workforce.

With the first Aggregates Project contract having just expired, Chislett mentioned that they intend to negotiate additional contracts in the future. In the last fiscal year ending on May 31 2017, the project generated $0.9 million.

The Goldboro Project

From the first time we met, Anaconda’s CEO, Dustin Angelo, has told me that Anaconda has lofty goals for expansion, as they intend on becoming a 50,000 ounce per year gold producer. To more than triple their current production rate, they will, without a doubt, lean heavily on their latest acquisition, the Goldboro Project, which is located a couple of hours northeast of Halifax, Nova Scotia.

In recent news, Anaconda was able to raise $3 million dollars in a non-brokered private placement. VP of Exploration, Paul McNeill, says roughly half will be put toward further exploration and development at Goldboro.

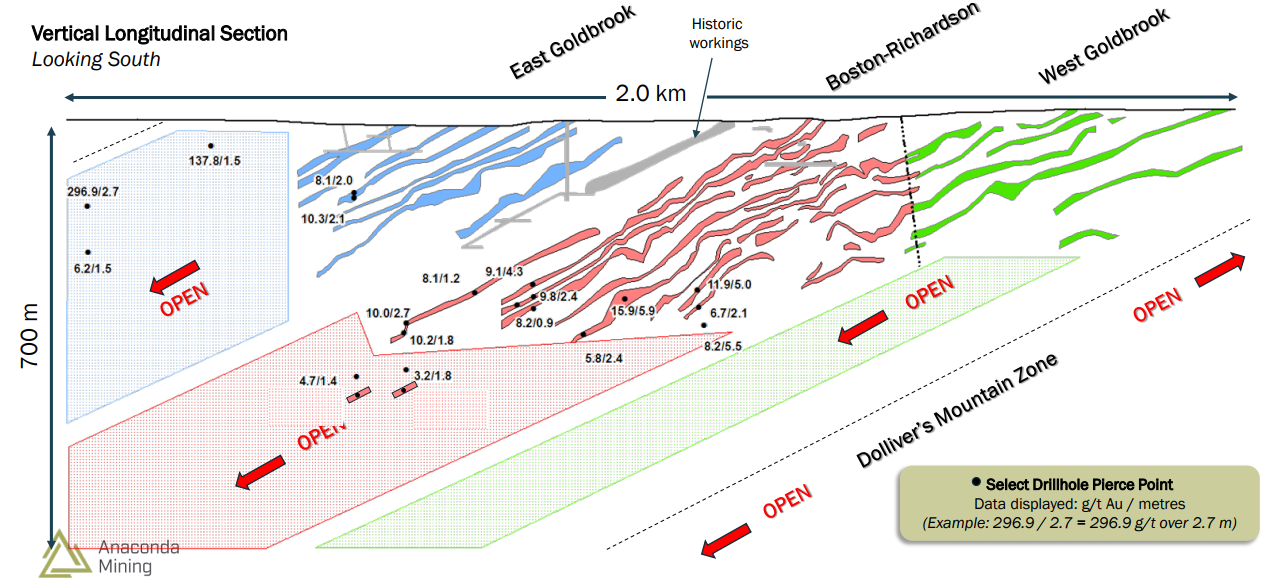

In a news release on November 1st, Anaconda announced a 6,000m diamond drill program, focusing on the Boston Richardson and East Goldbrook gold systems. The goal of the program is to expand the mineral resource along strike and down plunge, while also completing infill drilling in specific portions of the deposit as they look to move some of the Inferred resource up to the Measured and Indicated categories.

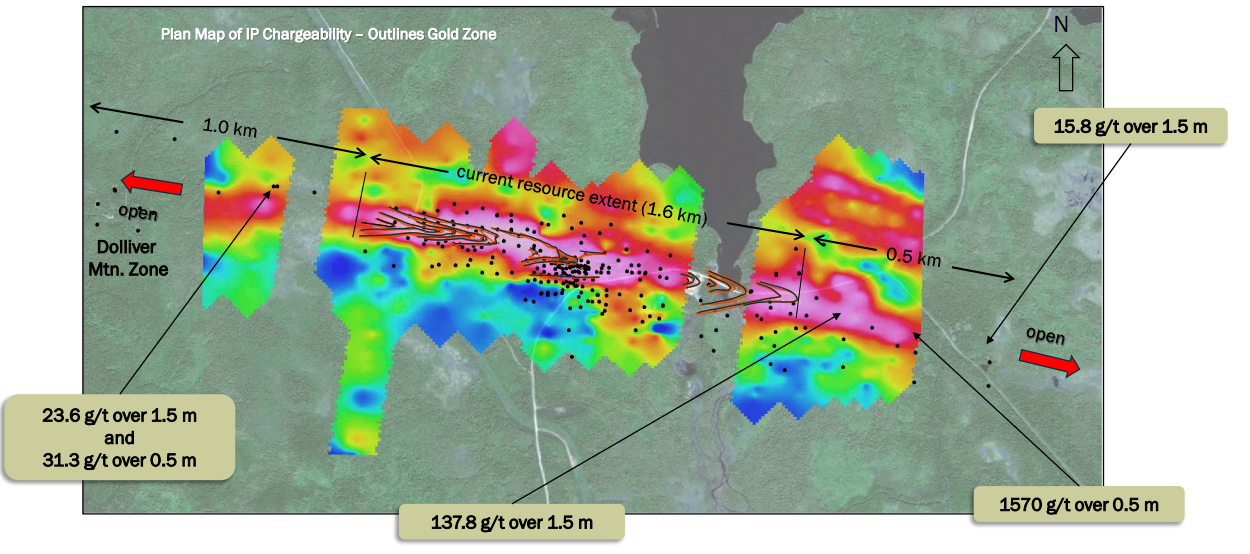

Goldboro IP Chargeability Map

In the same release, Anaconda reported that initial drill core observations support the thesis that the Goldboro Deposit continues at depth, as the first diamond drill hole (BR-17-06) intersected the geological structure hosting the Boston Richardson System between 400 to 475 meters, which is 75 meters below the current resource model.

Goldboro Deposit Vertical Longitudinal Section

PUSH: Drill results from the recently commenced 6,000m diamond drill program. Expansion of the resource at depth and along strike has the potential to do great things for the economics of this project. Pay close attention to drill results coming in the weeks and months ahead.

PUSH: Additionally, a PEA is scheduled to be completed by the end of this year, the economics of which could be enhanced with further expansion of the Goldboro Deposit.

Anaconda possesses a proven team with a track record for success in mining. I believe that Goldboro will be the next feather in their cap, as they look to develop the Project into a producing mine. For a detailed look at Anaconda, check out my last article here.

Concluding Remarks

Before my visit, I felt the future was very bright for Anaconda. After seeing their Point Rousse Project in person, I’m convinced Anaconda is a company that is dedicated to empowering its people. It has not only survived the depths of the recent bear market, but has emerged in this new gold bull market as a premier gold producer, set to grow in the coming years.

I’m looking to add to my position in Anaconda in the weeks ahead, and see weakness in the share price as an opportunity. Putting it all together, there’s a lot of news flow to watch for in the coming weeks and months, which could provide some PUSH for the stock price:

Results from the 6,000m diamond drill program at the Goldboro Project. They are looking to expand along strike and at depth.

Completion of a PEA on the Goldboro Project by the end of 2017

Stog’er Tight Deposit will begin production in early 2018

Maiden Resource Estimation announcement on the Argyle Zone in December 2017

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company(s) and sector that is best suited for your personal investment criteria. Junior Stock Review does not guarantee the accuracy of any of the analytics used in this report. I do own Anaconda Mining Inc. shares. Anaconda Mining Inc. is a Sponsor of Junior Stock Review.

Sterling Gold Project Mineralization – Core Shack

Sterling Gold Project Mineralization – Core Shack

Follow us on Twitter

Follow us on Twitter Become our facebook fan

Become our facebook fan